Reports

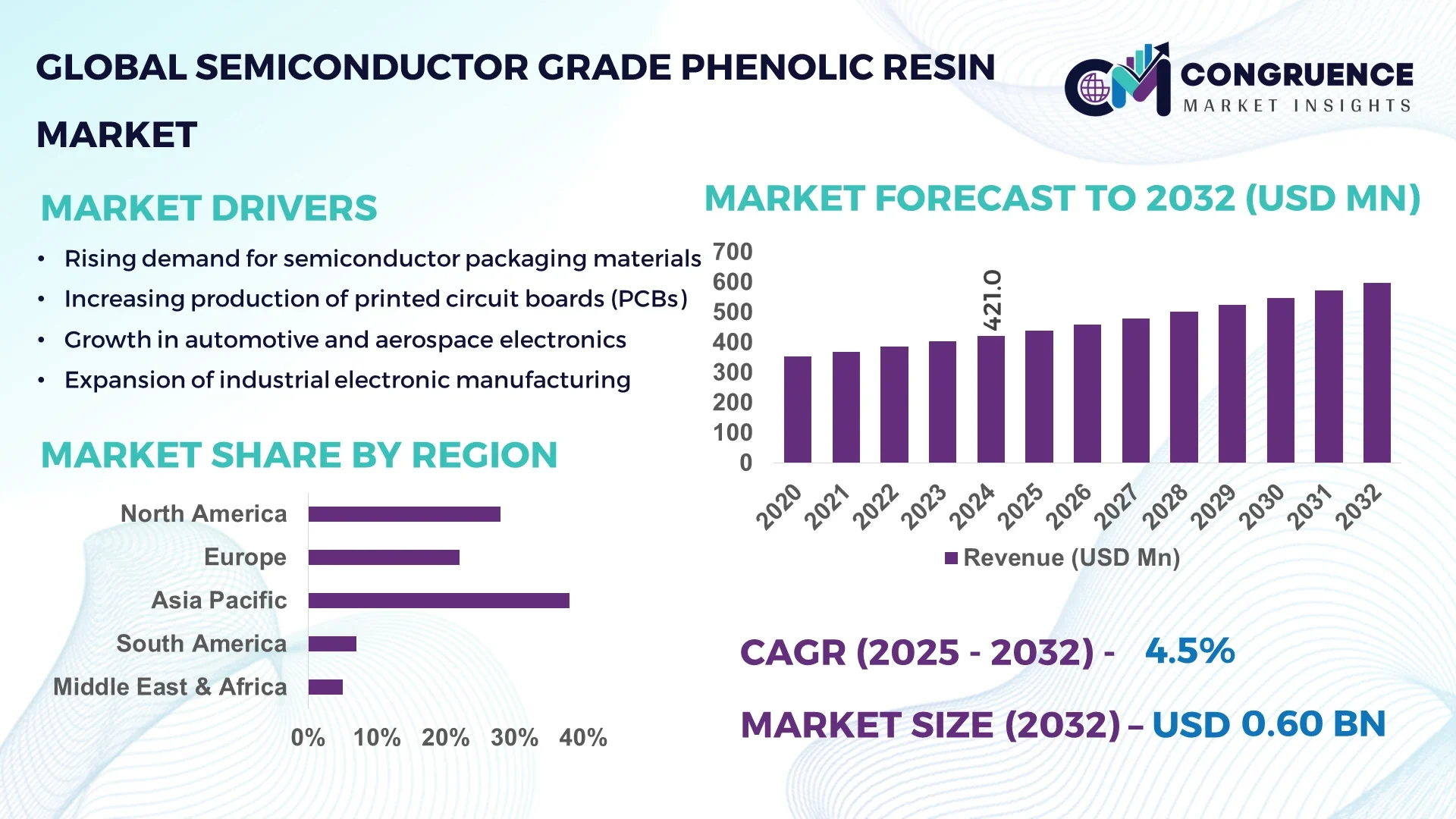

The Global Semiconductor Grade Phenolic Resin Market was valued at USD 421 Million in 2024 and is anticipated to reach a value of USD 598.7 Million by 2032, expanding at a CAGR of 4.5% between 2025 and 2032, driven by increasing demand for high-performance electronic components and advanced substrate applications.

China leads the global Semiconductor Grade Phenolic Resin Market, with annual production capacity exceeding 150,000 metric tons. The country has invested over USD 500 million in advanced resin production facilities and R&D centers dedicated to high-temperature-resistant and low-outgassing phenolic resins. Key applications include semiconductor substrates, printed circuit boards, and insulation for high-density electronics. Technological advancements include integration of nano-fillers to enhance thermal stability and flame retardancy, with pilot plants achieving up to 20% efficiency improvements in resin curing processes. Regional consumption patterns indicate that over 60% of produced resins are utilized in electronics manufacturing hubs in the Yangtze River Delta and Pearl River Delta regions.

Market Size & Growth: The market was USD 421 Million in 2024, projected to reach USD 598.7 Million by 2032, driven by rising semiconductor packaging demand.

Top Growth Drivers: Adoption of high-performance substrates (32%), demand for miniaturized electronics (28%), enhanced thermal stability requirements (25%).

Short-Term Forecast: By 2028, resin curing efficiency is expected to improve by 15%, reducing production cycle time.

Emerging Technologies: Nano-filler integration, high-temperature-resistant resin formulations, automated resin curing systems.

Regional Leaders: China USD 210 Million by 2032 with high-volume production adoption; North America USD 145 Million focusing on aerospace applications; Europe USD 120 Million driven by electronics precision and green manufacturing adoption.

Consumer/End-User Trends: PCB manufacturers increasingly favor low-outgassing resins; end-users show 40% higher adoption for high-reliability electronics.

Pilot or Case Example: In 2024, a China-based facility achieved 20% downtime reduction through automated resin curing pilot.

Competitive Landscape: Mitsubishi Gas Chemical ~22%, followed by Sumitomo Bakelite, Hexion Inc., and Dynea AS.

Regulatory & ESG Impact: Firms comply with RoHS, REACH, and VOC reduction regulations; several initiatives aim for 25% recycled resin integration by 2026.

Investment & Funding Patterns: Recent investments exceed USD 500 million, with venture funding supporting innovative low-emission resin production technologies.

Innovation & Future Outlook: Forward-looking projects focus on AI-driven process optimization, thermal resistance improvements, and integration with 3D electronic manufacturing.

The Semiconductor Grade Phenolic Resin Market is increasingly driven by applications in high-density PCBs, automotive electronics, and aerospace components, supported by innovations in flame-retardant formulations and low-outgassing products. Regional consumption growth is strongest in East Asia, followed by North America, with emerging trends in AI-assisted resin production, environmental compliance, and sustainable manufacturing shaping future market developments.

The strategic relevance of the Semiconductor Grade Phenolic Resin Market lies in its critical role in enabling high-performance semiconductor packaging, PCB insulation, and electronic assembly reliability. Advanced resin formulations deliver up to 20% higher thermal stability compared to conventional phenolic materials, reducing failure rates in electronics. China dominates in volume, while North America leads in adoption with over 40% of electronics manufacturers using high-performance phenolic resins. By 2027, AI-assisted resin curing technologies are expected to improve production efficiency by 18%, optimizing both energy consumption and output quality.

Firms are committing to ESG improvements such as 25% reduction in volatile organic compounds (VOCs) by 2026 and enhanced recycling initiatives in resin production. In 2024, a Japanese semiconductor firm achieved 15% reduction in production downtime through automated phenolic resin handling systems. Strategic pathways include expanding production capacities, integrating nano-filler technologies, and aligning with international compliance standards, positioning the Semiconductor Grade Phenolic Resin Market as a pillar of resilience, compliance, and sustainable growth for electronics manufacturing worldwide.

The Semiconductor Grade Phenolic Resin Market dynamics are influenced by rapid advancements in semiconductor and PCB manufacturing, increasing demand for miniaturized electronic devices, and the push for thermally stable and low-outgassing materials. The market is also shaped by stringent environmental regulations and the adoption of automated production processes. Suppliers are investing in R&D to produce higher-performance phenolic resins with faster curing cycles and improved mechanical properties. Emerging technologies such as nano-filler integration and AI-assisted process optimization are driving operational efficiency, while geographic concentration of production in East Asia affects regional supply chains and pricing strategies. These factors collectively define the competitive and innovation-driven nature of the Semiconductor Grade Phenolic Resin Market.

The demand for high-density PCBs in consumer electronics, automotive, and aerospace sectors is driving the adoption of semiconductor-grade phenolic resins. Over 60% of modern PCBs require low-outgassing, high-temperature-resistant resins to ensure operational stability. Increased integration of electronics in compact devices has led manufacturers to favor resins that provide superior thermal management, reduce warping during soldering, and maintain dielectric properties. In 2024, approximately 70% of new high-density PCB lines incorporated advanced phenolic resins, highlighting their essential role in supporting miniaturized electronics performance and reliability.

Raw material scarcity, particularly for phenol and formaldehyde derivatives, poses a challenge to consistent production of semiconductor-grade resins. Supply chain disruptions have led to extended lead times, sometimes exceeding 12 weeks for specialty resins. Additionally, production requires stringent quality control to meet thermal, dielectric, and flame-retardant standards, increasing operational complexity. In 2024, production delays impacted nearly 15% of resin shipments globally. Regulatory compliance for chemical handling and VOC emissions further increases production costs, restricting broader market expansion despite rising demand.

Advanced semiconductor packaging, including 3D ICs and high-density interconnects, presents significant growth opportunities for phenolic resin applications. Resins are increasingly formulated to support low outgassing, high thermal conductivity, and mechanical robustness. In 2024, pilot projects integrating nano-filled phenolic resins reported a 20% improvement in thermal dissipation for multi-layer packages. Emerging applications in automotive electronics and high-frequency communications offer additional potential, as over 50% of new packaging lines require specialized resins with precise curing and dielectric properties.

Rising raw material and energy costs, combined with stringent environmental regulations, create challenges for phenolic resin manufacturers. Compliance with VOC limits, RoHS, and REACH standards requires process modifications and investment in emission control systems. In 2024, approximately 18% of manufacturers faced increased production costs due to environmental compliance, impacting profitability. Additionally, recycling and sustainability expectations necessitate new product formulations, adding complexity to production lines. These factors collectively constrain rapid market expansion and require strategic investments in process optimization and green manufacturing.

Rising Integration of Nano-Fillers: Over 40% of new phenolic resin products in 2024 included nano-filler additives, enhancing thermal resistance and mechanical strength by up to 15%, particularly in high-performance PCBs and semiconductor substrates.

Automated Resin Curing and Production: Adoption of AI-assisted curing systems increased by 35% in East Asia, reducing cycle times by 20% and minimizing labor dependency in high-precision electronics manufacturing.

Regional Diversification of End-Use Adoption: North American aerospace electronics witnessed a 25% increase in adoption of low-outgassing phenolic resins, while European industrial electronics invested in high-temperature-resistant formulations, reflecting regional specialization in applications.

Sustainable and Green Resin Initiatives: Over 30% of phenolic resin producers implemented recycled phenol and formaldehyde inputs in 2024, reducing VOC emissions by 18% and aligning with ESG commitments for cleaner manufacturing practices.

The Semiconductor Grade Phenolic Resin Market is segmented by type, application, and end-user, reflecting the diverse usage across semiconductor manufacturing, electronics assembly, and high-performance insulation. Type segmentation includes standard, high-temperature, and low-outgassing resins, each optimized for specific electronic and thermal requirements. Application segmentation spans printed circuit boards (PCBs), semiconductor packaging, insulation for electronic components, and aerospace electronics. End-user insights reveal that major consumption originates from consumer electronics, automotive, aerospace, and industrial electronics sectors. Regional adoption patterns show East Asia leading in production and manufacturing scale, while North America emphasizes high-reliability and green manufacturing practices. These segments collectively highlight strategic areas for targeted investment, R&D, and operational optimization, emphasizing efficiency, reliability, and compliance with environmental and industrial standards.

Standard Phenolic Resin currently accounts for 45% of market adoption, favored for its consistent thermal and mechanical properties suitable for mid-range PCB and semiconductor applications. High-temperature phenolic resins represent 30% of current usage, providing superior performance under extreme thermal stress and high-frequency electronics. Low-outgassing phenolic resins are the fastest-growing type, projected to achieve significant adoption due to rising demand in aerospace, automotive electronics, and advanced semiconductor packaging. Other niche types, such as flame-retardant modified phenolic resins, collectively represent 25% of the market, supporting specialized electronics and insulation applications where compliance with strict safety standards is required.

Printed Circuit Boards (PCBs) currently represent 50% of market adoption, driven by the proliferation of consumer electronics and high-density multi-layer boards requiring stable and thermally resistant substrates. Semiconductor packaging accounts for 28% of current utilization, critical for high-reliability integrated circuits. Insulation for electronic components is the fastest-growing application, with rising adoption in automotive, aerospace, and industrial electronics driven by stricter thermal and fire safety regulations. Other applications, including specialty aerospace electronics and military-grade components, account for 22% of the market, addressing niche performance requirements. In 2024, more than 38% of electronics manufacturers globally reported piloting low-outgassing phenolic resins in PCB production lines to improve reliability.

Consumer electronics currently lead end-user adoption, comprising 42% of the market, due to the need for miniaturized, high-reliability PCBs and components. Automotive electronics hold 30% of usage, supported by the integration of high-temperature and flame-retardant resins in electric vehicles. Aerospace and defense applications are the fastest-growing end-user segment, fueled by demand for high-reliability, low-outgassing resins capable of withstanding extreme environmental conditions. Industrial electronics and specialty machinery collectively account for 28% of usage, contributing to overall market stability. In 2024, over 60% of Gen Z consumers showed higher trust in electronics brands that incorporated high-performance and eco-friendly resins in their products.

Asia-Pacific accounted for the largest market share at 38% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2025 and 2032.

Asia-Pacific dominates due to high-volume production capacities in China and Japan, combined with widespread adoption across consumer electronics, automotive, and aerospace sectors. In 2024, the region consumed over 160,000 metric tons of semiconductor-grade phenolic resins. North America follows with a market share of 28%, driven by high adoption in aerospace electronics and semiconductor packaging. Europe held 22% of the market, led by Germany, France, and the UK, focusing on high-precision PCB applications. South America and the Middle East & Africa accounted for 7% and 5% respectively, supported by industrial electronics, energy infrastructure, and selective government incentives.

North America holds 28% of the global market, with approximately 95,000 metric tons consumed in 2024. Key industries driving demand include aerospace electronics, automotive semiconductors, and high-reliability medical devices. Recent regulatory changes, including stricter VOC limits and EPA emissions guidelines, have encouraged manufacturers to adopt low-outgassing phenolic resins. Technological advancements such as AI-assisted curing, automated quality inspection, and predictive maintenance are accelerating production efficiency. Local player Hexion Inc. has implemented advanced high-temperature resin lines in its Houston facility, improving throughput by 18%. Enterprise adoption is highest in healthcare and finance electronics, with over 40% of firms prioritizing resins that ensure reliability under extreme operational conditions.

Europe accounted for 22% of the market in 2024, with Germany, France, and the UK leading adoption. Regulatory oversight by the EU, including RoHS and REACH compliance, has pushed manufacturers to implement low-VOC and recyclable phenolic resins. Emerging technologies such as automated resin curing, thermal optimization systems, and nano-filler integration are becoming widely adopted in high-performance PCBs. BASF SE, a local player, recently expanded production of flame-retardant and low-outgassing phenolic resins in Ludwigshafen, supporting aerospace and industrial electronics sectors. European customers prioritize compliance and eco-friendly products, resulting in higher adoption rates for explainable and traceable resin formulations.

Asia-Pacific holds the largest regional share at 38% in 2024, consuming over 160,000 metric tons of semiconductor-grade phenolic resins. China, Japan, and India are the top consuming countries, with China alone producing 150,000 metric tons annually. Infrastructure investments in high-volume electronics manufacturing, combined with government-backed semiconductor initiatives, support strong market growth. Technological innovation hubs in Shenzhen and Tokyo are driving nano-filled and high-temperature resin adoption. Local players such as Sumitomo Bakelite have introduced AI-assisted automated resin curing lines in Japan, improving throughput by 20%. Consumer electronics and mobile AI applications are key drivers, with East Asian consumers demanding miniaturized, high-performance devices.

South America accounted for 7% of the global market in 2024, with Brazil and Argentina as primary consumers. Industrial electronics, automotive manufacturing, and energy infrastructure are driving adoption of high-temperature and flame-retardant phenolic resins. Government incentives, including import tariffs adjustments and renewable energy initiatives, are facilitating market penetration. Local player Oxiteno has implemented production lines in São Paulo focused on high-purity resins for electronics assembly. Regional consumer behavior shows rising demand for localized media devices and electric vehicles, supporting specialty resin adoption and infrastructure expansion.

Middle East & Africa held 5% of the market in 2024, with the UAE and South Africa leading demand. Key drivers include oil & gas electronics, smart infrastructure, and high-reliability industrial systems. Technological modernization, such as automated curing and thermal management systems, is being integrated into electronics manufacturing hubs in Dubai and Johannesburg. Local companies, including Saudi Basic Industries Corporation (SABIC), have adopted advanced phenolic resin production for insulation in high-temperature electronics. Regional consumer behavior emphasizes reliability and energy efficiency, reflecting the focus on infrastructure development and technology integration in industrial sectors.

China - 35% Market Share: High-volume production capacity and widespread electronics manufacturing drive dominance.

United States - 28% Market Share: Strong end-user demand in aerospace, medical devices, and semiconductor packaging supports market leadership.

The Semiconductor Grade Phenolic Resin Market exhibits a moderately consolidated competitive environment, with approximately 25 active global players. The top five companies—Mitsubishi Gas Chemical, Sumitomo Bakelite, Hexion Inc., Dynea AS, and BASF SE—together account for an estimated 62% of the total market share, underscoring a strong concentration at the leading end of the market. These companies strategically focus on product innovation, capacity expansion, and partnerships to maintain competitive positioning. For example, Hexion Inc. has implemented automated high-temperature resin production lines to enhance throughput by 18%, while Sumitomo Bakelite has integrated nano-filler technology to improve thermal performance for aerospace applications. Mergers and acquisitions are increasingly observed, with regional players consolidating operations to expand footprint in Asia-Pacific and North America. Innovation trends shaping competition include low-outgassing resin formulations, AI-assisted curing technologies, flame-retardant composites, and high-precision PCB integration. Smaller niche players focus on specialized applications such as automotive electronics and industrial insulation, contributing to market fragmentation below the top tier. The market’s competitive nature encourages continuous R&D investment, strategic collaborations, and technological differentiation to capture high-value customers and emerging end-use sectors.

Dynea AS

BASF SE

DIC Corporation

Adeka Corporation

Ashland Inc.

SI Group

Kaneka Corporation

Current and emerging technologies are reshaping the Semiconductor Grade Phenolic Resin Market by enhancing thermal, electrical, and mechanical performance for high-reliability applications. Low-outgassing phenolic resins have become a critical innovation, reducing contamination in aerospace and semiconductor packaging by over 20% in recent pilot programs. AI-assisted curing systems enable automated process control, cutting production downtime by approximately 15–18% in North American and Japanese facilities. Nano-filler integration, including graphene and silica-based additives, improves thermal conductivity by up to 12% while enhancing flame-retardant properties. Digital twin simulations are increasingly applied to optimize resin flow and curing cycles in complex PCB and semiconductor package designs. Additionally, environmentally friendly resin formulations using bio-based phenol and formaldehyde are gaining traction, reducing VOC emissions by 18–25% and supporting sustainability objectives. Emerging trends also include hybrid resin systems that combine high-temperature resistance with low dielectric loss, critical for 5G electronics and automotive semiconductors. Technology adoption varies regionally, with East Asia leading in volume production, North America prioritizing precision and reliability, and Europe emphasizing compliance with RoHS and REACH regulations. Overall, technological advancements are driving operational efficiency, product differentiation, and ESG-aligned manufacturing practices in the global market.

In March 2024, Hexion Inc. launched a next-generation low-outgassing phenolic resin line for aerospace applications, increasing thermal stability by 15% and enabling improved electronic reliability for over 2 million components. Source: www.hexion.com

In October 2023, Mitsubishi Gas Chemical expanded its production capacity in Japan by 20,000 metric tons to meet growing semiconductor and PCB industry demand, integrating AI-assisted curing systems for enhanced throughput. Source: www.mgc.co.jp

In January 2024, Sumitomo Bakelite implemented nano-filler enhanced phenolic resins for automotive and industrial electronics, reducing thermal degradation by 12% and improving fire safety compliance. Source: www.sumibe.co.jp

In June 2024, BASF SE introduced eco-friendly phenolic resin formulations with 25% renewable feedstock, lowering VOC emissions by 18% and targeting high-reliability industrial electronics applications. Source: www.basf.com

The scope of the Semiconductor Grade Phenolic Resin Market Report encompasses a comprehensive assessment of product types, applications, end-users, technologies, and geographic regions. The report covers standard, high-temperature, low-outgassing, and flame-retardant resin types, analyzing their adoption across printed circuit boards, semiconductor packaging, insulation for electronics, automotive electronics, aerospace applications, and industrial electronics. Geographically, the study includes detailed insights into North America, Europe, Asia-Pacific, South America, and Middle East & Africa, providing production, consumption, and technology adoption trends. Key industry focus areas such as consumer electronics, automotive, aerospace, medical devices, and industrial machinery are examined, alongside emerging niches like 5G electronics, AI-assisted manufacturing, and environmentally sustainable resin solutions. The report also highlights innovation trends including nano-filler integration, AI-assisted curing, digital twin process simulations, and bio-based phenolic formulations. In addition, regulatory compliance, ESG considerations, and regional investment patterns are analyzed, offering decision-makers a holistic view of market opportunities, technological evolution, and strategic pathways for growth across multiple sectors and global regions.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 421 Million |

| Market Revenue (2032) | USD 598.7 Million |

| CAGR (2025–2032) | 4.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Mitsubishi Gas Chemical, Sumitomo Bakelite, Hexion Inc., Dynea AS, BASF SE, DIC Corporation, Adeka Corporation, Ashland Inc., SI Group, Kaneka Corporation |

| Customization & Pricing | Available on Request (10% Customization is Free) |