Reports

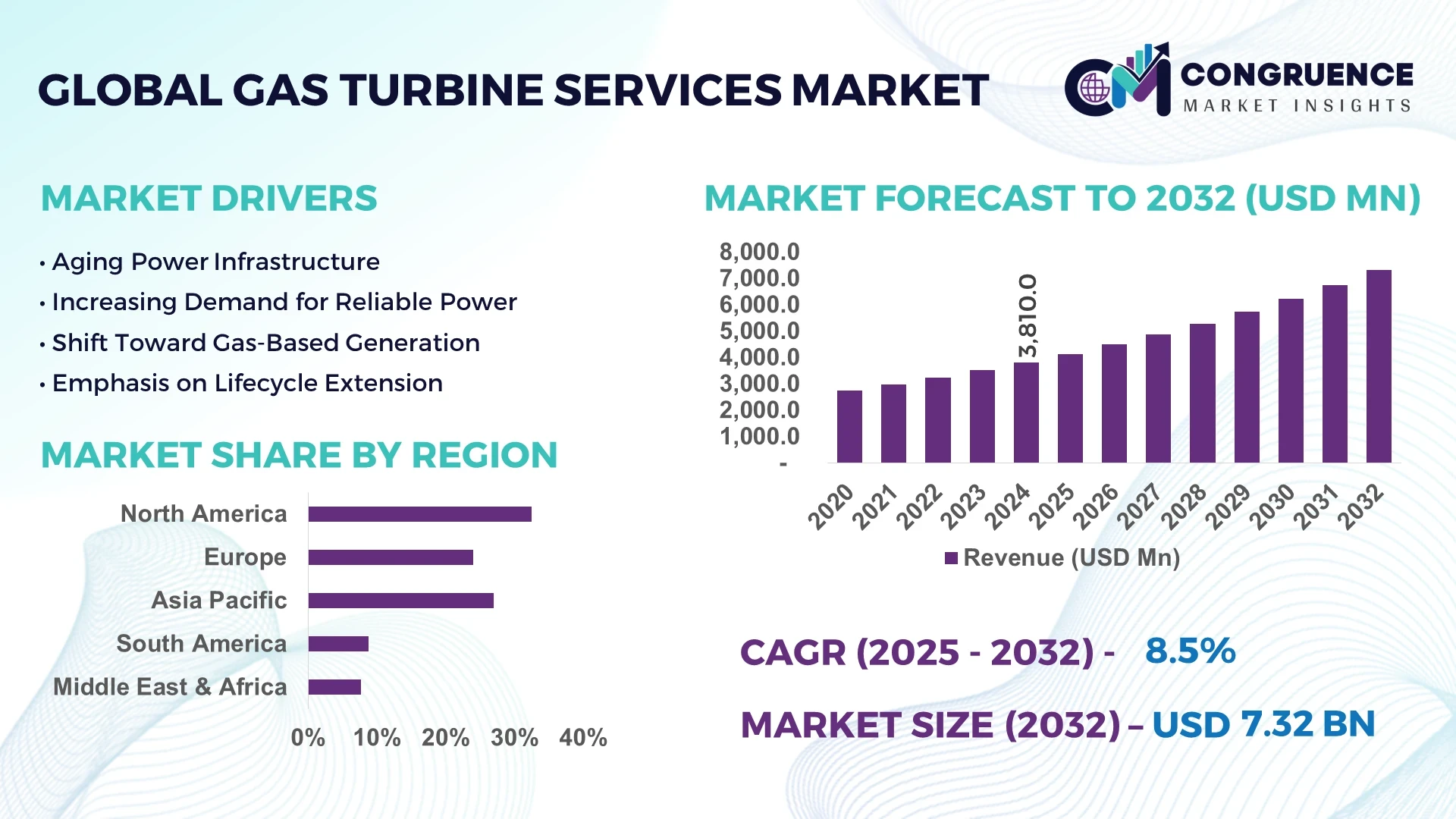

The Global Gas Turbine Services Market was valued at USD 3,810.0 Million in 2024 and is anticipated to reach a value of USD 7,317.5 Million by 2032 expanding at a CAGR of 8.5% between 2025 and 2032.

The United States remains the largest national market, hosting over 250 active service facilities and investing more than USD 1 billion annually in refurbishment and digital diagnostics upgrades. Leading regional utilities and industrial users deploy advanced aero-derivative maintenance practices and collaborate with OEMs on hydrogen-capable retrofits and remote inspection technology.

The Gas Turbine Services Market supports critical sectors including power generation, oil & gas, aviation, and marine propulsion. It increasingly utilizes digital twin simulations and AI-enhanced predictive maintenance to drive asset availability and reduce unplanned outages. Environmental regulations like NOₓ emissions limits and grid reliability standards are prompting upgrades such as dry low‑NOₓ (DLN) burner tuning and combustion inspection services. In emerging economies, infrastructure expansions demand modular maintenance contracts, while developed regions seek lifecycle extension of aging heavy-duty fleets. Product innovations include ultra-lightweight blade coatings, rapid-swap bearing modules, and integrated diagnostic sensors embedded within combustor hardware. Over the forecast period, service models are shifting to performance-based contracts and OEM independent service providers (ISP) gaining traction in aftermarket segments. Overall, the outlook indicates increasing automation, emissions compliance service integration, and diversification into hydrogen and biogas readiness.

AI is revolutionizing the Gas Turbine Services Market by enhancing operational performance, reducing maintenance cycles, and enabling condition-based service regimes. AI-driven analytics platforms continuously monitor turbine data—temperature, vibration, combustion dynamics—to predict potential failures up to 500 operating hours in advance. This predictive capacity allows operators to schedule maintenance windows strategically, reducing forced outage costs by approximately 18%.

Automated visual inspection systems powered by computer vision can detect blade erosion, tip wear, and coating degradation at a precision level under 20 microns, replacing manual inspections. These systems have improved first-pass repair success by more than 25%. Meanwhile, AI-powered thermographic analysis identifies combustion irregularities and hot-spots before they affect efficiency, enabling on-the-fly burner tuning adjustments with up to a 7% improvement in heat-rate consistency.

Supply chain and logistics also benefit. AI-based service-part demand forecasting reduces spare inventory levels by 15% while ensuring critical components remain available within 48-hour lead time. Moreover, asymmetric ML-driven scheduling models optimize field service crews across sites, achieving a 12% reduction in travel time and a 10% increase in service site coverage efficiency.

Through enterprise integration, AI tools consolidate performance insights across dispersed fleets, enabling benchmarking and lifecycle analysis. This allows service providers and operators within the Gas Turbine Services Market to identify underperforming assets and prioritize retrofits or digital upgrades. As a result, AI is shifting the market toward data-enriched service offerings, enhancing uptime, predictive diagnostics, and strategic asset investment decisions.

“In 2024, Siemens Energy deployed an AI-based burner acoustics system that detected combustion instability 200 cycles ahead of traditional monitors, reducing step-out events by 40% across a 15 GW utility fleet.”

The Gas Turbine Services Market dynamics are shaped by fleet aging, regulated emissions requirements, digital transformation, and fuel diversification. Heavy-duty turbines are reaching mid-life and require increased overhaul frequency, while aero-derivative models face growing demand in remote and fast-response settings. Regulatory frameworks for NOₓ, CO₂ emissions, and grid reliability targets are pushing OEMs and service providers to update turbines with DLN systems, hydrogen blend capabilities, and advanced coatings. Digitalization, remote diagnostics, and service-as-a-solution models are gaining market traction. Meanwhile, oil & gas infrastructure retrofits and offshore platform modernization create new service pathways. Efficiency demands are prompting cyclical maintenance and lifecycle extension projects across regions, supporting a stable demand for both scheduled and unplanned servicing programs.

Power operators are extending the operational life of aging turbines through scheduled mid-life inspections and hot-section renovations. In North America, over 60% of heavy-duty units have undergone at least one major inspection cycle in 2024. These structured overhaul initiatives stabilize asset performance, increase thermal efficiency by an average of 3%, and delay capital replacement—supporting sustained service demand across utility and industrial users.

Global supply chain bottlenecks—particularly for precision components such as turbine blades and DLN modules—have extended delivery lead times by up to 24 weeks in 2024. These delays reduce scheduling flexibility, increase downtime, and strain service agreements. Additionally, shifts to alternative fuel blends require new spare calibration parts, which are not yet widely stocked, further limiting rapid turnaround capabilities.

Operators are retrofitting existing turbines to run on hydrogen blends or dedicated low-carbon fuels. Pilot conversions completed in 2024 showed hydrogen blends up to 30% by volume without capacity loss. This trend opens aftermarket opportunities for combustion system tuning, material upgrades, and compliance documentation services—especially in regions with hydrogen infrastructure development plans.

The integration of advanced diagnostic systems, AI interfaces, and hybrid fuel technologies necessitates higher technician skillsets. In 2024, the industry reported a 22% increase in specialized training hours required per service job. This labor upskilling increases service company margins and raises the bar for workforce readiness, limiting expansion of independent service providers in certain regions.

Expansion of Performance-Based Service Contracts: Service providers are shifting from hourly-rate maintenance to performance-based agreements where compensation is tied to turbine output and availability. Stateside utilities report that 45% of new service contracts in 2024 include uptime or heat-rate guarantees, emphasizing long-term asset reliability over transactional visits.

Digital Twin Deployment Across Fleet Assets: Operators are adopting digital twins for remote monitoring and simulation-based maintenance planning. As of mid-2025, over 120 GW of installed capacity is monitored via twin platforms, enabling virtual stress testing and failure scenario emulation without site disruption. This supports proactive scheduling and retrofit planning.

Emergence of Mobile Rapid-Response Units: Aero-derivative turbine operators in offshore and tight-turnaround sectors deployed 28 mobile rapid-response service units in 2024. These configurations deliver on-site component replacement or diagnostic support within 48 hours, lowering unplanned downtime and enabling modular contract models.

Surge in Low-Emission Combustor Upgrades: Retrofitting turbines with DLN combustion tuning and catalytic systems has become a priority in 2024, driven by stricter environmental regulations. An estimated 300+ units across Europe, North America, and Asia underwent NOₓ reduction upgrades, reducing emissions by over 85% and extending service contract value.

The Gas Turbine Services Market is segmented based on type, application, and end-user, reflecting the industry’s broad and dynamic ecosystem. Each segment exhibits distinct operational demands and technological adoption rates. In terms of type, the market is segmented into heavy-duty, aero-derivative, and industrial turbines—each catering to specific performance and fuel versatility requirements. Applications are primarily concentrated in power generation, oil & gas, and marine propulsion, each with unique maintenance and operational priorities. End-user segments include utilities, independent power producers (IPPs), and industrial operators such as refineries, manufacturing plants, and offshore platforms. Technological shifts, environmental mandates, and regional infrastructure trends heavily influence these segments. Understanding these subdivisions helps stakeholders identify growth potential, tailor service models, and develop equipment life-cycle strategies with precision.

The Gas Turbine Services Market is dominated by heavy-duty turbines, which are widely used in utility-scale power generation and large industrial applications. Their robust construction and high power output requirements make them essential in national grids and energy-intensive industries. In 2024, heavy-duty turbines accounted for the largest share of total serviced units, particularly in countries with aging power infrastructure undergoing scheduled overhauls and retrofits.

Aero-derivative turbines represent the fastest-growing type, driven by their compact size, fuel flexibility, and rapid deployment capabilities. They are increasingly utilized in offshore platforms, remote installations, and peaker plants requiring fast response. Technological improvements such as modular engine cores and lightweight composite components are making maintenance faster and more cost-efficient, contributing to their rising demand.

Industrial turbines, typically smaller and used in localized cogeneration or backup systems, hold a niche but stable share. While their overall contribution is lower, they benefit from decentralization trends and growing demand in emerging manufacturing hubs.

Power generation is the most dominant application within the Gas Turbine Services Market, driven by the global shift toward cleaner combustion, system upgrades, and enhanced reliability requirements. Base-load and peaking power plants rely heavily on gas turbines, and as aging fleets undergo modernization, the demand for major overhauls and emissions-compliant upgrades continues to rise.

The oil & gas segment is the fastest-growing application area, fueled by upstream and midstream infrastructure development and growing offshore exploration activity. Turbines used for gas compression, power generation on platforms, and refining operations require specialized maintenance under harsh environmental conditions. The transition to energy-efficient processes and reduced flaring practices also increases reliance on well-maintained turbines.

Marine propulsion and auxiliary systems represent a smaller yet important application, particularly in naval and LNG shipping sectors. Though the volume is modest, service requirements are stringent, with rapid-turnaround and high-availability demands dictating service frameworks in this niche segment.

Utility companies are the leading end-users in the Gas Turbine Services Market, accounting for a majority of service contracts and scheduled maintenance events. Their widespread deployment of heavy-duty turbines for base-load electricity generation creates sustained demand for lifecycle management, part replacements, and performance optimization services. Utilities are also investing heavily in emissions control retrofits and hybrid system integration, further elevating service requirements.

Independent Power Producers (IPPs) are the fastest-growing end-user group, particularly in emerging markets and deregulated electricity sectors. Their focus on high-efficiency turbine operations, uptime optimization, and flexible output capabilities aligns well with service-based performance contracts and predictive maintenance technologies. The need to maintain competitiveness in capacity markets drives their investment in advanced service models.

Industrial end-users, including refineries, manufacturing hubs, and offshore platforms, contribute significantly due to continuous operations and stringent reliability demands. Though not as dominant as utilities, their emphasis on custom service schedules, remote diagnostics, and OEM-independent maintenance solutions creates valuable market opportunities.

North America accounted for the largest market share at 32.5% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.6% between 2025 and 2032.

The North American market continues to dominate due to its mature power generation infrastructure, extensive deployment of heavy-duty gas turbines, and consistent investment in turbine lifecycle management. In contrast, Asia-Pacific’s surge is propelled by rapid industrialization, expanding electricity demand, and a robust pipeline of combined cycle power plant projects. Each region exhibits distinct characteristics shaped by regulatory environments, industrial maturity, and technological readiness. While Europe emphasizes sustainability and turbine upgrades, South America and the Middle East are investing in modernizing legacy infrastructure. Regional energy diversification strategies and clean fuel adoption further influence service requirements, creating tailored opportunities for OEMs and independent service providers. Increasing emphasis on digitization and AI-based monitoring also enhances region-specific service frameworks.

North America held a dominant 32.5% share in the Gas Turbine Services Market in 2024, driven primarily by the widespread use of large-scale gas turbines in power generation and industrial sectors. The U.S. and Canada are leading contributors, with demand spurred by aging infrastructure and a strong focus on reliability and emissions reduction. Key industries include utilities, oil & gas, and aviation, all of which depend heavily on high-performance turbines. Regulatory emphasis on energy efficiency and air quality has encouraged frequent upgrades and maintenance programs. The region is witnessing significant adoption of digital twin technologies and predictive maintenance platforms to reduce downtime and extend asset life. Government support for clean energy and decarbonization pathways further enhances demand for advanced turbine servicing across both private and public sectors.

Europe accounted for approximately 25.4% of the global Gas Turbine Services Market in 2024. Leading markets such as Germany, the UK, and France are spearheading demand through modernization initiatives and strong decarbonization targets. The region's focus on renewable integration and flexible gas turbine operations supports service needs for hybrid and fast-ramping turbines. Regulatory bodies such as the European Environment Agency (EEA) are promoting stricter emission norms, pushing operators to invest in cleaner and more efficient turbine operations. Additionally, European operators are increasingly adopting remote diagnostics, performance optimization software, and advanced analytics to streamline O&M operations. Investment in hydrogen-ready turbines is another growing area, enhancing the long-term service market as gas-fired plants transition to low-carbon fuels.

Asia-Pacific ranked as the fastest-growing region in the Gas Turbine Services Market in 2024, with high volume consumption led by China, India, and Japan. The region's surge is attributed to aggressive infrastructure expansion, growing electricity demand, and robust investments in combined cycle gas turbine (CCGT) projects. China continues to prioritize gas-fired generation as a cleaner alternative to coal, while India is ramping up turbine capacity to meet rising industrial output and urbanization demands. Japan, with its technologically advanced grid systems, is emphasizing turbine efficiency and long-term performance contracts. The region is also becoming a hub for AI-integrated monitoring tools and condition-based service models, particularly in countries investing in smart grid technologies and digital industrial ecosystems. Asia-Pacific’s blend of demand scale and tech-forward service adoption positions it as a lucrative frontier for global service providers.

South America’s Gas Turbine Services Market is gaining traction, especially in Brazil and Argentina, which are investing in power infrastructure upgrades and energy diversification. Brazil is the region’s largest market, leveraging gas turbines to complement hydroelectric capacity during dry seasons. The region accounted for roughly 6.8% of global service volume in 2024. Infrastructure renewal projects and increasing reliance on natural gas over diesel for peaking power plants are creating service demand for performance enhancement and emissions compliance. Additionally, several countries are offering import duty waivers, tax incentives, and grid modernization grants to attract investment in turbine services. With operational focus shifting toward decentralized and mobile generation, the need for flexible maintenance strategies is also increasing.

The Middle East & Africa region is marked by rising service demand, particularly in UAE, Saudi Arabia, and South Africa, driven by strong activity in the oil & gas, construction, and power generation sectors. The region holds approximately 9.4% of the global market share. Many nations are undergoing technological modernization of existing plants, integrating remote monitoring, digital twins, and predictive diagnostics to reduce unplanned outages. Regional governments are also forming bilateral trade partnerships and localizing service operations to reduce dependence on foreign OEMs. With extreme environmental conditions and high operational loads, the focus on advanced coatings, component durability, and efficient cooling technologies is intensifying. Continued economic diversification in the Gulf and electrification efforts in Sub-Saharan Africa further support the long-term expansion of turbine service requirements.

United States – 28.3% Market Share

High turbine fleet density and extensive usage in power generation and oil & gas sectors contribute to its leadership.

China – 15.7% Market Share

Rapid expansion of gas-fired plants and increasing industrial turbine deployment fuel strong demand for services.

The Gas Turbine Services Market exhibits a moderately consolidated competitive environment, with over 30 active global and regional players consistently vying for market share. Major companies maintain a strong presence through long-term service agreements (LTSAs), robust aftermarket capabilities, and vertically integrated solutions. Leading participants compete based on technological innovation, service reliability, and lifecycle cost optimization. Competitive intensity has risen due to the emergence of third-party service providers and independent service companies (ISPs) offering cost-effective alternatives to OEM services.

Strategic initiatives such as cross-border partnerships, acquisitions, and service expansion into emerging markets are common, particularly in Asia-Pacific and the Middle East. Companies are heavily investing in digital transformation, focusing on AI-driven diagnostics, predictive analytics, and remote monitoring platforms. Recent trends also indicate a rising emphasis on environmental sustainability, where firms are retrofitting turbines to align with low-emission and hydrogen-ready standards. Innovation in material science and component durability is further intensifying R&D collaboration across the sector. Overall, the market is characterized by technical expertise, innovation race, and a growing preference for customized service packages.

General Electric Company

Siemens Energy AG

Mitsubishi Power, Ltd.

Ansaldo Energia S.p.A.

MAN Energy Solutions SE

Solar Turbines Incorporated

EthosEnergy Group Limited

MTU Aero Engines AG

Kawasaki Heavy Industries, Ltd.

Doosan Enerbility Co., Ltd.

The Gas Turbine Services Market is witnessing rapid technological advancement, driven by the need for enhanced operational efficiency, predictive maintenance, and reduced environmental impact. One of the most prominent technologies reshaping the sector is digital twin technology, which enables real-time performance modeling, failure prediction, and optimization of turbine components. These tools facilitate data-driven decision-making, reducing downtime and improving asset reliability.

Remote diagnostics and AI-powered predictive maintenance are increasingly adopted to monitor vibration, temperature, and fuel flow in real time. These technologies help detect anomalies early and schedule maintenance activities more efficiently. Another area gaining momentum is additive manufacturing (3D printing), which allows the quick and cost-effective production of spare parts, especially in remote or high-demand service scenarios.

Advanced coatings and thermal barrier technologies are also enhancing component longevity in high-temperature operations. Furthermore, innovations supporting hydrogen-fueled turbine retrofits are transforming older gas turbines into cleaner energy assets. Service providers are aligning offerings with the shift toward low-carbon fuels, with solutions optimized for mixed-fuel operations and emissions monitoring systems. These technology trends not only reduce lifecycle costs but also align with global decarbonization goals, ensuring long-term relevance and competitiveness for turbine service providers.

• In February 2024, Mitsubishi Power signed a long-term service agreement with a major utility in Thailand to support 12 gas turbines, integrating AI-based performance diagnostics for optimized operational reliability.

• In April 2024, Siemens Energy launched a new remote service center in Dubai, enhancing its ability to deliver real-time diagnostics and support across the Middle East and Africa gas turbine fleet.

• In September 2023, GE Vernova unveiled a new upgrade package for its 9HA turbines, incorporating advanced cooling and coating technologies to extend maintenance intervals by up to 25%.

• In November 2023, Ansaldo Energia secured a strategic partnership in India to provide localized maintenance services and expand its footprint in the high-growth Asia-Pacific turbine servicing market.

The Gas Turbine Services Market Report offers a comprehensive analysis of the industry, covering a wide spectrum of market segments, geographical regions, and end-use applications. The report includes a detailed breakdown by type (heavy-duty, industrial, and aeroderivative turbines), application (power generation, oil & gas, aviation, and marine), and end-users (utilities, industrial operators, and institutional users). It also highlights the global and regional distribution of demand, with a specific focus on key regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

Technological advancements such as AI-integrated monitoring, digital twins, and hydrogen readiness are included as critical service trends shaping the future. The report also provides insights into the competitive dynamics, profiling key market participants and outlining strategic initiatives and innovation activities. Niche segments such as hybrid fuel servicing and decentralized energy system support are explored for their emerging relevance.

Additionally, the scope incorporates analysis of macroeconomic factors influencing the market, such as regulatory trends, energy transition goals, and regional modernization programs. It is tailored for industry professionals, decision-makers, and stakeholders looking to understand both current performance and future opportunities in the global Gas Turbine Services Market.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 3,810.0 Million |

| Market Revenue (2032) | USD 7,317.5 Million |

| CAGR (2025–2032) | 8.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Service Type

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Technological Insights, Market Dynamics, Segment Analysis, Regional and Country-Wise Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | General Electric Company, Siemens Energy AG, Mitsubishi Power, Ltd., Ansaldo Energia S.p.A., MAN Energy Solutions SE, Solar Turbines Incorporated, EthosEnergy Group Limited, Bharat Heavy Electricals Ltd. (BHEL), MTU Aero Engines AG, Kawasaki Heavy Industries, Ltd., Sulzer Ltd., Doosan Enerbility Co., Ltd., Solar Turbines Incorporated |

| Customization & Pricing | Available on Request (10% Customization is Free) |