Reports

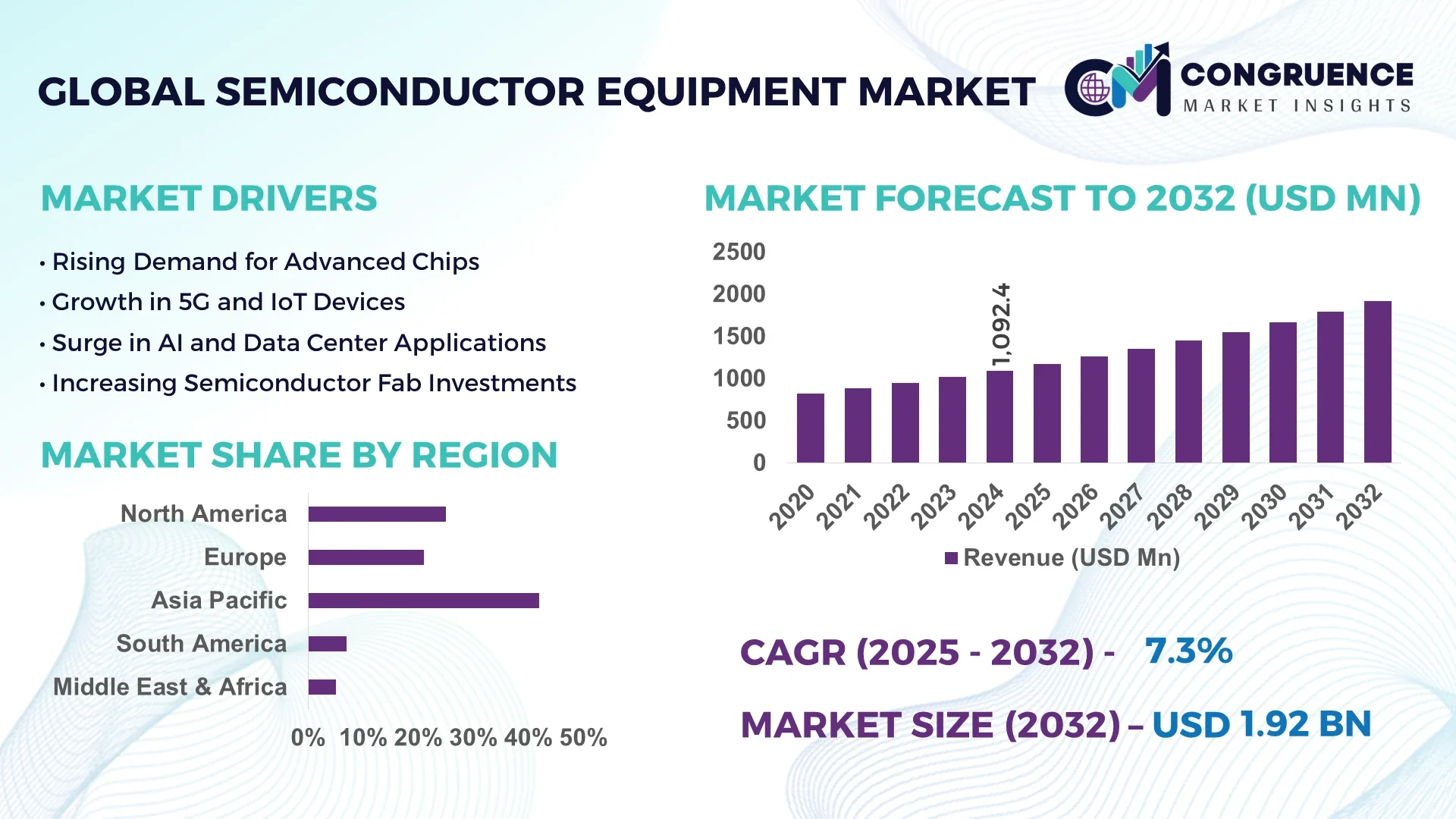

The Global Semiconductor Equipment Market was valued at USD 1,092.4 Million in 2024 and is anticipated to reach a value of USD 1,919.5 Million by 2032 expanding at a CAGR of 7.3% between 2025 and 2032.

To Learn More About This Report, Request A Free Sample Copy

Dominating the semiconductor equipment market, the United States leads with extensive investments in advanced fabrication facilities and cutting-edge research centers. This dominance is supported by a robust ecosystem of semiconductor foundries, equipment manufacturers, and R&D initiatives, which collectively drive innovation and high production efficiency. The US semiconductor equipment market plays a pivotal role in enabling domestic chip production, critical for technology sectors such as AI, automotive, and consumer electronics.

The semiconductor equipment market encompasses a wide range of tools and machinery used in wafer fabrication, assembly, testing, and packaging processes. This market is continuously evolving, driven by the increasing complexity of semiconductor devices and the push towards smaller nodes and higher yields. The demand for advanced lithography systems, etching machines, deposition tools, and inspection equipment remains high as manufacturers strive to meet the needs of emerging technologies like 5G, IoT, and artificial intelligence. Continuous innovation in equipment capabilities is crucial to support the transition to newer materials and semiconductor architectures, making the equipment market a vital part of the overall semiconductor industry supply chain.

Artificial intelligence (AI) is revolutionizing the semiconductor equipment market by enhancing manufacturing precision, reducing defects, and accelerating production cycles. AI-driven analytics enable real-time monitoring of equipment performance and process parameters, allowing early detection of anomalies and predictive maintenance, which minimizes downtime. Machine learning algorithms optimize lithography and etching processes by adjusting settings dynamically based on wafer conditions, leading to improved yields and higher throughput.

Furthermore, AI-powered automation is streamlining complex wafer inspection and metrology tasks, replacing manual and slower traditional methods. This leads to faster identification of defects and contamination, ensuring higher product quality. The integration of AI also facilitates adaptive process control, where equipment learns and adapts to variations in materials and environmental conditions, maintaining consistency across production batches. This transformation is enabling semiconductor manufacturers to meet the rising demand for smaller, more complex chips with higher performance and lower power consumption, while simultaneously managing costs and time-to-market pressures.

AI applications extend to supply chain optimization within semiconductor equipment manufacturing, where predictive demand forecasting and inventory management reduce lead times and improve resource utilization. By leveraging vast datasets generated throughout the production lifecycle, AI tools provide actionable insights that guide equipment design improvements and process innovations. The collaboration between AI software developers and semiconductor equipment makers is fostering a new era of smart factories, where interconnected equipment communicates seamlessly to optimize overall factory efficiency and agility.

“In early 2025, a breakthrough was announced where AI algorithms were integrated into extreme ultraviolet (EUV) lithography machines, enabling dynamic real-time correction of focus and overlay errors. This integration reportedly improved wafer throughput by over 15% and reduced defect rates significantly, marking a substantial leap in lithography precision.”

The semiconductor equipment market is driven by the relentless demand for cutting-edge manufacturing technologies that enable the production of smaller, faster, and more efficient chips. The growing adoption of AI, 5G networks, and IoT devices requires highly sophisticated equipment capable of supporting advanced semiconductor nodes below 5 nanometers. This demand encourages manufacturers to invest heavily in state-of-the-art lithography, deposition, and etching tools to maintain competitive advantage and meet stringent performance requirements. Additionally, increasing production capacity expansions by leading foundries fuel equipment demand worldwide.

The semiconductor equipment market faces restraints due to the escalating costs associated with acquiring and maintaining advanced manufacturing tools. The complexity of integrating new equipment into existing fabrication lines requires significant technical expertise and capital investment, which can be a barrier for smaller manufacturers. Prolonged equipment qualification cycles and the necessity for constant upgrades to keep pace with technological advancements increase operational expenses. These factors can slow down adoption rates and impact overall market growth, especially in regions with limited financial resources.

Emerging semiconductor manufacturing hubs in Asia and other regions present substantial opportunities for semiconductor equipment providers. Governments are promoting domestic chip production through subsidies and incentives, driving demand for localized equipment supply chains. This trend encourages equipment manufacturers to expand their footprint in these markets by establishing service centers and partnerships. Furthermore, the rise of niche semiconductor applications, such as automotive sensors and power electronics, opens new avenues for customized equipment solutions tailored to specific industry needs, enhancing market diversification.

Market growth is challenged by supply chain vulnerabilities and geopolitical uncertainties affecting semiconductor equipment production and distribution. Disruptions in the supply of critical components, such as specialized materials and precision parts, can delay equipment manufacturing and delivery schedules. Trade restrictions and export controls impose additional hurdles for cross-border equipment sales, complicating business operations for global suppliers. These challenges necessitate strategic risk management and diversification of supply sources to ensure continuity and competitiveness in the market.

Rise in Modular and Prefabricated Equipment Components: The adoption of modular and prefabricated equipment components is enabling faster assembly, easier maintenance, and improved operational flexibility. Prefabricated subsystems designed with high precision reduce downtime significantly and are increasingly popular in high-volume manufacturing, especially across North America and Asia. This trend supports quicker adaptation to evolving semiconductor technologies and shorter production cycle times.

Increased Automation and Robotics Integration: Automation and robotics are becoming integral to semiconductor fabs, minimizing human errors and boosting production throughput. Advanced robotic wafer handlers, automated material transport systems, and robotic process automation are now common in leading fabs, enhancing workflow efficiency and reducing contamination risks. These innovations contribute to higher yield consistency and overall manufacturing reliability.

Deployment of AI and Machine Learning for Process Optimization: AI-driven process optimization is a key market trend, where equipment collects and analyzes massive sensor data for real-time defect detection and predictive maintenance. Machine learning algorithms facilitate proactive process adjustments during fabrication, improving product quality and reducing scrap rates. This trend is essential for managing the complexities of advanced semiconductor nodes and enhancing factory agility.

Focus on Sustainability and Energy Efficiency: Manufacturers are prioritizing eco-friendly equipment designs that reduce energy consumption and minimize waste generation. Sustainable manufacturing practices are being integrated into equipment development to comply with environmental regulations and meet corporate sustainability goals. This includes the use of energy-efficient components and recycling technologies, fostering greener semiconductor production.

The semiconductor equipment market is segmented based on type, application, and end-user to provide detailed insights into the industry's structure and growth drivers. By analyzing these segments, stakeholders can better understand market dynamics and tailor strategies accordingly. Types include wafer fabrication equipment, assembly and packaging equipment, and inspection and testing equipment. Applications cover memory devices, logic devices, and discrete devices. End-users range from semiconductor foundries and integrated device manufacturers (IDMs) to outsourced semiconductor assembly and test (OSAT) providers. Each segment reflects unique demands influenced by technological advancements, production volumes, and emerging industry trends, driving targeted equipment investments.

The semiconductor equipment market by type includes wafer fabrication equipment, assembly and packaging equipment, and inspection and testing equipment. Wafer fabrication equipment leads the market, accounting for the largest revenue share due to the critical role it plays in chip manufacturing and the growing complexity of semiconductor nodes. This segment includes lithography, etching, deposition, and cleaning equipment that supports the scaling of integrated circuits to smaller nodes. Assembly and packaging equipment is the fastest growing segment, driven by increased demand for advanced packaging solutions such as system-in-package (SiP) and 3D packaging that improve chip performance and functionality. Inspection and testing equipment also holds a significant portion, with growth fueled by the need for defect detection and quality assurance as chips become more complex. Investments in inspection tools are rising to maintain high yield rates and reduce manufacturing defects.

In terms of application, the semiconductor equipment market is segmented into memory devices, logic devices, and discrete devices. Memory devices dominate the application segment due to the exponential demand for data storage driven by cloud computing, mobile devices, and data centers. This segment requires specialized equipment to manufacture DRAM, NAND, and emerging non-volatile memory technologies. Logic devices are the fastest growing segment, fueled by the expansion of AI, IoT, and automotive electronics markets that demand high-performance processors and ASICs. Discrete devices, including power semiconductors and sensors, are also experiencing steady growth as electric vehicles and industrial automation increase demand for energy-efficient components. Each application type requires specific fabrication and assembly equipment, reflecting their technological complexity and production volumes.

The semiconductor equipment market end-users comprise semiconductor foundries, integrated device manufacturers (IDMs), and outsourced semiconductor assembly and test (OSAT) providers. Foundries hold the largest market share by end-user, driven by the booming demand for contract chip manufacturing services from fabless semiconductor companies and technology OEMs. Foundries continuously upgrade their equipment to support advanced process technologies and high-volume manufacturing. IDMs are the fastest growing segment as they invest in expanding in-house production capabilities to gain greater control over the supply chain and technology development. OSAT providers maintain a significant presence due to increasing outsourcing of assembly and testing processes, especially for complex packaging requirements. The rising trend toward fabless semiconductor design and specialization supports growth across all end-user segments, influencing equipment demand patterns.

Asia-Pacific accounted for the largest market share at 42% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 7.8% between 2025 and 2032.

To Learn More About This Report, Request A Free Sample Copy

The dominance of Asia-Pacific is driven by significant semiconductor manufacturing hubs in countries like China, South Korea, and Taiwan, where massive investments in fabrication facilities and government support propel market expansion. North America’s rapid growth is fueled by aggressive investments in R&D, advanced equipment manufacturing, and policies encouraging domestic chip production. Europe and other regions continue to contribute steadily, supported by niche manufacturing and innovation centers.

Innovation and Domestic Production Drive Growth

North America’s semiconductor equipment market benefits from extensive investments in cutting-edge technologies such as EUV lithography and AI-enabled manufacturing. The U.S. leads with equipment manufacturing giants expanding their portfolios to support next-generation chips for AI, aerospace, and automotive sectors. The region’s focus on securing supply chains and promoting semiconductor sovereignty has led to new fabrication plants and equipment upgrades. Canada also contributes by specializing in advanced materials and equipment components. Together, these trends position North America as a hub for innovation and equipment development in the global semiconductor landscape.

Steady Growth Fueled by Advanced Research and Green Initiatives

Europe’s semiconductor equipment market shows steady growth driven by strong research institutions and government initiatives supporting sustainable manufacturing. Countries like Germany and France are prominent players, focusing on precision equipment for automotive electronics and industrial semiconductors. The region is increasingly adopting energy-efficient tools and automation to reduce environmental impact. Collaborative projects across the EU are enhancing equipment capabilities, particularly in sensor manufacturing and power electronics. Europe’s emphasis on green technologies and niche high-performance applications supports consistent demand for advanced semiconductor equipment.

Manufacturing Powerhouse with Expanding Capacity

Asia-Pacific remains the largest market, led by China, South Korea, and Taiwan, which house the world’s biggest semiconductor fabrication facilities. Massive investments in wafer fabrication, assembly, and packaging equipment continue to expand manufacturing capacity. The region is rapidly adopting advanced equipment for sub-5nm technologies and advanced packaging techniques to meet global chip demand. Governments provide subsidies and incentives to attract semiconductor equipment makers and foster local supply chains. Emerging markets like India are also gaining traction, focusing on equipment for electronics manufacturing services and chip assembly.

Emerging Market with Growing Semiconductor Assembly Focus

South America’s semiconductor equipment market is smaller but growing, primarily driven by increasing semiconductor assembly and testing activities. Brazil leads the region with expanding electronics manufacturing sectors that require assembly and packaging equipment. The market benefits from growing demand for consumer electronics and automotive components, which are driving investments in quality testing and inspection tools. While wafer fabrication remains limited, South America is strengthening its position as an assembly and testing hub, opening opportunities for equipment suppliers specializing in these segments.

Nascent Market with Focus on Assembly and Testing

The Middle East & Africa semiconductor equipment market is nascent but shows promise due to emerging electronics manufacturing initiatives in countries like Israel and the UAE. The region focuses mainly on semiconductor assembly, packaging, and testing equipment to support growing local demand for consumer electronics and telecommunications infrastructure. Strategic investments in technology parks and innovation hubs aim to build capabilities in equipment manufacturing and R&D. While wafer fabrication remains limited, the region is expected to increase its footprint in assembly and inspection segments as infrastructure improves.

China: Holding the highest market share valued at approximately USD 460 million in 2024, driven by massive investments in wafer fabrication and government incentives aimed at achieving semiconductor self-reliance.

United States: The second-largest market with a value near USD 310 million in 2024, supported by a strong equipment manufacturing base, innovation in advanced lithography, and policies promoting domestic semiconductor production.

The semiconductor equipment market is highly competitive with several global leaders dominating key segments such as wafer fabrication, assembly, and inspection equipment. Companies continuously invest in research and development to innovate and enhance product offerings, focusing on precision, efficiency, and sustainability. The market is characterized by frequent technological advancements and strategic collaborations aimed at meeting the demands of smaller semiconductor nodes and advanced packaging technologies. Leading players hold substantial market shares due to their extensive product portfolios, strong customer relationships, and global manufacturing footprints. The competition also includes emerging players focusing on niche equipment segments or regional markets, driving overall industry innovation. Market leaders are increasingly adopting AI, machine learning, and automation technologies to improve equipment performance and reduce production costs, strengthening their competitive advantage.

Applied Materials, Inc.

ASML Holding N.V.

Tokyo Electron Limited

Lam Research Corporation

KLA Corporation

SCREEN Semiconductor Solutions Co., Ltd.

Teradyne, Inc.

Advantest Corporation

Hitachi High-Technologies Corporation

Nikon Corporation

Advanced lithography technologies, including extreme ultraviolet (EUV) lithography, are central to the semiconductor equipment market, enabling the production of chips with smaller feature sizes and higher transistor density. Equipment integrating AI and machine learning algorithms is increasingly used for process control, defect inspection, and predictive maintenance, which improves manufacturing yield and reduces downtime. Furthermore, innovations in 3D packaging and system-in-package (SiP) technologies are driving demand for specialized assembly and testing equipment. Developments in metrology and inspection tools focus on detecting sub-nanometer defects, essential for maintaining quality at advanced process nodes. Additionally, the push toward sustainability is influencing technology trends, with equipment manufacturers designing energy-efficient machines and adopting environmentally friendly materials and processes. The integration of robotics and automation is streamlining semiconductor fabrication, improving precision, and minimizing contamination risks.

In March 2024, ASML announced the shipment of its latest generation EUV lithography system, capable of producing chips at the 3nm node, marking a significant milestone in advanced semiconductor manufacturing capabilities.

In October 2023, Applied Materials launched an AI-powered metrology platform designed to enhance defect detection speed and accuracy during wafer inspection processes, facilitating improved manufacturing yields.

In July 2024, Lam Research unveiled a new atomic layer deposition (ALD) system that supports complex 3D transistor architectures, addressing the growing demand for advanced logic devices.

In December 2023, KLA Corporation introduced a real-time process control solution using machine learning to optimize plasma etching, reducing defect rates and increasing throughput in semiconductor fabs.

The semiconductor equipment market report covers a comprehensive range of equipment types, including wafer fabrication, assembly and packaging, and inspection and testing tools, providing insights into their technological advancements and market performance. It analyzes applications across memory, logic, and discrete devices, highlighting how equipment demand varies with semiconductor technology evolution and industry needs. The report also explores end-user segments such as foundries, integrated device manufacturers (IDMs), and outsourced assembly and test providers, detailing their role in shaping equipment investment trends. Geographic insights span major regions, outlining market size, growth drivers, and emerging opportunities. Additionally, the report addresses key technological trends, competitive dynamics, and recent developments to offer a holistic view of the semiconductor equipment industry’s current status and future outlook.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Name | Global Semiconductor Equipment Market |

| Market Revenue (2024) | USD 1,092.4 Million |

| Market Revenue (2032) | USD 1,919.5 Million |

| CAGR (2025–2032) | 7.3% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape, Technological Insights, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Applied Materials, Inc., ASML Holding N.V., Tokyo Electron Limited, Lam Research Corporation, KLA Corporation, SCREEN Semiconductor Solutions Co., Ltd., Teradyne, Inc., Advantest Corporation, Hitachi High-Technologies Corporation, Nikon Corporation |

| Customization & Pricing | Available on Request (10% Customization is Free) |