Reports

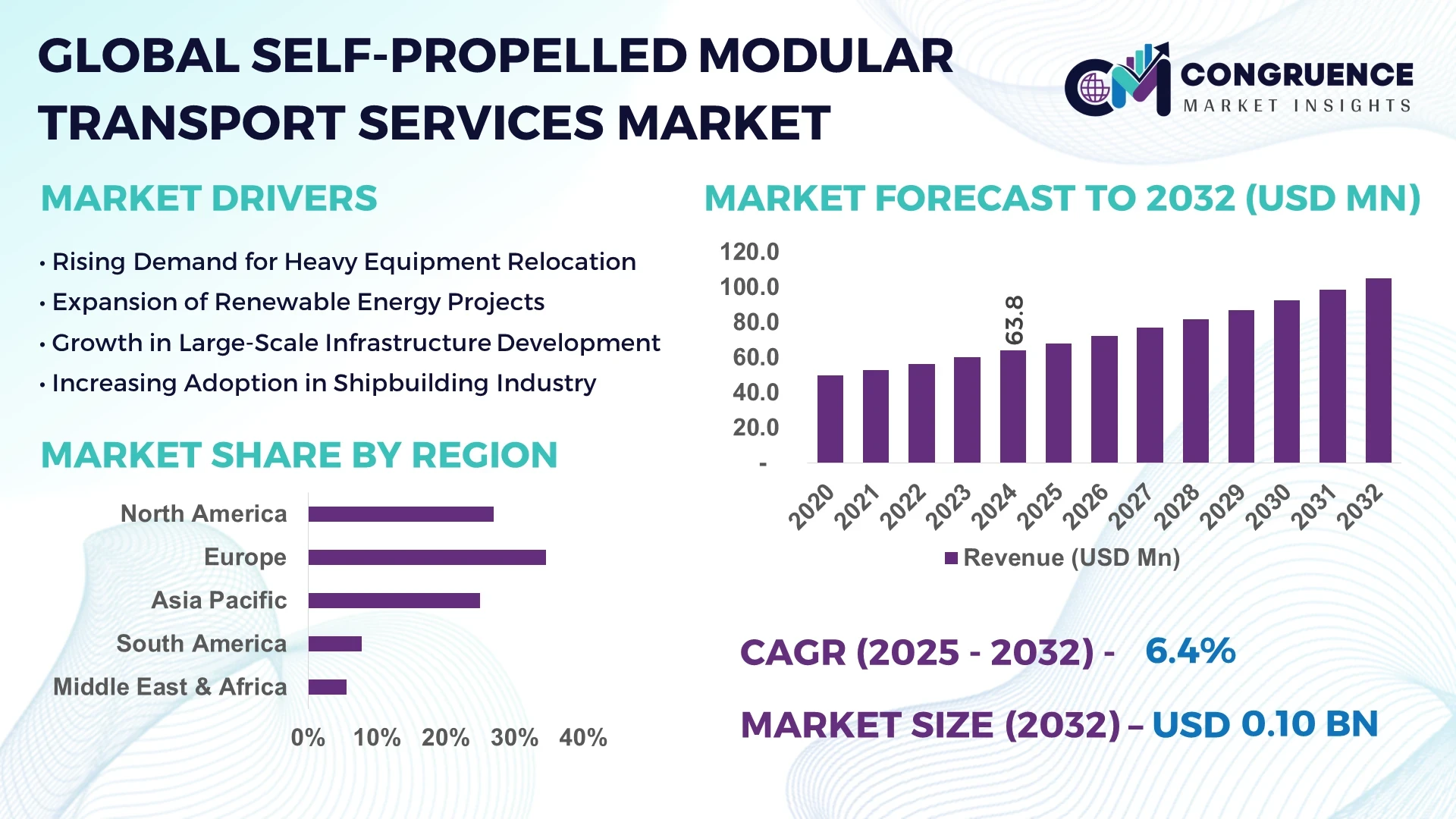

The Global Self-Propelled Modular Transport Services Market was valued at USD 63.84 Million in 2024 and is anticipated to reach a value of USD 104.86 Million by 2032 expanding at a CAGR of 6.4% between 2025 and 2032.

Germany leads the global Self-Propelled Modular Transport Services market with its extensive infrastructure investments, advanced engineering capabilities, and high deployment of automated transport systems across the heavy construction and shipbuilding sectors. The country also continues to adopt new manufacturing automation protocols, enhancing operational speed and precision.

The Self-Propelled Modular Transport Services market is witnessing steady growth driven by rising demand in heavy-load industries such as shipbuilding, construction, wind energy, and aerospace. These sectors require modular transport solutions to handle oversized and overweight cargo with precision and safety. Technological innovations such as GPS-integrated control systems, automated steering mechanisms, and hydraulic suspension advancements are significantly enhancing performance standards. Environmentally driven policies are pushing providers to adopt electric-powered modules, contributing to the shift toward sustainable logistics. Asia-Pacific, particularly China and India, is experiencing a surge in consumption due to large-scale infrastructure developments and increasing industrial output. Moreover, digital integration and predictive maintenance systems are emerging as key trends that allow operators to streamline transport logistics while minimizing downtime. These developments make Self-Propelled Modular Transport Services essential for modern industrial logistics strategies.

Artificial intelligence is increasingly revolutionizing the Self-Propelled Modular Transport Services Market by driving precision, safety, and automation in the movement of massive and complex cargoes. AI-powered routing algorithms are now enabling dynamic path planning, allowing modular transport systems to assess terrain, obstacles, and real-time traffic conditions to select the most efficient route with reduced human intervention. Additionally, AI-integrated load balancing ensures optimized distribution of weight across modular units, significantly reducing mechanical stress and enhancing equipment longevity.

In the Self-Propelled Modular Transport Services Market, predictive maintenance systems powered by AI are minimizing unplanned downtime through real-time diagnostics, reducing operational costs by up to 25%. These intelligent systems detect early signs of wear, misalignment, or hydraulic inefficiencies, allowing for timely interventions. Furthermore, computer vision and machine learning capabilities are now assisting in autonomous navigation and remote control operations, especially in restricted or hazardous environments.

AI is also contributing to better energy management within electric self-propelled modular transporters by adjusting energy use in real-time based on load size, terrain grade, and weather conditions. This leads to improved energy efficiency and supports the shift toward greener logistics. As the Self-Propelled Modular Transport Services Market continues to evolve, AI is becoming a critical component of smarter, safer, and more scalable transport solutions.

“In 2024, a leading European logistics firm integrated AI-based trajectory control and obstacle detection systems into its fleet of self-propelled modular transporters, reducing cargo delivery time by 18% and improving operational safety compliance in narrow and congested industrial zones.”

The Self-Propelled Modular Transport Services market is evolving rapidly due to the growing complexity of logistics in sectors such as offshore energy, shipbuilding, and large-scale civil construction. Increasing investments in infrastructure development and industrial expansion are fueling demand for highly specialized heavy-haul transportation systems. The market is being shaped by the integration of digital control systems, which provide enhanced load maneuverability, precision, and safety. Regulatory policies focusing on worker safety and emissions control are pushing companies to transition toward electric and hybrid modular transporters. At the same time, global supply chain modernization and just-in-time delivery requirements are driving adoption of these flexible transport solutions. End-users are increasingly favoring service-based business models, leading to a rise in demand for outsourcing heavy-load transportation to specialized providers. These shifts collectively reinforce the need for innovative, technology-driven solutions in the Self-Propelled Modular Transport Services market.

The expansion of renewable energy projects, particularly wind power, is a major driver of growth in the Self-Propelled Modular Transport Services market. Wind turbine components such as nacelles, blades, and towers are extremely large and heavy, requiring precise and secure transport over challenging terrains. The growing number of onshore and offshore wind farms, especially in Europe, the U.S., and China, is leading to higher demand for modular transport systems capable of handling complex logistics with safety and precision. According to recent data, global wind capacity additions exceeded 100 GW in 2023, driving large-scale deployment of transport services capable of supporting these installations. Self-propelled modular transporters equipped with hydraulic lift systems and intelligent control platforms are proving essential in reducing project delays and ensuring compliance with environmental and safety regulations.

Despite their advantages, the high capital and maintenance costs of self-propelled modular transport systems present a considerable restraint for broader adoption. These transporters are highly engineered machines requiring significant upfront investment and specialized personnel for operation and upkeep. Maintenance costs are further elevated by the need for periodic hydraulic system checks, software updates, and component replacements, especially in regions with limited access to advanced servicing infrastructure. Smaller companies and emerging economies often face budget constraints, making it difficult to justify such large expenditures, particularly when the frequency of use is low. Additionally, the need for skilled operators and trained technicians adds to operational overheads, limiting adoption among cost-sensitive market segments.

The emergence of large-scale infrastructure and megaprojects across Asia-Pacific, the Middle East, and Africa is opening significant opportunities in the Self-Propelled Modular Transport Services market. Urban redevelopment initiatives, transportation corridor developments, and smart city projects require efficient logistics solutions for transporting prefabricated building elements, tunnel boring machines, and bridge sections. For instance, infrastructure spending in Southeast Asia exceeded USD 300 billion in 2024, with a sizable share allocated to transportation and energy projects. These projects often involve transporting loads exceeding 500 tons over long distances and difficult terrains, creating a surge in demand for advanced modular transporter services. Cross-border logistics for industrial machinery and power systems is another emerging area, especially in regions with developing trade partnerships, offering ample room for market expansion.

One of the pressing challenges in the Self-Propelled Modular Transport Services market is maneuvering large cargo through urban centers or remote, underdeveloped regions. Urban areas often feature narrow roads, low bridges, and dense infrastructure, complicating the navigation of oversized loads. In contrast, remote project sites may lack proper roads, posing challenges related to terrain adaptability and route planning. Even with advanced steering systems and GPS-based navigation, real-world constraints like unpredictable road conditions, construction detours, or regulatory movement windows can disrupt logistics schedules. Moreover, obtaining permits for abnormal loads, especially across multiple jurisdictions, often results in administrative delays and legal complications, hindering the timely delivery of critical components and affecting project timelines.

• Rise in Modular and Prefabricated Construction: The adoption of modular and prefabricated construction is significantly altering transport logistics across industrialized regions. As construction companies increasingly shift toward off-site fabrication of building components, the demand for heavy-load transport systems capable of handling pre-assembled modules is accelerating. In North America and Western Europe, over 35% of new infrastructure projects utilized modular building methods in 2024. This trend directly supports the expansion of Self-Propelled Modular Transport Services, especially for transporting volumetric elements like bathroom pods, building frames, and utility cores to urban construction sites.

• Electrification of Self-Propelled Modular Transporters: Electric-drive modular transporters are emerging as a prominent trend in response to tightening emissions regulations. Major manufacturers have introduced battery-powered modules capable of operating in emission-sensitive zones such as ports, industrial parks, and urban construction sites. In 2024, nearly 20% of newly manufactured modular transporter units were electric-powered, showing a shift toward sustainable logistics. These models offer low-noise, zero-emission operations and are being integrated with regenerative braking systems to enhance energy efficiency during heavy-load movement.

• Integration of Telematics and Predictive Diagnostics: Advanced telematics systems embedded in modular transporters are enabling real-time tracking, diagnostics, and operational optimization. Fleet operators are utilizing AI-based predictive diagnostics to identify wear-and-tear patterns before mechanical failures occur. In 2024, more than 40% of the service providers in Europe adopted predictive maintenance platforms, resulting in a 22% reduction in unplanned equipment downtime. This trend enhances operational reliability and provides competitive advantage through reduced lifecycle costs.

• Growth in Cross-Continental Industrial Equipment Movement: The global increase in the movement of large industrial assets—such as reactors, wind turbine components, and aerospace assemblies—has triggered growth in cross-border Self-Propelled Modular Transport Services. Particularly in Asia and the Middle East, over-dimensional cargo shipments have increased by more than 30% compared to 2022 levels. Projects involving intermodal transfers across ports, highways, and inland zones are driving up demand for customized transport modules with higher axle loads and advanced steering systems capable of adapting to regional road infrastructure variations.

The Self-Propelled Modular Transport Services market is segmented based on type, application, and end-user. The type segment includes electronic, hydraulic, and hybrid models, each catering to different load capacities and environmental requirements. Applications range from transporting wind turbine components to aerospace parts, construction modules, and industrial machinery. Among these, construction and energy sectors continue to dominate, driven by increasing infrastructure and renewable energy projects globally. End-user segmentation reveals a strong foothold in heavy engineering, shipbuilding, and oil & gas industries, while growing usage is also seen in civil infrastructure development. Innovations such as digital control systems and remote operation capabilities are influencing preferences across all segments, especially for projects in regulated or remote environments.

Hydraulic self-propelled modular transporters remain the leading type due to their superior load-carrying capacity and flexibility across rugged terrains and uneven surfaces. These units are widely adopted in shipyards, heavy industries, and infrastructure projects where large-scale components must be moved with precision. Electronic models are the fastest-growing segment, driven by the global shift toward energy-efficient and low-noise transport solutions. These units are particularly suited for urban projects and emission-regulated zones. Hybrid models combining electric propulsion with hydraulic control systems are gaining niche traction in sectors that demand both power and environmental compliance. Additionally, specialized low-bed and high-frame configurations are being developed to support unique cargo profiles, further diversifying the product landscape and driving customization in service offerings.

The construction and infrastructure segment leads the market, as massive concrete sections, bridge elements, and modular building units increasingly require high-capacity transport services. Rapid urbanization, smart city initiatives, and high-rise development projects worldwide continue to expand this application. Wind energy installations represent the fastest-growing application area, with rising demand for moving large turbine blades and nacelles across long distances, often through rugged terrain. Transporting aerospace structures, such as aircraft fuselages and satellite systems, also contributes to market demand, albeit at a smaller scale. Meanwhile, applications in shipbuilding and oil & gas sectors remain steady, particularly in countries with active seaports or offshore drilling operations. These diverse applications collectively support the evolution and expansion of self-propelled transport service capabilities.

Heavy engineering and manufacturing companies are the dominant end-users, relying heavily on Self-Propelled Modular Transport Services for relocating equipment, production modules, and assembly line components. These industries demand high-capacity, precision-oriented logistics solutions that minimize delays and ensure safe transit of critical assets. The renewable energy sector is the fastest-growing end-user category, driven by the global surge in wind and solar projects that require the transport of massive structural components to remote or offshore locations. The shipbuilding industry remains a consistent contributor, particularly in regions like East Asia and Northern Europe where large-scale vessel production is active. Civil infrastructure contractors and EPC (Engineering, Procurement, and Construction) firms are also increasingly utilizing these services to move large preassembled bridge spans, beams, and tunnel boring machines, especially within megaprojects.

Europe accounted for the largest market share at 34.6% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.9% between 2025 and 2032.

Europe’s dominance in the Self-Propelled Modular Transport Services Market is supported by a dense network of heavy industries, consistent investment in infrastructure, and mature regulatory frameworks focused on transport safety. On the other hand, Asia-Pacific is witnessing a surge in demand, especially across industrial corridors in China, India, and Southeast Asia, where large-scale civil infrastructure and energy projects are ramping up the adoption of modular transport services. Global expansion of cross-border logistics, growing usage in renewable energy transport, and tech-enabled service innovations are collectively driving regional diversification in the Self-Propelled Modular Transport Services Market. Variations in environmental policies, digital infrastructure, and industrial density across regions are also influencing how quickly service providers scale operations and upgrade their fleets.

Heavy Logistics Transformation Driven by Construction and Renewable Sectors

North America held 28.2% of the global market share in the Self-Propelled Modular Transport Services Market in 2024, driven by active infrastructure modernization and high demand from wind energy, aerospace, and oil & gas industries. The U.S. and Canada are prioritizing transport modernization projects, contributing to increased usage of modular transporters in prefabricated construction and industrial relocation services. The implementation of the U.S. Infrastructure Investment and Jobs Act has opened funding channels that support large equipment mobilization and heavy-haul logistics. In parallel, technological innovations such as AI-based fleet diagnostics and remote-controlled SPMT units are accelerating digital transformation. Local governments are increasingly enforcing updated load compliance and emissions regulations, prompting service providers to upgrade fleets to electric and hybrid models, thereby boosting market adaptability.

Digital Innovation and Policy-Led Adoption Strengthening Specialized Transport Sector

Europe contributed 34.6% to the global Self-Propelled Modular Transport Services Market in 2024, led by mature markets including Germany, the United Kingdom, and France. Germany continues to be a hub for shipbuilding, automotive, and wind energy logistics, generating high-volume demand for heavy-load transportation. The European Union’s Green Deal and sustainability initiatives are pushing for the electrification of SPMTs and the integration of real-time telematics. France has also enhanced urban mobility laws to accommodate modular transport operations in smart city developments. Additionally, widespread adoption of IoT-enabled tracking and compliance systems in the logistics sector is fostering digital transparency. These trends are consolidating Europe’s lead in technologically advanced modular transport services while maintaining compliance with stringent EU-wide transportation regulations.

Infrastructure Boom and Smart Manufacturing Boosting Demand Across Industrial Hubs

Asia-Pacific recorded the highest growth momentum in the Self-Propelled Modular Transport Services Market in 2024, capturing over 22.1% of total volume. China, India, and Japan are the primary drivers due to aggressive investments in manufacturing, industrial automation, and energy projects. China's Belt and Road Initiative and India’s Gati Shakti program are increasing the frequency of oversized cargo transport, necessitating the use of advanced SPMT units. High-capacity infrastructure construction and modular urban development further reinforce market expansion. Additionally, regional technology hubs such as Shenzhen and Bengaluru are supporting domestic innovation in modular transport automation. The integration of AI in route optimization and load balancing across Asian fleets is creating new operational benchmarks in large-scale logistics.

Energy Infrastructure Growth and Industrial Logistics Supporting Market Expansion

Brazil and Argentina are the two key contributors to the Self-Propelled Modular Transport Services Market in South America, jointly accounting for over 7.3% of global share in 2024. Brazil’s ongoing investments in renewable energy infrastructure—especially wind and hydroelectric projects—are stimulating demand for specialized heavy transport. Argentina is expanding its mining and industrial processing sectors, requiring robust modular transporter services for equipment mobilization. Government-backed logistics infrastructure upgrades, including highway modernization programs, are facilitating smoother movement of oversized cargo. Trade liberalization efforts and favorable import duty policies for transport machinery are further supporting market growth. As digital adoption remains limited, companies are gradually integrating GPS tracking and remote diagnostics to meet evolving customer expectations.

Energy Sector Dominance and Cross-Border Trade Creating Transport Service Opportunities

The Middle East & Africa region accounted for 7.8% of the Self-Propelled Modular Transport Services Market in 2024, led by strong activity in the oil & gas, construction, and defense industries. Countries like the UAE, Saudi Arabia, and South Africa are at the forefront of infrastructure development and strategic asset relocation projects. The expansion of oil refineries and LNG facilities requires the transport of massive equipment, fueling demand for modular transport services. Technological upgrades are being introduced through partnerships with global logistics players, with a focus on integrating load monitoring and safety automation systems. Local trade agreements such as the African Continental Free Trade Area (AfCFTA) are expected to streamline logistics across borders, accelerating the adoption of advanced SPMTs in emerging African markets.

Germany – 18.5% market share

High production capacity, extensive use in shipbuilding, and strong engineering infrastructure drive Germany’s leadership in the Self-Propelled Modular Transport Services Market.

China – 15.2% market share

Strong end-user demand from large-scale construction, renewable energy installations, and smart city projects support China’s position in the global Self-Propelled Modular Transport Services Market.

The Self-Propelled Modular Transport Services market is characterized by a moderately consolidated competitive environment with approximately 25–30 active global and regional service providers. Leading companies are focused on offering comprehensive heavy-lift transport solutions, often bundled with engineering consulting and route feasibility services. Competitive differentiation is largely based on fleet capacity, regional coverage, technological integration, and custom service offerings. Top-tier players are investing in digital fleet management systems and predictive maintenance tools to increase reliability and minimize downtime.

Strategic collaborations between transport service providers and manufacturers of modular transporters are becoming increasingly common to enhance performance capabilities and address region-specific logistical challenges. In 2024, multiple firms launched AI-integrated SPMT units featuring remote-controlled navigation and autonomous obstacle detection, aimed at improving precision in congested or restricted environments. Additionally, market participants are expanding their operational footprint through mergers, acquisitions, and joint ventures, especially in Asia-Pacific and the Middle East. With rising demand from renewable energy, infrastructure, and defense sectors, competition is intensifying around rapid deployment, scalable transport solutions, and regulatory compliance.

Mammoet

Sarens Group

ALE Heavylift (now part of Mammoet, included here due to operational continuity)

Fagioli S.p.A.

Dorman Long Technology Limited

Global Specialized Services Inc.

BigLift Shipping

Anjes Cross Border Transportation Co., Ltd.

ATS International

Barnhart Crane & Rigging Company

Technological innovation is reshaping the Self-Propelled Modular Transport Services market, enabling higher precision, safety, and operational efficiency. One of the most transformative developments is the integration of autonomous navigation systems, which utilize GPS, LiDAR, and machine vision to enhance maneuverability in complex environments such as narrow urban corridors or uneven terrains. These systems help reduce operator dependency and improve safety in high-risk zones. Hydraulic lifting systems have also seen major advancements. Modern SPMTs are now equipped with multi-axle synchronized hydraulic suspensions, allowing for even load distribution and automatic leveling on slopes or unpaved surfaces. These features are critical for transporting extremely heavy or delicate cargo such as wind turbine components, reactors, or aerospace structures.

Electric propulsion modules are emerging as a sustainable alternative to diesel-driven units. These battery-powered SPMTs, especially in Europe and North America, are gaining popularity for zero-emission operations and reduced noise levels, essential for urban and sensitive industrial zones. Additionally, real-time telematics platforms are becoming standard across fleets. These technologies enable predictive maintenance through sensor-based diagnostics, minimizing downtime and reducing lifecycle costs. The use of modular control software, allowing scalable configuration of multiple transport units, is another key advancement that provides flexibility for varying project requirements, improving operational turnaround time and asset utilization.

• In February 2024, Mammoet unveiled its next-generation electric self-propelled modular transporter, which reduces CO₂ emissions by 60% during operations. The unit integrates regenerative braking and real-time energy monitoring to optimize performance in industrial zones and port facilities.

• In November 2023, Sarens expanded its fleet in India with 64-axle lines of electronic SPMTs. The expansion was made to support growing wind energy logistics and was tailored to handle nacelle and tower sections weighing over 200 tons per load.

• In March 2024, Fagioli S.p.A. implemented an AI-based load monitoring system on its modular transporters to enhance route safety in urban infrastructure projects. The system provides live data on axle load distribution and terrain adaptability, reducing manual intervention during critical transport operations.

• In July 2023, Barnhart Crane & Rigging Company partnered with a software firm to develop a centralized digital control platform for its modular transport operations. The system enables remote fleet management, real-time diagnostics, and advanced job scheduling, improving asset allocation across the U.S.

The Self-Propelled Modular Transport Services Market Report offers a comprehensive assessment of current and emerging market dynamics across multiple dimensions. It covers detailed analysis of market segments based on type—such as hydraulic, electric, and hybrid SPMTs—and their application in key industries including construction, wind energy, shipbuilding, aerospace, and heavy engineering. Special attention is given to the role of service providers and the transition from asset ownership to outsourced logistics models. The geographic scope spans across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, each evaluated for its unique industrial growth drivers, policy environment, and demand patterns. The report highlights major consuming countries such as Germany, China, the U.S., Brazil, and the UAE, detailing their infrastructure projects, industrial activities, and technological readiness.

Technological aspects explored include the adoption of electric propulsion, AI-driven diagnostics, and autonomous steering systems, as well as advancements in telematics and hydraulic performance. Niche markets—such as offshore wind transport services, defense infrastructure logistics, and digital twin-based fleet management—are also profiled to reflect the expanding scope of the industry. Overall, the report provides stakeholders with strategic insights necessary for market entry, expansion planning, operational optimization, and technology investment decisions.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 63.84 Million |

|

Market Revenue in 2032 |

USD 104.86 Million |

|

CAGR (2025 - 2032) |

6.4% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Mammoet, Sarens Group, ALE Heavylift (now part of Mammoet, included here due to operational continuity), Fagioli S.p.A., Dorman Long Technology Limited, Global Specialized Services Inc., BigLift Shipping, Anjes Cross Border Transportation Co., Ltd., ATS International, Barnhart Crane & Rigging Company |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |