Reports

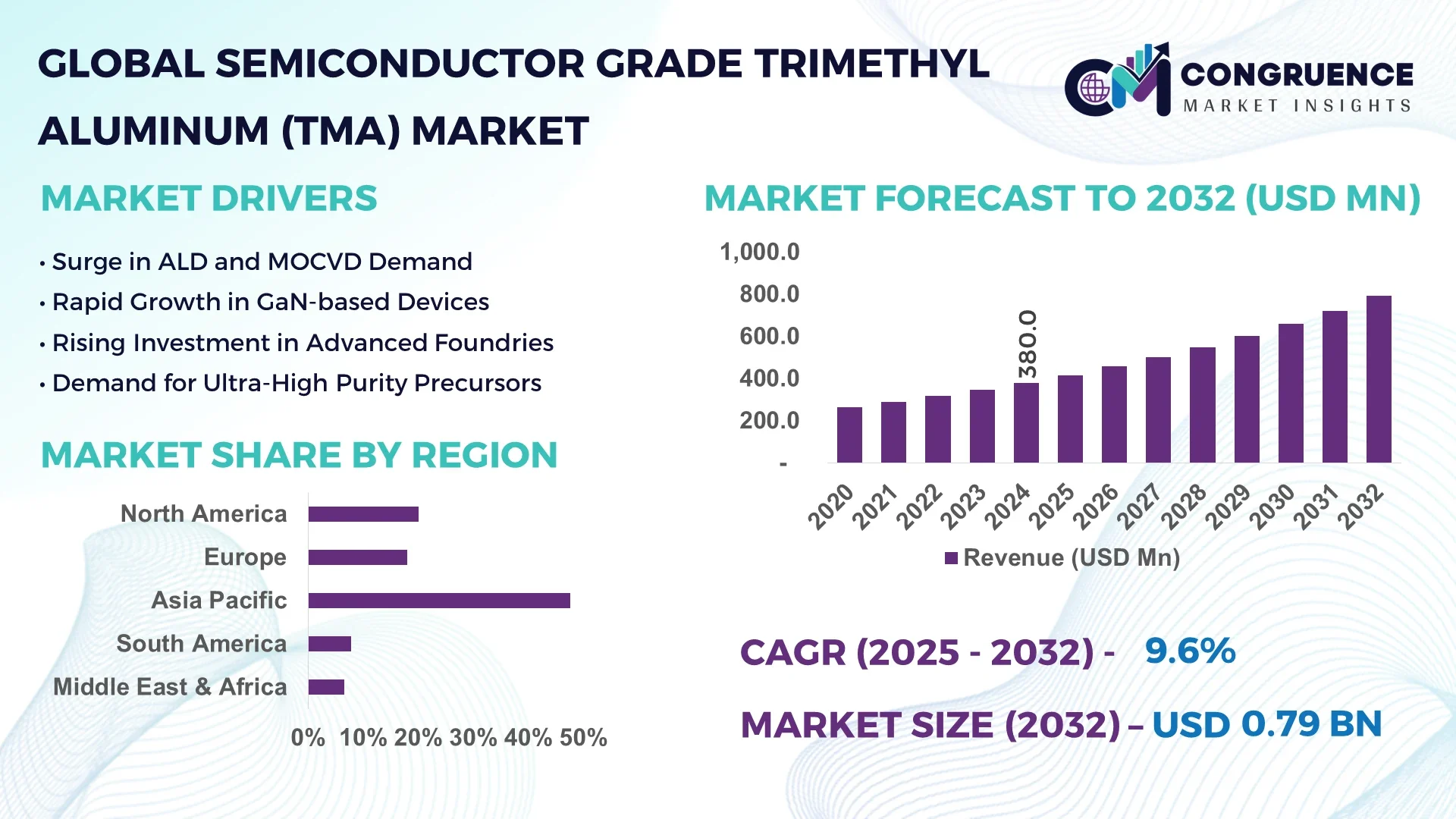

The Global Semiconductor Grade Trimethyl Aluminum (TMA) Market was valued at USD 380 Million in 2024 and is anticipated to reach a value of USD 791.2 Million by 2032 expanding at a CAGR of 9.6% between 2025 and 2032.

China leads production capacity with more than 5,000 metric tons of semiconductor-grade TMA produced annually. In 2024, targeted investment in purification infrastructure exceeded USD 45 million. Significant applications include atomic layer deposition in advanced 5nm logic foundries and high-k dielectric gate stacks. Technological upgrades involve dual-stage distillation and inline purity monitoring, enabling impurity reduction below 0.05 ppm.

Major application sectors include semiconductor fabrication, LED production, solar cell manufacturing, and RFID device assembly. ALD and chemical vapor deposition (CVD) processes account for approximately 78% of total TMA consumption, while LED chip production uses around 18% of volumes. Regulatory frameworks related to chemical handling and transport have spurred adoption of cylinder-traceability systems and end-to-end supply chain compliance. Asia-Pacific remains the largest consumer regionally, while expansion in North America, driven by CHIPS Act incentives, is boosting domestic demand. Emerging trends include contracts between IDMs and material suppliers and exploration of less pyrophoric precursor alternatives. The market outlook anticipates steady uptake in both existing and novel applications, supported by process miniaturization and sustainability investments.

AI applications are reshaping the Semiconductor Grade Trimethyl Aluminum (TMA) Market through intelligent process control, enhanced traceability, and quality assurance. Production plants are deploying AI-driven process analytics to monitor reaction chamber conditions in real time, reducing impurity deviations by up to 60%. Packaging units now use machine-learning algorithms to verify cylinder seal integrity, reducing leakage incidents by over 40% through anomaly detection.

Operational efficiency has improved through AI-based predictive maintenance systems. One facility reported cutting unplanned downtime by 35% by analyzing thermal sensor data and adjusting heater cycles during distillation processes. The Semiconductor Grade Trimethyl Aluminum (TMA) Market benefits from this reduced downtime, particularly in precision purification equipment.

In supply-chain operations, AI-driven demand forecasting has optimized inventory levels of high-purity TMA, reducing safety stock by 22% while still meeting fab demand spikes. This translates into cost savings and fewer disruptions in manufacturing flows. Quality control has also been enhanced; computer vision systems now inspect cylinder filling volumes and valve alignment with 98% accuracy, reducing rejection rates. As advanced packaging and plasma-based deposition technologies evolve, AI is enabling tighter control down to atomic-level precursor specifications.

The Semiconductor Grade Trimethyl Aluminum (TMA) Market is thus integrating AI across the full lifecycle—from raw-material purification to final delivery—yielding gains in safety, reliability, and operational excellence tailored to high-end semiconductor manufacturing.

“In late 2024, a major precursor supplier implemented AI surveillance during ALD precursor filtration, reducing particulate contamination by 70% and increasing batch throughput by roughly 18%.”

The Semiconductor Grade Trimethyl Aluminum (TMA) Market is experiencing dynamic shifts driven by advanced fab construction, purity-driven process demands, and safety compliance pressures. Major trends include integration of high-capacity distillation units and spin-transfer packaging systems suited for ultra-pure applications. Influences such as semiconductor node scaling to 3nm and expansion in LED fabrication continue to fuel material demand. Downsides include volatility in feedstock chemicals and stringent handling safety regulations. Environmental and economic factors, including chemical storage standards and trade policies, also play significant roles. Industry consolidation and contract agreements between foundries and chemical suppliers are redefining supply chain resilience. Overall, demand is shaped by technological sophistication, regulatory complexity, and strategic alliances within the Semiconductor Grade Trimethyl Aluminum (TMA) Market.

Transition to sub-7nm and 5nm technologies necessitates use of ALD processes where TMA is essential. Over 92% of new 3nm-capable fabs now incorporate TMA-based ALD systems. In 2024, there were more than 3,100 ALD tools globally deploying TMA as a precursor, underscoring demand from process miniaturization.

TMA’s pyrophoric nature demands rigorous handling protocols. In 2023, fourteen reported fire or leak incidents highlighted the risk margin. Strict safety protocols—such as argon blanketing, stainless steel cylinders, and inert glove boxes—add complexity and capital cost, limiting accessibility to smaller-scale manufacturers.

Long-term growth is supported by memory-industry demand. In 2024, approximately 30% of global 3D NAND chips—over 1.5 billion units—used TMA-enhanced ALD stacks. Memory module fabrication, especially for DRAM and NAND, is estimated to drive demand toward 500 metric tons annually by 2026.

Ultra-high purity TMA (≥ 6N) production is concentrated among fewer than ten global producers. A 2023 supply disruption in Europe caused a month-long backlog across several fabs. Even trace contaminants—such as water at 0.1 ppm—can compromise chip quality, increasing supply-chain vulnerability.

Widespread Adoption of ALD in 5nm and Below Fabs: As of 2024, ALD equipment using TMA is deployed in over 61% of fabs capable of 5nm production. Expansion of these fabs across Asia and North America has placed premium focus on TMA supply and consistency, with new contracts signed for multi-year supply.

Increasing Use in LED and GaN Device Fabrication: In 2023, TMA consumption in GaN LED manufacturing rose by 12%, reaching approximately 610 metric tons, indicating a widening application scope in optoelectronics.

Vertical Integration Between Foundries and Chemical Suppliers: By the end of 2024, three of the top-five global foundries entered long-term supply agreements with precursor manufacturers, hedging against supply chain disruptions and ensuring dedicated TMA processing capacity.

Emergence of Safer Precursor R&D Initiatives: In late 2023, over 18 research projects were initiated globally to develop less pyrophoric aluminum precursors, aiming to match TMA’s deposition properties while improving handling safety—though none have reached commercial scale as of 2024.

The Semiconductor Grade Trimethyl Aluminum (TMA) Market is strategically segmented based on type, application, and end-user, reflecting the industry's complex technological demands and process specialization. Segmentation by type includes varying purity levels and packaging formats, enabling customization for different fabrication technologies. Application-wise, TMA is utilized across ALD, CVD, and other high-precision processes supporting semiconductor, optoelectronic, and photovoltaic device manufacturing. End-users include foundries, IDMs, and OEMs involved in producing logic chips, memory devices, compound semiconductors, and display panels. Each segment exhibits distinct adoption trends influenced by regional fab development, evolving technological nodes, safety handling standards, and end-product requirements. This segmentation offers valuable insights into emerging investment pockets and process-specific consumption patterns in the TMA value chain.

Semiconductor grade TMA is generally segmented into 6N purity, ultra-high purity (UHP) grades, and custom-packaged variants. The 6N purity segment leads the market due to its compatibility with advanced ALD processes required for high-performance logic and memory applications. These grades deliver minimal metallic and oxygen impurities, essential for sub-5nm node integration.

The fastest-growing type is the ultra-high purity packaged variant, often supplied in high-pressure stainless-steel cylinders with integrated leak detection systems. This growth is driven by strict safety and purity requirements for emerging compound semiconductor and AI processor fabrication, where even 0.01 ppm deviations can impact yield.

Other notable types include cylinder-traceable variants used in cleanroom automation and bulk-delivery systems for high-volume fabs. While niche, these variants play a crucial role in facilities prioritizing automated refill and traceability protocols to reduce human intervention and contamination risk.

TMA plays a pivotal role in atomic layer deposition (ALD) and chemical vapor deposition (CVD) processes. Among these, ALD dominates due to its critical importance in forming ultra-thin oxide layers and high-k dielectrics in sub-7nm semiconductor manufacturing. ALD processes using TMA are widely adopted across logic, DRAM, and FinFET fabrication.

The fastest-growing application is in gallium nitride (GaN)-based device manufacturing, particularly in the LED and power electronics segments. Increasing adoption of GaN technologies in electric vehicles and RF communication has amplified the demand for high-purity TMA in high-k/low-k dielectric layer formation.

Other applications include solar cells, especially for passivated emitter and rear contact (PERC) cells, where TMA is used in surface treatments. RFID and compound semiconductor fabrication are emerging as important use cases, driven by expanding IoT and 5G infrastructure, both of which require precision deposition technologies where TMA is a key precursor.

The leading end-user of semiconductor grade TMA is the integrated device manufacturers (IDMs) segment. These vertically integrated companies operate high-volume fabs requiring consistent TMA supply for process stability and yield control. Their in-house purification systems and strict audit protocols necessitate high-grade TMA aligned with fab-specific process design kits (PDKs).

The fastest-growing end-user segment is specialty foundries and compound semiconductor fabs, especially those producing GaN and SiC-based devices for automotive and power grid applications. Their rapid scale-up is fueled by increasing demand for high-efficiency devices and regional government support for semiconductor independence.

Other significant end-users include third-party OEMs, research laboratories, and fabless-design outsourcing companies. These groups contribute to niche demand, particularly in prototyping, pilot lines, and R&D programs. Their consumption, although lower in volume, emphasizes flexibility, speed of delivery, and packaging innovation within the broader TMA ecosystem.

Asia-Pacific accounted for the largest market share at 47.6% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 10.5% between 2025 and 2032.

Asia-Pacific continues to dominate the Semiconductor Grade Trimethyl Aluminum (TMA) Market due to its vast semiconductor manufacturing infrastructure and significant investment in advanced chip fabrication technologies. Countries like China, South Korea, Japan, and Taiwan lead in consumption volumes, fueled by the presence of world-leading foundries and memory producers. North America, on the other hand, is witnessing rapid momentum due to federal semiconductor funding, increased fab construction, and growing self-reliance in materials sourcing. The region's expansion is further accelerated by collaborations between chemical manufacturers and semiconductor giants for secure precursor supply chains. Across Europe and emerging markets, moderate yet stable growth is supported by digitalization and energy-efficient electronic infrastructure. Each region presents distinct opportunities shaped by industrial policy, fab activity, and technology adoption.

North America held a significant 24.3% share of the global Semiconductor Grade Trimethyl Aluminum (TMA) Market in 2024. The region’s demand is primarily driven by logic chip production, advanced node development, and expansion of AI and automotive semiconductor facilities. The CHIPS and Science Act has allocated substantial federal funding to support domestic manufacturing, directly benefiting precursor demand. The U.S. leads in fab construction projects, including multiple 5nm and 3nm nodes that require TMA in atomic layer deposition processes. Technological innovation includes AI-integrated TMA purification systems and automated distribution solutions. Regulatory frameworks from the Environmental Protection Agency and Department of Transportation have also enhanced safety protocols for TMA storage and logistics. Increasing investments in fab automation and digital twins further strengthen the region’s reliance on high-purity materials like TMA.

Europe accounted for approximately 15.1% of the Semiconductor Grade Trimethyl Aluminum (TMA) Market in 2024. Key contributors include Germany, France, and the Netherlands, driven by the presence of R&D-intensive chip manufacturers and equipment providers. The EU’s push toward green semiconductor manufacturing has encouraged adoption of recyclable TMA packaging and environmentally compliant processes. Regulatory bodies like REACH and ECHA are enforcing tighter chemical safety standards, pushing innovation in packaging integrity and traceability. Emerging technologies in GaN and SiC device fabrication, particularly in automotive and energy sectors, are increasing the regional demand for ultra-high purity TMA. Europe also benefits from robust cross-border collaboration between universities, fabs, and chemical suppliers to optimize precursor usage and minimize emissions.

Asia-Pacific leads the global Semiconductor Grade Trimethyl Aluminum (TMA) Market with a commanding 47.6% share in 2024. China, South Korea, Taiwan, and Japan represent the top consumers of TMA due to their dense concentration of semiconductor fabs. These countries host the largest memory and foundry players globally, who rely heavily on TMA for ALD processes. Infrastructure advancements include megafab complexes, on-site precursor production, and localized logistics networks ensuring uninterrupted supply. Innovation hubs in Shanghai, Hsinchu, and Seoul are fostering next-generation material research, including safer and purer TMA formulations. Government-backed tech parks and industrial zones further support high-volume production and R&D. The region’s position is reinforced by strong OEM integration and a skilled semiconductor workforce.

South America contributed roughly 4.2% to the global Semiconductor Grade Trimethyl Aluminum (TMA) Market in 2024, with Brazil and Argentina leading the regional demand. While small in volume, the market is growing due to the emergence of domestic electronics manufacturing clusters and increasing semiconductor import substitution policies. Government-backed R&D grants and industrial incentives have supported pilot fabs and specialty device facilities. The region is also leveraging its strength in energy infrastructure to support power electronics that use GaN-based technologies requiring TMA deposition. Infrastructure challenges remain, but ongoing bilateral agreements with global suppliers are improving access to semiconductor-grade materials and encouraging investment in local cleanroom infrastructure.

Middle East & Africa represented approximately 3.8% of the global Semiconductor Grade Trimethyl Aluminum (TMA) Market in 2024. The UAE and South Africa are leading regional adoption, driven by diversification strategies that include semiconductor assembly and packaging lines. Free trade zones such as Dubai Silicon Oasis are attracting foreign investment and fostering local chip component production. Regional demand is also influenced by smart city initiatives and high-tech infrastructure requiring localized manufacturing of sensor-based electronics. TMA is used in selective ALD applications in these contexts. Regulatory enhancements, such as chemical traceability systems and safety standards enforcement, are promoting safe TMA handling. Additionally, partnerships with European and Asian suppliers are helping build regional capabilities in precursor distribution and tech transfer.

China – 31.2% Market Share

High production capacity and proximity to leading memory and foundry fabs drive China's dominance in the Semiconductor Grade Trimethyl Aluminum (TMA) Market.

United States – 24.3% Market Share

Strong end-user demand from advanced-node fabs and policy-driven semiconductor expansion fuel the U.S. leadership in the Semiconductor Grade Trimethyl Aluminum (TMA) Market.

The Semiconductor Grade Trimethyl Aluminum (TMA) Market is characterized by a moderately consolidated competitive environment with approximately 12 to 15 globally active producers, alongside several regional and niche suppliers. Leading players focus on maintaining ultra-high purity standards, stable supply chains, and customized packaging solutions tailored to advanced semiconductor node requirements. Competitive differentiation is increasingly based on purity levels, container technology, delivery systems, and value-added services such as fab integration and on-site refilling support.

Strategic initiatives are shaping market dynamics, including multi-year supply agreements with Tier 1 semiconductor fabs, mergers to consolidate manufacturing capacity, and joint ventures focused on regional production facilities. For instance, new production lines have been established in East Asia and the U.S. to support fab expansions. Companies are also investing in traceable packaging, AI-based monitoring systems, and digital logistics for enhanced safety and real-time inventory management.

Innovation remains central to competition, particularly around advanced ALD-specific formulations and the development of next-generation TMA alternatives for compound semiconductors. Moreover, companies are collaborating with equipment manufacturers to optimize precursor flow systems and ensure compatibility with evolving toolsets. The market is expected to remain highly competitive with increasing emphasis on localization, ESG compliance, and smart delivery mechanisms.

Nouryon

Albemarle Corporation

UP Chemical Co., Ltd.

SAFC Hitech (a division of Merck KGaA)

Linde plc

Jiangsu Nata Opto-electronic Material Co., Ltd.

Suzhou Xiangcheng Youxian Electronic Material Co., Ltd.

Tanfac Industries Limited

AkzoNobel Specialty Chemicals

Taiyo Nippon Sanso Corporation

Technological advancements in the Semiconductor Grade Trimethyl Aluminum (TMA) Market are primarily driven by the growing need for ultra-high purity deposition precursors compatible with sub-5nm and future sub-2nm nodes. A key area of innovation lies in advanced atomic layer deposition (ALD) and chemical vapor deposition (CVD) processes, where TMA is used for precise oxide film formation, critical for logic and memory devices. These deposition techniques demand TMA with purity levels exceeding 99.9999% and minimal trace metals or hydrocarbons.

Another significant development is in container and delivery system technology. Smart containers with integrated pressure monitoring, traceability tags, and inert gas purging mechanisms are enhancing safety and handling in fab environments. New materials used in cylinder coatings prevent contamination and extend shelf life. Digitized supply chain tools now enable real-time TMA usage tracking across fabs, improving process optimization and reducing waste.

In addition, AI-integrated precursor control systems are being adopted to ensure optimal flow rates and predictive maintenance. These systems reduce downtime and improve material utilization efficiency in high-volume manufacturing. Emerging trends also include research into alternative precursors for compound semiconductor deposition, particularly for GaN and SiC applications, expanding the role of TMA in power electronics and photonics.

Furthermore, sustainability is influencing technology choices, with increasing emphasis on recyclable containers, reduced hazardous emissions, and greener synthesis processes. Collectively, these innovations ensure that the TMA supply chain remains resilient, efficient, and aligned with the evolving needs of next-gen semiconductor devices.

In March 2024, Nouryon announced the commissioning of a new ultra-high purity TMA production unit in Texas to support domestic semiconductor fabs, enabling localized supply and reducing trans-Pacific dependency.

In December 2023, Merck KGaA launched a smart logistics platform for its SAFC Hitech line, enhancing traceability and safety compliance for TMA deliveries using real-time IoT tracking across multiple fab partners.

In May 2024, UP Chemical partnered with a major South Korean foundry to co-develop custom ALD precursors, including advanced TMA formulations tailored for high-k dielectric deposition in AI chip manufacturing.

In October 2023, Taiyo Nippon Sanso unveiled a next-generation TMA container system with improved thermal insulation and automated leak detection, boosting safety and stability during high-volume semiconductor processing.

The Semiconductor Grade Trimethyl Aluminum (TMA) Market Report provides a comprehensive analysis of key market segments, geographies, applications, and technologies shaping the global landscape. It covers segmentation by type (e.g., 6N purity, ultra-high purity, custom packaging), application (e.g., ALD, CVD, GaN device fabrication), and end-user categories such as IDMs, foundries, and OEMs.

Geographically, the report spans five key regions—North America, Europe, Asia-Pacific, South America, and Middle East & Africa—highlighting both mature and emerging semiconductor markets. Each region’s industrial trends, fab infrastructure, and material sourcing strategies are examined in detail.

Technological focus includes the use of TMA in advanced node logic chips, memory, compound semiconductors, and optoelectronics. It also reviews the evolution of container systems, delivery automation, and AI-driven fab integration tools. Environmental and safety considerations, such as regulatory standards for hazardous chemical transport and sustainable packaging, are also discussed.

This report offers actionable insights for industry stakeholders including material manufacturers, fab operators, equipment vendors, and government policymakers. It serves as a strategic tool to assess innovation trends, competitive positioning, supply chain dynamics, and future investment opportunities within the global Semiconductor Grade Trimethyl Aluminum (TMA) Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 380.0 Million |

| Market Revenue (2032) | USD 791.2 Million |

| CAGR (2025–2032) | 9.6% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Market Drivers & Restraints, Technology Insights, Market Dynamics, Segment Analysis, Regional and Country Insights, Competitive Landscape, Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Nouryon, Albemarle Corporation, UP Chemical Co., Ltd., SAFC Hitech (a division of Merck KGaA), Linde plc, Jiangsu Nata Opto-electronic Material Co., Ltd., Suzhou Xiangcheng Youxian Electronic Material Co., Ltd., Tanfac Industries Limited, AkzoNobel Specialty Chemicals, Taiyo Nippon Sanso Corporation |

| Customization & Pricing | Available on Request (10% Customization is Free) |