Reports

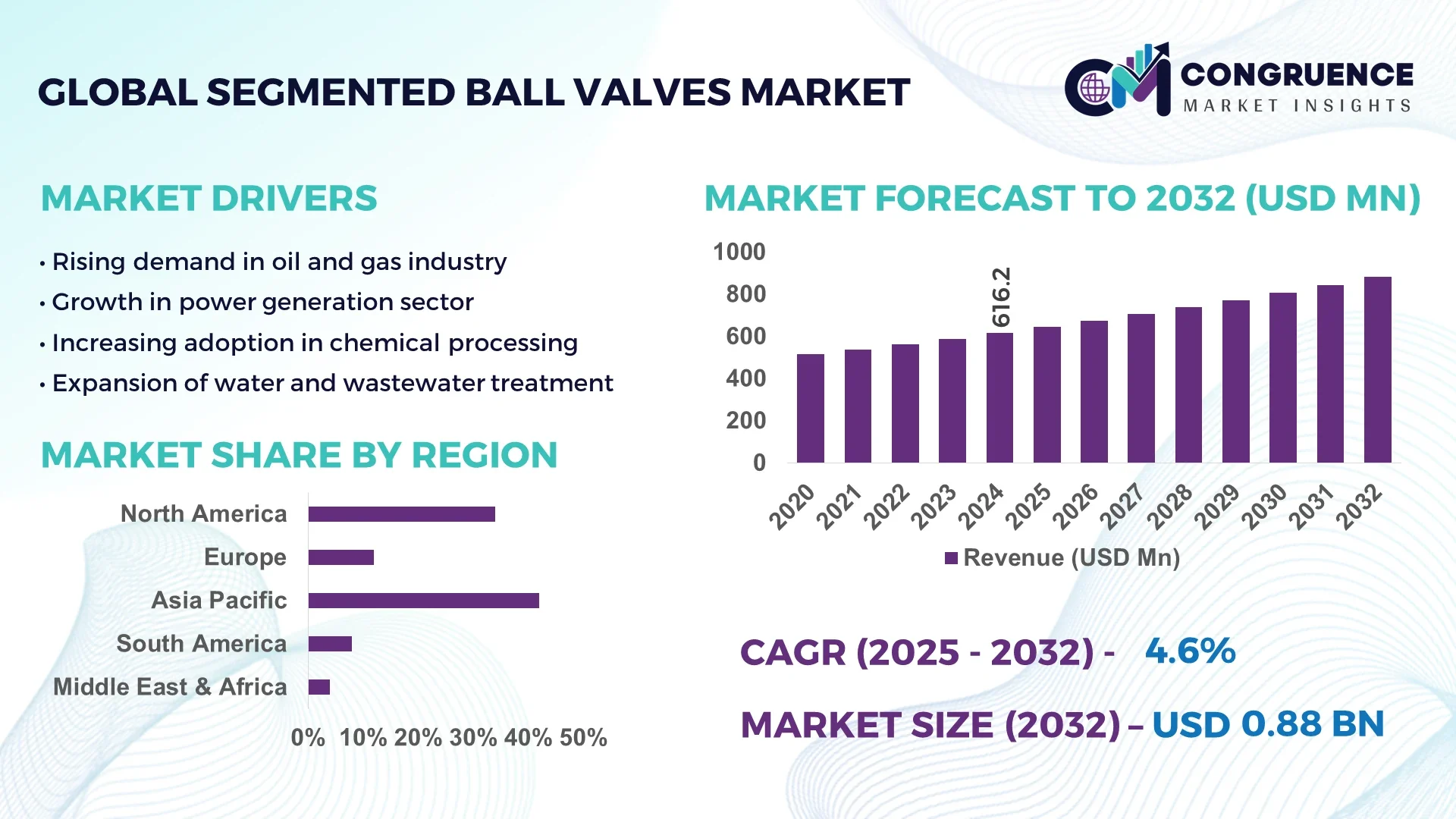

The Global Segmented Ball Valves Market was valued at USD 616.19 Million in 2024 and is anticipated to reach a value of USD 883.02 Million by 2032 expanding at a CAGR of 4.6%% between 2025 and 2032.

China, as the leading country in this market, demonstrates formidable production capacity with over 1.1 million segmented ball valves deployed in 2024 across municipal water systems, petrochemical refineries, and LNG terminals. Significant investment continues in upstream and downstream infrastructure, while advancements in smart actuator integration and corrosion-resistant materials support its technological leadership.

Key industry sectors include oil and gas responsible for deployment of over 2.3 million segmented ball valves in refining, pipelines, and LNG systems in 2024 and chemical and petrochemical industries utilizing over 1.8 million valves for precision flow control in reactors and distillation systems. Water and wastewater treatment also accounted for approximately 1.6 million valves in filtration plants, desalination and sewer systems, especially in Asia Pacific. Pulp and paper applications consumed about 1.4 million valves, and other sectors such as mining, food processing, pharmaceuticals, and power generation accounted for the remaining volume. Recent innovations include integration of smart actuators and positioners enabling remote diagnostics and predictive maintenance with over 1.1 million valves now using these systems globally. Materials innovations feature duplex stainless steel, Hastelloy, and ceramic coated alloys with over 1.7 million units manufactured using such high durability materials. Modular valve designs are gaining traction, with around 920,000 modular segmented ball valves sold in 2024, facilitating easier maintenance and adaptability. Environmental and regulatory drivers include deployment of more than 850,000 low emission valves certified under ISO 15848 and 300,000 fire safe units meeting API 607 for emergency shutdowns. Regional consumption patterns emphasize Asia Pacific, which accounted for over 2.7 million valve deployments in 2024 led by China and India, followed by North America with over 1.8 million units, particularly in U.S. refineries and pulp mills. Emerging trends include enhanced flow efficiency via modified V notch geometry achieving 18% better throttling accuracy, eco compliant valve solutions, modularity, and smart technologies for predictive maintenance. Future outlook projects continued adoption across heavy industries, infrastructure and municipal projects, especially driven by environmental compliance and automation needs.

The incorporation of AI in the Segmented Ball Valves Market is reshaping maintenance strategies and operational efficiencies. AI driven predictive maintenance dramatically reduces unplanned outages by sourcing and analyzing rich sensor data including actuator torque, vibration, temperature, position feedback, and acoustic signals. These analytics enable early detection of wear, leaks, or blockages before failures occur, extending valve lifespan, reducing maintenance costs, enhancing safety, and maintaining continuous process efficiency. This transformation is particularly vital in sectors like oil and gas, water treatment, chemical, and power generation.

Valve manufacturers are now offering platforms combining AI, diagnostics, and human expertise to prioritize maintenance needs. For example, systems such as Valmet’s VII and ValvesNow use AI based analytics of diagnostics data from positioners like ND9000 to flag underperforming valves and optimize maintenance schedules. AI powered service demand forecasting predicts valve service intervals more accurately based on extensive service data, thereby enhancing lifecycle reliability.

In automation systems, digital valve controllers equipped with advanced sensors and AI enabled software now provide continuous monitoring of actuator performance, packing, and system integrity. These next generation controllers facilitate early failure identification and support proactive maintenance planning through automatically generated insights.

Collectively, AI is transforming the Segmented Ball Valves Market by delivering smarter, condition based maintenance, reducing downtime, and improving operational efficiency in critical industrial applications.

"In 2024, Valmet’s AI powered service demand forecast, leveraging machine learning on extensive valve diagnostics data, successfully predicted optimal service intervals with accuracy improvements of over 20% in lifecycle estimation and maintenance scheduling for industrial valve fleets."

The Segmented Ball Valves Market is influenced by multiple interconnected factors ranging from industrial automation, environmental regulations, and material innovations to digitalization of flow control systems. With growing demand across oil and gas, chemical, power, and water treatment industries, the market reflects strong reliance on advanced valve technologies capable of offering superior throttling accuracy and minimal leakage. Increasing adoption of automated process control systems and smart actuators integrated with IoT and AI capabilities is further enhancing operational reliability. Additionally, regulatory mandates on emissions and safety certifications continue to shape product development, while fluctuations in raw material supply and global infrastructure spending significantly impact market behavior.

Rising automation across industries is one of the strongest growth drivers for the Segmented Ball Valves Market. Modern refineries, petrochemical plants, and power generation facilities demand advanced valve systems that can integrate with distributed control systems (DCS) and supervisory control and data acquisition (SCADA) platforms. These valves allow precise throttling and consistent flow regulation, making them essential for critical applications. In 2024, over 70% of newly commissioned industrial plants in Asia Pacific implemented automated flow control solutions, with segmented ball valves being a key component due to their durability and accuracy. By reducing manual intervention and enabling real time monitoring, automation enhances safety, reduces downtime, and optimizes energy usage, thereby strengthening demand for segmented ball valves globally.

A major restraint in the Segmented Ball Valves Market arises from the complexity associated with installation and long term maintenance. Segmented ball valves, particularly when fitted with advanced actuators and digital controllers, require specialized expertise for setup and calibration. Industries such as oil and gas and water treatment often report extended installation timelines, which can delay project execution. Furthermore, periodic servicing is essential to prevent leakage or flow disruption, and this involves high labor and spare part costs. In regions with limited access to skilled workforce, the maintenance factor becomes an even greater barrier. These operational hurdles increase the total cost of ownership, limiting widespread adoption in cost sensitive markets and mid scale industrial applications.

The growing emphasis on sustainability and digital transformation offers a significant opportunity in the Segmented Ball Valves Market. Manufacturers are increasingly developing low emission valves that comply with stringent international standards such as ISO 15848 and API 607, addressing both regulatory and environmental concerns. Parallelly, the integration of smart actuators, sensors, and AI enabled diagnostics opens new avenues for predictive maintenance and lifecycle optimization. By 2025, an estimated 1.5 million segmented ball valves worldwide are expected to feature smart monitoring capabilities, allowing operators to predict failures and reduce downtime by up to 25%. The demand for environmentally sustainable and intelligent solutions is driving innovation, making this segment one of the fastest growing opportunities in the market.

The Segmented Ball Valves Market faces considerable challenges due to fluctuations in raw material availability and escalating production costs. Stainless steel, Hastelloy, and ceramic coatings, which are critical materials for manufacturing high performance valves, are subject to global price volatility influenced by mining output, trade restrictions, and geopolitical tensions. In 2024, stainless steel prices rose by over 18% compared to the previous year, directly impacting the production costs of valves. Additionally, compliance with strict certification standards for fire safety and emissions further raises manufacturing expenditures. Small and mid sized manufacturers often struggle to absorb these rising costs, creating pressure on profit margins and slowing down their expansion capabilities in competitive markets.

• Rise in Modular and Prefabricated Construction: The adoption of modular and prefabricated construction methods is driving higher demand for segmented ball valves that can integrate seamlessly into pre-assembled piping systems. In 2024, over 320,000 segmented ball valves were supplied to modular construction projects across Europe and North America, where efficiency and reduced labor requirements are key priorities. These valves ensure precision fitment within prefabricated systems and help achieve shorter project timelines while maintaining stringent performance standards.

• Growing Demand for Smart and Connected Valves: The integration of IoT and AI into segmented ball valves has accelerated, with more than 1.2 million smart-enabled valves installed globally by 2024. These valves offer real-time monitoring, automated diagnostics, and predictive maintenance features that significantly reduce unplanned downtime in critical industries such as oil and gas and power generation. Smart valve adoption is expanding rapidly in Asia Pacific, where industrial automation investments reached record levels, supporting the shift toward intelligent process control.

• Expansion of Low-Emission and Eco-Compliant Designs: Environmental compliance is a central trend reshaping product design. By 2024, over 900,000 segmented ball valves were manufactured with low-fugitive emission certifications, meeting stringent global standards for leakage prevention. This shift is especially evident in the chemical and petrochemical industries, where regulatory compliance is non-negotiable. Eco-compliant designs are also gaining traction in municipal water projects, where reducing emissions and ensuring system reliability are critical to infrastructure sustainability.

• Material Advancements in Valve Manufacturing: Material innovation has become a defining trend, with more than 1.5 million segmented ball valves in 2024 manufactured using duplex stainless steel, ceramic coatings, and Hastelloy. These advanced materials provide superior corrosion resistance and extended lifecycle in harsh environments such as offshore oil platforms, desalination plants, and chemical processing units. This shift is particularly beneficial for industries with extreme operational conditions, as it reduces replacement frequency and long-term costs.

The Segmented Ball Valves Market is structured across types, applications, and end-user categories, each contributing differently to industry growth. Types such as V-notch, T-port, and trunnion-mounted valves serve diverse operational needs ranging from precise throttling to high-pressure flow control. Applications cover oil and gas, chemicals, water treatment, pulp and paper, power generation, and emerging sectors like food and pharmaceuticals, each with unique performance requirements. End-users span heavy industrial plants, utilities, and specialized facilities, with adoption patterns influenced by automation levels, regulatory compliance, and infrastructure investments. This segmentation highlights the versatility of segmented ball valves as they adapt to both traditional industries and emerging application areas, demonstrating balanced growth opportunities across multiple sectors.

V-notch segmented ball valves represent the leading type, widely adopted due to their exceptional precision in flow control and suitability for throttling applications. In 2024, more than 1.4 million V-notch valves were deployed globally, primarily in chemical and pulp and paper industries, where fine regulation of fluids is crucial. Trunnion-mounted valves are gaining momentum as the fastest-growing type, with demand rising in high-pressure applications across oil and gas pipelines and refineries. Their ability to withstand extreme conditions while ensuring leak-free operation makes them increasingly preferred for heavy-duty industrial systems. T-port and L-port segmented valves also contribute to niche applications, particularly in water distribution and food processing, where multiple flow paths are required for process flexibility. Other specialized types, including high-temperature alloy-based valves, remain significant in power plants and petrochemical units where durability is a priority. Together, this diversity in product types ensures that segmented ball valves remain adaptable across industries, supporting both standard and high-performance needs.

The oil and gas sector remains the dominant application area for segmented ball valves, with more than 2.2 million units installed in refineries, LNG facilities, and pipeline systems in 2024. Their role in providing reliable control under high-pressure and corrosive environments secures their position as industry essentials. Water and wastewater treatment represent the fastest-growing application, fueled by rising infrastructure investment and an increasing focus on safe and sustainable water management. More than 1.3 million valves were supplied to desalination plants, sewage systems, and municipal water projects in 2024, marking steady adoption. The chemical and petrochemical sector also contributes substantially, relying on precision flow control for reactors and distillation processes. Pulp and paper industries continue to utilize segmented ball valves for fiber processing and bleaching lines, while the food and beverage and pharmaceutical sectors are emerging as smaller but growing consumers, driven by hygiene standards and process optimization. These diverse applications highlight the versatile role of segmented ball valves across global industries.

Heavy industries such as oil and gas and petrochemicals lead as the primary end-users of segmented ball valves, with over 3.1 million units deployed in 2024 to support exploration, refining, and chemical manufacturing operations. Their reliance on durable and leak-resistant valves ensures consistent performance in demanding environments. The utilities sector, particularly water treatment plants and municipal distribution systems, is the fastest-growing end-user group, with investments in infrastructure modernization leading to deployment of over 1.5 million valves in 2024. Pulp and paper manufacturers, power plants, and mining facilities also contribute significantly, utilizing segmented ball valves to maintain efficiency in complex industrial processes. Meanwhile, food processing and pharmaceutical industries are gradually increasing adoption as hygiene, safety, and precision become more critical in production facilities. Collectively, the end-user landscape demonstrates both established reliance from traditional industries and growing opportunities from emerging sectors, reinforcing the strategic importance of segmented ball valves in global industrial infrastructure.

Asia Pacific accounted for the largest market share at 42% in 2024 however, Middle East and Africa is expected to register the fastest growth, expanding at a CAGR of 5.3% between 2025 and 2032.

The Segmented Ball Valves Market across Asia Pacific has been shaped by massive infrastructure investments, rapid industrialization, and large-scale deployment in water treatment and petrochemical plants. Meanwhile, Middle East and Africa is gaining momentum due to its expanding oil and gas capacity, construction boom, and regulatory emphasis on safety compliance. These dynamics create a dual pathway for growth, with mature consumption in Asia Pacific and new opportunities emerging in developing economies.

Digital Transformation Driving Demand in Critical Flow Control Systems

The North America Segmented Ball Valves Market accounted for approximately 28% of the global volume in 2024, with strong adoption across oil and gas pipelines, chemical industries, and power generation facilities. The demand is supported by large-scale refinery upgrades and the modernization of water treatment plants across the United States and Canada. Regulatory changes from agencies such as the Environmental Protection Agency have reinforced the need for low-emission valves, spurring investment in eco-compliant technologies. Additionally, North America has been at the forefront of adopting smart actuators and AI-based valve diagnostics, with over 450,000 valves now featuring integrated digital monitoring systems, reducing downtime and optimizing operational efficiency across industries.

Green Energy Transition Reshaping Flow Control Technologies

The Europe Segmented Ball Valves Market contributed nearly 21% of global volume in 2024, with Germany, the United Kingdom, and France leading adoption. The transition toward renewable energy, coupled with stringent directives from regulatory bodies such as the European Environment Agency, has accelerated the demand for low-emission valve solutions. The region is also actively integrating Industry 4.0 technologies into manufacturing and process industries, with nearly 300,000 segmented ball valves deployed in smart factories by 2024. Sustainability initiatives, including carbon neutrality commitments, have further pushed the adoption of eco-friendly valve designs, creating opportunities for manufacturers offering high-performance and environmentally compliant solutions.

Industrial Expansion and Infrastructure Modernization Fueling Growth

The Asia Pacific Segmented Ball Valves Market held the dominant position with 42% of the global share in 2024, led by China, India, and Japan. China alone accounted for more than 1.2 million units, driven by rapid urbanization and expansion of its petrochemical and water treatment facilities. India’s infrastructure push, particularly in water management and smart city projects, added over 480,000 valves to its consumption in the same year. Japan continues to lead in advanced manufacturing, with emphasis on high-precision valves for automotive and electronics industries. The region is also an innovation hub, where materials engineering and automation are advancing, creating a strong pipeline for next-generation segmented ball valve solutions.

Energy Sector Investments Strengthening Market Presence

The South America Segmented Ball Valves Market captured nearly 6% of global demand in 2024, with Brazil and Argentina leading adoption. Brazil’s robust oil and gas industry, particularly offshore exploration, accounted for more than 230,000 valve installations. Argentina contributed significantly through investments in shale gas and water treatment projects. Infrastructure development across both countries, including new hydroelectric projects, is fueling additional valve demand. Government-backed energy reforms and favorable trade agreements are encouraging local production and imports of technologically advanced valves, positioning the region for steady industrial expansion and stronger adoption of segmented ball valves.

Oil & Gas Expansion and Construction Boom Driving Market Growth

The Middle East and Africa Segmented Ball Valves Market accounted for around 3% of global share in 2024, with the UAE, Saudi Arabia, and South Africa being the most dynamic markets. The oil and gas sector continues to dominate demand, with over 160,000 valves installed in upstream and downstream operations across the Gulf region. Rapid infrastructure development, including large-scale construction projects and desalination plants, is also creating new opportunities. Technological modernization is underway, with AI-powered diagnostics and IoT-enabled valves increasingly deployed in the UAE. Regulatory reforms and international trade partnerships are further enhancing access to advanced valve technologies, fueling the region’s rapid growth trajectory.

China – 28% market share | China leads the Segmented Ball Valves Market due to its vast production capacity and strong end-user demand across petrochemical, water, and power industries.

United States – 19% market share | The United States dominates with widespread adoption in oil and gas pipelines, refinery upgrades, and advanced digital valve monitoring systems.

The Segmented Ball Valves Market is characterized by a moderately consolidated competitive environment, with more than 40 active global and regional manufacturers competing across diverse industrial sectors. Leading companies hold strong positions through extensive distribution networks, advanced product portfolios, and technological integration in valve automation and diagnostics. Innovation trends such as IoT-enabled smart valves, AI-driven predictive maintenance solutions, and eco-compliant low-emission designs are defining the competitive strategies of top players. Strategic collaborations, mergers, and acquisitions remain frequent, with several companies expanding into new geographic markets or strengthening their service capabilities through digital platforms. In 2024, over 15 notable product launches were recorded, focusing on corrosion-resistant materials, modular valve designs, and enhanced actuator compatibility. Partnerships between valve manufacturers and automation technology firms are also reshaping competitive dynamics, enabling bundled solutions that combine hardware reliability with software-driven insights. The competitive intensity is further reinforced by mid-sized companies specializing in niche applications, such as pulp and paper or desalination, contributing to a balanced yet highly innovation-driven market landscape.

Emerson Electric Co.

Flowserve Corporation

Metso Corporation (Valmet Flow Control)

Crane Co.

KITZ Corporation

IMI Critical Engineering

Velan Inc.

Samson AG

Bray International Inc.

Cameron International

Apollo Valves

Neles Corporation

Technological advancements in the Segmented Ball Valves Market are reshaping how industries manage flow control, safety, and operational efficiency. A major trend is the integration of smart valve positioners and AI-enabled diagnostic systems, which allow real-time monitoring of torque, vibration, temperature, and leakage. By 2024, over 1.3 million segmented ball valves were equipped with digital positioners, enabling predictive maintenance that reduces downtime by up to 25%. This shift not only extends product life cycles but also enhances safety in critical applications like petrochemicals and power generation.

Material innovations have further strengthened product performance. Advanced alloys such as duplex stainless steel, Hastelloy, and Inconel are now widely used, with more than 1.1 million units manufactured using corrosion-resistant materials in 2024. Ceramic coatings and composite materials are also gaining traction, particularly in chemical processing and desalination plants, where aggressive environments demand high durability.

Automation and modular valve design are also key developments. Over 800,000 modular segmented ball valves were deployed in 2024, supporting faster maintenance and flexible integration into industrial systems. Additionally, smart actuator technology now allows remote operation and self-calibration, significantly improving efficiency in large-scale installations. Together, these innovations are positioning segmented ball valves as a cornerstone of intelligent industrial infrastructure.

• In March 2023, Emerson introduced an upgraded Fisher digital valve controller equipped with AI-based analytics, enabling predictive diagnostics across segmented ball valves. The system demonstrated a 22% improvement in maintenance scheduling accuracy for refineries and chemical plants.

• In October 2023, Flowserve expanded its European manufacturing facility to increase production of segmented ball valves with low-emission certifications. The expansion added a capacity of 120,000 valves annually, supporting stricter environmental compliance across Europe.

• In February 2024, Metso (Valmet Flow Control) launched a new modular segmented ball valve series featuring enhanced V-notch geometry, achieving 18% better flow accuracy. Over 30,000 units were deployed in pulp and paper mills within six months of launch.

• In July 2024, KITZ Corporation unveiled a high-performance segmented ball valve designed for LNG terminals, built with duplex stainless steel and smart actuators. Early trials showed a 17% increase in durability compared to previous models in cryogenic conditions.

The Segmented Ball Valves Market Report provides a comprehensive overview of global industry performance, covering product types, applications, end-user industries, and geographic regions. The scope of the report includes detailed analysis of segmented ball valve types such as V-notch, T-port, trunnion-mounted, and modular designs, each serving specific operational needs across industrial sectors. By 2024, more than 6.5 million valves were deployed worldwide, demonstrating the scale of adoption across critical infrastructure. The report addresses key applications, including oil and gas, water and wastewater treatment, chemicals, power generation, pulp and paper, and emerging fields such as pharmaceuticals and food processing. With over 2.2 million valves used in oil and gas alone in 2024, the report emphasizes the dominant sectors while also highlighting fast-growing segments like water treatment, which added more than 1.3 million installations in the same year.

Geographically, the scope spans Asia Pacific, North America, Europe, South America, and the Middle East and Africa, with Asia Pacific accounting for 42% of global demand in 2024. The report also examines regional consumption patterns, infrastructure projects, and regulatory frameworks shaping demand. Additionally, the scope explores technological advancements, including AI-driven valve monitoring, modular designs for flexible integration, and material innovations that enhance durability. By combining insights into established industries and emerging applications, the report offers decision-makers a structured perspective on market opportunities, challenges, and innovation pathways driving the segmented ball valves industry globally.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 616.19 Million |

|

Market Revenue in 2032 |

USD 883.02 Million |

|

CAGR (2025 - 2032) |

4.6% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Emerson Electric Co., Flowserve Corporation, Metso Corporation (Valmet Flow Control), Crane Co., KITZ Corporation, IMI Critical Engineering, Velan Inc., Samson AG, Bray International Inc., Cameron International, Apollo Valves, Neles Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |