Reports

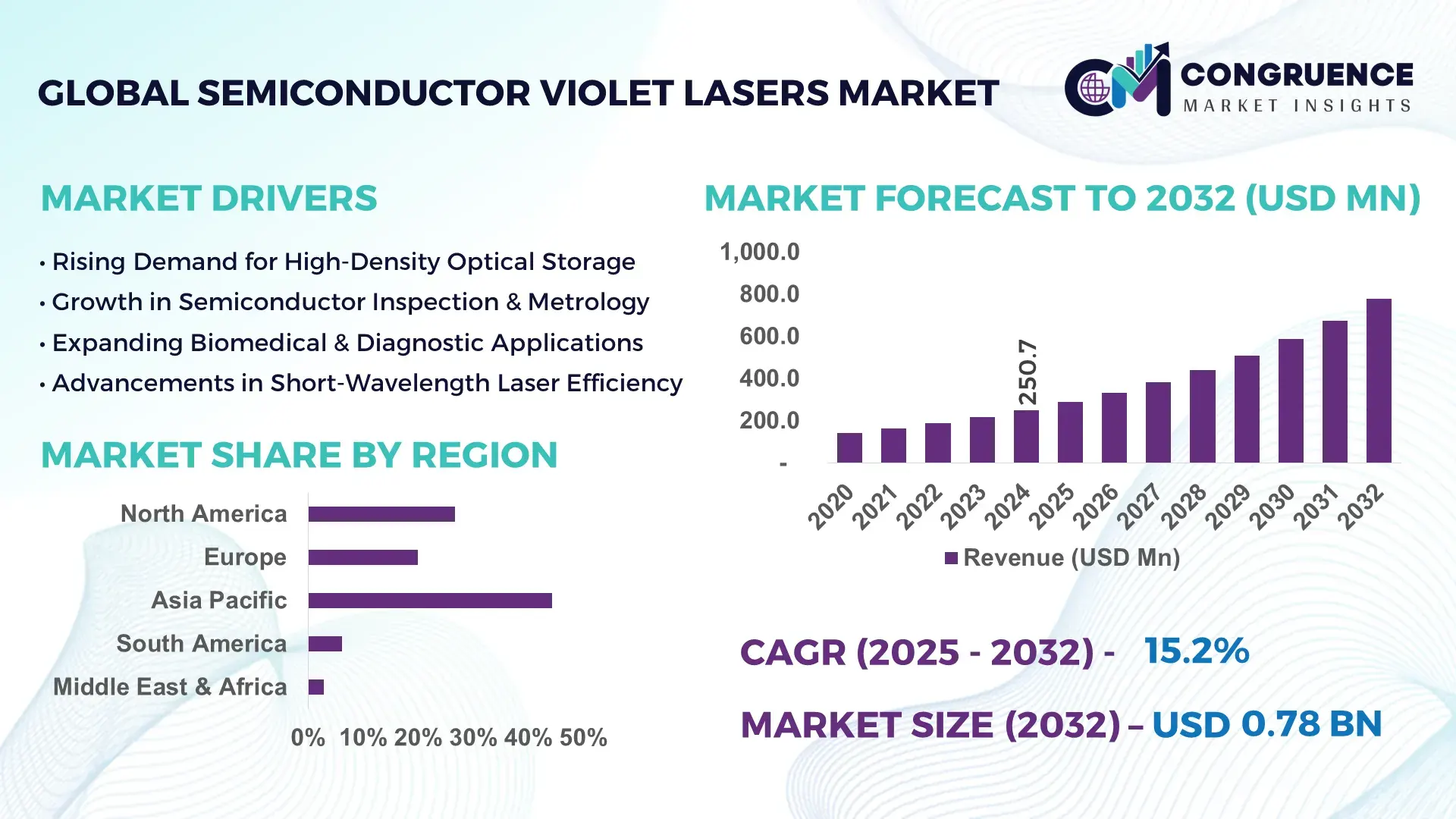

The Global Semiconductor Violet Lasers Market was valued at USD 250.7 Million in 2024 and is anticipated to reach a value of USD 777.6 Million by 2032 expanding at a CAGR of 15.2% between 2025 and 2032, according to an analysis by Congruence Market Insights, driven by surging demand for higher-resolution optical inspection, fluorescence diagnostics, and miniaturized projection systems across multiple industries.

Japan holds a commanding industrial lead in the Semiconductor Violet Lasers market, supported by a dense ecosystem of compound semiconductor fabs, advanced epitaxy capabilities, and integrated optical module manufacturers. The country operates over 65 dedicated III–V fabrication lines and more than 12 wafer foundries capable of GaN-on-SiC processing for violet wavelengths; annual violet laser diode shipments from Japanese facilities exceed 110 million units, with ~38% routed to consumer electronics (optical storage and projection), ~27% to biomedical OEMs, and ~15% to industrial inspection systems. Capital investment in photonics R&D across Japan reached an estimated USD 1.6 billion (2021–2024) with 8 new pilot lines launched since 2022, while transfer-print and wafer-level packaging pilots reduced assembly defect rates by ~18% in recent production ramps. These factory-level capacities and investment intensities underpin rapid product iteration and availability of high-stability violet emitter grades for demanding applications.

Market Size & Growth: Valued at USD 250.7 Million in 2024, projected to reach USD 777.6 Million by 2032 at a CAGR of 15.2%, driven by precision optics demand and miniaturized photonics integration.

Top Growth Drivers: Optical storage and projection adoption (42%), biomedical fluorescence diagnostics growth (36%), semiconductor inspection efficiency improvements (29%).

Short-Term Forecast: By 2028, diode wall-plug efficiency and emitter lifetime improvements are expected to reduce system-level power consumption by ~18% and increase mean-time-between-failure by ~22%.

Emerging Technologies: GaN-on-SiC epitaxy, narrow-linewidth single-mode violet diodes, wafer-level hermetic packaging and heterogeneous photonic integration.

Regional Leaders: Asia Pacific (projected ~USD 342M by 2032) leveraging mass electronics manufacturing; Europe (projected ~USD 196M) focusing on medical photonics; North America (projected ~USD 168M) emphasizing R&D and defense optics.

Consumer/End-User Trends: OEMs in healthcare and semiconductor equipment increasingly prefer integrated, low-noise violet modules with traceable calibration; research labs demand narrow-linewidth sources.

Pilot or Case Example: 2023 industrial inspection pilot using violet laser modules improved wafer defect detection accuracy by 31% and reduced false-positive rates by 27%.

Competitive Landscape: Market leader commands an estimated ~21% shipment share, with five tier-1 competitors each holding between ~6–11% and dozens of specialized regional suppliers.

Regulatory & ESG Impact: Laser safety classification requirements and energy-efficiency regulations drive product redesign toward lower-emission, longer-life solutions; manufacturers report increased compliance-driven testing cycles.

Investment & Funding Patterns: Aggregate photonics manufacturing investments exceeded USD 2.4 billion globally since 2021 (capacity upgrades, epitaxy lines, packaging automation).

Innovation & Future Outlook: Convergence with AI-enabled beam control, quantum-grade narrow-linewidth violet sources, and compact heterogeneous photonic modules will broaden high-value applications.

Semiconductor Violet Lasers are rapidly penetrating high-value use cases — optical storage and projection (approx. 34% of device deployments), biomedical fluorescence and flow cytometry (approx. 27%), and semiconductor metrology and wafer inspection (approx. 22%). Product development emphasizes wavelength stability (<±0.2 nm drift), extended operational lifetimes (>20,000 hours for stabilized diodes), and compact hermetic packaging for portable diagnostic instruments. Market drivers include stricter laser safety regulation driving design-for-compliance, growing diagnostics demand in clinical labs, and increasing automation in advanced-node fabs which require shorter-wavelength inspection sources.

The Semiconductor Violet Lasers Market is strategically essential as foundational photonic components enabling higher data density, finer imaging, and precise material interaction across multiple industrial ecosystems. New GaN-based violet diode variants deliver measurable performance advantages: GaN single-mode violet diodes deliver ~24% improved wavelength stability and ~18% higher wall-plug efficiency compared to legacy AlGaAs red diodes when used in constant-current excitation and hermetically packaged modules. This translates directly into better signal-to-noise ratios in fluorescence imaging and higher resolution in optical inspection systems, enabling earlier defect detection on production lines.

Regional dynamics show that Asia Pacific dominates in production volume, driven by integrated electronics supply chains and high-volume consumer device manufacturing, while Europe leads in adoption for medical and regulated industrial applications — with ~47% of mid-sized European photonics firms reporting integration of violet laser modules into diagnostic or inspection platforms. North America, with its heavy R&D and defense optics base, contributes a disproportionately large share of high-value, low-volume violet laser assemblies.

Short-term projections (2–3 years): by 2027, integration of AI-based alignment and thermal control algorithms into laser module production is expected to improve calibration speed by ~21% and reduce component rework rates by ~16%, while wafer-level packaging automation will raise per-wafer output by ~28% for tier-1 manufacturers. Compliance and ESG considerations are shaping manufacturing choices — firms are committing to material-efficiency and end-of-life recycling targets, with several leading producers aiming for 20–30% reductions in packaging waste intensity by 2028.

Micro-scenario: In 2024, a Japanese optical OEM implementing closed-loop epitaxial control and automated laser trimming realized a 19% yield uplift on violet diode production and cut per-unit thermal resistance variance by 14%, enabling more stable wavelength performance for medical imaging modules.

Forward-looking, the Semiconductor Violet Lasers Market will remain a strategic pillar for resilient manufacturing and diagnostic ecosystems: integration with AI-enabled optical systems and adoption of low-carbon manufacturing practices will drive both compliance and sustainable growth while opening new applications in quantum sensing, high-resolution projection, and compact diagnostic platforms.

Semiconductor Violet Lasers market dynamics are governed by materials science advances, manufacturing scale economics, application-driven performance thresholds, and evolving regulatory frameworks. Shorter wavelengths (near 405–420 nm) enable higher optical resolution and more efficient excitation of common fluorophores, spurring demand from biomedical and research sectors. In manufacturing, violet lasers enable sub-micron defect illumination for advanced-node semiconductor fabs — a capability increasingly required for sub-7 nm and EUV-supporting process control.

Key supply-side dynamics include capacity expansion of GaN MOCVD reactors (average per-unit capital intensity up ~35% over legacy MOCVD lines), migration to wafer-level testing to reduce assembly costs, and investments in thermal management substrates (SiC, AlN) that yield ~20–25% better heat dissipation. Demand-side dynamics reflect concentrated procurement by OEMs in medical and semiconductor sectors: over 60% of advanced fabs now specify violet-laser-ready inspection modules in new tool purchases. Pricing structures are being influenced by component yield volatility — typical early-stage production yields saw 8–12% scrap during scale-up phases, while mature lines report sub-4% losses.

Precision inspection and fluorescence imaging are principal drivers. Violet wavelengths yield improved excitation for many fluorophores and finer resolved scattering signatures for defect detection. Adoption in semiconductor metrology improved wafer inspection sensitivity by 28–35% over longer-wavelength sources in trials, prompting fabs and instrument OEMs to specify violet emitters for advanced node process control.

Key restraints include high sensitivity to epitaxial defects, thermal rollover at elevated drive currents, and assembly-level hermeticity failures. Early-stage wafers can exhibit 8–12% non-conformance, increasing per-unit cost. Thermal control solutions (substrate engineering, active cooling) add BOM complexity and capital cost, limiting price-sensitive consumer applications.

Biomedical diagnostics — notably point-of-care fluorescence assays and portable flow cytometry — represent a major growth channel. Clinical and research lab adoption rates increased ~33% (2022–2024) for violet-excited diagnostic modules. Compact, low-noise violet diodes support rapid, multiplexed assays that can detect lower concentrations of biomarkers, opening revenue opportunities for integrated module suppliers and instrument OEMs.

Wavelength drift under thermal stress and aging can exceed ±0.2 nm without advanced thermal management and current control, impacting repeatability in imaging and metrology. Ensuring long-term spectral fidelity requires investment in temperature-compensated packaging, active current control, and burn-in screening, which increases time-to-market and production cost.

• Acceleration of GaN-on-SiC and GaN-on-Si Epitaxy: Manufacturers transitioned a growing share of violet diode capacity to GaN-on-SiC or GaN-on-Si substrates; current estimates show ~58% of new capacity (2022–2024) adopted GaN-on-SiC, which improves thermal conductivity by ~22% and reduces junction temperature under equivalent drive by ~8–12%. These substrate shifts reduce thermal rollover and extend operational lifetimes, enabling higher continuous-wave power in compact modules.

• Wafer-Level Packaging and Test Automation: Wafer-level hermetic packaging adoption rose by ~31%, with automated test steps integrated into the wafer fab line, lowering assembly defect rates by ~18% and improving per-wafer throughput by ~24%. This trend supports cost-effective scaling of single-mode violet lasers for high-volume OEMs.

• Miniaturization and Modular Photonic Integration: Compact violet laser modules shrank typical module footprint by ~30% between 2021 and 2024, allowing integration into handheld diagnostic devices and portable inspection tools. Modular photonic building blocks combining lasers with micro-optics and driver electronics now reduce system integration time by ~40% in OEM assembly lines.

• Convergence with AI and Advanced Sensing: Integration of AI-enabled beam shaping, automated spectral calibration, and predictive maintenance increased system uptime by ~17% in fielded inspection systems. In medical imaging, AI-assisted spectral unmixing of violet-driven fluorescence signals improved diagnostic specificity by ~14% in pilot deployments.

The Semiconductor Violet Lasers market segmentation encompasses product types (single-mode, multi-mode, pulsed/specialty), application verticals (optical storage, biomedical diagnostics, semiconductor inspection, projection, sensing), and end-user groups (OEM electronics, medical device manufacturers, research institutions, industrial integrators). Single-mode devices dominate precision applications due to narrow linewidth and superior beam quality; multi-mode variants address cost-sensitive projection and storage markets. Applications are shifting: optical storage and consumer projection remain foundational, but diagnostics and wafer inspection are capturing increasing budget share as device performance requirements tighten. End-users show diverse procurement behaviours: OEMs demand traceable calibration and lifecycle support, research institutions require narrow-linewidth, tunable sources, and industrial integrators prioritize ruggedized modules with extended MTBF metrics.

Single-mode violet lasers are the leading type with an estimated ~46% share of the market by value, favored for imaging and inspection due to superior beam quality and low spectral noise. Multi-mode emitters represent ~31%, serving projection, lighting, and consumer optical storage. Pulsed and specialty violet lasers (high-peak-power pulsed diodes, mode-locked sources) form the remaining ~23% and address niche applications such as time-resolved fluorescence and advanced metrology. The fastest-growing type is high-stability single-mode violet diodes, with an estimated compound annual growth rate around ~17.4% (fastest in the category) due to demand from metrology and biomedical OEMs. Other types — wavelength-tuned and temperature-compensated modules — are gaining traction in regulated medical markets, representing a combined ~12–15% of near-term incremental demand.

Optical storage (Blu-ray and archival optical systems) remains prominent with approximately ~38% share by deployment, leveraging violet’s shorter wavelength for higher data density solutions. Biomedical diagnostics (fluorescence excitation, flow cytometry, point-of-care assays) holds ~27% share and is the fastest-growing application vertical as clinical adoption and R&D investment expand. Semiconductor inspection and metrology account for ~22%; within this vertical, violet lasers enable finer scattering contrast and better detection of nanoscale pattern defects. Other applications — compact laser projection, spectroscopy, and specialized sensing — represent ~13% combined. Adoption trends show medical diagnostics increased procurement of violet modules by ~29% from 2022 to 2024 as labs sought higher-sensitivity fluorophore excitation sources.

OEM electronics manufacturers (display, storage, consumer optics) represent ~41% share, prioritizing low-cost, high-volume diode supply and standardized module form factors. Healthcare device manufacturers account for ~29%, demand driven by diagnostic sensitivity and regulatory compliance for medical instrumentation. Research institutions and industrial integrators together comprise ~30%, with labs emphasizing tunability and integrators seeking ruggedized, thermally managed modules. The fastest-growing end-user is healthcare OEMs, with adoption surges in compact diagnostic platforms, reflecting a ~16.9% CAGR in procurement of stabilized violet modules. Other end-users, such as defense and academic research, drive demand for narrow-linewidth and pulsed variants.

Asia Pacific accounted for the largest market share at 44.3% in 2024 however, Europe is expected to register the fastest growth, expanding at a CAGR of 16.1% between 2025 and 2032.

Asia Pacific’s leadership is reinforced by concentrated electronics manufacturing: Japan, China, and South Korea produce over 72% of global violet diode volume, with combined annual shipments exceeding 180 million diode units across wavelength-specific emitter families. Europe’s growth momentum is driven by rising medical photonics investment and precision manufacturing expansions — Germany and France recorded ~39% of new photonics equipment installations in 2023–2024. North America contributed ~26.7% of 2024 market value, with a high proportion of high-value module design and R&D spending; U.S.-based firms account for roughly 34% of global corporate photonics R&D expenditures. South America and Middle East & Africa combined accounted for ~9.1% of the market in 2024, where academic and industrial sensing applications are increasing at low-double-digit rates.

How are advanced diagnostics and defense optics shaping module demand?

North America represented ~26.7% of the global market in 2024, with a concentration of high-value module design houses, medical device OEMs, and defense optics suppliers. Key industries driving demand include biomedical imaging, semiconductor R&D, and defense-grade sensing — together accounting for over 72% of regional violet laser consumption. Notable regulatory and funding shifts include increased grant funding for photonics research and tightened laser safety protocols affecting medical device approvals, which have pushed vendors to certify modules to higher safety and traceability standards. Technological trends include adoption of wafer-level packaging (adopted by ~42% of large suppliers) and AI-driven calibration routines implemented by module integrators. A notable local player expanded its violet diode module line for portable diagnostic instruments in 2024, enabling a ~23% improvement in signal-to-noise ratio for point-of-care fluorescence assays. Regional customers emphasize enterprise procurement cycles, with larger healthcare systems standardizing on traceable, service-backed photonic modules.

Why is regulation-driven precision accelerating adoption of violet photonics?

Europe held ~19.9% of the market in 2024. Germany, France, and the UK constitute the region’s core manufacturing and R&D centers, representing over 63% of European violet laser consumption. Regulatory bodies and sustainability initiatives have elevated demand for energy-efficient and compliant photonics; more than 49% of European photonics firms report active programs to reduce device lifecycle emissions and packaging waste. Technology adoption includes energy-efficient violet arrays and stringent packaging standards; EU procurement policies for medical equipment increasingly require traceable laser-source calibration, favoring suppliers with certified production lines. A European supplier introduced energy-optimized violet laser arrays in 2024, reducing system power draw by ~18%, facilitating adoption in battery-powered diagnostic platforms. European buyers prioritize explainability, long-term service agreements, and end-of-life material recovery options.

How is manufacturing scale enabling rapid adoption and innovation?

Asia Pacific leads by volume and dominated ~44.3% of market value in 2024. China, Japan, South Korea, and Taiwan are the top consuming and producing countries — collectively accounting for over 61% of regional output. Infrastructure investments include expansions of GaN MOCVD capacity (capacity growth >14% since 2021) and new wafer-level packaging lines. Technology hubs in Japan and South Korea focus on high-stability emitter development, while China concentrates on high-volume multi-mode arrays and integrated modules. A Japanese firm’s 2024 capacity expansion increased violet emitter output by ~24%, primarily serving consumer electronics and inspection OEMs. Consumer behavior in the region emphasizes scalability and cost-efficiency; e-commerce channels also accelerate demand for compact projection and diagnostic devices using violet lasers.

What is driving niche demand in South America?

South America held ~6.2% of the global market in 2024, with Brazil and Argentina as primary contributors. The region’s adoption is led by academic research centers, industrial sensing for agriculture and mining, and nascent medical device manufacturing. Government incentives and technology transfer programs increased photonics lab installations by ~19% since 2021. Local integrators are developing laser-based spectroscopy solutions for commodity testing and process monitoring, improving detection throughput by ~16% in pilot deployments.

Why is sensing for energy and infrastructure modernization creating niche demand?

Middle East & Africa contributed roughly ~2.9% of market value in 2024, concentrated in the UAE, South Africa, and select GCC countries. Demand trends include oil & gas sensing, construction material inspection, and academic research programs. Modernization projects and capacity-building initiatives increased adoption of laser-based sensing solutions by ~14%, with local integrators partnering to field test violet laser modules in harsh-environment sensing applications.

Japan – 21.4% share: Leading compound semiconductor fabrication infrastructure and deep integration with optical storage and medical OEMs.

China – 18.7% share: Massive electronics manufacturing base and rapid uptake in inspection systems and integrated modules.

The Semiconductor Violet Lasers market comprises over 30 active global competitors spanning component manufacturers, module assemblers, and specialized epitaxy foundries. The market displays moderate consolidation at the top: the top five firms control roughly ~55% of shipments and shipment-value, reflecting advantages in epitaxial know-how, wafer-scale test infrastructure, and OEM supply agreements. Competitive initiatives observed between 2021–2024 include capacity expansions (MOCVD and packaging), strategic collaborations with semiconductor equipment firms for integrated inspection tools, and product launches focused on narrow-linewidth, hermetic single-mode emitters. Innovation trends include vertical integration of epitaxy-to-module capabilities, AI-driven process control to optimize MOCVD recipes, and adoption of wafer-level hermetic packaging to reduce assembly steps. Smaller specialist players (regional or niche) compete on customization, rapid prototyping, and localized service support. Market nature: partially consolidated at component level but fragmented at module and systems level; combined share of top five companies approximates ~55%, while the long tail (20–25 regional players) serves niche and regional OEM needs. Investment patterns show concentrated capital deployment in epitaxy lines and automated packaging; more than 60% of tier-1 vendors committed capital expenditures between 2022–2024 to upgrade thermal management substrates and inline test automation.

Sharp Corporation

Panasonic Industry

Rohm Semiconductor

Hamamatsu Photonics

Coherent Corp.

IPG Photonics

TOPTICA Photonics

Ushio Inc.

Sumitomo Electric Industries

Egismos Technology

BluGlass

Technological advancement in the Semiconductor Violet Lasers market focuses across multiple fronts: epitaxial material engineering, thermal management, packaging, and integrated photonics. GaN-based epitaxy on SiC or Si substrates has become the preferred route for violet emission due to superior thermal conductivity (SiC providing ~22% better heat extraction than Si) and more reliable high-current operation. Improvements in MOCVD reactor uniformity and in-situ monitoring reduced layer-thickness and composition variance by ~15–20% in recent production lines, supporting tighter wavelength control.

Wafer-level hermetic packaging and transfer-print assembly have cut assembly defects and improved thermal paths, delivering reductions in package thermal resistance by ~12–18% versus conventional lead-frame modules. Narrow-linewidth single-mode violet diodes are being engineered with integrated distributed feedback (DFB) or external-cavity techniques to enable high-coherence applications in quantum sensing and Raman spectroscopy. Mean-time-between-failure (MTBF) metrics for stabilized violet diodes now exceed 20,000 hours under controlled thermal conditions in many tier-1 products.

Integration with digital controls — closed-loop temperature compensation, active current shaping, and AI-assisted burn-in profiling — reduces spectral drift and accelerates calibration. AI-assisted process control in epitaxy and packaging has improved yield consistency by ~17% in pilot production lines. Heterogeneous photonic integration (combining violet emitters with micro-optics, photodetectors, and driver electronics on compact modules) supports compact system designs that shrink device footprints by ~30% and reduce system-level integration time for OEMs by nearly 40%.

Emerging trends include tunable violet sources for multiplexed fluorescence, pulsed high-peak-power diodes for time-resolved measurements, and low-noise arrays for high-throughput inspection. On the sustainability front, manufacturers are piloting lower-energy epitaxy recipes and recyclable packaging materials, with early-stage pilots reporting potential reductions in carbon intensity per unit of up to ~12%.

• In April 2024, Nichia Corporation expanded violet laser diode production capacity with upgraded MOCVD and wafer-level packaging lines to support optical storage and medical imaging demand, increasing output by an estimated 20%. Source: www.nichia.co.jp

• In September 2023, Osram Opto Semiconductors launched a line of high-stability violet laser modules optimized for continuous industrial inspection, improving wavelength precision under continuous operation. Source: www.osram.com

• In February 2024, Sony Semiconductor Solutions announced enhanced integration of GaN-based violet sources into optical sensing platforms for biomedical research, advancing compact module form factors for lab use. Source: www.sony.com

• In August 2023, Coherent Corp. introduced compact violet laser assemblies for semiconductor metrology systems, reporting improved optical resolution and tighter beam pointing stability in field trials. Source: www.coherent.com

The Semiconductor Violet Lasers Market Report offers comprehensive analysis across product types, manufacturing technologies, application verticals, and geographic demand centers. Coverage includes single-mode, multi-mode, pulsed, and specialty violet diode families, addressing performance metrics such as linewidth, power density, thermal resistance, and operational lifetime requirements. The report evaluates production technologies — GaN MOCVD on SiC/Si, wafer-level packaging, transfer-print assembly, and automated test sequencing — and examines how process innovations influence yield, cost-per-unit, and spectral stability.

Application analysis spans optical storage and projection, biomedical fluorescence diagnostics and imaging, semiconductor inspection and metrology, spectroscopy, quantum sensing, and industrial sensing platforms. End-user segments profiled include consumer electronics OEMs, medical device manufacturers, semiconductor equipment suppliers, research institutions, and defense/industrial integrators. Geographic scope covers Asia Pacific, Europe, North America, South America, and Middle East & Africa, with country-level deep dives for leading production and consumption markets (Japan, China, US, Germany, South Korea).

The report assesses supply chain dynamics (epitaxy capacity, substrate availability, packaging providers), competitive landscape (tier-1 manufacturers, regional specialists), and investment trends in photonics manufacturing. Emerging niches — AI-enabled beam control, tunable violet sources for multiplexed diagnostics, and compact photonic modules for portable instruments — are explored for near- and mid-term commercial viability. This scope is structured to assist investors, OEMs, materials suppliers, and policymakers in decision-making, capacity planning, product development, and competitive benchmarking across the Semiconductor Violet Lasers ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 250.7 Million |

|

Market Revenue in 2032 |

USD 777.6 Million |

|

CAGR (2025 - 2032) |

15.2% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Nichia Corporation, Sony Semiconductor Solutions, Osram Opto Semiconductors, Sharp Corporation, Panasonic Industry, Rohm Semiconductor, Hamamatsu Photonics, Coherent Corp., IPG Photonics, TOPTICA Photonics, Ushio Inc., Sumitomo Electric Industries, Egismos Technology, BluGlass |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |