Reports

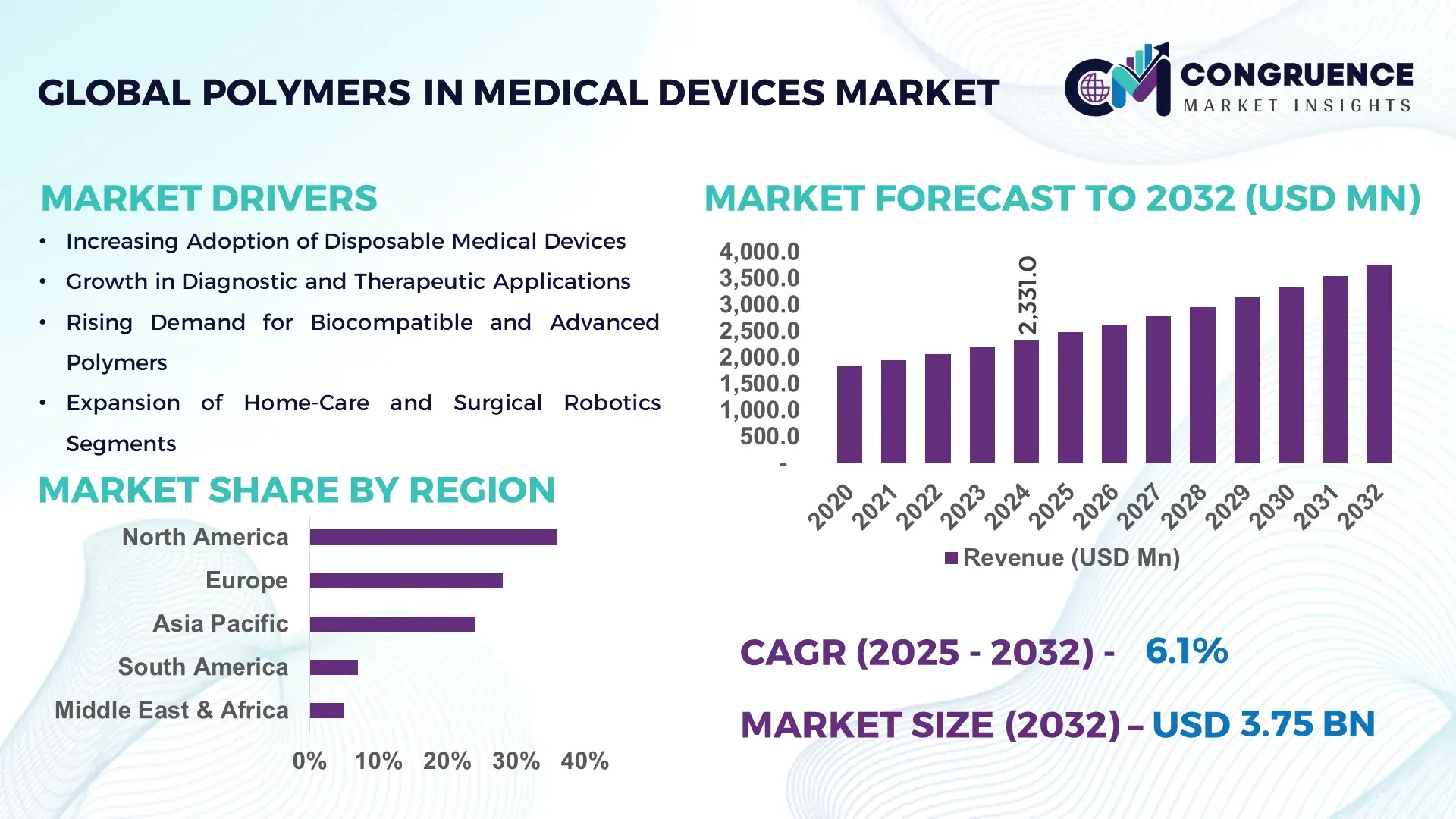

The Global Polymers in Medical Devices Market was valued at USD 2,331.0 Million in 2024 and is anticipated to reach a value of USD 3,754.7 Million by 2032 expanding at a CAGR of 6.14% between 2025 and 2032, according to an analysis by Congruence Market Insights. The growth is driven by the rising demand for lightweight, biocompatible, and durable materials in medical applications.

The United States dominates the Polymers in Medical Devices Market with advanced manufacturing infrastructure and robust R&D investments. The country houses over 70% of North American polymer processing facilities dedicated to medical-grade polymers. Investment in new extrusion and molding technologies exceeded USD 450 million in 2023 alone. Key applications include cardiovascular devices, orthopedic implants, and diagnostic instruments, supported by high adoption rates of bioresorbable polymers and advanced copolymer blends. Consumer adoption is significant, with over 60% of healthcare providers integrating polymer-based disposable devices into daily clinical procedures.

Market Size & Growth: Valued at USD 2,331.0 Million in 2024; projected to reach USD 3,754.7 Million by 2032; driven by increasing demand for biocompatible polymers in healthcare.

Top Growth Drivers: Rising adoption of disposable devices (48%), innovation in bioresorbable polymers (35%), and efficiency improvements in polymer processing (30%).

Short-Term Forecast: By 2028, production efficiency in extrusion and injection molding is expected to improve by 22%.

Emerging Technologies: Bioresorbable polymers, nanocomposite polymers, and 3D printing in medical device prototyping.

Regional Leaders: North America (USD 1,120.0 Million), Europe (USD 980.0 Million), Asia-Pacific (USD 850.0 Million) by 2032; Europe leads in sustainable polymer adoption, North America in innovative device integration, Asia-Pacific in cost-effective production.

Consumer/End-User Trends: Hospitals and outpatient clinics increasingly prefer single-use polymer devices; 58% of end-users prioritize infection control and sterilization ease.

Pilot or Case Example: In 2023, a U.S.-based medical device manufacturer achieved 15% production downtime reduction by integrating automated polymer molding lines.

Competitive Landscape: Market leader: Medtronic (~18% share); major competitors include Abbott Laboratories, B. Braun Melsungen AG, Smith & Nephew, and Boston Scientific.

Regulatory & ESG Impact: Stringent FDA and ISO 13485 compliance; ESG initiatives include polymer recycling programs targeting 20% waste reduction by 2026.

Investment & Funding Patterns: Over USD 500 Million invested in polymer innovation and production facility upgrades; venture funding in polymer-based bioresorbable technologies has increased 28% in 2023.

Innovation & Future Outlook: Integration of nanocomposite polymers in implants, 3D-printed polymer devices, and smart polymer coatings for enhanced antimicrobial performance.

Polymers in Medical Devices are increasingly used across cardiovascular, orthopedic, and diagnostic segments, contributing to over 60% of global usage. Recent innovations include nanocomposite coatings, bioresorbable stents, and additive manufacturing for customized implants. Regulatory compliance, environmental considerations, and rising adoption of single-use devices are driving growth, particularly in North America and Europe, while emerging markets show rapid uptake of cost-effective polymer devices.

The Polymers in Medical Devices Market is strategically pivotal due to its role in enabling high-performance, biocompatible, and cost-effective medical solutions. Advanced thermoplastic polyurethane (TPU) delivers 12% better elasticity and sterilization resistance compared to conventional polycarbonate materials. North America dominates in volume, while Europe leads adoption with 62% of hospitals and outpatient centers integrating advanced polymer devices. By 2027, 3D-printed polymer implants are expected to reduce prototyping time by 40%, while bioresorbable polymers can decrease long-term device complications by 25%. Firms are committing to ESG improvements, targeting 20% polymer waste reduction by 2026 through recycling and sustainable sourcing. In 2023, Medtronic achieved a 15% reduction in production downtime via AI-driven polymer molding line optimization. Looking forward, the Polymers in Medical Devices Market will remain a cornerstone for sustainable, high-performance, and compliant medical solutions globally.

The Polymers in Medical Devices Market is experiencing significant transformation driven by technological advancements, increasing healthcare expenditures, and the need for lightweight, durable, and biocompatible materials. Innovations in polymer chemistry, additive manufacturing, and sterilization techniques are reshaping production and design standards. Demand is rising for applications in cardiovascular, orthopedic, diagnostic, and single-use devices. Regulatory frameworks and ESG initiatives are influencing material selection, encouraging biodegradable, recyclable, and low-toxicity polymers. Consumer trends emphasize patient safety, infection control, and minimally invasive devices, increasing the adoption of advanced polymers across both developed and emerging markets.

The surge in single-use medical devices has significantly driven the demand for polymers. Hospitals and clinics increasingly adopt disposable devices to reduce infection risks and enhance operational efficiency. In 2023, over 58% of U.S. hospitals reported a shift to polymer-based single-use surgical instruments and diagnostic tools. Innovations in bioresorbable polymers and lightweight thermoplastics allow for high-performance, sterilizable, and cost-effective solutions, making polymers a preferred choice for disposable applications. Manufacturers are expanding polymer processing capabilities, investing in extrusion and injection molding technologies to meet growing production demands.

Strict regulatory requirements from the FDA, ISO, and CE standards pose challenges for polymer-based medical device manufacturers. Each polymer type requires rigorous testing for biocompatibility, sterilization stability, and long-term safety. For instance, polycarbonate and polyurethane devices must undergo extensive validation for toxicity, leachables, and mechanical performance. Compliance timelines and documentation requirements increase production costs and delay product launches. Additionally, the integration of new polymer materials, such as nanocomposites and bioresorbables, necessitates additional approvals, limiting rapid adoption despite high market demand.

Personalized medicine offers substantial growth potential for polymer-based devices. Additive manufacturing enables customized implants and patient-specific surgical guides, increasing clinical efficacy. In 2023, 3D-printed polymer orthopedic implants demonstrated a 40% reduction in production time while enhancing patient outcomes. Bioactive polymer coatings and nanocomposite blends allow device functionalization tailored to individual patient needs. Emerging technologies, such as smart polymers with antimicrobial or drug-eluting properties, open new avenues for innovation, particularly in cardiovascular and orthopedic applications.

Fluctuations in raw material prices, coupled with the cost of high-purity medical-grade polymers, challenge manufacturers. Polyurethane, polycarbonate, and silicone-based materials require stringent quality controls, increasing production expenses. Supply chain disruptions for specialty monomers have led to delays in manufacturing and higher procurement costs. Energy-intensive processing methods, such as injection molding and extrusion, add operational costs. Companies must balance material quality, regulatory compliance, and cost efficiency while maintaining production capacity to meet growing global demand.

Rising Demand for Bioresorbable Polymers: Adoption of bioresorbable polymers in stents and implants has increased by 38% globally, driven by enhanced patient safety and reduced post-operative complications.

Integration of 3D Printing: 3D-printed polymer devices are increasingly used in orthopedic and dental applications, reducing prototype development time by 40% and improving design customization.

Nanocomposite Polymers for Implants: Advanced nanocomposite polymer coatings enhance mechanical strength and antimicrobial properties. Over 25% of new cardiovascular devices in 2023 integrated such coatings.

Sustainable and Recyclable Polymers: Eco-friendly polymers with recyclability are being adopted in Europe and North America. Approximately 22% of new disposable medical devices in 2023 used recyclable polymer materials, supporting ESG initiatives.

The Polymers in Medical Devices Market exhibits a diversified segmentation structure across types, applications, and end-users, reflecting the industry’s evolving technological landscape. Material preferences are shifting toward high-performance polymers that exhibit biocompatibility, chemical stability, and suitability for minimally invasive procedures. Application-wise, the demand spans disposable instruments, implants, diagnostic systems, and advanced drug-delivery mechanisms, each driven by adoption trends in major healthcare systems. End-user insights indicate strong penetration in hospitals, specialty clinics, and ambulatory centers, with usage patterns aligning with rising infection-control protocols and procedural efficiency needs. Collectively, these segments illustrate a dynamic, innovation-driven market with distinct demand clusters shaped by clinical priorities and regulatory pathways.

The market encompasses several polymer categories, including polyethylene (PE), polypropylene (PP), polyvinyl chloride (PVC), polystyrene (PS), polycarbonate (PC), silicone-based polymers, and thermoplastic elastomers (TPE). Among these, polyethylene leads with a 29% share, supported by its high biocompatibility, flexibility, and suitability for disposable medical components such as tubing and connectors. Polypropylene follows closely due to its chemical resistance and widespread use in syringes and diagnostic housings. In comparison, silicone-based polymers currently account for 22% of adoption, while polycarbonate holds 18%, but thermoplastic elastomers are growing fastest, with adoption projected to surpass 26% by 2032, driven by their usability in soft-touch surgical instruments, catheter components, and ergonomic device interfaces. TPE also represents the fastest-growing segment, supported by a CAGR of 7.2%, attributed to increasing demand for flexibility, patient comfort, and compatibility with advanced molding techniques. Other segments—such as PVC, PS, and specialty copolymers—hold a combined 31% share, serving niche requirements in blood bags, diagnostic cartridges, and transparent housings. Technological advancements in medical-grade compounding and sterilization compatibility continue to strengthen their relevance.

Polymer usage in medical devices spans implants, diagnostic equipment, disposables, therapeutic devices, and drug-delivery systems. Disposable medical devices lead with a 38% share, due to increasing emphasis on infection control and hospital safety protocols. In comparison, diagnostic applications account for 27% of adoption, while implantable device applications hold 21%, but drug-delivery systems are growing fastest, expected to exceed 28% penetration by 2032, supported by advances in polymer-based microencapsulation and sustained-release platforms. The drug-delivery segment also exhibits the fastest-growing trajectory, supported by a CAGR of 7.5%, as polymer formulations enable high precision, controlled dosing, and reduced toxicity. Other application areas—including wound-care systems, rehabilitative products, and surgical robotics—collectively form the remaining 14%, showing steady demand in specialized healthcare settings. Consumer adoption trends reinforce this: In 2024, more than 41% of hospitals globally initiated pilots integrating polymer-based disposable surgical kits, while over 55% of outpatient centers increased their dependence on polymer diagnostic consumables due to efficiency and sterility advantages.

End-users include hospitals, specialty clinics, ambulatory surgical centers, and diagnostic laboratories. Hospitals lead with a 46% share, driven by high procedure volumes and extensive utilization of polymer-based disposable and implantable devices. In comparison, specialty clinics account for 28% of adoption, while ambulatory surgical centers represent 18%, but diagnostic laboratories are growing fastest, with adoption expected to surpass 24% by 2032, supported by a CAGR of 7.8% linked to increasing use of polymer-based consumables for automated analyzers and high-throughput testing systems. Other end-users—such as home-care setups and research institutions—comprise the remaining 8%, benefiting from miniaturized polymer-based devices and point-of-care innovations. Industry adoption metrics continue to rise: In 2024, more than 35% of healthcare networks in Asia expanded use of polymer-based catheter systems, while nearly 48% of North American outpatient centers incorporated polymer-enhanced minimally invasive devices to improve patient recovery times.

North America accounted for the largest market share at 36% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.8% between 2025 and 2032.

The market landscape shows strong regional disparities rooted in healthcare expenditure, manufacturing capabilities, and regulatory environments. North America leads due to its advanced medical device production ecosystem, representing over one-third of global consumption of high-grade polymer-based components. Europe follows with an estimated 28% share, driven by strict medical-grade material compliance and growing demand for sustainable polymers. Asia-Pacific holds around 24% and continues accelerating due to rapid hospital infrastructure expansion, with China and India collectively accounting for more than 55% of regional usage. South America and the Middle East & Africa collectively contribute approximately 12%, supported by rising imports of polymer-based disposables and gradual local manufacturing upgrades. These regional variations shape procurement, innovation intensity, and end-user demand patterns.

North America accounted for approximately 36% of the global polymers in medical devices market in 2024, supported by strong demand across the healthcare, diagnostics, and minimally invasive surgical device industries. The region benefits from a mature regulatory ecosystem, with continuous updates in material safety standards that encourage the use of biocompatible and high-performance polymers. Growth is further driven by digital transformation trends, including the integration of polymer-based components in smart wearables, connected diagnostic devices, and personalized healthcare solutions. Local industry players continue to expand material innovation; for example, a leading U.S.-based polymer solutions company recently commercialized a novel medical-grade thermoplastic designed for next-generation vascular devices. Consumer behavior in the region reflects high adoption of technologically advanced medical products, with over 60% of healthcare providers prioritizing devices with enhanced durability and ergonomic polymer-based designs. This environment positions North America as a hub for early adoption and product standardization across the industry.

Europe represented nearly 28% of the global market in 2024, with Germany, the UK, and France collectively accounting for more than 65% of regional demand. The region’s strong focus on compliance, safety, and sustainability drives increased adoption of advanced polymers, especially in wound care, orthopedic devices, and high-precision diagnostics. European regulatory bodies emphasize stricter material validation, pushing the market toward eco-efficient and recyclable medical polymers. Emerging technologies such as additive manufacturing and micro-molding are being aggressively adopted to improve device performance. A leading manufacturer in Germany recently expanded its production of specialty polymer coatings for cardiovascular devices, reinforcing regional competitiveness. Consumer behavior trends show significantly higher acceptance of ethically sourced and environmentally aligned medical materials, with over 55% of healthcare procurement teams favoring polymer-based devices with sustainability credentials. This regulatory and innovation-driven environment continues to strengthen Europe’s position in the global industry.

Asia-Pacific holds an estimated 24% of global market volume and ranks as the fastest-expanding region in terms of adoption. China, India, and Japan collectively account for over 70% of regional consumption, driven by large patient populations, expanding healthcare infrastructure, and increasing domestic medical device manufacturing. The region is experiencing a rapid shift toward high-precision polymer components in diagnostic equipment, IV systems, and wearable health devices. Innovation hubs in China and Japan are accelerating the integration of advanced biomaterials and lightweight polymers in surgical and implantable products. A major Japanese manufacturer recently invested in next-generation polymer blends for high-durability catheters, reinforcing regional technological strength. Consumer behavior in Asia-Pacific highlights strong preference for cost-efficient, high-performance disposable devices, with mobile health applications and e-commerce platforms accelerating access across urban and semi-urban markets. These structural changes collectively enhance the region’s growth trajectory.

South America contributes close to 7% of the global market, led primarily by Brazil and Argentina, which together account for over 65% of regional demand. The region’s market is supported by growing investments in healthcare infrastructure and a rising shift toward polymer-based disposables for infection prevention and cost efficiency. Modernization of hospital networks and public health programs continues to increase the need for lightweight, durable, and sterilization-friendly materials. Trade policies encouraging imports of advanced medical components are also accelerating market penetration. A notable Brazilian medical supplier recently expanded its distribution of polymer-based surgical kits, improving access in secondary healthcare centers. Consumer behavior trends indicate rising reliance on localized languages and compatibility features for diagnostic devices, aligning with evolving patient engagement standards. These factors collectively enhance South America’s adoption of medical polymers.

The Middle East & Africa region accounts for approximately 5% of global demand, with the UAE, Saudi Arabia, and South Africa driving more than 60% of regional consumption. Demand is shaped by rapid modernization of healthcare facilities, increasing imports of medical polymers, and expanding use of advanced materials in diagnostic, dental, and surgical devices. Governments across the region are strengthening medical manufacturing capabilities through strategic partnerships and investment incentives. A notable UAE-based medical products firm has recently launched new polymer-based consumables to support hospital sterilization programs. Consumer behavior is shifting toward higher acceptance of technologically enhanced diagnostic devices, influenced by rising awareness and digital health expansion. Infrastructure upgrades, combined with growing emphasis on quality compliance, continue to support increased adoption of medical-grade polymers.

United States – 28% Market Share: Leads due to its advanced medical device manufacturing ecosystem and strong adoption of high-performance medical polymers.

China – 18% Market Share: It ranks second owing to large-scale production capacity, expanding domestic healthcare infrastructure, and increasing integration of polymer-based components in mainstream medical devices.

The global Polymers in Medical Devices market exhibits a moderately consolidated yet competitive structure, with approximately 100–120 active suppliers worldwide. The top five companies account for roughly 20% of the overall market, while the remainder is highly fragmented among regional and specialty material providers.

Major companies such as BASF SE, DuPont, Evonik Industries, Celanese Corporation, and DSM Biomedical continue to strengthen their positions through expansion of medical-grade polymer production capacity, acquisitions, and launch of advanced bioresorbable or eco-friendly polymer materials. Companies are expanding global supply networks and enhancing specialty compounding capabilities to better serve device OEMs.

Innovation trends — including bioresorbable polymers, antimicrobial elastomers, sustainable polymer grades, and recyclable medical plastics — are intensifying competition. Smaller specialized manufacturers are also entering the market with custom polymer grades tailored to niche applications, adding to fragmentation. As demand grows across disposables, implantables, diagnostics, and wearable devices, competition will remain dynamic.

Celanese Corporation

DSM Biomedical

SABIC

Eastman Chemical Company

The industry is undergoing significant transformation driven by material innovation and evolving regulatory expectations. Bioresorbable polymers have emerged as a major focus area because they dissolve naturally inside the body, eliminating secondary surgeries. These materials are increasingly used in implants, sutures, orthopedic devices, and drug-delivery systems.

High-performance thermoplastics and elastomers are being optimized to deliver better biocompatibility, chemical resistance, sterilization endurance, and mechanical performance. These materials support demanding applications such as catheters, diagnostic equipment, wearable sensors, and wound-care products. Another major trend is the rise of 3D-printing compatible medical-grade polymers, which enable patient-specific implant manufacturing and rapid prototyping. A growing share of new medical devices now incorporate additive-manufacturing requirements, reflecting the technology’s mainstream acceptance.

Sustainability-driven innovation is accelerating rapidly. Manufacturers are developing recycled-content medical-grade polymers and installing specialized recycling lines for polycarbonate, polyester, and other engineering plastics. This transition is supported by rising environmental pressure and regulatory targets. Advancements in antimicrobial polymer coatings and nanocomposite surfaces are also prominent, helping reduce infection risks in critical-care devices and implants. These materials combine polymer matrices with functional additives to create durable bactericidal surfaces without compromising sterilization compatibility.

Overall, the market is being reshaped by advancements in bioresorbability, recyclability, high-performance materials, and additive manufacturing — all of which are aligned with improved clinical outcomes and sustainability.

In March 2024, SABIC announced a successful pilot to create circular polymers from used medical plastic collected at a hospital, advancing advanced-recycling routes for medical waste and enabling return of recycled content into medical-grade polymer streams for further processing. Source: www.sabic.com

In April 2024, Evonik expanded production capacities for its RESOMER® powder biomaterials at the Darmstadt site, adding solvent-free micronization technology and custom powder production to support precision implants and aesthetic applications in medical devices. Source: www.evonik.com

In June 2024, DuPont agreed to acquire Donatelle Plastics Incorporated, a transaction intended to deepen DuPont’s healthcare and medical-device solutions by adding precision molding and polymer component capabilities for device manufacturers. Source: www.dupont.com

In July 2024, Eastman expanded its circular product offerings (Eastman Renew) and scaled material-to-material recycling efforts, including partnerships to collect and process mixed plastics — moves that support supply of recycled-content polymer inputs suitable for non-food and industrial healthcare applications. Source: www.eastman.com

The report covers the full spectrum of polymer materials used in medical devices — including resins, elastomers, bioresorbable polymers, TPEs, and high-performance thermoplastics. It evaluates major processing technologies such as injection molding, extrusion, blow molding, compounding, and 3D printing. Applications analyzed include disposables, implants, diagnostic equipment, surgical instruments, catheter systems, wound care, drug-delivery devices, and emerging wearable healthcare technologies.

Regional analysis spans North America, Europe, Asia Pacific, South America, and the Middle East & Africa, providing insights into consumption patterns, regulatory standards, and manufacturing capabilities. The competitive landscape assessment includes market share trends, strategic initiatives (expansions, partnerships, and product innovations), and analysis of consolidation vs. fragmentation.

The report also highlights emerging opportunities in sustainable materials, circular-economy polymers, antimicrobial surfaces, bioresorbables, and digital-manufacturing-enabled medical polymers.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 2,331.0 Million |

| Market Revenue (2032) | USD 3,754.7 Million |

| CAGR (2025–2032) | 6.14% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments, Regulatory & ESG Overview |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | BASF SE, DuPont, Evonik Industries, Celanese Corporation, DSM Biomedical, SABIC, Eastman Chemical Company |

| Customization & Pricing | Available on Request (10% Customization Free) |