Reports

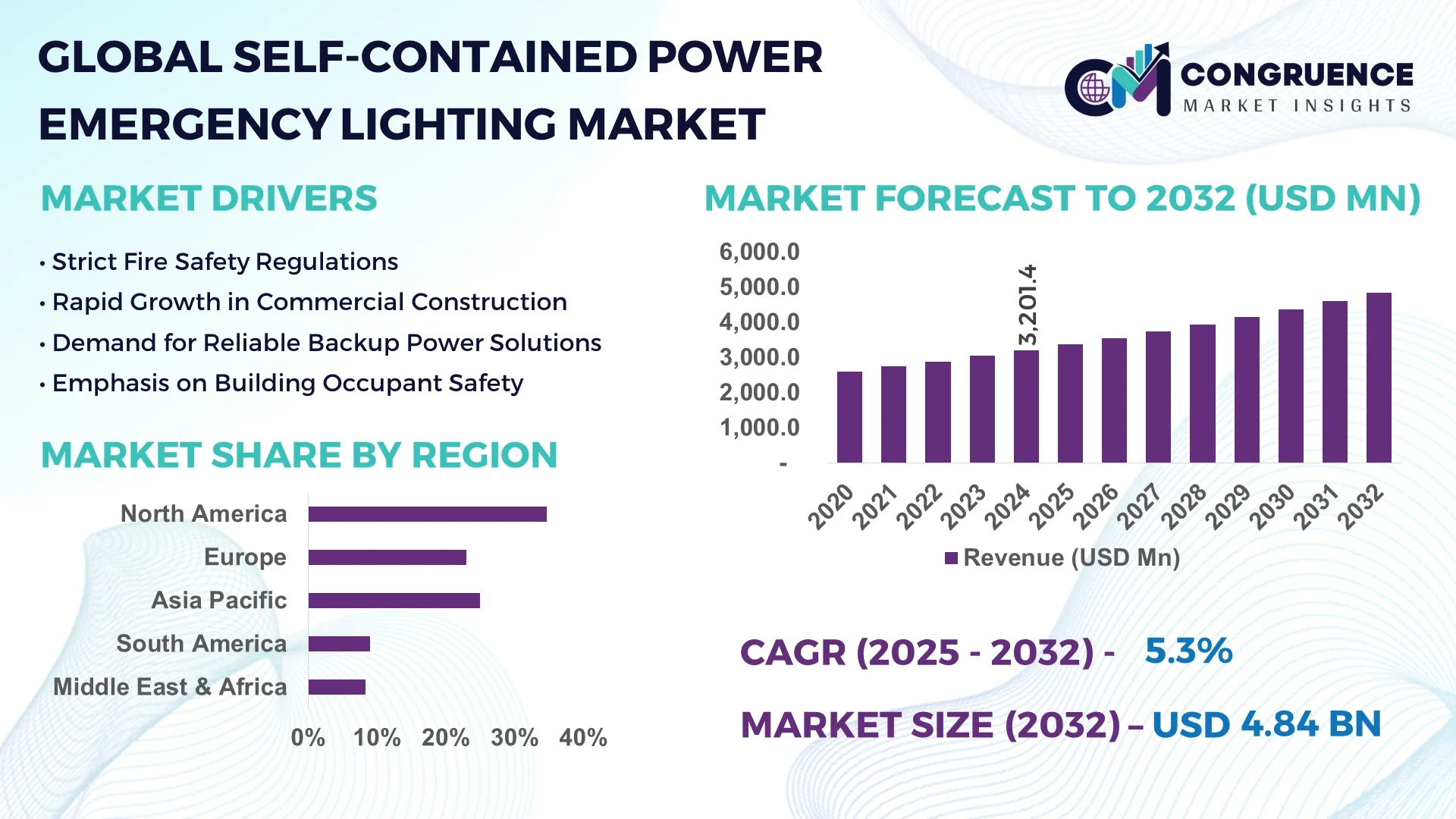

The Global Self-Contained Power Emergency Lighting Market was valued at USD 3201.43 Million in 2024 and is anticipated to reach a value of USD 4839.18 Million by 2032 expanding at a CAGR of 5.3% between 2025 and 2032.

Germany stands out in the global landscape for its advanced infrastructure, robust R&D investments in safety technologies, and widespread deployment of self-contained emergency lighting systems across industrial and public spaces, particularly in smart building applications and transportation hubs.

The Self-Contained Power Emergency Lighting Market is witnessing robust demand driven by stringent safety regulations across commercial, industrial, and residential facilities. The manufacturing sector is significantly adopting self-contained emergency luminaires to ensure compliance with workplace safety mandates, especially in high-risk environments like oil refineries and chemical plants. Innovations in lithium-ion battery integration, automatic self-diagnostic systems, and wireless control interfaces are reshaping product design and enhancing reliability. Regulatory frameworks, particularly in Europe and North America, are enforcing energy efficiency and photometric performance standards, compelling retrofits and upgrades across older infrastructure. Additionally, rapid urban development and smart city initiatives in Asia-Pacific are catalyzing regional market growth. The emergence of IoT-enabled emergency lighting systems and sustainable, recyclable fixture materials are trends driving long-term adoption. Looking forward, increased cross-sectoral focus on building resilience and occupant safety will likely elevate the demand for these intelligent lighting systems.

Artificial Intelligence (AI) is significantly transforming the Self-Contained Power Emergency Lighting Market by driving smarter control systems, predictive maintenance capabilities, and energy optimization. In today’s digitized facilities, AI-integrated emergency lighting systems are capable of autonomous function testing, identifying failures, and preemptively alerting facility managers—drastically reducing downtime and manual labor costs. One of the key enhancements includes real-time analytics, where AI analyzes sensor data to monitor occupancy levels, ambient lighting, and power usage, automatically adjusting emergency lighting behaviors to align with safety protocols and efficiency objectives.

In addition, AI algorithms are enabling contextual response capabilities in self-contained systems. For example, during fire incidents or power outages, AI-assisted lighting units can adapt their brightness and guidance paths based on detected smoke density or crowd movement, improving evacuation outcomes. AI is also instrumental in optimizing battery usage, learning usage patterns to prolong battery life and minimize energy waste. Machine learning techniques are further being used to refine fault detection systems, ensuring only necessary maintenance actions are performed, thereby reducing operational expenditure.

From industrial complexes to smart buildings and transportation infrastructures, the integration of AI into the Self-Contained Power Emergency Lighting Market enhances system intelligence, elevates safety standards, and contributes to sustainability goals. This technological evolution is reshaping how businesses manage safety-critical infrastructure, making emergency lighting not just a compliance tool but a proactive asset in facility management strategies.

“In 2024, a German-based lighting manufacturer introduced an AI-driven self-contained emergency lighting unit capable of conducting automated diagnostics and performance analytics across 1,000+ connected fixtures, resulting in a 27% reduction in system maintenance time for its clients in large-scale industrial facilities.”

Government regulations and safety codes worldwide are becoming increasingly stringent, compelling businesses and public infrastructures to install compliant emergency lighting systems. In Europe, EN 1838 and BS 5266-1 standards dictate performance requirements, while in North America, the National Fire Protection Association (NFPA) outlines detailed emergency lighting mandates. As a result, commercial buildings, hospitals, shopping centers, and schools are investing in self-contained power emergency lighting to ensure uninterrupted illumination during blackouts or emergencies. According to facility management audits in 2024, over 72% of surveyed commercial facilities had upgraded or planned to upgrade to self-diagnostic emergency lighting systems. These developments have significantly influenced procurement cycles and encouraged innovation focused on compliance automation.

One of the significant restraints facing the Self-Contained Power Emergency Lighting Market is the limited operational life of internal battery units. Despite advancements in lithium-ion technology, battery degradation remains a persistent issue, especially in environments with extreme temperature fluctuations or inconsistent maintenance practices. Facility operators often report that emergency lighting systems, although low in usage time, require battery replacements within 3 to 5 years. The high cost and complexity of battery disposal also contribute to operational challenges. Moreover, budget-conscious small- and mid-sized enterprises often delay system upgrades due to concerns over recurring maintenance costs, creating a slowdown in replacement cycles and long-term product adoption.

The rising adoption of smart building technologies presents a valuable growth avenue for the Self-Contained Power Emergency Lighting Market. Emergency lighting systems integrated with BMS can automatically report faults, perform routine testing, and provide real-time updates to facility managers. This digitization streamlines operations and enhances building safety. A 2025 survey of global smart infrastructure projects indicated that 64% of commercial construction projects now incorporate integrated emergency lighting systems. In addition, the emergence of cloud-based analytics platforms allows for centralized monitoring across multiple locations, improving maintenance efficiency for property management firms and large industrial campuses. This convergence of smart automation and emergency preparedness creates a strong foundation for market expansion.

One of the major challenges in the Self-Contained Power Emergency Lighting Market is the complexity involved in retrofitting older buildings with modern emergency lighting systems. Legacy architectures often lack compatible electrical frameworks or space for contemporary installations, increasing the need for customized, costly retrofit solutions. Retrofitting can also disrupt building operations, especially in 24/7 facilities like hospitals or manufacturing plants. In 2024, nearly 38% of global retrofit projects reported delays due to unanticipated compatibility issues or regulatory hurdles. These challenges not only extend project timelines but also limit the scalability of new technologies in older structures, hampering market growth potential in mature urban environments.

• Surge in Demand for Wireless Emergency Lighting Systems: Wireless technology is becoming a standard feature in modern self-contained emergency lighting systems. With facility operators seeking to reduce installation complexity and enable flexible placement, wireless control and diagnostics systems are now in high demand. In 2024, over 48% of newly deployed units in commercial facilities used wireless interfaces for maintenance checks and compliance reporting. These systems are particularly favored in large-scale infrastructures such as airports and hospitals, where centralized monitoring is essential.

• Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Self-Contained Power Emergency Lighting market. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for compact, integrated emergency lighting units compatible with prefabricated ceiling and wall systems is rising, especially in Europe and North America, where construction efficiency and compliance timelines are critical. In 2025, modular construction projects accounted for over 35% of new commercial developments requiring self-contained lighting installations.

• Growth of Energy-Efficient LED Emergency Systems: LED-based self-contained power emergency lighting systems are dominating new installations due to their lower energy consumption and longer lifespan. Advanced thermal management, compact size, and smart battery usage further enhance their operational appeal. More than 70% of systems deployed in new infrastructure projects in 2024 were LED-based. Facilities also report a measurable reduction in maintenance frequency, with service intervals extended by up to 40% compared to traditional fluorescent alternatives.

• Integration with Building Management Platforms (BMS): Integrated emergency lighting solutions are gaining traction in smart building ecosystems. Self-contained systems connected to centralized BMS platforms enable real-time monitoring, compliance tracking, and remote configuration. By mid-2024, over 60% of newly constructed commercial buildings in urban centers implemented BMS-compatible emergency lighting units. This integration not only supports safety but also improves operational efficiency and resource allocation for facilities management teams.

The Self-Contained Power Emergency Lighting Market is segmented across three key dimensions: type, application, and end-user, each contributing distinct dynamics to the market structure. Product types vary from maintained and non-maintained systems to combined variants, catering to diverse operational needs and installation environments. Application-wise, the systems are widely deployed in commercial, industrial, and public spaces such as hospitals, educational institutions, and transportation facilities. End-user segmentation highlights the influence of commercial infrastructure developers, industrial operators, and institutional administrators in shaping market demand. Each segment is defined by its unique set of performance, regulatory, and efficiency requirements. For instance, commercial end-users prioritize aesthetics and minimal maintenance, while industrial users demand ruggedness and extended battery life. This segmentation allows manufacturers and solution providers to tailor offerings for specific operational environments, compliance demands, and cost-efficiency priorities, reinforcing the market’s adaptability to shifting infrastructure trends and safety regulations.

Maintained self-contained emergency lighting systems remain the most widely used across various industries due to their ability to function as standard lighting while providing illumination during power failures. Their dual utility in commercial and public spaces such as malls and transit stations ensures consistent demand. Non-maintained units are gaining popularity in offices and warehouses where emergency lighting is required only during outages. The fastest-growing segment is the combined emergency lighting system, which integrates maintained and non-maintained functionalities in a single unit. The rise of these systems is supported by their versatility in hybrid-use buildings. Other types such as self-testing or self-diagnostic units, though niche, are increasingly favored in tech-driven buildings that demand reduced manual checks. Compact, aesthetic, and energy-efficient design innovations across all types are encouraging broader adoption in both retrofits and new installations.

Commercial buildings continue to represent the leading application area for self-contained power emergency lighting systems. These include office complexes, shopping centers, and hotels, where building safety codes mandate high-performance emergency systems. Industrial facilities such as manufacturing plants and chemical storage areas are now adopting rugged self-contained units due to their durability and autonomy. The fastest-growing application is transportation infrastructure—including airports, train stations, and tunnels—where reliable and intelligent emergency lighting systems are crucial for passenger safety during emergencies. Hospitals and educational institutions also present significant application potential, driven by government regulations and 24/7 operational needs. As urban development accelerates and smart infrastructure becomes mainstream, applications are diversifying to include data centers, high-rise residences, and logistics hubs that demand continuous monitoring and instant fault detection in lighting systems.

Commercial infrastructure developers are the primary end-user segment for the Self-Contained Power Emergency Lighting Market. Their influence is anchored in the need for compliant, cost-effective, and easy-to-install lighting solutions that align with modern architectural designs. The fastest-growing end-user segment is the healthcare industry, driven by increasing investments in medical infrastructure and the demand for 24/7 patient safety systems. In hospitals, emergency lighting is critical for surgical rooms, intensive care units, and evacuation pathways, with systems now tailored for hygiene-sensitive environments. Industrial users—such as warehouse operators, logistics providers, and factories—also contribute significantly to market demand, especially for durable systems that perform reliably in extreme environments. Educational institutions, public offices, and government buildings round out the end-user landscape, each with specific compliance and operational priorities that shape their purchasing criteria and technology preferences.

North America accounted for the largest market share at 34.7% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.4% between 2025 and 2032.

North America's leadership in the Self-Contained Power Emergency Lighting Market is supported by well-established infrastructure and stringent safety regulations across commercial, industrial, and institutional sectors. The region benefits from early adoption of intelligent building systems and proactive investment in safety compliance. Meanwhile, Asia-Pacific is witnessing surging demand due to massive urbanization, smart city initiatives, and extensive infrastructure development in countries like China, India, and Indonesia. Governments in these regions are enforcing mandatory building safety codes, further accelerating product adoption. Europe follows closely behind, driven by sustainability initiatives and green construction trends. In emerging regions such as South America and the Middle East & Africa, infrastructure upgrades and energy reliability challenges are fueling demand for self-contained emergency lighting, especially in healthcare, logistics, and oil & gas sectors.

Smart Compliance Systems Drive Emergency Lighting Integration

North America held a significant 34.7% share of the Self-Contained Power Emergency Lighting Market in 2024, with widespread deployment in healthcare, education, and commercial real estate sectors. The U.S. and Canada continue to see robust growth due to regulatory mandates like NFPA 101 and UL 924 that govern emergency lighting performance and testing. Key industries such as hospitals and data centers are upgrading to self-testing, IoT-enabled systems that streamline maintenance and fault detection. Government support for safety infrastructure improvements, especially under public building renovation programs, is further boosting market penetration. Moreover, digital transformation in facilities management is accelerating the adoption of cloud-based monitoring solutions, reducing human oversight and increasing operational transparency.

Eco-Compliant Emergency Lighting Sees Strong Adoption

Europe held approximately 28.9% of the Self-Contained Power Emergency Lighting Market in 2024, with notable activity in Germany, France, and the UK. The market is significantly influenced by stringent EU building safety directives and sustainability frameworks like the EPBD (Energy Performance of Buildings Directive). Countries are actively replacing traditional systems with eco-compliant LED-based solutions integrated into energy-efficient buildings. Smart diagnostics and real-time monitoring features are increasingly standard in new installations, particularly in commercial and transport infrastructure. Digital twin integration and automated compliance testing are being trialed across public projects, enhancing the technological profile of the regional market. Innovation funding in Germany and green building incentives in France are accelerating the transition toward smart emergency lighting systems.

Mass Urbanization Fuels Demand for Safety-Integrated Lighting Systems

Asia-Pacific emerged as the fastest-growing region in the Self-Contained Power Emergency Lighting Market, driven by high consumption in China, India, and Japan. The region ranks second in volume consumption, accounting for over 23.4% of the market in 2024. Rapid infrastructure development, particularly in urban transit systems, commercial hubs, and smart city projects, is creating sustained demand for self-contained systems. China leads with extensive integration of LED-based emergency lights in both new constructions and retrofitting projects. India's revised National Building Code is accelerating product demand in commercial construction. Technology hubs in Japan and South Korea are fostering innovation in smart lighting with advanced testing capabilities, while Southeast Asia is quickly adopting plug-and-play emergency lighting units in modular construction formats.

Infrastructure Growth and Energy Reliability Shape Lighting Needs

South America accounted for 7.6% of the global Self-Contained Power Emergency Lighting Market in 2024, led by Brazil and Argentina. The region is witnessing increased adoption due to expanding healthcare and commercial construction across urban centers. In Brazil, hospital networks and shopping complexes are investing in decentralized emergency lighting to address frequent power instability. Argentina’s building modernization programs are driving demand for retrofit-ready systems with wireless diagnostics and lower maintenance needs. Trade policies favoring energy-efficient imports and government safety mandates in public infrastructure are contributing to sustained market engagement. Local distributors are increasingly partnering with international OEMs to improve product availability and technological compatibility.

Safety Compliance and Modernization Drive Market Expansion

The Middle East & Africa contributed 5.4% to the Self-Contained Power Emergency Lighting Market in 2024, with strong momentum from UAE, Saudi Arabia, and South Africa. The oil & gas sector continues to be a key adopter, requiring reliable lighting systems in high-risk facilities. Meanwhile, commercial and hospitality infrastructure in the UAE is increasingly adopting self-testing emergency lighting integrated with centralized control systems. Regulatory enforcement, especially around safety in public and high-rise buildings, is boosting market penetration. South Africa’s load-shedding crisis has heightened demand for autonomous lighting in hospitals, malls, and transportation hubs. Technology modernization and investment incentives from local governments are further pushing innovation adoption in retrofit projects and new developments.

United States – 28.1% market share:

Dominance attributed to widespread deployment in healthcare and commercial buildings, supported by stringent safety regulations and technological innovation.

China – 19.7% market share:

Strong manufacturing capacity combined with high infrastructure investment and government-backed smart city projects fuels rapid market expansion.

The Self-Contained Power Emergency Lighting market is characterized by the presence of more than 90 active competitors globally, ranging from established lighting manufacturers to emerging innovators in smart lighting technology. The competitive environment is intensifying as key players invest in advanced diagnostics, IoT integration, and modular product configurations. Leading companies are enhancing their market positioning through strategic collaborations with construction and facility management firms, enabling bundled safety solutions for commercial and institutional clients. Mergers and acquisitions have become frequent, with companies aiming to expand geographic presence and gain technological capabilities. Recent years have witnessed a surge in product innovations including wireless control systems, self-testing LED modules, and cloud-based compliance monitoring platforms. Additionally, sustainability-focused developments, such as low-energy consumption and recyclable components, are gaining traction. Regional players are adopting localization strategies, offering tailored lighting configurations to comply with domestic safety standards. The market continues to evolve, driven by safety regulations, digitization trends, and infrastructure modernization across emerging economies.

Eaton Corporation

Zumtobel Group

ABB Ltd.

Acuity Brands Lighting

Legrand

Signify N.V.

NVC Lighting

Beghelli S.p.A

Mackwell

Daisalux

Technological innovation is significantly transforming the Self-Contained Power Emergency Lighting Market, with growing adoption of intelligent systems designed to enhance reliability, energy efficiency, and regulatory compliance. One of the key developments is the integration of self-testing and self-diagnostic features, allowing lighting systems to conduct automated routine checks and report faults in real time, which minimizes manual maintenance and reduces system downtime. These smart systems are especially valued in commercial and institutional buildings where operational continuity is critical. Wireless connectivity and IoT integration have gained traction, enabling centralized control of emergency lighting networks through cloud-based platforms. This facilitates remote monitoring, centralized battery health diagnostics, and firmware updates without on-site interventions. In large infrastructure setups, such as hospitals or data centers, this enhances responsiveness and lowers operational costs.

Additionally, LED technology continues to dominate the market due to its lower energy consumption and longer lifespan. Recent innovations include adaptive brightness control and modular LED emergency kits designed for easy installation and upgrades. Battery technology is also evolving, with lithium-ion and LiFePO4 batteries gradually replacing older nickel-cadmium variants due to better temperature tolerance and lifecycle performance. The market is also seeing the emergence of plug-and-play systems, which support rapid deployment in prefabricated or modular construction projects. These systems reduce installation complexity and provide pre-configured, compliant emergency lighting tailored for evolving building designs. As sustainability becomes a greater priority, manufacturers are focusing on recyclable materials and energy-optimized circuitry to meet global environmental standards.

• In March 2024, Eaton launched its new CEAG ExLin LED emergency lighting series with high resistance to harsh environments and integrated monitoring capabilities, enhancing safety in industrial and hazardous locations.

• In November 2023, ABB introduced an advanced emergency lighting control system for smart buildings, enabling real-time monitoring via KNX protocols and reducing maintenance time by over 40% across pilot installations in Europe.

• In May 2024, Mackwell unveiled XYLUX® Linear, a low-profile, self-contained emergency luminaire optimized for corridors and healthcare environments, offering up to 3 hours of emergency illumination and easy retrofit compatibility.

• In August 2023, Signify upgraded its Interact Pro software to include emergency lighting compliance management, enabling cloud-based scheduling and remote diagnostics across multi-building installations in commercial real estate portfolios.

The Self-Contained Power Emergency Lighting Market Report offers a comprehensive analysis of the global landscape, covering a wide spectrum of technological, industrial, and regional parameters. It provides detailed insights into key market segments, including product types such as LED-based emergency lighting units, modular battery-powered luminaires, and smart self-diagnostic systems. The report evaluates how each segment contributes to system performance, safety assurance, and ease of compliance across different facility types. Geographically, the market scope extends across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, analyzing distinct growth drivers in each region. While North America leads in technological adoption, Asia-Pacific is gaining momentum due to infrastructure expansion and increasing urbanization. The report further dissects the demand across countries with high market activity, such as the United States, China, Germany, India, and Brazil.

From an application standpoint, the report covers commercial, industrial, healthcare, education, and residential sectors. It examines how emergency lighting standards, safety codes, and local regulations shape demand in each sector. It also considers trends in retrofitting versus new installations. Technological innovations addressed include wireless monitoring systems, battery advancements (LiFePO4 and lithium-ion), and cloud-based compliance tools. The report also evaluates emerging trends such as modular emergency lighting in prefabricated construction and smart integration into building automation systems. Additionally, the analysis includes niche segments like offshore platforms and hazardous locations requiring explosion-proof solutions. This report serves as a strategic decision-making tool, enabling stakeholders to assess current market dynamics and plan targeted investments based on evolving global demand and technology-driven opportunities.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 3201.43 Million |

|

Market Revenue in 2032 |

USD 4839.18 Million |

|

CAGR (2025 - 2032) |

5.3% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

DYWIDAG Systems International, Williams Form Engineering Corporation, Con-Tech Systems Ltd., Ischebeck Titan Limited, Hayward Baker Inc., Bauer Spezialtiefbau GmbH, Nucor Skyline, Nippon Steel Corporation, Technopile Foundations, Soletanche Freyssinet |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |