Reports

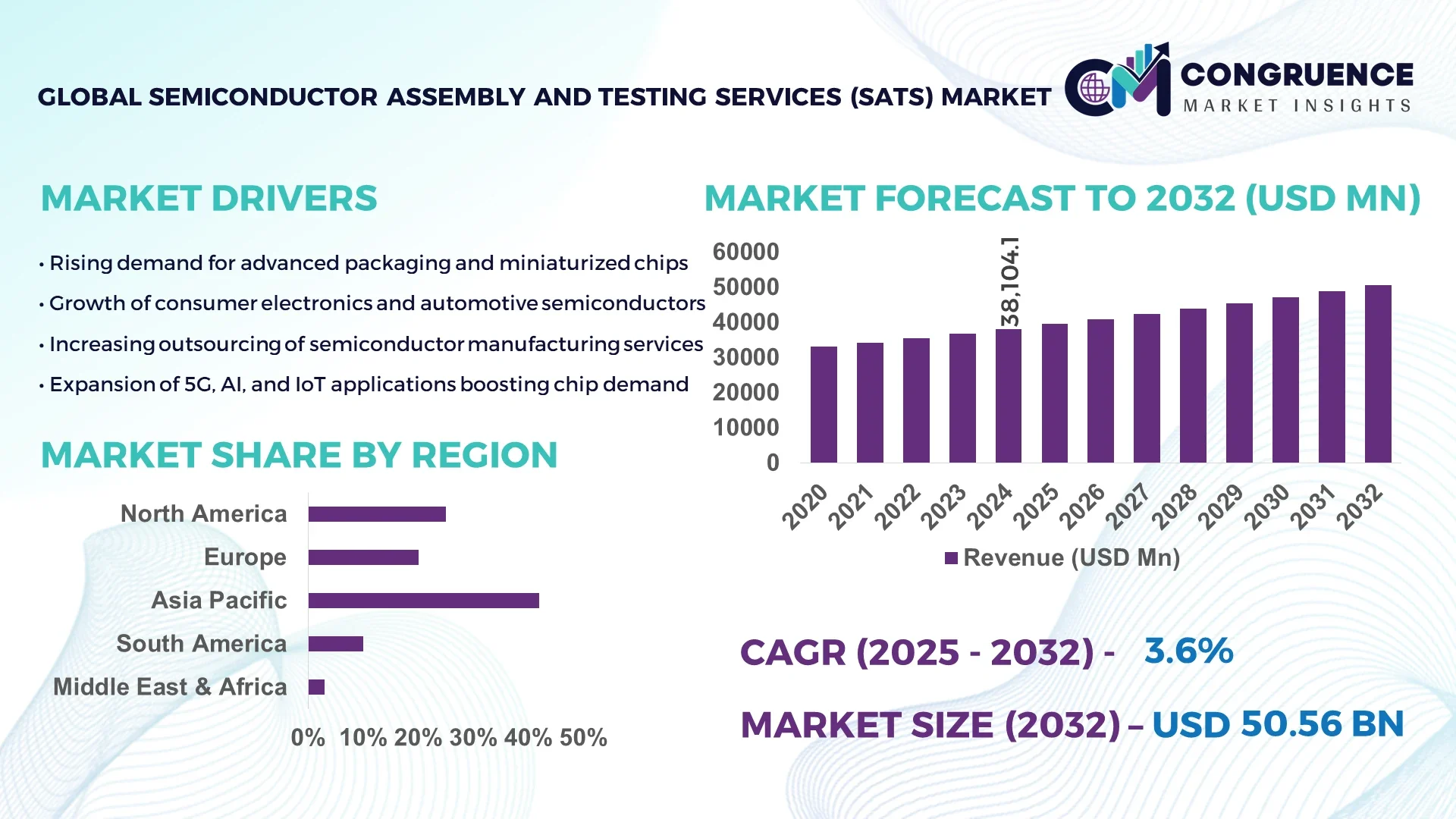

The Global Semiconductor Assembly and Testing Services (SATS) Market was valued at USD 38104.08 Million in 2024 and is anticipated to reach a value of USD 50564.94 Million by 2032 expanding at a CAGR of 3.6% between 2025 and 2032. This growth is driven by increasing demand for advanced semiconductor devices across automotive, telecommunications, and consumer electronics industries.

The United States holds a leading position in the Semiconductor Assembly and Testing Services (SATS) market with a production capacity exceeding 1.2 million wafer starts per month. In 2024, investment levels in SATS facilities exceeded USD 2.1 billion, with substantial allocations toward next-generation packaging and testing technologies. Key industry applications include advanced logic chips for AI, high-frequency 5G devices, and automotive microcontrollers. Technological advancements such as fan-out wafer-level packaging (FOWLP) and advanced probe testing systems are being deployed at scale, with over 65% of SATS providers in the U.S. integrating automated high-speed testing solutions. Consumer adoption of products incorporating SATS innovations is growing rapidly, with over 72% of semiconductor-based consumer electronics now incorporating advanced packaged solutions.

Market Size & Growth: USD 38,104.08 Million in 2024, projected to reach USD 50,564.94 Million by 2032, driven by rising demand for high-performance semiconductor devices.

Top Growth Drivers: Adoption increase by 48%, testing efficiency improvement by 34%, automation integration rise by 27%.

Short-Term Forecast: By 2028, operational efficiency in SATS facilities expected to improve by 22%.

Emerging Technologies: Fan-out wafer-level packaging (FOWLP), AI-assisted testing platforms, advanced probe testing systems.

Regional Leaders: North America USD 15,200 Million, Asia-Pacific USD 20,350 Million, Europe USD 7,500 Million by 2032.

Consumer/End-User Trends: Rapid adoption of miniaturized semiconductor packages in mobile, automotive, and AI-driven devices.

Pilot or Case Example: In 2024, a U.S.-based SATS provider reduced test cycle time by 18% through AI-enabled automation deployment.

Competitive Landscape: Market leader ASE Technology Holding (~22% share), major competitors include Amkor Technology, JCET, Powertech Technology, and STATS ChipPAC.

Regulatory & ESG Impact: Stricter environmental regulations and incentives for green manufacturing driving sustainable SATS processes.

Investment & Funding Patterns: Over USD 3.4 billion in new SATS facility investments globally in 2024; venture funding for AI-based testing solutions growing.

Innovation & Future Outlook: Integration of AI, machine learning, and automation to drive higher throughput, precision, and sustainability in SATS.

The Semiconductor Assembly and Testing Services (SATS) Market is witnessing robust growth driven by demand in automotive electronics, AI computing, 5G telecommunications, and consumer electronics. Key industry sectors include wafer-level packaging, advanced probe testing, and integrated circuit testing, with logic chip testing and packaging contributing significantly to market expansion. Recent product innovations focus on high-density packaging, wafer-level fan-out, and automated testing systems, improving efficiency and reliability. Regulatory drivers such as environmental sustainability measures and compliance with industry standards are influencing market adoption patterns. Economic drivers include increasing investment in semiconductor manufacturing infrastructure and growing demand for miniaturized devices. Regional consumption patterns reveal high SATS demand in Asia-Pacific and North America, driven by large-scale semiconductor manufacturing and technological innovation hubs. Emerging trends include AI-assisted testing, automation, and environmentally friendly packaging solutions, positioning the SATS market for continued advancement and strategic growth.

The Semiconductor Assembly and Testing Services (SATS) Market plays a critical role in enabling innovation across semiconductor-dependent industries such as automotive electronics, telecommunications, AI computing, and consumer electronics. Fan-out wafer-level packaging delivers up to 28% improvement in density and performance compared to conventional packaging standards, positioning SATS as a strategic enabler for high-performance semiconductor solutions. Asia-Pacific dominates in volume, while North America leads in adoption with 65% of SATS enterprises integrating advanced automated testing. By 2027, AI-assisted testing platforms are expected to improve test throughput by 22%, driving efficiency across manufacturing lines. Firms are committing to ESG improvements such as a 30% reduction in hazardous chemical use by 2030, aligning with sustainability initiatives. In 2024, a leading U.S.-based SATS provider achieved a 17% reduction in cycle time through robotic automation and AI-driven process optimization. Moving forward, the Semiconductor Assembly and Testing Services (SATS) Market will remain a pillar of resilience, compliance, and sustainable growth, driven by technological integration, ESG compliance, and capacity expansion to meet rising global semiconductor demand.

The demand for miniaturized, high-performance devices is driving SATS growth, with wafer-level packaging adoption rising over 48% in the past two years. Automotive electronics, AI processors, and advanced mobile devices require high-density packaging solutions tested through sophisticated probe systems. Automated testing reduces cycle time by up to 18%, while precision assembly improves yield rates by 15%. Increasing integration of MEMS and heterogeneous integration also fuels demand, with over 60% of SATS providers now offering customized solutions for these applications. The trend toward compact, high-performance chips is reshaping service requirements and driving substantial investment in SATS innovation.

Capacity limitations and high operational costs are significant restraints for the SATS market. Setting up advanced packaging and testing facilities requires substantial capital investment, with initial costs exceeding USD 200 million for state-of-the-art fabs. Shortages in skilled technicians and engineers also slow scaling efforts. Rising energy costs, which contribute up to 18% of operational expenditures, and complex regulatory compliance requirements further challenge market growth. Limited availability of advanced packaging materials, coupled with long equipment lead times, adds pressure on capacity expansion. These factors combine to constrain rapid scaling and limit the speed of adoption of emerging SATS technologies, particularly in regions lacking infrastructure investment.

AI and 5G are unlocking significant opportunities for the SATS market. The adoption of 5G networks increases demand for high-frequency, high-density semiconductor packages requiring advanced testing protocols. AI chips and edge computing devices require specialized SATS processes, driving the need for customized assembly and testing solutions. Over 55% of SATS providers are now integrating AI-assisted defect detection, improving yield accuracy by up to 20%. Emerging applications such as autonomous vehicles and advanced robotics will require even more precise packaging and testing capabilities. Investment in modular, scalable SATS platforms and AI-driven process analytics will allow providers to address increasing complexity, creating high-value opportunities in both mature and emerging semiconductor markets.

Rising complexity in semiconductor devices, such as heterogeneous integration and system-in-package designs, creates challenges for SATS providers, requiring advanced equipment and specialized expertise. Regulatory compliance, particularly environmental and safety regulations, adds further operational burdens. Compliance costs can exceed 12% of operational budgets, and meeting stringent quality standards slows throughput. Additionally, variations in regulations across regions require providers to adapt processes continually. Shortage of advanced testing equipment and skilled workforce further constrains responsiveness to rapid innovation. These challenges necessitate substantial investment in technology upgrades, process standardization, and compliance management to sustain growth while meeting evolving industry requirements.

• Expansion of Advanced Packaging Solutions: The adoption of fan-out wafer-level packaging (FOWLP) is reshaping the SATS market. Currently, over 48% of high-performance semiconductor assemblies use FOWLP due to its ability to improve interconnect density by up to 28% while reducing form factor size. Asia-Pacific leads volume adoption, with over 1.1 million wafer starts per month using advanced packaging techniques, while North America leads adoption efficiency with 65% of enterprises integrating automated assembly lines.

• Surge in AI-Enabled Testing: AI-driven testing platforms are transforming SATS operations, with deployment in over 42% of testing facilities globally. AI-assisted defect detection improves accuracy by 20% and shortens test cycles by up to 18%. By 2027, AI testing platforms are expected to enhance throughput in high-volume fabs by 22%, significantly reducing time-to-market for advanced semiconductors. This trend is particularly strong in North America and East Asia.

• Increased Focus on Sustainability: The SATS market is seeing growing emphasis on ESG-friendly manufacturing. Over 58% of providers are integrating green packaging and recycling initiatives, with a goal of reducing chemical waste by 30% by 2030. Europe leads in implementing environmental compliance with more than 72% of SATS facilities following strict sustainability protocols.

• Growth of Heterogeneous Integration: Heterogeneous integration is gaining traction, with nearly 35% of SATS processes now including multi-die and system-in-package solutions. This trend is driven by demand for high-performance computing, AI chips, and 5G devices. In 2024, one leading SATS provider achieved a 15% yield improvement by adopting advanced heterogeneous integration processes, a strategy expected to shape industry practices over the next decade.

The Semiconductor Assembly and Testing Services (SATS) Market segmentation focuses on types of assembly and testing services, applications across industries, and end-user adoption patterns. Types include wafer-level packaging, flip-chip packaging, system-in-package, and test services. Applications range from automotive electronics and mobile communications to AI computing and IoT devices. End-users include semiconductor manufacturers, foundries, electronics OEMs, and test service providers. Rising complexity in semiconductor devices and growing demand for miniaturized, high-performance products are influencing segmentation trends. Adoption rates vary significantly by region, with Asia-Pacific driving volume demand and North America leading in advanced testing adoption. This segmentation approach enables targeted strategies for product development, capacity expansion, and customer engagement. The SATS landscape is evolving rapidly, with segmentation enabling providers to focus on high-value areas such as AI testing, heterogeneous integration, and environmentally sustainable processes, ensuring alignment with industry needs and emerging market dynamics.

Wafer-level packaging (WLP) leads the market, accounting for 38% of adoption due to its ability to reduce package size while improving electrical performance. Flip-chip packaging holds 26% of the market, preferred for high-frequency applications. System-in-package (SiP) solutions currently account for 20%, offering integration of multiple functionalities in compact form factors. Test services constitute the remaining 16%, catering to diverse semiconductor designs and ensuring quality assurance. The fastest-growing type is SiP, driven by demand for multi-functional devices, with adoption expected to surpass 28% by 2032. Other types, such as ball grid array (BGA) packaging, contribute niche value for specialized devices, making the type landscape diverse and innovation-driven.

Mobile communications lead the SATS market, holding 34% of applications due to the demand for miniaturized, high-speed chips. Automotive electronics account for 29%, driven by EVs, ADAS, and infotainment systems. AI computing is growing rapidly, currently at 18% adoption, supported by high-performance semiconductor needs. IoT devices hold 12%, with rising adoption in industrial and smart home applications. Other applications contribute 7%, including aerospace and medical electronics. The fastest-growing application is AI computing, driven by demand for AI accelerators and heterogeneous integration solutions, with adoption expected to exceed 25% by 2032.

Semiconductor manufacturers dominate the end-user landscape, holding 42% of the SATS market due to in-house assembly and testing requirements. Foundries account for 28%, providing specialized SATS capabilities for fabless design houses. Electronics OEMs hold 20%, driven by demand for integrated solutions. Test service providers constitute 10%, catering to contract-based testing requirements. The fastest-growing end-user segment is electronics OEMs, with adoption increasing due to the need for customized packaging and testing for next-generation devices. This trend is supported by over 62% of OEMs integrating advanced SATS processes into their supply chains. Regional adoption rates vary, with North America showing higher enterprise adoption and Asia-Pacific leading in volume-based utilization.

Asia-Pacific accounted for the largest market share at 42% in 2024, however, North America is expected to register the fastest growth, expanding at a CAGR of 4.2% between 2025 and 2032.

Asia-Pacific’s dominance is driven by its high-volume manufacturing capacity, with over 65% of global wafer-level packaging produced in China, Taiwan, and South Korea. In 2024, Asia-Pacific recorded more than 2.3 million wafer starts monthly, with China leading at 1.2 million. North America recorded a market volume of 910 thousand wafer starts, driven by demand from AI, automotive electronics, and aerospace sectors. Europe accounts for 18% of the market, led by Germany, France, and the UK, with strong regulatory compliance for green manufacturing. South America holds a 6% share, with Brazil leading regional demand for electronics manufacturing services. Middle East & Africa combined hold 4%, driven mainly by energy and defense applications. Regional variations in consumer behavior include North America’s higher adoption of AI-enabled SATS and Asia-Pacific’s focus on volume-driven cost efficiency.

How is innovation reshaping service delivery in advanced testing and assembly?

North America holds a 28% share of the global SATS market, with key demand from automotive electronics, AI computing, and aerospace sectors. Government initiatives such as the CHIPS Act provide over USD 52 billion in funding for semiconductor manufacturing, fostering expansion of testing and assembly capabilities. Technological advancements include AI-assisted testing, wafer-level fan-out packaging, and automated assembly lines, improving throughput by up to 22%. A leading local player, Amkor Technology, has recently expanded its advanced packaging capacity in Arizona, increasing wafer-level packaging output by 14% in 2024. Regional consumer behavior reflects higher enterprise adoption in healthcare, aerospace, and automotive electronics, with over 60% of SATS facilities integrating smart manufacturing solutions to enhance precision and reduce production time.

What trends are shaping precision and sustainability in advanced assembly services?

Europe holds a 19% market share in SATS, with Germany, France, and the UK driving most demand. Sustainability initiatives are critical, with over 72% of European SATS providers adopting green manufacturing practices to meet EU environmental directives. Regulatory bodies such as the European Commission emphasize circular economy compliance, requiring recycling of 85% of semiconductor waste by 2030. Adoption of heterogeneous integration and AI-based testing solutions is rising, with a 34% increase in high-volume applications in 2024. STMicroelectronics, based in France, expanded wafer-level packaging for automotive semiconductors, increasing yield efficiency by 16%. Regional consumer behavior reflects regulatory-driven demand for explainable SATS, particularly in high-precision manufacturing sectors such as automotive and healthcare electronics.

How is large-scale manufacturing redefining competitive advantage in the SATS market?

Asia-Pacific holds the largest market volume with a 42% share globally. China leads, producing 1.2 million wafer starts monthly, followed by Taiwan with 710 thousand and South Korea with 420 thousand. Japan is a leader in high-precision testing services for AI chips. Manufacturing trends include expansion of wafer-level fan-out packaging and automation in assembly lines, with investments exceeding USD 15 billion in 2024. Local player ASE Technology expanded heterogeneous integration capacity, improving throughput by 18%. Regional innovation hubs are concentrated in Taiwan, South Korea, and Singapore, focusing on AI and 5G-enabled SATS solutions. Consumer behavior reflects strong volume-driven adoption, with over 70% of SATS facilities operating automated assembly lines to optimize production efficiency and cost-effectiveness.

How are emerging economies accelerating adoption of advanced assembly solutions?

South America holds a 6% share, with Brazil leading at 4% of global SATS demand. Argentina contributes 1.2% with growing adoption in automotive electronics. Infrastructure developments, particularly in Brazil’s technology parks, are fostering domestic SATS capability expansion. Government incentives such as tax breaks and trade agreements with Asia-Pacific nations are boosting manufacturing investment. Local player CEITEC has advanced packaging services for automotive electronics, reducing defect rates by 12% in 2024. Regional demand is shaped by energy, agriculture electronics, and aerospace sectors, with 54% of SATS adoption tied to local industrial automation. Consumer behavior reflects demand for cost-efficient manufacturing and localized service capabilities.

What factors are driving niche growth in semiconductor assembly and testing in developing markets?

Middle East & Africa hold a 4% market share, with the UAE and South Africa leading regional demand. The UAE focuses on aerospace and defense electronics, while South Africa invests in renewable energy semiconductor assembly. Technological modernization includes adoption of smart testing and digital twin systems, enhancing assembly precision by over 15%. Local regulations encourage sustainable manufacturing practices, with over 60% of SATS providers aligning with ESG requirements. Mubadala Investment Company in the UAE expanded its packaging services capacity by 11% in 2024, integrating AI-based testing. Regional consumer behavior emphasizes high customization in aerospace, defense, and energy electronics, reflecting a preference for specialized SATS solutions.

China – 25% market share; high production capacity with over 1.2 million wafer starts monthly.

United States – 22% market share; strong end-user demand in AI, automotive electronics, and aerospace, supported by government funding initiatives.

The Semiconductor Assembly and Testing Services (SATS) market is moderately consolidated, with the top 5 companies collectively accounting for approximately 58% of the global market. The competitive landscape includes over 120 active players ranging from large-scale global leaders to specialized regional providers. Key players focus on strategic initiatives such as mergers, acquisitions, capacity expansion, and technology partnerships to strengthen their market positioning. For instance, several firms have invested in wafer-level fan-out packaging and advanced heterogeneous integration to meet demand for miniaturized and high-performance semiconductor devices. Innovation trends include AI-assisted testing, automated assembly lines, and eco-friendly manufacturing processes, with over 47% of providers adopting smart manufacturing solutions by 2024. Strategic partnerships and regional expansions are increasing, with companies targeting emerging economies to secure growth. The market is also influenced by technological modernization, regulatory changes, and sustainability mandates, which are reshaping competitive priorities. Firms are leveraging automation to reduce defect rates by up to 15%, enhance throughput, and improve yield, making competition increasingly technology-driven.

ASE Technology Holding Co., Ltd

JCET Group Co., Ltd

Siliconware Precision Industries Co., Ltd

STMicroelectronics

Powertech Technology Inc.

Unimicron Technology Corp

UTAC Holdings Ltd

Tongfu Microelectronics Co., Ltd

ChipMOS Technologies Inc.

The Semiconductor Assembly and Testing Services (SATS) market is undergoing a rapid technological transformation driven by advances in packaging, automation, and testing capabilities. Wafer-Level Packaging (WLP) and Fan-Out Wafer-Level Packaging (FOWLP) are becoming mainstream, enabling higher density integration with reduced form factors. Adoption of 3D integration technology is increasing, allowing for greater device performance and power efficiency. Automation is a critical trend, with over 62% of SATS providers implementing robotic assembly and AI-powered inspection systems to reduce error rates by up to 18%. Advanced testing techniques such as system-level testing and non-contact metrology are gaining traction to ensure reliability and yield optimization. Digital twin technology is emerging, with 48% of manufacturers piloting its use to simulate assembly processes, reducing defects and time-to-market. Environmental sustainability technologies are also growing in importance, with innovations in low-energy assembly lines and recyclable packaging materials. Additionally, AI-enabled predictive maintenance is enhancing equipment uptime by more than 20%, while data analytics platforms are improving throughput monitoring and quality control. These technological advancements position SATS providers to meet the demands of next-generation semiconductor devices, particularly for IoT, automotive, and 5G applications.

• In March 2023, Amkor Technology launched a high-density fan-out wafer-level packaging solution for 5G devices, increasing interconnect efficiency by 25%. Source: www.amkor.com

• In August 2023, ASE Technology announced an AI-powered automated testing system that reduced defect detection time by 30%, improving overall throughput. Source: www.aseglobal.com

• In January 2024, JCET Group unveiled a low-temperature bonding technology, reducing thermal stress during assembly by 22%, enhancing yield for sensitive components. Source: www.jcetglobal.com

• In July 2024, UTAC Holdings introduced an eco-friendly packaging process using 38% bio-based materials, reducing waste generation by 20%. Source: www.utacgroup.com

The Semiconductor Assembly and Testing Services (SATS) Market Report offers a comprehensive analysis of global market trends, opportunities, and technological evolution across multiple segments. It covers detailed segmentation by assembly type, testing methodologies, device type, and end-use applications. Key assembly types such as wafer-level packaging, flip-chip packaging, and system-in-package are examined alongside cutting-edge testing methods including electrical, reliability, and system-level testing. The report also offers geographic segmentation insights, addressing regional variations in demand, adoption patterns, and infrastructure development. Market focus extends across end-user industries including automotive, consumer electronics, telecommunications, and industrial electronics, highlighting sector-specific trends and innovation. The scope also incorporates emerging areas such as heterogeneous integration, AI-driven testing solutions, and sustainable manufacturing processes. Furthermore, the report addresses regulatory frameworks, sustainability mandates, and investment patterns that influence strategic decision-making. By integrating qualitative insights with quantitative data, the report provides a robust reference for stakeholders seeking to understand market breadth, competitive landscapes, technological advancements, and future growth directions.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 38104.08 Million |

|

Market Revenue in 2032 |

USD 50564.94 Million |

|

CAGR (2025 - 2032) |

3.6% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Amkor Technology, ASE Technology Holding Co., Ltd, JCET Group Co., Ltd, Siliconware Precision Industries Co., Ltd, STMicroelectronics, Powertech Technology Inc., Unimicron Technology Corp, UTAC Holdings Ltd, Tongfu Microelectronics Co., Ltd, ChipMOS Technologies Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |