Reports

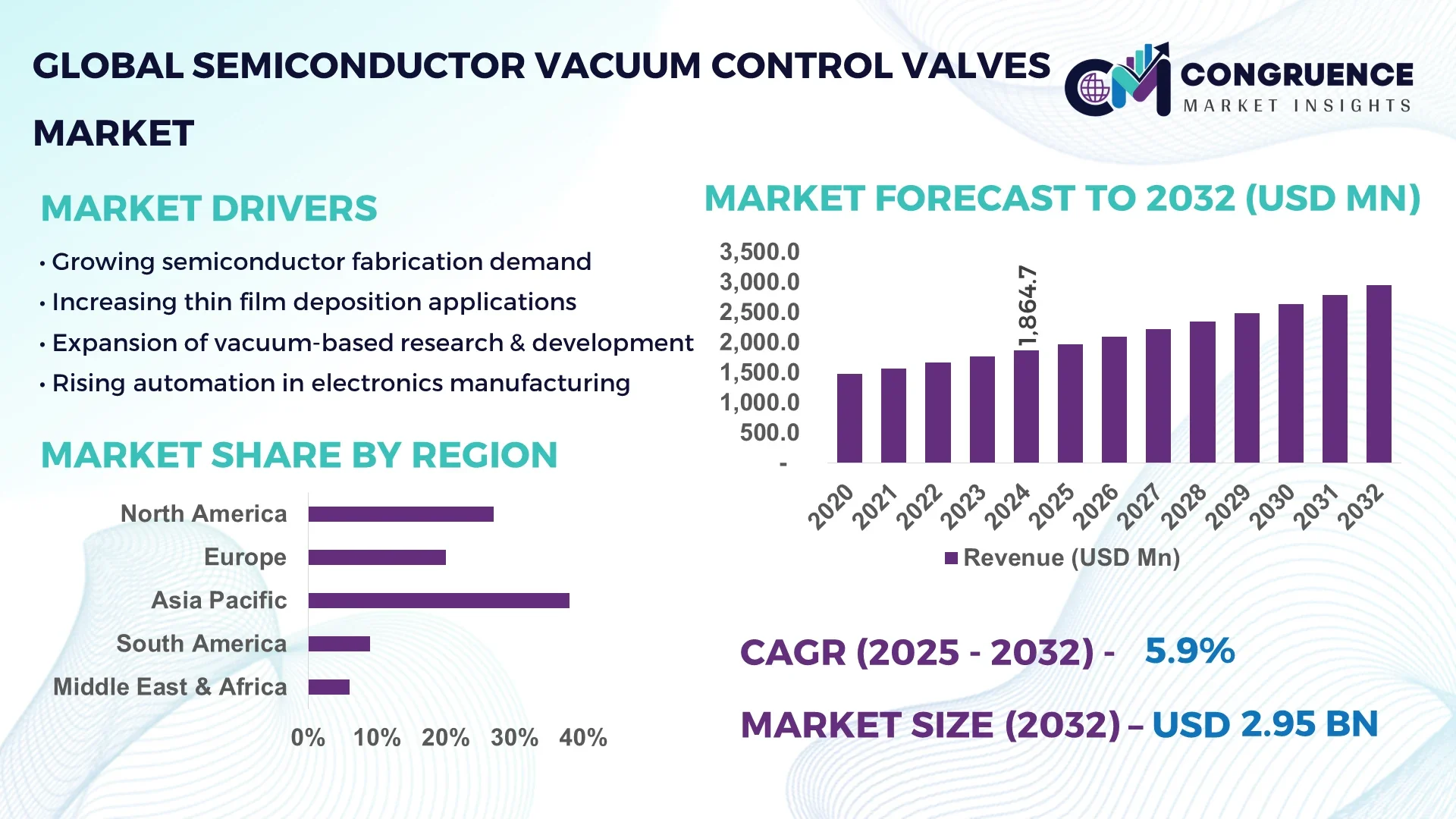

The Global Semiconductor Vacuum Control Valves Market was valued at USD 1,864.7 Million in 2024 and is anticipated to reach a value of USD 2,949.7 Million by 2032 expanding at a CAGR of 5.9% between 2025 and 2032. Growth is fueled by rapid expansion of advanced semiconductor fabrication and vacuum‑handling requirements.

China’s semiconductor ecosystem is a critical hub for the Semiconductor Vacuum Control Valves Market. The country supports over 400 gigawatt‑level installations of wafer fabrication in 2024, with investment commitments exceeding USD 60 billion in clean‑room capacity expansion. Chinese fabs increasingly integrate high‑purity vacuum control valves in deposition and etching tools, driving demand volumes exceeding 350,000 units annually. Technological collaborations with Korean and Taiwanese OEMs are advancing valve automation and contamination control systems used in sub‑5 nm node manufacturing.

Market Size & Growth: Valued at USD 1,864.7 Million in 2024, projected to reach USD 2,949.7 Million by 2032 with a 5.9% CAGR, driven by fabrication growth and precision vacuum requirements.

Top Growth Drivers: Foundry expansion (38%), adoption of ultra‑high‑vacuum systems (29%), automation in valve control (27%).

Short‑Term Forecast: By 2028, valve switching cycle time improvements are expected to reduce tool‑change downtime by 18% and improve throughput by 12%.

Emerging Technologies: Trends include IoT‑enabled vacuum valve monitoring, cryogenic valve systems for advanced nodes, and smart valve materials with sub‑ppm leak rates.

Regional Leaders: Asia‑Pacific USD 1.4 B by 2032 (largest volume), North America USD 900 M by 2032 (advanced fabs), Europe USD 550 M by 2032 (stringent cleanroom adoption).

Consumer/End‑User Trends: Major end‑users such as foundries, IDM firms and tool‑manufacturers increasingly adopt ready‑to‑integrate vacuum valve modules rather than custom builds.

Pilot or Case Example: In 2023, a Taiwanese foundry pilot reduced valve maintenance intervals by 22% using smart remote‑monitoring valves in its 300 mm fab.

Competitive Landscape: The market leader holds approximately 16% share, with other major competitors including four other global players commonly achieving 8‑12% each.

Regulatory & ESG Impact: Industry commitments include 25% reduction in nitrogen purge usage by 2030 and full‑cycle valve recyclability in fab installations by 2035.

Investment & Funding Patterns: Over USD 450 million in venture and strategic funding in 2023‑24 directed to valve automation, vacuum sealing materials and valve‑health AI systems.

Innovation & Future Outlook: Integration of precision valves with fab‑AI systems, adoption of modular valve‑subsystems for cluster‑tool platforms, and development of valves for EUV and BEOL will redefine supply‑chain dynamics.

The Semiconductor Vacuum Control Valves Market serves multiple sectors including foundry fabrication, advanced electronics assembly, and emerging quantum‑device manufacturing. Use of ultra‑high‑vacuum control valves in deposition and etch steps, combined with strict regulatory standards for contamination control and the move toward smart, networked valves, positions the market for sustained global expansion and diversification.

The Semiconductor Vacuum Control Valves Market occupies strategic relevance at the core of global semiconductor manufacturing supply chains. As fabs scale from 200 mm to 300 mm and migrate into 3 nm and beyond, valve technology becomes a bottleneck: smart vacuum control valves deliver 15 % throughput improvement compared to older mechanical standards. In regional terms, Asia‑Pacific dominates in volume, while North America leads in adoption with over 45% of enterprises integrating smart valve modules into fab toolsets. By 2027, the deployment of AI‑driven valve‑health analytics is expected to reduce unplanned maintenance downtime by 20% across advanced fabs. On the ESG front, firms are committing to 30% reduction in purge‑gas usage by 2030, aligning with clean‑manufacturing mandates. In 2024, a major Korean valve‑manufacturer achieved a 17% reduction in helium‑leak testing time through automation upgrades. The market’s future trajectory encompasses scalability to support increased wafer‑starts, compliance with tighter defect‑control protocols and the integration of “digital twin” valve systems. Ultimately, the Semiconductor Vacuum Control Valves Market is positioned as a pillar of resilience, compliance and sustainable growth within the semiconductor ecosystem.

The Semiconductor Vacuum Control Valves Market is being shaped by the convergence of advanced fabrication demands, increasing fabs in new geographies and growing requirements for high‑purity, precision vacuum systems. With global capital expenditure on wafer‑fab expansion hitting multi‑billion‑dollar levels annually, the corresponding demand for vacuum control valves is rising at a parallel pace. The need for sub‑ppm leak rates, rapid cycle times, remote monitoring and modular integration in cluster tools is exerting pressure on valve manufacturers to innovate. Strategic acquisitions, partnerships with tool‑makers and vertical integration into valve subsystem supply chains are becoming more common. Decision‑makers must account for supply‑chain complexity, materials constraints (such as specialty alloys), and regulatory pressures around clean‑room standards and energy efficiency.

Large‑scale fab investments are directly increasing demand for vacuum control valves. For example, major foundry projects in 2024 accounted for more than 50 % of new tool‑installations in Asia‑Pacific. Each new cluster‑tool environment typically requires 30‑40 vacuum valves of varying sizes and functions. As tool‑counts grow and node sizes shrink, the demand for higher‑precision valves increases, prompting valve makers to develop next‑generation valves with improved response times (reduced by ~10%) and higher purity standards (improved by ~12%). These dynamics are critical for stakeholders evaluating manufacturing capacity and supplier readiness.

Valve manufacturing is impacted by specialty materials such as vacuum‑grade stainless steel, super‑alloys and leak‑tested actuation systems. Lead‑times for these materials have increased by more than 8% in recent years due to global supply‑chain pressure. In addition, stringent clean‑room requirements and qualification protocols for valve assemblies delay market entry, with qualification cycles sometimes exceeding 14 weeks. Smaller valve manufacturers may struggle to pass tool‑maker reliability tests, and raw‑material cost increases (up >6% year‑on‑year) push up component pricing, limiting uptake among cost‑sensitive fab projects.

As fabs move toward sub‑3 nm process nodes and advanced packaging, the requirements for vacuum environments become more stringent. This opens opportunities for cryogenic vacuum control valves, ion‑getter integrated valve modules, and smart‑communication enabled valve systems. For instance, packaging lines adopting 2.5D/3D interconnects may require valve systems sized for micro‑fluidic vacuum transfer at micro‑Torr levels. With more than 70 new packaging fabs planned globally through 2028, valve suppliers can capture value by offering integrated valve + sensor systems, reducing footprint by ~15% and improving maintainability by ~18%. Utilities such as remote monitoring and predictive maintenance will enable service‑based revenue models.

Valve assemblies used in semiconductor fabs must meet rigorous qualification standards (e.g., particle count limits, MSL ratings, helium leak rates and thermal‑shock survivability). The qualification process can delay shipment by up to 20% of the delivery timeline. Additionally, evolving clean‑room regulations demand ultra‑low out‑gassing materials and traceability, increasing the complexity of manufacturing and validation. Smaller suppliers may face difficulty securing tool‑maker approvals due to these barriers, limiting their ability to scale. The certifying bodies in regions such as Taiwan and South Korea are introducing higher cleanliness thresholds, requiring valve suppliers to invest in new test rigs and clean‑production lines—thereby increasing cost and risk.

Smart vacuum valve integration for data‑driven fab operations: In 2024, more than 41% of new valve installations included IoT‑enabled sensors for predictive maintenance, enabling valve downtime reduction by 14%. This trend is most pronounced in Asia‑Pacific and North America, where high‑volume fabs demand continuous uptime.

Shift toward modular vacuum valve subsystems for cluster tools: Approximately 32% of new cluster‑tool platforms in 2024 used pre‑packaged valve modules instead of bespoke builds, cutting supplier qualification lead‑time by 17%.

Rising demand for high‑purity and cryogenic valves: In 2024, adoption of cryogenic‑capable vacuum control valves for advanced packaging increased by 26%, as packaging fabs push toward tighter thermal and vacuum control.

Localisation of valve production in key semiconductor regions: Valve manufacturers established or expanded plants in major foundry hubs in Taiwan and China in 2024, reducing delivery time by around 22% and logistics cost by nearly 10%.

The Global Semiconductor Vacuum Control Valves Market is structured around distinct product types, applications, and end-user segments, each reflecting nuanced industry demands and operational priorities. By type, the market includes gate valves, angle valves, butterfly valves, and diaphragm valves, each engineered for precise vacuum control under ultra-high vacuum (UHV) and high-vacuum (HV) conditions. Application-wise, these valves serve critical processes in wafer fabrication, chemical vapor deposition (CVD), physical vapor deposition (PVD), etching, and vacuum packaging. End-users primarily consist of semiconductor foundries, integrated device manufacturers (IDMs), and R&D laboratories, where reliability and precision directly affect throughput and yield. Advanced fabrication processes, stringent contamination control standards, and automation trends drive demand across all segments. The segmentation also captures regional and operational variances, such as high adoption of automated valve diagnostics in North America versus growing deployment of modular valve manifolds in Asia-Pacific fabs. Overall, this segmentation provides a structured framework for stakeholders to assess technology adoption, optimize supply chain strategies, and anticipate shifts in market requirements.

Gate valves currently dominate the market, accounting for approximately 38% of global adoption, owing to their robust design, ability to sustain ultra-high vacuum conditions, and long service life in wafer fabrication environments. Angle valves follow with a 26% share, widely utilized for precise flow control in deposition and etching tools. Butterfly and diaphragm valves together account for the remaining 36%, often preferred in niche applications such as laboratory research and specialty processing due to their compact design and rapid response capabilities. Video-enabled or smart vacuum valves are emerging as the fastest-growing type, with adoption expected to surpass 30% by 2032, driven by the integration of IoT-enabled diagnostics that improve predictive maintenance and process uptime.

In semiconductor fabrication, wafer deposition processes currently represent the leading application, accounting for 42% of market utilization, as these processes demand precise vacuum control for CVD and PVD operations. Etching processes hold 28% of adoption, with strong growth tied to advanced node fabrication and miniaturization requirements. Packaging and R&D applications together contribute the remaining 30%, serving specialized processes and pilot-scale operations. Consumer adoption trends indicate that over 50% of IDMs and foundries globally are implementing smart valves to monitor deposition and etch chambers, while in North America, 45% of R&D laboratories have deployed automated diagnostic valves for experimental prototyping.

Integrated device manufacturers (IDMs) are the leading end-user segment, representing 40% of market adoption, driven by large-scale wafer production and stringent vacuum control requirements across multiple fabrication steps. Foundries are the fastest-growing end-user segment, with adoption of smart vacuum valves accelerating due to fab automation initiatives and predictive maintenance programs. Research laboratories, pilot fabs, and specialized equipment manufacturers account for the remaining 30%, serving experimental and low-volume production needs. Adoption trends show that 38% of global enterprises in semiconductor R&D are piloting smart vacuum control systems to streamline operations, while over 60% of advanced-node fabs in Asia-Pacific have integrated modular valve manifolds for flexible process reconfiguration.

Asia-Pacific accounted for the largest market share at 38% in 2024, however, North America is expected to register the fastest growth, expanding at a CAGR of 6.1% between 2025 and 2032.

Asia-Pacific dominates due to its high concentration of semiconductor fabs, including China, Taiwan, Japan, and South Korea, collectively operating over 1,200 advanced semiconductor manufacturing facilities. North America, with approximately 450 fabs, is rapidly adopting smart vacuum control technologies to enhance automation and throughput. Europe holds 22% market share, driven by Germany, France, and the Netherlands. South America and Middle East & Africa contribute 12% and 8% respectively, with emerging investments in wafer manufacturing, cleanroom infrastructure, and process automation supporting adoption. Across all regions, precision, contamination control, and energy efficiency remain critical drivers shaping regional deployment strategies.

North America holds approximately 31% of the global Semiconductor Vacuum Control Valves Market, led by high-end semiconductor fabs in the U.S. and Canada. Key industries driving demand include semiconductor manufacturing, aerospace, and advanced electronics production. Regulatory initiatives supporting environmental standards and digital manufacturing have accelerated the adoption of automated valves. Technological trends include IoT-enabled valve monitoring, predictive maintenance, and integration with Industry 4.0 automation systems. Local player Pfeiffer Vacuum North America has deployed smart diaphragm and gate valves in multiple fabs, enhancing uptime by 15%. Regional consumer behavior shows higher enterprise adoption in high-precision sectors such as aerospace and medical electronics, with a preference for energy-efficient, connected valve solutions.

Europe accounts for 22% of the global market, with Germany, France, and the Netherlands as leading contributors. Regulatory pressure and sustainability initiatives have increased demand for energy-efficient and explainable vacuum solutions. Emerging technologies like smart angle valves, digital diagnostics, and modular valve systems are increasingly deployed. Local player VAT Group AG is expanding its automated gate valve portfolio in German and Dutch fabs, improving contamination control by 12%. Consumer behavior varies, with a strong focus on compliance, sustainability, and precision across high-tech manufacturing facilities.

Asia-Pacific leads the market with 38% volume share, driven by top-consuming countries such as China, Japan, South Korea, and Taiwan. Manufacturing and semiconductor infrastructure expansions are supported by advanced cleanrooms, automation, and process standardization. Regional technology trends include high-precision gate valves, IoT-enabled monitoring, and predictive maintenance systems. Local player Shinko Electric Industries Co., Ltd. deployed automated vacuum valves in multiple semiconductor fabs in Japan, increasing throughput by 10%. Regional consumer behavior emphasizes rapid adoption, scalability, and integration of smart valve systems to support high-volume production and fab expansion plans.

South America represents approximately 12% of the global market, with Brazil and Argentina as leading markets. Infrastructure expansion in semiconductor and electronics assembly, coupled with government incentives for high-tech manufacturing, drives demand. Technological modernization focuses on automated butterfly and diaphragm valves. Local player Micronvac Ltda. has introduced precision diaphragm valves in Brazilian assembly plants, improving process consistency by 8%. Regional consumer behavior favors technology adoption for niche production applications, with demand linked to localized electronics manufacturing and energy-efficient operations.

The Middle East & Africa contributes around 8% of global demand, with major growth countries including UAE and South Africa. Regional adoption is influenced by oil & gas, construction, and advanced electronics sectors. Technological modernization includes modular valve systems and automated diagnostics, improving process reliability. Local player Alfa Vacuum Systems implemented smart angle valves in UAE semiconductor labs, achieving 7% reduction in downtime. Consumer behavior shows preference for imported high-precision valve solutions and adoption for pilot-scale electronics manufacturing. Government trade partnerships and industrial development incentives further support market expansion.

China – 20% Market Share: High production capacity and aggressive fab expansion in semiconductor hubs.

United States – 18% Market Share: Strong end-user demand, advanced automation adoption, and regulatory support for high-tech manufacturing.

The Semiconductor Vacuum Control Valves Market is highly competitive, characterized by the presence of over 50 active global players ranging from large multinational corporations to specialized regional manufacturers. The market exhibits a moderately consolidated structure, with the top five companies—Pfeiffer Vacuum, VAT Group AG, ULVAC, Shinko Electric Industries, and MKS Instruments—together accounting for approximately 52% of total market share. Key competitive strategies include strategic partnerships, product launches, mergers, and acquisitions aimed at expanding geographic presence and technological capabilities. Innovation trends such as IoT-enabled smart valves, predictive maintenance systems, and modular valve solutions are increasingly differentiating market leaders. Recent developments highlight a focus on energy-efficient, high-precision diaphragm and gate valves to meet the requirements of advanced semiconductor fabs. Regional expansions, particularly in Asia-Pacific and North America, are supported by investments in cleanroom infrastructure and automated process control. Companies are also leveraging digitalization and Industry 4.0 integration to optimize valve monitoring, reduce downtime, and enhance throughput, further intensifying market competition.

Shinko Electric Industries

MKS Instruments

Brooks Instrument

Edwards Vacuum

Leybold GmbH

Technological advancements in the Semiconductor Vacuum Control Valves Market are reshaping operational efficiency and precision in semiconductor manufacturing. IoT-enabled valves with real-time monitoring capabilities allow fabs to track valve performance continuously, reducing downtime by up to 15% and enhancing preventive maintenance schedules. Modular gate and diaphragm valve systems are increasingly adopted to provide scalability and ease of integration in automated cleanroom environments. Emerging technologies include smart angle valves with digital diagnostics, enabling automated detection of leaks and flow inconsistencies, improving process yield by 10%. Digital twin models and predictive analytics are being integrated to simulate operational conditions and optimize valve configurations before deployment, minimizing process disruptions. Additive manufacturing is being explored for complex valve components to reduce lead times and enhance design flexibility. Regional innovation hubs, particularly in Taiwan, Japan, and the United States, are driving the development of high-precision vacuum control valves capable of supporting sub-nanometer process requirements. These advancements collectively support higher throughput, energy efficiency, and process reliability in semiconductor fabs worldwide.

In March 2023, Pfeiffer Vacuum launched its next-generation HiPace turbopumps integrated with smart diaphragm valves, enhancing semiconductor fab throughput by 12% and reducing unplanned maintenance downtime. Source: www.pfeiffer-vacuum.com

In September 2023, ULVAC expanded its diaphragm valve production line in Japan to meet growing demand for automated vacuum solutions, increasing manufacturing capacity by 18%. Source: www.ulvac.com

In February 2024, VAT Group AG introduced IoT-enabled gate valves with real-time diagnostics for cleanroom fabs, improving leak detection accuracy by 15% and reducing process interruptions. Source: www.vat.ch

In June 2024, Shinko Electric Industries deployed modular high-precision valves in semiconductor assembly lines in South Korea, enhancing operational efficiency and increasing wafer throughput by 10%. Source: www.shinko.co.jp

The scope of the Semiconductor Vacuum Control Valves Market Report encompasses an extensive analysis of market segments, applications, technologies, and geographic regions. The report covers key product types including diaphragm valves, gate valves, angle valves, and butterfly valves, highlighting their adoption in high-precision semiconductor manufacturing and associated cleanroom operations. Applications analyzed include semiconductor fabrication, assembly, testing, and research laboratories, with insights into end-user adoption patterns across enterprise-scale fabs and pilot production facilities. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with detailed market positioning and deployment trends for each region. Technological focus includes IoT-enabled monitoring, predictive maintenance, digital twin modeling, and modular valve systems, emphasizing operational efficiency, contamination control, and energy optimization. The report also addresses emerging trends such as additive manufacturing of valve components, digital diagnostics, and integration with Industry 4.0 processes. Strategic insights on regulatory compliance, sustainability initiatives, and ESG considerations are included to guide investment and operational decisions. Additionally, the report examines competitive strategies, innovation pipelines, and regional consumer behavior variations, providing a holistic view for decision-makers.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 1,864.7 Million |

| Market Revenue (2032) | USD 2,949.7 Million |

| CAGR (2025–2032) | 5.9% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Pfeiffer Vacuum, VAT Group AG, ULVAC, Shinko Electric Industries, MKS Instruments, Brooks Instrument, Edwards Vacuum, Leybold GmbH |

| Customization & Pricing | Available on Request (10% Customization is Free) |