Reports

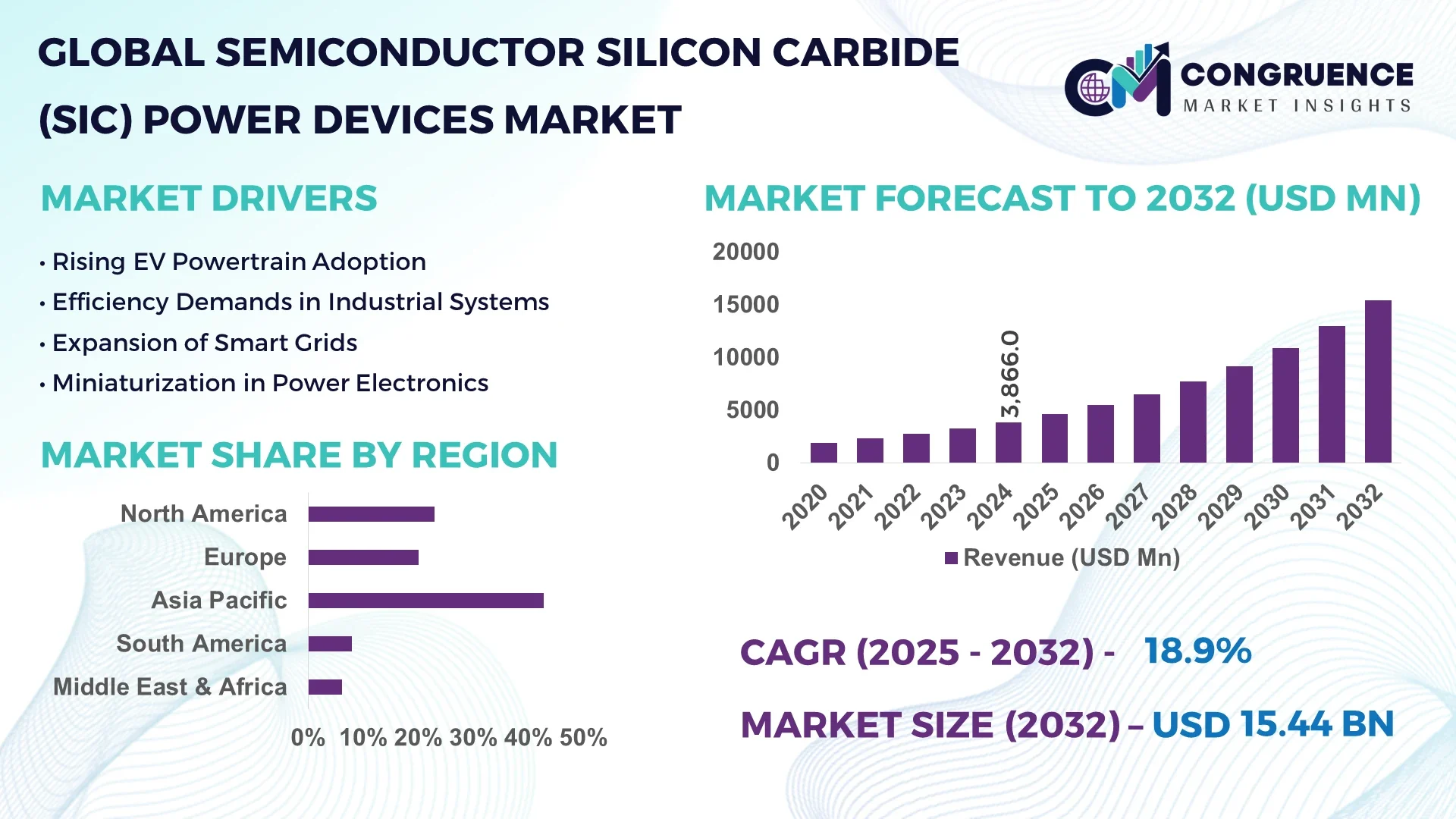

The Global Semiconductor Silicon Carbide (SiC) Power Devices Market was valued at USD 3,866 Million in 2024 and is anticipated to reach a value of USD 15,442.46 Million by 2032 expanding at a CAGR of 18.9% between 2025 and 2032.

The United States leads the Semiconductor Silicon Carbide (SiC) Power Devices market with its advanced fabrication facilities, strong capital investment in high-voltage SiC wafer production, and continued application in electric vehicle (EV) powertrains, smart grids, and renewable energy inverters driven by next-generation manufacturing and R&D advancements.

The Semiconductor Silicon Carbide (SiC) Power Devices market is witnessing robust expansion driven by increasing demand across electric vehicles, industrial motor drives, renewable energy systems, and power supply sectors. Automotive OEMs are integrating SiC MOSFETs and Schottky diodes into onboard chargers and traction inverters to enhance range and reduce system losses. Emerging innovations include high-density SiC modules for industrial robotics and fast-charging infrastructures, along with the introduction of 200mm SiC wafer fabrication lines to improve scalability. Regulatory initiatives focusing on decarbonization and energy efficiency standards are fostering SiC adoption in grid infrastructure and solar inverters. Asia-Pacific and Europe are expanding their consumption of SiC power devices to strengthen EV adoption and industrial efficiency programs. With the evolving electrification of transportation and the deployment of 5G networks, the Semiconductor Silicon Carbide (SiC) Power Devices market is positioned for significant technological upgrades and value chain optimization over the forecast period.

Artificial Intelligence is transforming the Semiconductor Silicon Carbide (SiC) Power Devices Market by accelerating design optimization, defect detection, and predictive maintenance across manufacturing processes. AI-powered analytics are improving wafer quality by identifying microscopic defects in SiC substrates and thin-film layers, reducing scrap rates and enhancing yield rates in production lines. Machine learning models are being utilized to refine device simulation parameters, reducing the development time for new SiC MOSFET and diode architectures used in electric vehicle inverters and industrial power systems. AI-enabled supply chain intelligence tools are optimizing raw material sourcing and logistics for SiC substrates, reducing lead times and operational downtime across fabrication plants. In the Semiconductor Silicon Carbide (SiC) Power Devices Market, AI is also enhancing thermal management modeling in power module designs, ensuring reliable high-voltage operations under varying loads. Additionally, AI-driven predictive analysis is enabling maintenance teams to forecast potential failures in SiC power modules in renewable energy plants and EV charging infrastructures, ensuring operational continuity and cost efficiency. As 5G and IoT deployments require advanced power management systems, AI integration into testing and production workflows is providing precise parametric controls, minimizing variability and ensuring consistent device quality within the Semiconductor Silicon Carbide (SiC) Power Devices Market. The combination of AI with digital twin technologies is further driving real-time monitoring and optimization of high-volume SiC device fabrication and packaging.

“In 2024, a leading SiC manufacturer implemented an AI-powered optical inspection system in its 200mm wafer production line, resulting in a 37% reduction in defect rates and a 22% improvement in yield consistency for automotive-grade SiC MOSFETs.”

The Semiconductor Silicon Carbide (SiC) Power Devices market is evolving rapidly due to rising electrification in transport, industrial automation, and clean energy sectors. Increased deployment of SiC MOSFETs and Schottky diodes in electric vehicle fast-charging stations and industrial motor drives is reshaping the industry’s landscape, emphasizing high efficiency and thermal performance. The market is further influenced by the shift towards wide-bandgap materials, which allow for high-voltage, high-temperature operations with lower switching losses, aligning with sustainability mandates globally. Advances in wafer manufacturing, particularly 200mm SiC wafer lines, are enabling scalability to meet the growing demand in the Semiconductor Silicon Carbide (SiC) Power Devices market while maintaining quality consistency. Additionally, technological advancements in module integration and packaging methods are increasing the adoption of SiC devices in renewable energy inverters and grid infrastructure. These dynamics are driving new opportunities while encouraging global collaboration across supply chains, reshaping the Semiconductor Silicon Carbide (SiC) Power Devices market with improved durability, power density, and operational efficiency.

The accelerated global shift towards electric vehicles is a significant driver in the Semiconductor Silicon Carbide (SiC) Power Devices market. Automakers are increasingly using SiC MOSFETs in traction inverters and onboard chargers, enabling higher power density and extended vehicle range due to reduced energy losses. Additionally, the expansion of fast-charging networks is driving demand for high-voltage SiC devices capable of handling faster charging cycles while maintaining thermal stability. With over 14 million new EV registrations in 2024 globally, there is a parallel surge in the adoption of SiC power devices across the automotive supply chain. SiC devices’ ability to operate efficiently at high switching frequencies and temperatures aligns with the growing need for compact, lightweight designs in EV platforms and charging stations, directly fueling demand in the Semiconductor Silicon Carbide (SiC) Power Devices market.

High production costs and complex manufacturing processes pose a significant restraint in the Semiconductor Silicon Carbide (SiC) Power Devices market. SiC wafer production requires advanced fabrication technologies and high-purity materials, contributing to higher substrate costs compared to traditional silicon wafers. Defect rates during SiC crystal growth and wafer processing also remain higher, leading to lower yields and added operational expenses for manufacturers. Additionally, the challenges associated with scaling up 200mm SiC wafer production and processing to meet high-volume demand without compromising quality further increase capital expenditures. These factors collectively create entry barriers for new players and limit the availability of cost-competitive SiC devices, constraining widespread adoption despite the evident benefits of the Semiconductor Silicon Carbide (SiC) Power Devices market in high-efficiency applications.

The adoption of SiC devices in renewable energy systems and smart grids presents significant opportunities in the Semiconductor Silicon Carbide (SiC) Power Devices market. SiC-based power devices are increasingly used in solar inverters, energy storage systems, and wind power converters due to their ability to handle high voltages and frequencies with minimal energy losses. Global renewable energy installations surpassed 450 GW in 2024, fueling demand for advanced power electronics capable of efficient energy conversion and distribution. Governments worldwide are investing in grid modernization programs to improve energy efficiency and integrate renewable energy sources, creating further opportunities for SiC power devices in high-voltage grid and microgrid applications. The rising emphasis on decarbonization and energy efficiency standards across key regions is expected to accelerate the Semiconductor Silicon Carbide (SiC) Power Devices market growth within the renewable energy and smart grid sectors.

Supply chain limitations and material shortages remain a critical challenge in the Semiconductor Silicon Carbide (SiC) Power Devices market. The specialized nature of SiC substrate production, combined with limited suppliers capable of producing high-quality SiC wafers, creates bottlenecks in the supply chain, particularly during periods of high demand. Geopolitical tensions and restrictions on critical raw material exports can disrupt the availability of high-purity silicon carbide powders, impacting wafer production timelines. The limited availability of specialized equipment for SiC wafer processing and inspection further compounds production constraints. These challenges affect delivery timelines for downstream manufacturers and can lead to increased lead times for automotive and renewable energy customers relying on SiC devices. Addressing these supply chain challenges is essential for ensuring steady growth and scalability in the Semiconductor Silicon Carbide (SiC) Power Devices market.

• Surge in 200mm SiC Wafer Adoption: Manufacturers are accelerating the transition to 200mm SiC wafer production lines to improve scalability in the Semiconductor Silicon Carbide (SiC) Power Devices market. This shift allows for a higher number of devices per wafer, reducing the cost per chip while maintaining quality consistency for automotive and renewable applications. In 2024, several fabs reported over 15% improvement in yield rates during pilot 200mm production, enhancing supply for electric vehicle traction inverters and fast-charging infrastructure.

• Integration in High-Power EV Inverters: The deployment of SiC MOSFETs in 800V electric vehicle architectures is expanding, driven by the need for faster charging and extended driving range. Automakers have reported using SiC devices to achieve up to 7% efficiency gains in traction inverters, reducing energy losses during high-speed operations. This trend is enhancing the competitiveness of SiC devices within the Semiconductor Silicon Carbide (SiC) Power Devices market, aligning with the rising demand for high-voltage electric mobility platforms.

• Advanced Packaging for Thermal Management: Innovations in advanced packaging techniques, such as double-sided cooling and substrate thinning, are reducing thermal resistance in SiC power modules. These methods support higher power density, essential for applications in industrial motor drives and solar inverters. Reports indicate that packaging improvements have led to up to a 20% reduction in operating temperatures under heavy loads, strengthening the operational reliability of devices in the Semiconductor Silicon Carbide (SiC) Power Devices market.

• Integration in Renewable Energy Systems: SiC devices are increasingly integrated into solar inverters, wind turbines, and energy storage systems due to their ability to handle high voltages and switching frequencies efficiently. In 2024, installations of SiC-based inverters in utility-scale solar projects demonstrated a 2% improvement in power conversion efficiency, enabling better utilization of generated solar power. This integration is driving consistent demand within the Semiconductor Silicon Carbide (SiC) Power Devices market, aligning with global clean energy transitions.

The Semiconductor Silicon Carbide (SiC) Power Devices market segmentation includes types, applications, and end-user insights, each defining specific operational and demand characteristics. In terms of types, the market includes SiC MOSFETs, Schottky diodes, hybrid modules, and bare die. Applications span electric vehicle powertrains, renewable energy inverters, industrial motor drives, and power supplies, each contributing to high-voltage and high-efficiency power management. End-user segments include automotive OEMs, renewable energy system integrators, industrial automation providers, and power utilities actively deploying SiC power devices to improve operational efficiency and sustainability targets. The segmentation structure ensures stakeholders can identify the demand clusters, technological adoption rates, and application-specific trends within the Semiconductor Silicon Carbide (SiC) Power Devices market.

The Semiconductor Silicon Carbide (SiC) Power Devices market by type includes SiC MOSFETs, Schottky diodes, hybrid modules, and bare die, each fulfilling critical roles across sectors. SiC MOSFETs lead this segment, driven by their superior high-voltage handling and lower switching losses, widely adopted in electric vehicle powertrains and fast-charging stations due to their ability to extend driving range and improve energy efficiency. The fastest-growing type is hybrid SiC modules, driven by rising demand for integrated solutions combining MOSFETs and diodes in a single package for industrial motor drives and renewable energy inverters, enabling compact and efficient power systems. Schottky diodes remain essential in high-frequency applications, while bare die SiC components support customized module development, especially for R&D in advanced mobility and energy projects. Each type supports the growth trajectory of the Semiconductor Silicon Carbide (SiC) Power Devices market, addressing performance demands in next-generation energy systems.

In the Semiconductor Silicon Carbide (SiC) Power Devices market, applications include electric vehicle powertrains, renewable energy inverters, industrial motor drives, power supplies, and rail traction systems. Electric vehicle powertrains lead the application segment, supported by the transition to 800V architectures, where SiC devices enhance power density, enable faster charging, and reduce energy losses during operation. Renewable energy inverters represent the fastest-growing application, driven by the increasing deployment of utility-scale solar and wind projects that require high-efficiency energy conversion to support grid stability. Industrial motor drives continue to use SiC devices for high-speed, energy-efficient operations, while power supply systems leverage SiC’s high-frequency performance in data centers and telecom infrastructure. Rail traction systems are adopting SiC modules for regenerative braking and efficient acceleration, expanding the application diversity within the Semiconductor Silicon Carbide (SiC) Power Devices market.

End-users in the Semiconductor Silicon Carbide (SiC) Power Devices market include automotive OEMs, renewable energy integrators, industrial automation companies, power utilities, and transportation infrastructure providers. Automotive OEMs are the leading end-user segment, actively deploying SiC devices in electric vehicles to improve driving range and powertrain efficiency while supporting lightweight vehicle design strategies. Renewable energy system integrators are the fastest-growing end-user segment, driven by global investments in solar and wind energy projects that require advanced power conversion systems for efficient grid integration. Industrial automation companies are incorporating SiC modules in motor drives and robotics to reduce energy consumption while increasing operational speeds. Power utilities are adopting SiC devices for smart grid applications and high-voltage distribution, while transportation infrastructure providers utilize SiC devices in rail and fast-charging networks, collectively shaping the demand landscape in the Semiconductor Silicon Carbide (SiC) Power Devices market.

Asia-Pacific accounted for the largest market share at 42.8% in 2024 however, North America is expected to register the fastest growth, expanding at a CAGR of 19.5% between 2025 and 2032.

The Semiconductor Silicon Carbide (SiC) Power Devices market in Asia-Pacific is witnessing significant volume growth due to large-scale electric vehicle manufacturing hubs in China, Japan, and South Korea, coupled with increasing deployment of SiC-based inverters in renewable energy projects across India and Southeast Asia. The region benefits from the presence of advanced semiconductor fabs and local supply chains, supporting high-volume SiC wafer production and device integration. Across key consuming sectors, including automotive, renewable energy, and industrial automation, SiC device adoption is driven by the need for high-efficiency power conversion and compact designs. The Semiconductor Silicon Carbide (SiC) Power Devices market in Asia-Pacific is further supported by government electrification programs, local subsidies for EV infrastructure, and increasing investments in smart grids, driving consistent demand and technology advancement across the region.

North America holds a 28.3% market share within the Semiconductor Silicon Carbide (SiC) Power Devices market, driven by strong electric vehicle production, renewable energy system integration, and industrial automation. Key industries such as automotive, energy storage, and aerospace are pushing demand for high-efficiency SiC MOSFETs and diodes for power management and thermal efficiency. The region has seen notable government incentives supporting EV manufacturing and charging infrastructure, including federal tax credits and state-level grants, driving SiC device adoption. Technological advancements in digital twin simulations and AI-enhanced wafer inspection are accelerating SiC fabrication quality, while regulatory initiatives around decarbonization are boosting the deployment of SiC-based power systems in the Semiconductor Silicon Carbide (SiC) Power Devices market.

Europe captures a 21.7% market share in the Semiconductor Silicon Carbide (SiC) Power Devices market, with Germany, France, and the UK being major contributors due to strong EV penetration and renewable energy investments. European regulatory bodies are enforcing sustainability initiatives such as Fit for 55, promoting the adoption of low-loss power electronics in transport and grid infrastructure. Technological integration of SiC devices in rail electrification and offshore wind inverters is advancing rapidly, supported by research funding and industrial collaborations. The Semiconductor Silicon Carbide (SiC) Power Devices market in Europe benefits from smart grid expansions and widespread electric mobility initiatives, which are accelerating the use of high-voltage SiC devices for efficient power conversion and reduced carbon footprints.

Holding the highest volume globally, the Asia-Pacific Semiconductor Silicon Carbide (SiC) Power Devices market leads in consumption with China, Japan, and India as top consumers, driven by expanding EV production, renewable deployments, and high-speed rail electrification. Regional manufacturing trends include the establishment of advanced 200mm SiC wafer fabs and vertical integration across the SiC value chain, supporting scalability and cost reduction. The region’s technology hubs are advancing SiC module design for compact, efficient power systems in industrial robotics and solar inverters. This environment fosters strong innovation, propelling demand within the Semiconductor Silicon Carbide (SiC) Power Devices market while supporting regional clean energy and electrification goals.

Brazil and Argentina are key countries within the South America Semiconductor Silicon Carbide (SiC) Power Devices market, which holds a regional market share of 3.8%. The region is witnessing a growing focus on electrification of transportation and industrial operations, with increasing investment in solar and wind energy projects that require high-efficiency SiC inverters for effective power management. Infrastructure upgrades in transmission networks are encouraging the use of SiC devices for reduced energy losses, supporting sustainability efforts. Government incentives for local manufacturing of clean energy equipment and EV components further strengthen the Semiconductor Silicon Carbide (SiC) Power Devices market’s expansion across South America.

The Middle East & Africa Semiconductor Silicon Carbide (SiC) Power Devices market is driven by regional demand across the oil & gas, renewable energy, and construction sectors, with UAE and South Africa emerging as major growth countries. The market is expanding as governments implement energy efficiency mandates and diversify energy sources with solar and wind projects that require reliable SiC power devices for grid integration and power management. Technological modernization in industrial operations and the adoption of digital monitoring systems in the energy sector are promoting the use of SiC modules for efficient thermal and electrical management. Local regulations supporting renewable energy development further support demand within the Semiconductor Silicon Carbide (SiC) Power Devices market across the region.

China: 36.2% market share

High production capacity and robust electric vehicle demand drive China’s dominance in the Semiconductor Silicon Carbide (SiC) Power Devices market.

United States: 23.5% market share

Strong end-user demand across EV, aerospace, and industrial sectors, coupled with advanced manufacturing infrastructure, positions the United States as a leader in the Semiconductor Silicon Carbide (SiC) Power Devices market.

The Semiconductor Silicon Carbide (SiC) Power Devices market is characterized by intense competition with over 45 active global and regional players focusing on SiC MOSFETs, Schottky diodes, and integrated power modules. Key competitors are pursuing vertical integration to secure wafer supply, improve device quality, and scale 200mm wafer production lines to meet increasing demand from electric vehicle, renewable energy, and industrial sectors. Strategic initiatives such as joint ventures between SiC wafer manufacturers and automotive OEMs are shaping market positioning, enabling secured long-term supply for EV applications. Leading players are advancing their portfolios through new product launches featuring higher voltage ratings, improved thermal management, and compact module designs targeting fast-charging and industrial motor drive systems. Collaborative research projects on advanced packaging technologies and AI-enabled wafer inspection systems are fostering innovation within the Semiconductor Silicon Carbide (SiC) Power Devices market. Mergers and partnerships are being utilized to expand geographic reach and manufacturing capacities, while companies are also investing in localized production to mitigate supply chain challenges and address regional electrification goals.

Wolfspeed, Inc.

ROHM Co., Ltd.

STMicroelectronics N.V.

Infineon Technologies AG

ON Semiconductor Corporation

Mitsubishi Electric Corporation

Fuji Electric Co., Ltd.

Littelfuse, Inc.

Microchip Technology Inc.

Toshiba Electronic Devices & Storage Corporation

GeneSiC Semiconductor Inc.

UnitedSiC (now part of Qorvo, Inc.)

The Semiconductor Silicon Carbide (SiC) Power Devices market is evolving through the adoption of advanced wafer technologies, innovative device structures, and precision packaging to meet the rising demand for high-efficiency power conversion across electric vehicles, renewable energy, and industrial automation sectors. The shift to 200mm SiC wafer fabrication is a major technological milestone, enabling higher device yields per wafer while maintaining crystal quality essential for high-voltage applications. This transition is complemented by the deployment of fourth-generation SiC MOSFETs with reduced RDS(on) and enhanced short-circuit robustness, supporting fast-switching, high-frequency operations in EV traction inverters and industrial motor drives.

New advancements in trench MOSFET and planar MOSFET structures are reducing switching losses while maintaining thermal stability during heavy load cycles. Integrated SiC Schottky diodes and MOSFET hybrid modules are being developed for compact, high-power density solutions, addressing space and efficiency needs in fast-charging infrastructures and onboard EV chargers. Precision packaging innovations, such as double-sided cooling and substrate thinning, are further optimizing thermal management, ensuring reliable performance under high-temperature operations.

AI-powered wafer inspection and defect detection technologies are enhancing yield rates by identifying micro-level crystal defects early in the production process. Integration of digital twin simulations and real-time monitoring systems is improving predictive maintenance and production precision. Collectively, these technologies are positioning the Semiconductor Silicon Carbide (SiC) Power Devices market to support the next generation of electrified transportation, advanced renewable systems, and high-efficiency industrial operations while aligning with global decarbonization and energy efficiency goals.

• In March 2023, Wolfspeed inaugurated its new 200mm Silicon Carbide wafer fabrication facility in New York, designed to increase production capacity for high-voltage SiC devices used in electric vehicle and renewable energy applications, enhancing North America’s SiC supply chain resilience.

• In September 2023, Infineon Technologies launched its CoolSiC™ MOSFET 650V G2 series with optimized RDS(on) and reduced switching losses, targeting fast-charging and solar inverter markets to enable high-efficiency, compact power module designs for advanced energy systems.

• In February 2024, ROHM announced the development of its fourth-generation SiC MOSFETs featuring a 40% reduction in on-resistance and improved short-circuit withstand capabilities, intended for next-generation electric vehicle traction inverters and industrial motor drive systems.

• In May 2024, STMicroelectronics began pilot production of 200mm SiC wafers at its Italian facility, achieving high-quality substrate consistency aimed at meeting the rising demand for SiC-based devices in automotive and industrial power electronics across Europe and Asia.

The Semiconductor Silicon Carbide (SiC) Power Devices Market Report provides an extensive analysis of SiC MOSFETs, Schottky diodes, hybrid modules, and bare die used across critical sectors including electric vehicles, renewable energy inverters, industrial motor drives, power supplies, and transportation infrastructure. Covering over 25 countries across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, the report examines the distribution of manufacturing hubs, technological readiness, and consumption patterns for SiC power devices within regional energy transition and electrification initiatives.

This report outlines the adoption of 200mm SiC wafer manufacturing and the emergence of advanced packaging solutions such as double-sided cooling, supporting high-frequency and high-voltage operations. It explores industry focus areas including integration of SiC devices in 800V EV architectures, utility-scale solar inverters, rail electrification, and industrial robotics requiring compact, high-efficiency power conversion systems.

Additionally, the Semiconductor Silicon Carbide (SiC) Power Devices Market Report highlights trends in localized production, investment in supply chain resilience, and technological collaborations across OEMs and semiconductor manufacturers. The scope includes the analysis of evolving end-user demands for sustainable and efficient power management solutions and tracks emerging niche segments such as aerospace electrification, high-speed rail, and advanced data center power systems where SiC power devices are increasingly relevant for supporting operational reliability and energy efficiency objectives globally.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 3866 Million |

|

Market Revenue in 2032 |

USD 15442.46 Million |

|

CAGR (2025 - 2032) |

18.9% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Wolfspeed, Inc., ROHM Co., Ltd., STMicroelectronics N.V., Infineon Technologies AG, ON Semiconductor Corporation, Mitsubishi Electric Corporation, Fuji Electric Co., Ltd., Littelfuse, Inc., Microchip Technology Inc., Toshiba Electronic Devices & Storage Corporation, GeneSiC Semiconductor Inc., UnitedSiC (now part of Qorvo, Inc.) |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |