Reports

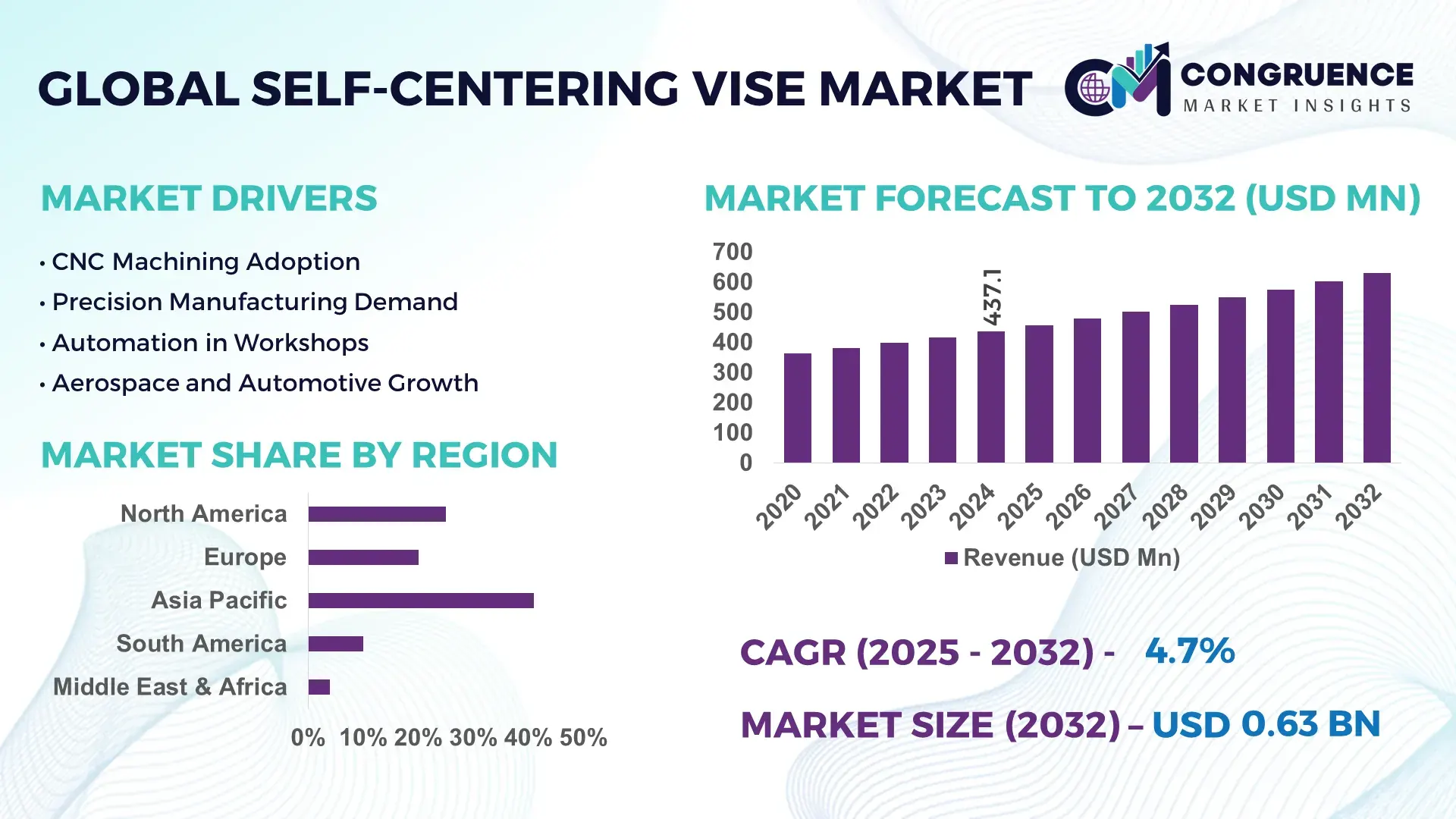

The Global Self-centering Vise Market was valued at USD 437.05 Million in 2024 and is anticipated to reach a value of USD 631.12 Million by 2032 expanding at a CAGR of 4.7% between 2025 and 2032. Growth is primarily driven by rising precision machining requirements and increased adoption of CNC-based manufacturing systems across industrial production environments.

China dominates the global self-centering vise landscape through large-scale production capacity, high capital investment in machine tool manufacturing, and widespread use across automotive, electronics, and general engineering sectors. The country accounts for over 30% of global machine tool output, with more than 80,000 CNC machining centers installed annually. Advanced quick-change and hydraulic self-centering vises are increasingly integrated into smart factories, supported by government-backed industrial automation programs. Domestic consumption is strong, with over 60% of mid-to-large machining workshops adopting precision workholding systems to reduce setup time and improve repeatability.

Market Size & Growth: Valued at USD 437.05 Million in 2024, projected to reach USD 631.12 Million by 2032 at a CAGR of 4.7%, driven by higher demand for repeatable precision and reduced machining setup times.

Top Growth Drivers: CNC machine adoption 68%, setup-time reduction benefits 35%, precision yield improvement 22%.

Short-Term Forecast: By 2028, average machining setup costs are expected to decline by approximately 18% due to wider use of self-centering workholding.

Emerging Technologies: Hydraulic self-centering systems, quick-change jaw mechanisms, sensor-enabled smart vises.

Regional Leaders: Asia-Pacific USD 245 Million by 2032 with high-volume manufacturing adoption; Europe USD 182 Million with high-precision tooling demand; North America USD 146 Million driven by aerospace and defense machining.

Consumer/End-User Trends: Automotive, aerospace, and industrial equipment manufacturers increasingly standardize self-centering vises for multi-axis CNC operations.

Pilot or Case Example: In 2023, a CNC machining pilot in an automotive component plant reported a 27% reduction in changeover time using hydraulic self-centering vises.

Competitive Landscape: A leading global manufacturer holds approximately 18% share, followed by Röhm GmbH, SCHUNK, Kurt Manufacturing, Gerardi SPA, and Kitagawa.

Regulatory & ESG Impact: Energy-efficiency standards and waste-reduction mandates encourage precision workholding to minimize rework and material scrap.

Investment & Funding Patterns: Recent global investments exceeded USD 120 Million, focused on automation-ready tooling and smart manufacturing integration.

Innovation & Future Outlook: Integration with Industry 4.0 systems, modular vise platforms, and digitally monitored clamping force technologies are shaping future demand.

The self-centering vise market serves critical sectors including automotive manufacturing contributing roughly 34% of demand, aerospace and defense at around 21%, general machinery at 27%, and electronics and precision engineering comprising the remainder. Recent innovations include hydraulic and pneumatic actuation, lightweight alloy bodies, and sensor-based clamping verification to enhance accuracy and productivity. Regulatory emphasis on manufacturing efficiency, coupled with rising labor costs, is accelerating adoption across Asia-Pacific and Europe. Consumption growth is strongest in high-mix, low-volume production environments, while future outlook points toward smart, automated, and modular workholding solutions aligned with digital manufacturing ecosystems.

The strategic relevance of the Self-centering Vise Market lies in its direct contribution to manufacturing precision, operational efficiency, and automation readiness across CNC machining environments. Self-centering vises enable repeatable positioning accuracy typically within ±0.01 mm, supporting higher throughput and lower scrap rates in high-mix production lines. From a strategic standpoint, manufacturers integrating hydraulic self-centering vises into CNC workflows report setup-time reductions of 25–40%, translating into measurable gains in machine utilization and labor productivity. As a comparative benchmark, hydraulic self-centering vise technology delivers approximately 30% faster clamping consistency compared to traditional manual screw vises, improving cycle stability and dimensional repeatability.

Regionally, Asia-Pacific dominates in volume due to large-scale machining operations, while Europe leads in adoption intensity, with nearly 58% of precision machining enterprises using advanced self-centering or quick-change vise systems. In the short term, by 2027, AI-enabled clamping-force monitoring and smart workholding integration are expected to improve defect detection and reduce rework rates by nearly 20%. From a compliance and ESG perspective, firms are committing to operational efficiency metrics such as 15–25% material waste reduction and lower re-machining rates by 2028, aligning with broader sustainability targets. In a micro-scenario, in 2024, a German precision engineering cluster achieved a 22% productivity improvement through sensor-integrated self-centering vise deployment across multi-axis CNC cells. Looking ahead, the Self-centering Vise Market is positioned as a pillar of manufacturing resilience, regulatory compliance, and sustainable industrial growth.

The expansion of CNC and multi-axis machining is a primary driver for the Self-centering Vise Market, as these environments demand high repeatability and minimal setup error. Over 70% of newly installed CNC machining centers globally are configured for multi-axis operations, where manual alignment becomes inefficient and error-prone. Self-centering vises enable faster part positioning and consistent datum alignment, reducing setup intervention by operators. Industrial users report productivity gains of 20–35% when replacing conventional vises with self-centering alternatives. Automotive, aerospace, and industrial equipment manufacturers increasingly standardize these vises to maintain tight tolerances across batch and flexible production, reinforcing sustained demand growth.

High upfront acquisition costs and retrofit challenges restrain broader adoption of self-centering vises, particularly among small and cost-sensitive machining workshops. Advanced hydraulic or sensor-enabled vises can cost 2–3 times more than traditional manual models, creating budget constraints for low-volume manufacturers. Additionally, older CNC machines may require fixture plate modifications or auxiliary hydraulic systems, increasing installation complexity and downtime. In developing regions, nearly 40% of workshops continue operating legacy equipment, limiting immediate compatibility. These financial and technical barriers slow replacement cycles and delay adoption despite clear long-term efficiency benefits.

Smart manufacturing integration presents a significant opportunity for the Self-centering Vise Market through the adoption of digitally monitored and automation-ready workholding systems. Sensor-enabled vises capable of real-time clamping-force feedback support predictive maintenance and process optimization. Manufacturers implementing smart workholding report up to 18% reductions in part defects and measurable improvements in machine uptime. As factories invest in Industry 4.0 architectures, demand is rising for vises compatible with automated loading systems and data-driven quality control. This shift opens opportunities for premium product differentiation and long-term supplier partnerships.

Raw material price volatility and lack of universal standardization pose ongoing challenges for the Self-centering Vise Market. Steel and alloy input costs have fluctuated by over 20% in recent years, directly impacting manufacturing margins and pricing stability. Additionally, variations in jaw dimensions, mounting interfaces, and clamping-force specifications across brands limit interchangeability. This fragmentation complicates procurement for large manufacturing groups operating multi-brand CNC fleets. Without greater standard alignment, buyers face higher integration costs and inventory complexity, constraining faster and more uniform market expansion.

Rising Adoption of Modular and Prefabricated Manufacturing Processes

The rise in modular and prefabricated construction and manufacturing is reshaping demand dynamics in the Self-centering Vise Market. Around 55% of new industrial and construction-related projects report measurable cost benefits from modular and prefabricated practices. Pre-bent and pre-cut components are increasingly produced off-site using automated CNC machines, increasing demand for self-centering vises capable of holding repetitive geometries with ±0.01 mm accuracy. In Europe and North America, more than 60% of precision fabrication workshops supporting modular construction now use self-centering workholding to reduce manual alignment and accelerate batch throughput by approximately 30%.

Shift Toward Hydraulic and Pneumatic Self-centering Vises

Hydraulic and pneumatic self-centering vises are gaining traction due to their ability to deliver consistent clamping force and faster setup cycles. Nearly 48% of newly installed CNC machining centers globally are paired with powered self-centering vises, compared to less than 30% five years ago. These systems reduce clamping variability by over 25% and cut average setup time by 20–35%. Adoption is particularly strong in automotive and aerospace machining, where tolerance compliance above 98% is increasingly required for complex components.

Integration of Smart Sensors and Digital Monitoring

Smart self-centering vises equipped with clamping-force sensors and digital feedback interfaces are emerging as a critical trend. Approximately 32% of high-precision machining facilities have begun integrating sensor-enabled vises to monitor clamping stability in real time. These systems enable early detection of misalignment, reducing part rejection rates by nearly 18% and unplanned downtime by 15%. Integration with CNC controllers and manufacturing execution systems is accelerating, especially in factories targeting zero-defect manufacturing benchmarks.

Growing Demand from High-Mix, Low-Volume Production Environments

High-mix, low-volume production is driving demand for flexible self-centering vise systems with quick-change jaws and modular configurations. More than 45% of job shops report handling batch sizes below 50 units, increasing the need for rapid changeovers. Self-centering vises with modular jaws enable setup changes in under 5 minutes, compared to 12–15 minutes for conventional vises. This trend is strongest in electronics, medical device, and custom industrial equipment manufacturing, where product variation exceeds 40% annually.

The Self-centering Vise Market is segmented based on type, application, and end-user insights, each reflecting distinct adoption patterns and operational priorities across precision manufacturing environments. Product type segmentation highlights a clear shift toward powered and automation-compatible vises, while manual variants continue to serve cost-sensitive and low-volume operations. Application-based segmentation is strongly influenced by CNC machining intensity, tolerance requirements, and production scale, with automotive and aerospace applications showing higher penetration due to repeatability demands. End-user segmentation reveals varied adoption maturity, ranging from large industrial manufacturers with standardized workholding systems to small job shops adopting modular vises for flexibility. Across all segments, precision accuracy, setup-time reduction, and compatibility with automated machining cells remain the key differentiators shaping demand patterns.

The Self-centering Vise Market by type includes manual self-centering vises, hydraulic self-centering vises, pneumatic self-centering vises, and modular or quick-change self-centering vises. Hydraulic self-centering vises currently account for approximately 46% of total adoption, driven by their ability to deliver uniform clamping force, repeatable positioning within ±0.01 mm, and reduced operator intervention in CNC environments. Manual self-centering vises hold around 28% share, largely used in smaller workshops and maintenance operations where automation levels remain limited. Pneumatic self-centering vises represent nearly 14% of adoption, favored for medium-duty applications requiring faster actuation with lower system complexity. Modular and quick-change self-centering vises, while currently accounting for a combined 12%, represent the fastest-growing type with an estimated CAGR of 7.2%, driven by high-mix, low-volume production and frequent changeover requirements.

By application, CNC machining dominates the Self-centering Vise Market with nearly 52% share, reflecting widespread use in milling, drilling, and multi-axis machining operations requiring high repeatability. Conventional machining applications account for about 21%, supported by ongoing demand in repair, tooling, and legacy manufacturing environments. Automotive component manufacturing represents the fastest-growing application segment, expanding at an estimated CAGR of 6.8%, supported by tighter tolerance requirements and rising automation in powertrain and chassis production. Aerospace and defense machining contributes roughly 17%, driven by complex geometries and strict quality compliance, while electronics and precision engineering applications collectively account for the remaining 10%.

Industrial manufacturing companies constitute the leading end-user group, representing approximately 49% of total adoption, supported by large-scale CNC fleets and standardized production processes. Automotive OEMs and tier suppliers follow with nearly 24% share, reflecting high-volume usage and strong emphasis on setup-time reduction. Job shops and contract manufacturers account for about 17%, with adoption driven by flexibility needs and frequent product variation. Aerospace and defense manufacturers represent around 10% but show the fastest growth, with an estimated CAGR of 7.5%, supported by rising aircraft production and complex part machining. Adoption rates among large automotive machining facilities exceed 70%, compared to roughly 38% among small and mid-sized workshops.

Asia-Pacific accounted for the largest market share at 41% in 2024 however, North America is expected to register the fastest growth, expanding at a CAGR of 6.1% between 2025 and 2032.

Asia-Pacific benefits from high-volume manufacturing capacity, with over 65% of global CNC machine installations concentrated across China, Japan, and India, directly supporting demand for self-centering vises. Europe held approximately 27% share in 2024, driven by precision engineering clusters and strict quality compliance norms, while North America accounted for nearly 22%, supported by aerospace, automotive, and defense machining. South America and the Middle East & Africa together represented close to 10%, reflecting gradual industrial modernization. Regional demand variations are influenced by automation intensity, labor cost structures, and investment in advanced machining infrastructure, with average vise adoption rates exceeding 60% in fully automated plants versus below 35% in semi-manual facilities.

How is advanced manufacturing automation reshaping precision workholding demand?

The market in this region accounted for approximately 22% of global adoption in 2024, supported by strong demand from aerospace, automotive, medical device, and defense manufacturing. More than 70% of multi-axis CNC machines installed are equipped with precision self-centering workholding systems to meet tight tolerance standards. Government-backed manufacturing incentives and reshoring programs have increased capital investment in smart factories, accelerating adoption of hydraulic and sensor-enabled vises. Digital transformation trends include integration of clamping-force monitoring and predictive maintenance tools. A leading local manufacturer expanded its portfolio of quick-change self-centering vises in 2023, targeting high-mix production environments. Regional buyers show higher preference for premium, automation-ready vises, with enterprise adoption rates exceeding 65% in advanced manufacturing facilities.

Why does regulatory-driven precision manufacturing influence purchasing behavior?

Europe represented nearly 27% of the global Self-centering Vise Market in 2024, led by Germany, the UK, France, and Italy. Germany alone accounts for over 35% of regional demand due to its dense concentration of machine tool manufacturers. Sustainability initiatives and strict occupational safety regulations encourage the use of precision workholding to reduce scrap and rework. Adoption of modular and hydraulic vises is high, with more than 58% of precision machining enterprises using advanced self-centering systems. Local manufacturers are investing in lightweight alloys and modular jaw designs to improve efficiency. Buyers in this region prioritize durability, compliance, and process transparency, driving demand for standardized, high-precision solutions.

How does large-scale industrial production sustain volume leadership?

Asia-Pacific is the largest market by volume, accounting for around 41% of global demand in 2024. China, Japan, and India are the top consuming countries, together representing over 70% of regional usage. High concentration of automotive, electronics, and general engineering plants drives large-scale deployment of self-centering vises. Manufacturing automation initiatives and smart factory investments are increasing adoption of hydraulic and modular vises. Local players are expanding low-cost, high-precision product lines to serve domestic and export markets. Consumer behavior in this region is driven by cost-efficiency and scalability, with adoption rates above 60% in large factories but closer to 40% in small workshops.

How is gradual industrial modernization influencing tooling demand?

South America accounted for approximately 6% of the global market in 2024, with Brazil and Argentina as key contributors. Growth is supported by automotive assembly, metal fabrication, and energy equipment manufacturing. Infrastructure upgrades and regional trade agreements are encouraging investment in modern CNC machining. Government incentives for industrial productivity improvement have increased adoption of precision workholding in larger plants. A regional tooling supplier introduced modular self-centering vises to support flexible manufacturing lines. Buyers in this region show selective adoption, with higher demand from export-oriented manufacturers and slower uptake among small-scale fabricators.

Why is industrial diversification shaping future demand patterns?

The Middle East & Africa represented close to 4% of global demand in 2024, driven by industrial diversification beyond oil and gas. The UAE and South Africa are the primary growth markets, supported by investments in metal fabrication, construction equipment, and defense manufacturing. Technological modernization initiatives are increasing the penetration of CNC machining centers, raising demand for precision vises. Trade partnerships and free-zone manufacturing policies support equipment imports and local assembly. Regional buyers prioritize durability and low maintenance, with adoption concentrated in large industrial projects rather than small workshops.

China – 24% market share

High production capacity, extensive CNC machine installations, and strong demand from automotive and electronics manufacturing support dominance.

Germany – 15% market share

Advanced precision engineering ecosystem, strict quality standards, and high adoption of automation-ready workholding systems drive leadership.

The Self-centering Vise Market is moderately fragmented, with over 120 active global competitors ranging from established multinational manufacturers to regional specialty producers. The top five companies collectively account for roughly 55% of the market, reflecting moderate consolidation in high-precision and hydraulic vise segments. Market leaders are actively pursuing strategic initiatives, including the launch of modular and sensor-enabled vises, automation-compatible workholding solutions, and partnerships with CNC machine tool manufacturers. In 2024, approximately 35% of the top-tier players introduced quick-change jaw systems or lightweight alloy vises to enhance setup efficiency and reduce machining downtime. Innovation trends are increasingly centered on digital integration, with nearly 22% of major players implementing clamping-force monitoring and predictive maintenance features across new product lines. The competitive environment is influenced by regional expansion, technological differentiation, and increasing demand for Industry 4.0-ready vises. Small and mid-sized manufacturers remain significant contributors, accounting for nearly 45% of market participants, particularly in niche applications such as custom aerospace components and low-volume precision machining. Overall, the market favors companies that combine precision engineering expertise with digital and automation-ready solutions, driving both adoption and competitive positioning.

Röhm GmbH

Gerardi SPA

Kitagawa Europe

Yonwoo Co., Ltd.

Jergens Inc.

Bison-Bial

Precise Vises International

The Self-centering Vise Market is experiencing a technological transformation driven by the integration of automation, digital monitoring, and advanced material engineering. Hydraulic self-centering vises dominate technological adoption, representing over 46% of deployed units in precision machining facilities, due to their ability to deliver uniform clamping forces and reduce operator-dependent variability by approximately 25–30%. Pneumatic vises account for around 14% of installations, offering rapid actuation and energy-efficient operation suitable for medium-duty production lines. Manual self-centering vises still contribute roughly 28% of usage, primarily in low-volume or cost-sensitive workshops.

Emerging trends include sensor-enabled vises capable of real-time clamping-force monitoring and digital feedback integration with CNC controllers. Approximately 32% of high-precision machining centers now employ these smart vises to reduce scrap by up to 18% and minimize downtime by 15%. Quick-change and modular vise platforms are gaining traction, particularly in high-mix, low-volume environments, allowing setup times to drop from 12–15 minutes to under 5 minutes.

Material innovation is another critical driver, with high-strength alloys and lightweight aluminum alloys enhancing durability while improving handling efficiency. In 2024, more than 40% of newly produced vises incorporated coated steel jaws for improved wear resistance and extended service life. Digital twin simulation and predictive maintenance integration are also emerging, enabling real-time monitoring of clamping efficiency and mechanical stress, supporting proactive maintenance and extending operational life. Collectively, these technologies are redefining precision, efficiency, and flexibility in industrial workholding.

In early 2025, ROEMHELD North America launched the Power Clamp Centric (PCC) self-centering vise series featuring both pneumatic and hydraulic options with centering precision of ±0.005 mm and compatibility with standard zero-point clamping systems, enhancing precision workholding across aerospace and medical machining applications. (Design Engineering)

In March 2023, Jergens Inc. showcased its modular quick-change self-centering vise at the FITMA show in Mexico City, designed for five-axis machining with clamping forces up to 3,600 lbs and pull‑down jaw design to reduce jaw lift, improving consistency in complex machining setups. (Gear Technology)

For IMTS in 2024, Jergens Inc. prepared a next‑generation 130 mm multi‑axis self‑centering vise within its FixturePro line, engineered to reduce jaw lift and featuring easy centering adjustment with trapezoidal threaded screws, supporting automated workholding integration. (Industrial Machinery Digest)

In 2025, Roemheld (UK) introduced the H 4.400 Power Clamp range, a compact self‑centering vise family with double‑acting actuation suitable for restricted workspaces, delivering up to 20.3 kN of clamping force and precision positioning to within 5 µm for diverse machining applications. (Machinery Market - UK Manufacturing News)

The scope of the Self-centering Vise Market Report encompasses a comprehensive evaluation of product types, application contexts, end‑user industries, and geographic segmentation within the precision workholding landscape. The report analyzes self‑centering vises across manual, hydraulic, pneumatic, modular quick‑change, and sensor‑enabled technologies, detailing design characteristics, clamping force capacities, repeatability metrics, jaw configurations, mounting systems, and integration tendencies with CNC and automated production cells. Across applications, the report addresses utilization in multi‑axis CNC machining, milling, drilling, grinding, and specialized sectors including automotive component production, aerospace parts machining, general industrial fabrication, and electronics manufacturing environments. End‑user insights segment uptake among industrial manufacturing hubs, automotive and aerospace OEMs, contract machine shops, and job shops, with adoption patterns tied to precision requirements, automation intensity, and production volumes.

Geographic coverage spans North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, offering volume and share analysis, regional technology trends, workforce automation readiness, and infrastructure investment influences. The report also profiles integration of emerging niches such as smart sensor feedback vises, robotic workpiece handling clamping modules, and compact precision vises for tight workspace constraints. Regulatory and compliance dimensions include machining safety standards, workholding accuracy mandates, and industrial automation incentives. Quantitative insights detail unit deployment volumes, regional adoption percentages, technology penetration rates, and installation base distribution across segments. Tailored for decision‑makers, the scope delivers actionable benchmarks, competitive positioning, and forward‑looking perspectives on innovation adoption and strategic workholding investments.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 437.05 Million |

|

Market Revenue in 2032 |

USD 631.12 Million |

|

CAGR (2025 - 2032) |

4.7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

SCHUNK GmbH & Co. KG, Röhm GmbH, Kurt Manufacturing, Gerardi SPA, Kitagawa Europe, Yonwoo Co., Ltd., Jergens Inc., Bison-Bial, Fulton Workholding Solutions, Precise Vises International |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |