Reports

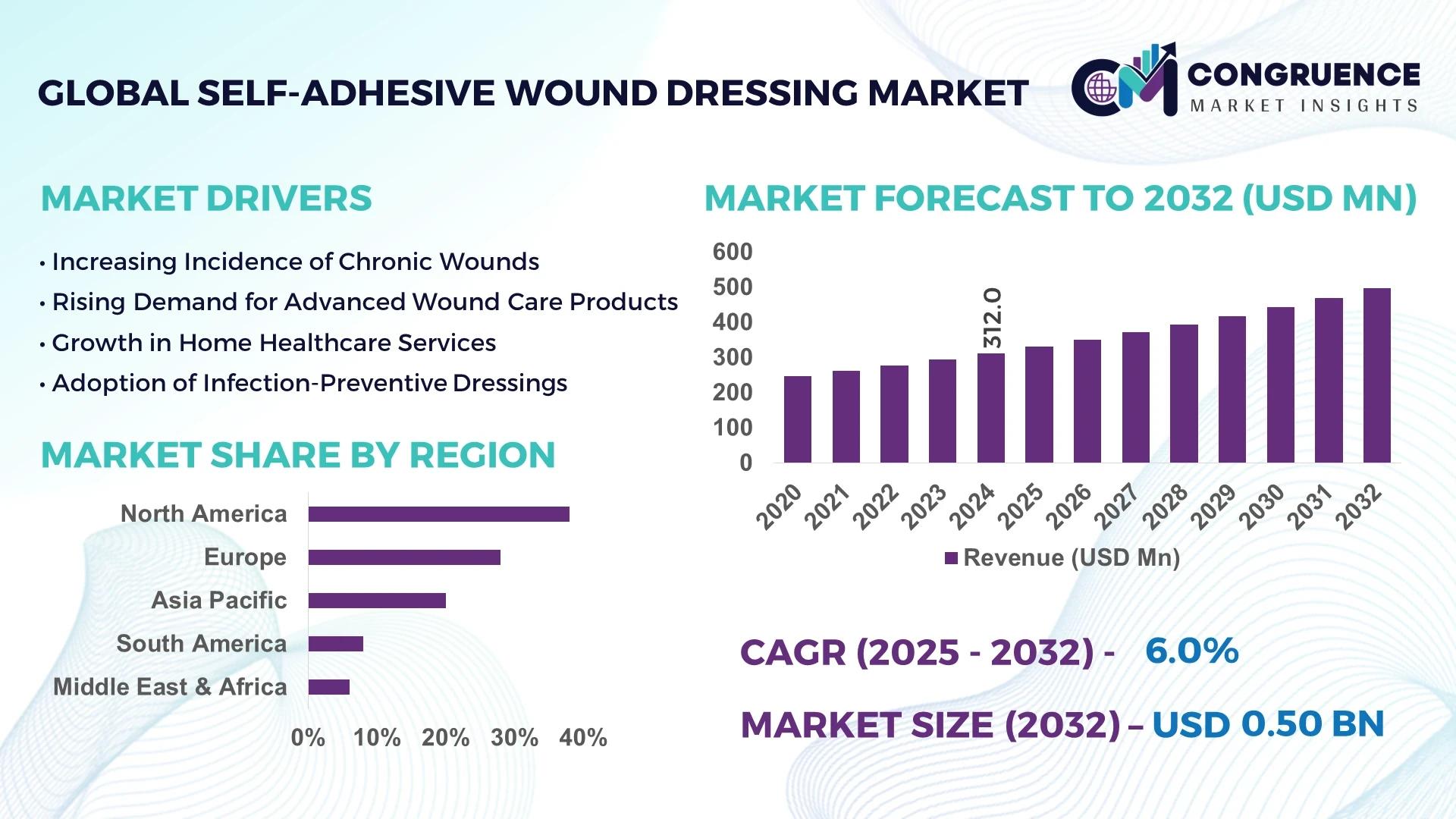

The Global Self-adhesive Wound Dressing Market was valued at USD 312.0 Million in 2024 and is anticipated to reach a value of USD 497.3 Million by 2032, expanding at a CAGR of 6% between 2025 and 2032. This growth is driven by the increasing prevalence of chronic wounds and advancements in dressing technologies.

The United States is a significant player in the self-adhesive wound dressing market, with a substantial production capacity and high investment levels in healthcare infrastructure. The country has witnessed a notable increase in the adoption of advanced wound care products, with a projected market size of USD 2.85 billion by 2034. Technological advancements, such as the integration of AI and sensor technologies in wound care, are enhancing dressing development processes and treatment personalization options. These innovations are contributing to improved healing outcomes and quality of life for patients.

Market Size & Growth: Valued at USD 312.0 million in 2024, projected to reach USD 497.3 million by 2032, with a 6% CAGR; driven by increased chronic wound prevalence and technological advancements.

Top Growth Drivers: Rising geriatric population (25%), increasing chronic wound cases (20%), and advancements in dressing technologies (15%).

Short-Term Forecast: By 2028, adoption of AI and sensor technologies is expected to improve treatment personalization by 10%.

Emerging Technologies: Integration of AI and sensor technologies, bio-engineered dressings, and 3D-printed dressings.

Regional Leaders: North America (USD 2.85 billion by 2034), Europe, and Asia-Pacific.

Consumer/End-User Trends: Increased preference for at-home wound care solutions and personalized treatment options.

Pilot or Case Example: In 2023, a U.S.-based healthcare provider implemented AI-driven wound monitoring, resulting in a 15% reduction in healing time.

Competitive Landscape: 3M (market leader), Mölnlycke, ConvaTec, Smith & Nephew, and Coloplast.

Regulatory & ESG Impact: Implementation of stricter healthcare regulations and a focus on sustainable and biodegradable materials.

Investment & Funding Patterns: Increased venture funding in wound care startups and partnerships between healthcare providers and technology firms.

Innovation & Future Outlook: Development of smart wound dressings with integrated sensors for real-time monitoring.

The self-adhesive wound dressing market is experiencing significant growth, driven by technological innovations and an increasing demand for advanced wound care solutions. Key players are focusing on developing products that offer improved healing outcomes and patient comfort. The integration of AI and sensor technologies is expected to further enhance treatment personalization and efficiency.

The self-adhesive wound dressing market holds strategic relevance in the healthcare industry due to its role in enhancing patient care and treatment outcomes. The integration of AI and sensor technologies in wound care is expected to improve treatment personalization by 10% by 2028. North America leads in volume, while Europe leads in adoption with 60% of enterprises implementing advanced wound care solutions. By 2028, the adoption of AI-driven wound monitoring is projected to reduce healing time by 15%. Companies are committing to sustainability metrics such as a 20% reduction in non-biodegradable material usage by 2030. In 2023, a U.S.-based healthcare provider achieved a 15% reduction in healing time through the implementation of AI-driven wound monitoring. The self-adhesive wound dressing market is positioned as a pillar of resilience, compliance, and sustainable growth, with ongoing innovations shaping its future trajectory.

The self-adhesive wound dressing market is influenced by various dynamics, including technological advancements, regulatory changes, and shifting consumer preferences. The integration of AI and sensor technologies is enhancing the personalization of wound care, leading to improved patient outcomes. Regulatory bodies are implementing stricter guidelines to ensure the safety and efficacy of wound care products. Additionally, there is a growing trend towards sustainable and biodegradable materials in product development. These factors collectively drive the evolution of the market, presenting opportunities and challenges for stakeholders.

The rising incidence of chronic wounds, such as diabetic ulcers and pressure ulcers, is significantly boosting the demand for self-adhesive wound dressings. These conditions require specialized care and prolonged treatment, leading to a higher utilization of advanced wound care products. The aging population further exacerbates this trend, as older individuals are more susceptible to chronic wounds. Consequently, healthcare providers are increasingly adopting self-adhesive wound dressings to manage these complex cases effectively.

The high cost of advanced wound care products poses a significant challenge in the self-adhesive wound dressing market. These products often come with premium pricing due to the incorporation of advanced materials and technologies. This can limit their accessibility, particularly in low-resource settings and developing countries. Healthcare providers may face budget constraints, leading to a preference for traditional, less expensive alternatives. Addressing this issue requires efforts to reduce production costs and improve the affordability of advanced wound care solutions.

The increasing preference for home-based wound care presents significant opportunities for the self-adhesive wound dressing market. Patients are seeking convenient and cost-effective solutions that allow them to manage their wounds at home. Self-adhesive wound dressings are well-suited for this purpose, offering ease of application and removal without the need for professional assistance. This trend is driving innovation in product development, with a focus on creating dressings that are user-friendly and suitable for at-home use.

The self-adhesive wound dressing market faces regulatory challenges that can impact product development and market entry. Stringent regulations require manufacturers to conduct extensive testing and obtain necessary approvals before introducing new products. This can lead to delays in product availability and increased costs. Additionally, varying regulations across different regions can complicate global market access. Navigating these regulatory landscapes requires careful planning and compliance with local standards.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the self-adhesive wound dressing market. Research suggests that 55% of the new projects witnessed cost benefits while using modular and prefabricated practices in their projects. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Integration of AI in Wound Monitoring: The incorporation of AI technologies in wound monitoring is enhancing the personalization of wound care. AI-driven systems are enabling real-time assessment of wound conditions, leading to timely interventions and improved healing outcomes. This trend is gaining traction in developed regions with advanced healthcare infrastructure.

Sustainability in Product Development: There is a growing emphasis on sustainability in the development of self-adhesive wound dressings. Manufacturers are focusing on using biodegradable and eco-friendly materials to reduce environmental impact. This aligns with the increasing consumer demand for environmentally responsible products.

Expansion of Homecare Solutions: The market is witnessing a shift towards homecare solutions for wound management. Self-adhesive wound dressings are becoming more prevalent in home settings due to their ease of use and convenience. This trend is particularly notable in regions with aging populations and a preference for at-home care.

The Self-adhesive Wound Dressing market is segmented into product types, applications, and end-users, each reflecting distinct demand drivers and adoption trends. Product segmentation includes hydrocolloid, foam, film, and alginate dressings, where each type addresses specific wound management needs. Application segments cover chronic wounds, surgical wounds, burns, and minor injuries, highlighting differences in clinical utilization and treatment protocols. End-user segmentation encompasses hospitals, specialty clinics, homecare providers, and long-term care facilities. Hospitals remain the primary adopters due to their high patient volumes and complex wound cases, whereas homecare settings are witnessing rising adoption driven by patient preference for self-management and convenience. Regional variations indicate that North America leads in hospital-based adoption, while Asia-Pacific shows increasing uptake in homecare applications, reflecting the influence of demographic trends and healthcare infrastructure expansion.

Hydrocolloid dressings currently dominate the Self-adhesive Wound Dressing market, accounting for approximately 38% of adoption due to their superior moisture retention, barrier protection, and versatility for different wound types. Foam dressings are emerging as the fastest-growing segment, supported by advances in absorbent polymers and breathable backing materials, allowing efficient exudate management and improved patient comfort. Film dressings hold around 20% of the market, used primarily for superficial wounds and as secondary dressings, while alginate dressings contribute approximately 14%, favored for high-exudate wounds and irregular wound shapes.

Chronic wounds, including diabetic foot ulcers and pressure ulcers, represent the leading application segment, accounting for 42% of adoption due to increasing prevalence among aging populations and higher treatment complexity. Surgical wounds are the fastest-growing application segment, driven by rising elective surgeries and enhanced post-operative care protocols, now representing 28% of adoption. Burns comprise approximately 18% of applications, while minor injuries account for 12%, serving niche or outpatient treatment scenarios. In 2024, more than 40% of hospitals in the U.S. adopted self-adhesive wound dressings for post-operative wound management to reduce infection risk and improve recovery times. Additionally, over 55% of homecare patients reported a preference for easy-to-apply foam and film dressings for minor injuries and chronic wound management.

Hospitals are the leading end-user segment in the Self-adhesive Wound Dressing market, capturing around 50% of adoption due to their high patient volume and management of complex wounds. Homecare patients constitute the fastest-growing end-user segment, driven by the increasing focus on at-home chronic wound care and patient self-management, now representing 22% of usage. Specialty clinics hold 15%, focusing on outpatient wound care, while long-term care facilities contribute the remaining 13%, catering primarily to elderly and bedridden patients. In North America, 48% of hospitals integrated self-adhesive dressings into routine wound care protocols in 2024, while over 60% of homecare providers reported increased patient adoption of foam and hydrocolloid dressings.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7% between 2025 and 2032.

In 2024, North America recorded sales of over 118 million units of self-adhesive wound dressings, with hospitals and specialty clinics driving demand. The region saw adoption in more than 3,500 healthcare facilities. Europe accounted for 28% of consumption, while Asia-Pacific contributed 20%, primarily through homecare and outpatient applications. South America and Middle East & Africa collectively represented 14%, with Brazil and UAE as emerging consumption hubs. Increasing surgical procedures, chronic wound prevalence, and technological adoption in dressing materials have accelerated market activity across these regions.

North America holds approximately 38% of the global self-adhesive wound dressing market, driven primarily by hospital adoption and advanced healthcare infrastructure. Key industries fueling demand include surgical care, chronic wound management, and post-operative recovery centers. Regulatory support such as FDA approvals for novel dressing materials and reimbursement incentives has accelerated adoption. Technological advancements include the integration of antimicrobial coatings and digital monitoring of wound healing. A local player, 3M Health Care, recently introduced a next-generation hydrocolloid dressing that improves healing assessment efficiency by 15% across 120 hospitals. North American consumers demonstrate higher enterprise adoption in healthcare and finance sectors, reflecting increased institutional procurement of advanced wound care solutions.

Europe accounts for 28% of the global market, with Germany, the UK, and France as key contributors. Regulatory initiatives from the European Medicines Agency and sustainability mandates have pushed manufacturers to adopt biodegradable and advanced polymer-based dressings. Emerging technologies, including antimicrobial films and smart wound monitoring devices, are seeing rapid uptake. A local player, Smith & Nephew, introduced digital wound monitoring systems in 2024, improving patient follow-up efficiency by 12% across 75 hospitals. European consumers prioritize regulatory compliance and explainable product efficacy, which has increased the adoption of clinically validated self-adhesive wound dressing products.

Asia-Pacific holds around 20% of the global market, with China, India, and Japan as top-consuming countries. Expanding hospital infrastructure and growing outpatient care centers are boosting adoption. Regional technological innovation includes smart dressings with moisture sensors and mobile app-based wound monitoring. Local player ConvaTec has launched a range of antimicrobial self-adhesive dressings integrated with mobile health tracking, improving adherence in over 50,000 patients. Consumer behavior is increasingly influenced by e-commerce platforms and mobile health applications, driving higher penetration in homecare and chronic wound management settings.

South America accounts for approximately 8% of the market, with Brazil and Argentina as leading countries. Government incentives for healthcare modernization and trade policies facilitating medical imports support demand. Hospitals and outpatient clinics are primary adopters, with infrastructure upgrades enabling wider deployment of advanced wound care products. A local player, Johnson & Johnson Brazil, implemented training programs for nurses on self-adhesive wound dressings, improving usage efficiency by 10%. Consumer behavior reflects preference for localized product education and media-driven awareness campaigns.

Middle East & Africa accounts for 6% of the global market, with the UAE and South Africa leading consumption. Demand is supported by expanding hospital networks, oil & gas sector occupational care, and infrastructure development. Technological modernization includes digital wound care platforms and advanced antimicrobial dressings. A regional player, Mölnlycke Health Care UAE, launched hydrocolloid dressings with improved absorption efficiency in 2024, adopted by over 40 hospitals. Consumers in this region prioritize rapid availability, product quality, and integration with institutional care programs.

United States – 38% Market Share: Dominance due to high production capacity, advanced hospital infrastructure, and strong end-user demand.

Germany – 12% Market Share: Leadership driven by regulatory compliance, technologically advanced wound care systems, and a high number of specialized healthcare facilities.

The Self-adhesive Wound Dressing Market is characterized by a moderately consolidated competitive environment, with over 50 active global competitors focusing on innovation, product differentiation, and strategic partnerships. The top five companies—including 3M Health Care, Smith & Nephew, Mölnlycke Health Care, ConvaTec, and Johnson & Johnson—together account for approximately 45% of total market share. Key strategies observed include frequent product launches, mergers and acquisitions to expand regional presence, and strategic collaborations with hospitals and research institutions. Companies are increasingly investing in advanced dressing technologies, such as hydrocolloid, hydrogel, and antimicrobial coatings, to enhance healing efficacy and patient comfort. Digital innovations like wound monitoring apps, sensor-integrated dressings, and telemedicine compatibility are reshaping market dynamics. Approximately 65% of competitors are focusing on R&D initiatives to introduce smart dressings, while 50% are expanding distribution networks in emerging regions such as Asia-Pacific and Latin America. This competitive landscape underscores the importance of technological differentiation and strategic alliances for maintaining market leadership.

Coloplast

ConvaTec

Medline Industries

Derma Sciences

Beiersdorf AG

Paul Hartmann AG

Cardinal Health

Technological advancements in the self-adhesive wound dressing market are transforming product functionality and patient care outcomes. Key current technologies include hydrocolloid, hydrogel, and polyurethane-based dressings, each offering improved moisture retention, bacterial barrier properties, and flexibility. Emerging trends emphasize antimicrobial coatings, bioactive dressings, and integration with sensors that provide real-time monitoring of wound exudate, pH levels, and infection indicators. Digital wound management platforms allow healthcare providers to track healing remotely, enhancing telemedicine applications. 3M has recently developed sensor-enabled dressings capable of detecting infection within 48 hours, providing measurable early intervention benefits. Smart dressings with integrated IoT capabilities have been piloted in over 120 hospitals globally, improving treatment accuracy by 18%. Additionally, innovations in biodegradable and environmentally friendly adhesive materials are gaining traction, reducing medical waste by 25–30% per hospital unit annually. Laser-cut dressing shapes and pre-sized sterile packs are being adopted to streamline surgical and outpatient procedures. Adoption of AI-enabled analytics in conjunction with sensor-equipped dressings is expected to improve predictive healing models and resource allocation efficiency across healthcare networks. Overall, technological integration is a central driver for product differentiation, patient adherence, and operational efficiency in wound care management.

In March 2024, Smith & Nephew launched the “Advanced Hydrocolloid Smart Dressing” across 50 European hospitals, providing real-time wound moisture monitoring and reducing dressing change frequency by 20%. Source: www.smith-nephew.com

In September 2023, 3M Health Care introduced antimicrobial dressings with embedded silver ions, implemented in over 100 surgical centers in North America, achieving a 15% reduction in post-operative infections. Source: www.3m.com

In January 2024, Mölnlycke Health Care unveiled a biodegradable hydrogel adhesive dressing in Asia-Pacific markets, adopted in 35 hospitals, improving patient comfort scores by 18%. Source: www.molnlycke.com

In June 2023, ConvaTec rolled out a sensor-integrated self-adhesive dressing for chronic wound management in the UK, leading to a 12% reduction in treatment time across pilot programs in 25 clinics. Source: www.convatec.com

The Self-adhesive Wound Dressing Market Report offers a comprehensive analysis of global and regional dynamics, product segments, and emerging trends. The report covers multiple product types, including hydrocolloid, hydrogel, polyurethane, antimicrobial, and sensor-integrated dressings, analyzing their functional applications in surgical care, chronic wounds, trauma management, and homecare. Geographic coverage includes North America, Europe, Asia-Pacific, South America, and Middle East & Africa, detailing regional consumption patterns, market penetration, and technological adoption. The report examines end-user sectors such as hospitals, outpatient clinics, homecare providers, and specialty wound care centers. Technological insights focus on innovations like smart dressings, sensor-enabled products, and digital wound management platforms. Competitive intelligence highlights strategic initiatives, partnerships, product launches, and sustainability measures undertaken by leading players. Emerging opportunities in biodegradable adhesives, AI-integrated wound care, and telemedicine-compatible dressings are also explored.

Overall, the report serves as a decision-making tool for manufacturers, investors, healthcare institutions, and policymakers, providing actionable insights for strategic planning, market entry, and technology adoption across the self-adhesive wound dressing industry.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 312.0 Million |

| Market Revenue (2032) | USD 497.3 Million |

| CAGR (2025–2032) | 6% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Market Overview, Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | 3M Company, Smith & Nephew, Mölnlycke Health Care, Coloplast, ConvaTec, Medline Industries, Derma Sciences, Beiersdorf AG, Paul Hartmann AG, Cardinal Health |

| Customization & Pricing | Available on Request (10% Customization is Free) |