Reports

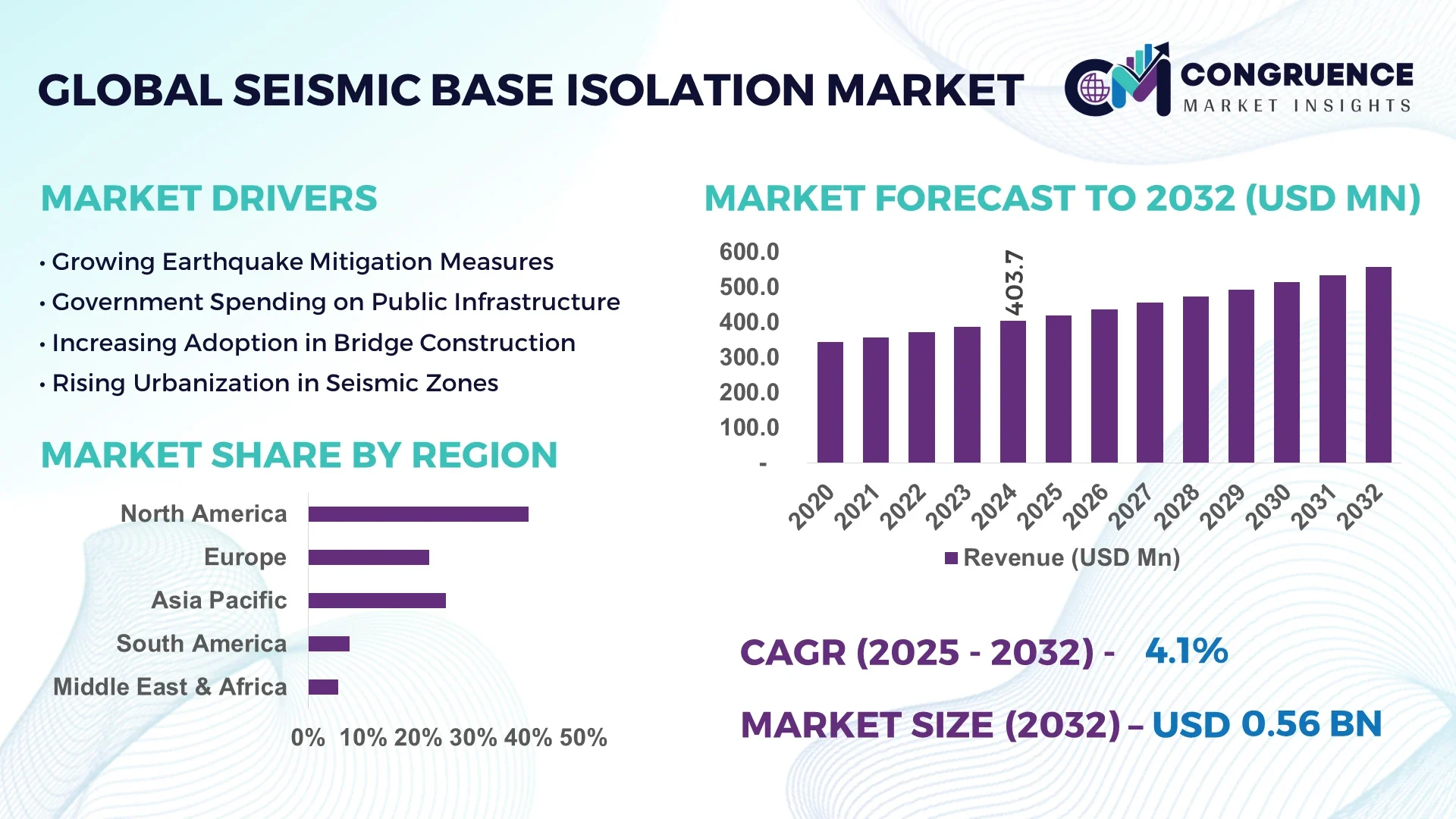

The Global Seismic Base Isolation Market was valued at USD 403.7 Million in 2024 and is anticipated to reach a value of USD 556.8 Million by 2032, expanding at a CAGR of 4.1% between 2025 and 2032.

The United States is expected to dominate the Seismic Base Isolation market, owing to its advanced infrastructure, high adoption rate of seismic technologies, and stringent building regulations that push the adoption of seismic base isolation systems.

Seismic base isolation technology helps protect buildings and infrastructure from the destructive effects of earthquakes by decoupling the building from ground motion. This technology is gaining significant traction in regions that are prone to seismic activity, such as Japan, the United States, and countries in the Pacific Ring of Fire. The market growth can also be attributed to the increasing demand for retrofitting older structures to meet modern safety standards. The technology not only enhances the resilience of infrastructure but also offers significant cost savings by minimizing damage during seismic events. As the demand for safer, more resilient buildings increases globally, the market for seismic base isolation is poised to witness robust growth.

AI is playing a crucial role in the advancement of seismic base isolation technologies, revolutionizing how engineers design, analyze, and implement seismic protection systems. One of the primary contributions of AI is in the area of predictive analysis. AI-powered algorithms can predict the behavior of seismic base isolation systems under various earthquake scenarios by analyzing vast amounts of historical seismic data. This allows engineers to optimize the design of these systems for maximum effectiveness and durability, ensuring that structures can withstand even the most severe seismic events.

Furthermore, AI is being integrated into the monitoring and maintenance of seismic base isolation systems. AI-enabled sensors can monitor the performance of isolation bearings in real time, identifying potential issues before they become critical. This real-time data collection and analysis provide building owners with proactive maintenance schedules, reducing costs and improving the longevity of the systems. Machine learning models also help in designing customized isolation solutions by analyzing structural responses to seismic forces, thereby providing tailor-made recommendations for specific building types and locations.

AI's application in seismic base isolation extends to the creation of smarter and more adaptive systems. For example, AI-driven base isolators can adjust their stiffness and damping properties in real-time during an earthquake, offering dynamic protection that adapts to changing seismic conditions. This integration of AI technologies not only enhances the performance of seismic base isolation but also contributes to the overall safety of buildings and infrastructure, making them more resilient to earthquakes and other natural disasters.

“In 2024, a collaboration between AI and seismic engineers led to the development of an AI-powered seismic base isolation system in Japan, offering real-time adjustments to base isolators during earthquakes, enhancing the safety of high-rise buildings in urban centers.”

The rising demand for earthquake-resistant infrastructure is a key driver for the growth of the Seismic Base Isolation market. As seismic activity increases in high-risk regions such as the Pacific Ring of Fire, there is growing awareness about the importance of implementing robust seismic protection systems in buildings and infrastructure. Governments are mandating stricter regulations to ensure the safety of buildings, especially in earthquake-prone areas. This has led to a surge in the adoption of seismic base isolation technologies in both new constructions and retrofitting projects. Countries like Japan, the U.S., and Chile, with high seismic activity, are at the forefront of adopting these systems, thereby driving demand in the market.

The high initial installation costs associated with seismic base isolation systems represent a restraint for market growth. Although the long-term benefits, such as reducing repair costs after an earthquake and enhancing safety, outweigh the initial investment, the upfront cost can be a barrier, particularly for smaller developers and building owners. The complexity of installation and the need for specialized materials and expertise further contribute to the overall cost. In addition, the high capital investment required to retrofit existing buildings with seismic base isolation systems can be a significant challenge, limiting the broader adoption of this technology in certain regions and sectors.

The growing opportunity in the Seismic Base Isolation market lies in the retrofitting of existing infrastructure. As older buildings and structures around the world need to comply with modern safety standards, seismic base isolation offers a cost-effective solution to enhance their earthquake resilience. This is particularly relevant in earthquake-prone areas where many structures were built before the advent of seismic protection technologies. Retrofitting projects are expected to see significant growth as governments and private entities allocate funds to upgrade infrastructure to withstand seismic events. This opportunity is especially evident in regions like California, Japan, and New Zealand, where earthquake preparedness is a priority.

One of the key challenges for the Seismic Base Isolation market is the lack of widespread awareness and education regarding the benefits and effectiveness of seismic base isolation systems. While the technology has proven to be highly effective in mitigating earthquake damage, many building owners, developers, and even some engineers remain unfamiliar with its potential applications. This knowledge gap, combined with the perceived complexity and cost of implementing such systems, may slow down adoption in regions with lower seismic activity or in developing countries where seismic risks are not well understood. Increased efforts in education and awareness campaigns are necessary to overcome this challenge and promote the widespread adoption of seismic base isolation technology.

• Rise in Modular and Prefabricated Construction: The adoption of modular and prefabricated construction is becoming a significant trend in the Seismic Base Isolation market. Modular construction allows for the prefabrication of building components, including seismic base isolation systems, off-site in controlled environments. This approach minimizes on-site labor costs, speeds up construction timelines, and ensures higher precision in the manufacturing of seismic protection systems. With the increasing need for fast-track construction projects, particularly in earthquake-prone regions, the demand for prefabricated seismic base isolation systems is expected to rise, especially in countries like Japan and the United States.

• Technological Advancements in Materials: One of the key trends in the Seismic Base Isolation market is the continuous improvement in the materials used for base isolators. High-performance bearings made from advanced materials like elastomers and lead-rubber compounds are becoming increasingly popular due to their ability to absorb seismic energy more effectively. The development of new materials with enhanced durability, flexibility, and shock-absorption capabilities is pushing the market toward more efficient and longer-lasting solutions. The trend is particularly relevant for the retrofitting of older infrastructure, where the need for reliable and cost-effective seismic solutions is critical.

• Government Regulations and Safety Standards: Stringent government regulations and safety standards aimed at reducing earthquake damage are another driving force behind the Seismic Base Isolation market. Countries prone to seismic activity are increasingly adopting building codes that require the incorporation of seismic protection technologies in new and existing structures. In regions such as California, New Zealand, and Japan, compliance with these regulations is mandatory for both new constructions and building retrofits. These regulations are not only driving demand for seismic base isolation systems but also ensuring that the technology is incorporated into a wide range of infrastructure projects.

• Rising Demand for Retrofitting Projects: The growing trend of retrofitting older buildings to meet modern safety standards is boosting the Seismic Base Isolation market. As more older structures are deemed vulnerable to seismic activity, property owners and governments are investing in retrofitting solutions to minimize damage during earthquakes. This trend is particularly significant in areas like California, where older buildings are common and the risk of earthquakes is high. Retrofitting offers a cost-effective way to enhance the resilience of these buildings without the need for complete reconstruction, leading to a growing demand for seismic base isolation solutions in the retrofitting sector.

The Seismic Base Isolation market is segmented into various types, applications, and end-user insights. In terms of type, the market is categorized into elastomeric bearings, lead-rubber bearings, and sliding bearings. Elastomeric bearings are widely used due to their cost-effectiveness and high energy absorption capacity. The market is also divided by application into residential, commercial, and industrial buildings, with the commercial segment dominating due to urbanization and the need for seismic protection in business-critical infrastructure. The end-user segments include government projects, private developers, and retrofitting projects. Retrofitting is becoming increasingly important, especially for older structures in earthquake-prone areas, and is one of the fastest-growing segments.

The Seismic Base Isolation market includes elastomeric bearings, lead-rubber bearings, and sliding bearings. Among these, elastomeric bearings dominate the market, accounting for a substantial share due to their affordability, ease of installation, and excellent seismic energy absorption capabilities. These bearings are used in a wide range of applications, from new construction to retrofitting projects. The lead-rubber bearings segment is the fastest-growing, driven by their superior performance in seismic areas, as they offer both flexibility and stability during an earthquake. These bearings are commonly used in high-risk seismic zones where enhanced protection is required. The sliding bearings segment, while growing, remains smaller in comparison, as they are more suitable for specialized applications such as bridges or structures with high lateral movement requirements.

The Seismic Base Isolation market can be segmented by application into residential, commercial, and industrial buildings. The commercial segment leads the market, accounting for the largest share. Urbanization and the increasing need for seismic safety in business-critical infrastructure like office buildings, hospitals, and government facilities are driving this growth. As governments enforce stricter building codes, commercial buildings, especially in earthquake-prone regions, are increasingly incorporating seismic base isolation systems to protect both human life and valuable infrastructure. The residential segment is also significant, especially in earthquake-sensitive areas, with homeowners opting for base isolation systems to ensure the safety of their families. Industrial applications are seeing growth due to the need to protect large industrial assets, such as manufacturing plants and warehouses, which are susceptible to earthquake damage.

In terms of end-users, the Seismic Base Isolation market is divided into government projects, private developers, and retrofitting projects. The retrofitting segment is the fastest-growing, as many older buildings, particularly in earthquake-prone regions, require seismic upgrades. Retrofitting is a cost-effective way to make existing infrastructure safer without the need for complete reconstruction. Government projects also account for a significant portion of the market, as public infrastructure like bridges, schools, and hospitals are increasingly required to meet strict seismic safety regulations. Additionally, private developers are contributing to the market's growth, particularly for commercial and residential buildings in high-risk seismic areas. Developers are investing in seismic base isolation systems to enhance the resilience of their properties and comply with local building regulations.

North America accounted for the largest market share at 40% in 2024; however, the Asia-Pacific region is expected to register the fastest growth, expanding at a CAGR of 6.5% between 2025 and 2032.

North America and Europe are the current leaders in the Seismic Base Isolation market, driven by stringent regulations and high demand for earthquake-resistant infrastructure. Asia-Pacific, especially countries like Japan and India, is expected to witness robust growth due to rising construction activities and the increasing focus on disaster prevention. The Middle East and Africa are also emerging markets, driven by infrastructure development and urbanization in earthquake-prone regions.

Leading the Way in Seismic Safety Innovations

North America continues to dominate the Seismic Base Isolation market, accounting for a significant share in 2024. The growth in the region is primarily driven by the demand for earthquake-resistant infrastructure due to the presence of earthquake-prone areas like California and Alaska. Furthermore, increased government initiatives, building regulations, and the need for retrofitting older structures are contributing to the demand. High investments in commercial and residential construction, particularly in urban centers, further enhance the market's growth. Leading countries like the United States and Canada are investing heavily in seismic safety technology, resulting in a stable and growing market for seismic base isolation.

Strengthening Infrastructure with Advanced Seismic Protection

Europe is a key player in the Seismic Base Isolation market, driven by stringent building codes and high construction standards. Countries like Italy, Greece, and Turkey, which are situated in seismically active regions, are major contributors to the market growth. The increasing number of retrofitting projects in older infrastructure, along with new commercial and residential projects, is fueling the demand for seismic base isolation systems. Additionally, Europe’s emphasis on sustainability and disaster-resilient construction has resulted in steady growth for base isolation technologies. As urbanization continues in many European countries, the demand for safe, earthquake-resistant buildings remains high, driving market expansion.

Rapid Adoption of Seismic Base Isolation in Earthquake-Prone Areas

Asia-Pacific is expected to witness the fastest growth in the Seismic Base Isolation market, with countries such as Japan, China, and India at the forefront. Japan, being highly earthquake-prone, has a long-standing history of implementing advanced seismic technologies, including base isolation systems. The rising construction activities in developing countries like India and China, coupled with increasing awareness about earthquake risk mitigation, are significantly driving the demand for seismic base isolation. Moreover, the adoption of international standards and regulations for seismic safety is propelling market growth in the region. As urban areas continue to expand, particularly in earthquake-prone zones, the demand for such technologies is expected to rise substantially.

Emerging Market for Earthquake-Resilient Technologies

South America is witnessing a gradual increase in the adoption of seismic base isolation technologies, particularly in earthquake-prone areas like Chile and Peru. The region’s rapid urbanization, coupled with a growing awareness of seismic risks, is driving the demand for seismic base isolation systems. Governments in countries like Brazil and Argentina are implementing stricter building codes, contributing to the market growth. Moreover, the increase in large-scale construction projects and the need to protect infrastructure, including residential, commercial, and public buildings, is propelling market demand. South America's relatively underdeveloped seismic safety market is expected to expand as construction activities rise and new projects demand enhanced safety measures.

Boosting Seismic Resilience in Growing Urban Centers

The Middle East and Africa are emerging markets for Seismic Base Isolation, driven by rapid infrastructure development and urbanization in seismic zones such as Turkey, Iran, and parts of the UAE. The growing number of high-rise buildings, along with the increasing focus on earthquake-resistant technologies, is contributing to the adoption of seismic base isolation systems. The region’s focus on developing safe infrastructure amid frequent seismic activities has led to the implementation of seismic isolation technologies. Countries in the Middle East, particularly those in regions prone to earthquakes, are increasingly investing in seismic retrofitting and new construction projects, thereby driving the market for seismic base isolation technologies.

United States (28%): The U.S. leads the market, driven by rigorous seismic safety standards and substantial infrastructure investments in earthquake-prone areas such as California.

Japan (23%): Japan holds a significant share, owing to its advanced seismic isolation technologies and proactive approach to disaster prevention in earthquake-prone regions.

The Seismic Base Isolation market is characterized by a competitive landscape with several prominent players innovating to maintain leadership. Key players are focusing on advanced research and development to improve product offerings, with an emphasis on high-performance materials and better cost-effectiveness for large-scale infrastructure projects. Leading players in the market are continuously expanding their product portfolios to cater to the increasing demand for seismic resilience across both new constructions and retrofitting of existing structures. Strategic partnerships and collaborations are common in the market to enhance technology development and expand geographic presence, particularly in earthquake-prone regions. Companies are also adopting mergers and acquisitions as a growth strategy to consolidate their market positions. As demand rises in the Asia-Pacific, North America, and European regions, the competition intensifies, with companies vying to provide solutions that comply with strict building regulations while offering superior earthquake protection.

Bridgesource Inc.

Freyssinet Ltd.

MTS Systems Corporation

Rheinmetall AG

Taylor Devices, Inc.

Entek Corporation

Earthquake Protection Systems, Inc.

Building Technology Engineers (BTE)

Kawasaki Heavy Industries, Ltd.

The Seismic Base Isolation market has witnessed significant technological advancements aimed at improving the resilience of structures during seismic events. One of the most notable innovations is the development of high-damping rubber bearings, which are designed to absorb the seismic energy and reduce the impact on buildings during an earthquake. These bearings use a combination of rubber and steel to create a flexible yet strong base, allowing for both movement and energy dissipation, which is critical in minimizing the damage to infrastructure.

In addition, lead-rubber bearings are gaining popularity due to their superior ability to absorb energy. These bearings combine lead and rubber, with the lead core acting as a damping agent to dissipate the energy from ground motion. This combination ensures that buildings can move independently of seismic forces, providing enhanced protection against earthquakes.

Another technological development includes smart monitoring systems integrated with seismic base isolation. These systems utilize sensors and IoT (Internet of Things) technology to track the movement and condition of buildings in real-time. By collecting data on ground motion and structural health, these systems enable predictive maintenance and proactive risk management, which can help mitigate potential damage and improve building safety during future seismic events.

Advancements in simulation software have also played a crucial role in optimizing the design and effectiveness of seismic isolation systems. High-fidelity computational models allow engineers to simulate various seismic scenarios and assess the behavior of structures under different conditions, leading to more accurate and effective base isolation designs. These technological innovations are revolutionizing the Seismic Base Isolation market, making buildings more resilient and safer in earthquake-prone regions.

In June 2024, Hitachi Metals Techno expanded its production facility to meet the rising demand for seismic dampers in earthquake-prone regions. This expansion aims to enhance the company's capacity to supply high-performance seismic isolation solutions for critical infrastructure projects.

In May 2024, Mitsubishi partnered with a government-funded earthquake resilience program in Japan, supplying advanced hybrid base isolation solutions for new infrastructure projects. This collaboration underscores Mitsubishi's commitment to enhancing seismic safety in earthquake-prone areas.

In March 2024, IHI Corporation introduced a next-generation sliding isolation system, improving structural safety for high-rise buildings in urban centers. This innovation aims to provide enhanced protection against seismic events, particularly in densely populated areas.

In February 2024, LAPP introduced the ETHERLINE® FD bioP Cat.5e, its first bio-based Ethernet cable produced in series. This sustainable variant features a bio-based outer sheath composed of 43% renewable raw materials, reducing the carbon footprint by 24% compared to traditional fossil-based TPU sheaths.

The Seismic Base Isolation Market Report provides a detailed overview of the technologies and market dynamics shaping the seismic isolation industry. This report covers the various types of base isolation systems, including elastomeric bearings, lead-rubber bearings, and sliding isolation systems, all of which are designed to reduce the impact of seismic forces on structures. The market is driven by the increasing demand for earthquake-resistant buildings and infrastructure, especially in regions that are highly susceptible to seismic activities such as Japan, the United States, and parts of Europe. The report also explores how innovations in materials, such as advanced composites and sustainable products, are enhancing the performance and longevity of seismic isolation systems.

Moreover, the report analyzes key applications of seismic base isolation, including residential buildings, commercial infrastructure, bridges, and other critical facilities. It also identifies the major end-users in the market, such as construction companies, government agencies, and engineering firms that are driving demand for these technologies. The scope extends to various geographic regions, examining the adoption of seismic base isolation technologies in North America, Europe, Asia-Pacific, and other emerging markets. It highlights the role of regulatory frameworks and standards in promoting the use of base isolation systems to protect human life and property from the devastating effects of earthquakes. This comprehensive market report serves as a valuable resource for stakeholders seeking to understand the current state and future potential of the seismic base isolation market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 403.7 Million |

|

Market Revenue in 2032 |

USD 556.8 Million |

|

CAGR (2025 - 2032) |

4.1% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Bridgesource Inc., Freyssinet Ltd., MTS Systems Corporation, Rheinmetall AG, Taylor Devices, Inc., Entek Corporation, Earthquake Protection Systems, Inc., Building Technology Engineers (BTE), Kawasaki Heavy Industries, Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |