Reports

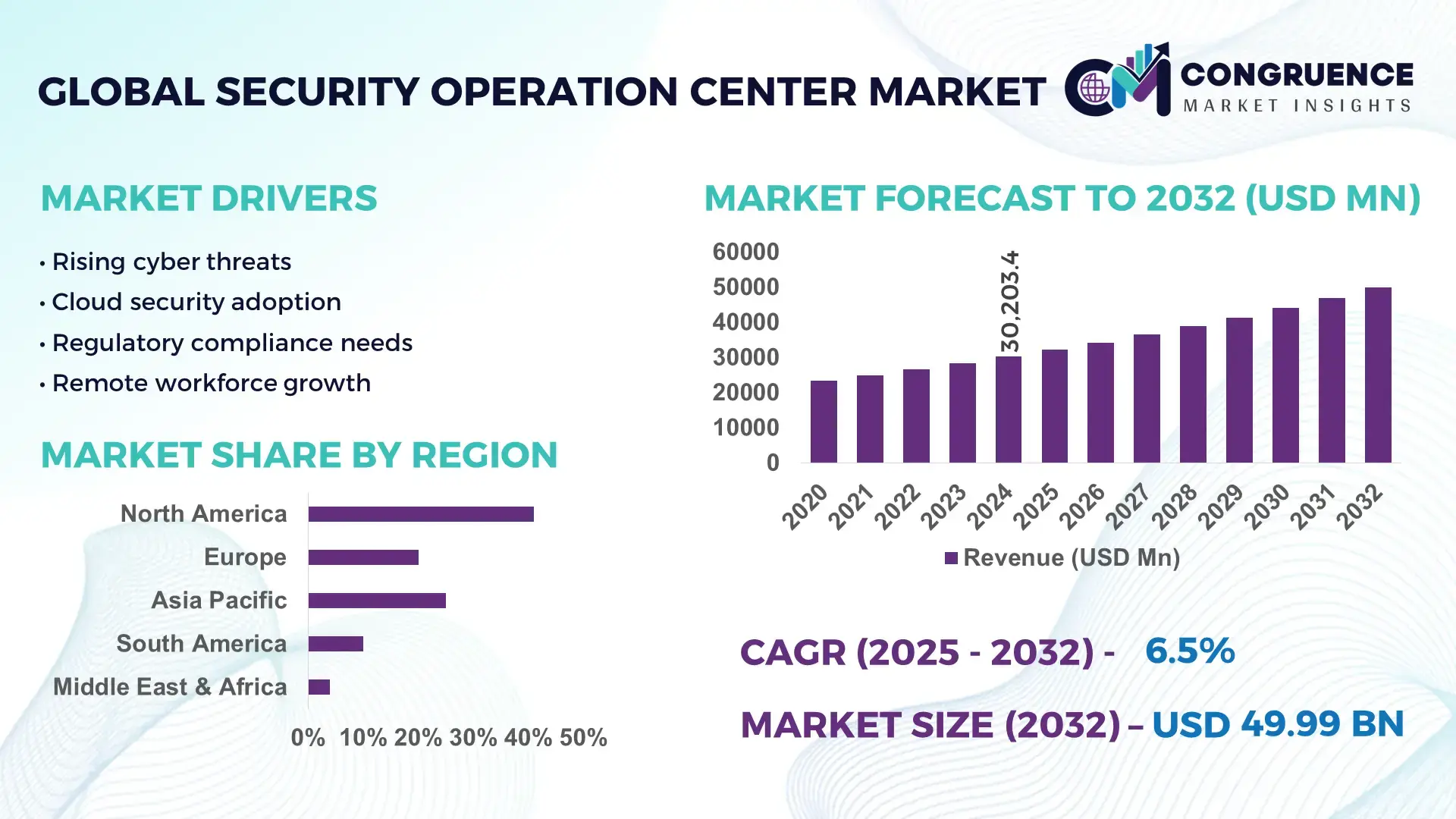

The Global Security Operation Center Market was valued at USD 30203.4 Million in 2024 and is anticipated to reach a value of USD 49986.49 Million by 2032 expanding at a CAGR of 6.5% between 2025 and 2032. This growth is primarily supported by the rising complexity of cyberattacks, expanding cloud and hybrid IT environments, and the increasing need for real-time threat detection and response capabilities across enterprises.

The United States represents the most prominent country in the Security Operation Center market, supported by extensive SOC infrastructure, high cybersecurity expenditure, and advanced technology adoption. More than 3,500 large organizations in the country operate internal, outsourced, or hybrid SOC models, processing billions of security events daily. In 2024, U.S. cybersecurity spending surpassed USD 90 billion, with SOC platforms, managed detection and response (MDR), and automation tools forming a major investment focus. SOC deployments are heavily concentrated in BFSI, defense, healthcare, IT services, and critical infrastructure, with over 65% of SOCs leveraging AI-driven SIEM, SOAR, and XDR technologies to improve operational efficiency. Managed SOC adoption is expanding rapidly among mid-sized enterprises, driven by cost optimization and skills shortages, while large enterprises continue to invest in high-capacity, in-house SOCs integrated with national and sectoral threat intelligence networks.

Market Size & Growth: Valued at USD 30203.4 million in 2024, expected to reach USD 49986.49 million by 2032 at a CAGR of 6.5%, driven by escalating cyber risk exposure and continuous security monitoring needs.

Top Growth Drivers: Cloud workload security adoption (68%), SOC automation and orchestration deployment (54%), regulatory compliance-driven monitoring requirements (47%).

Short-Term Forecast: By 2028, organizations are projected to achieve up to 35% improvement in incident response efficiency through AI-enabled SOC operations.

Emerging Technologies: Artificial intelligence–driven SIEM platforms, SOAR-based automated response, and Extended Detection and Response (XDR) integration.

Regional Leaders: North America projected to reach USD 18500 million by 2032 with AI-first SOC models; Europe expected at USD 12800 million driven by compliance-centric SOC adoption; Asia-Pacific forecast at USD 11200 million supported by cloud-native SOC expansion.

Consumer/End-User Trends: BFSI and IT & telecom sectors together account for over 45% of SOC deployments, with rising preference for managed SOC services among SMEs.

Pilot or Case Example: In 2024, a major U.S. financial services organization implemented SOAR-enabled SOC workflows, achieving a 42% reduction in incident resolution time.

Competitive Landscape: IBM leads with approximately 14% share, followed by Accenture, AT&T Cybersecurity, Secureworks, and Palo Alto Networks.

Regulatory & ESG Impact: Data protection regulations and critical infrastructure cybersecurity mandates are increasing SOC adoption and operational transparency requirements.

Investment & Funding Patterns: Global investments exceeding USD 18 billion were directed toward SOC modernization, MDR platforms, and security analytics during 2023–2024.

Innovation & Future Outlook: Integration of generative AI, predictive threat intelligence, and unified security platforms is defining next-generation SOC architectures.

The Security Operation Center market supports a broad range of industry verticals, with BFSI contributing approximately 28% of total demand, followed by IT & telecom, government, healthcare, energy, and manufacturing. Continuous innovation in AI-driven threat detection, automated incident response, and cloud-native SOC platforms is reshaping operational models and reducing response times. Regulatory mandates related to data privacy, financial security, and critical infrastructure protection remain key demand drivers, while economic digitization is expanding SOC adoption in emerging regions. Looking ahead, SOC-as-a-Service models, convergence of IT and OT security, and predictive analytics are expected to play a critical role in shaping future market growth and enterprise security strategies.

The Security Operation Center Market has become strategically indispensable as enterprises transition toward hyperconnected digital ecosystems, cloud-native architectures, and remote work environments. SOCs now function as centralized command structures that integrate threat intelligence, incident response, compliance monitoring, and business continuity management. From a strategic standpoint, AI-enabled SOC platforms are redefining operational benchmarks; for example, Extended Detection and Response (XDR) delivers nearly 45% faster threat correlation and response compared to traditional SIEM-only architectures. Regionally, North America dominates in operational volume due to large-scale enterprise deployments, while Europe leads in adoption, with approximately 62% of regulated enterprises operating dedicated or managed SOCs aligned with compliance mandates. In the short term, by 2027, AI-driven security orchestration and automated response is expected to improve mean-time-to-respond (MTTR) by nearly 40% across enterprise SOC environments. From a compliance and ESG perspective, firms are committing to measurable sustainability outcomes, including 30% reductions in data center energy consumption and increased use of carbon-efficient cloud SOC platforms by 2028. A micro-scenario highlighting this trajectory occurred in 2024, when the United States federal cybersecurity infrastructure achieved a 38% reduction in high-severity incident dwell time through nationwide SOAR and AI threat-hunting initiatives. Looking forward, the Security Operation Center Market is positioned as a core pillar of organizational resilience, regulatory compliance, and sustainable digital growth, enabling enterprises to secure assets while aligning cybersecurity investments with long-term governance and efficiency objectives.

The increasing frequency and complexity of cyberattacks are a primary driver of growth in the Security Operation Center Market. Enterprises now face multi-vector threats including ransomware, zero-day exploits, and supply-chain attacks, with global organizations processing millions of security events daily. Over 70% of large enterprises report that attack dwell times exceed acceptable thresholds without centralized SOC operations. As a result, organizations are investing in 24/7 monitoring, advanced threat intelligence, and automated incident response to minimize operational disruption. The rise of cloud workloads and remote endpoints has further expanded attack surfaces, making decentralized security tools ineffective. SOCs provide unified visibility and correlation across networks, endpoints, and applications, enabling faster detection and containment. This heightened threat environment is compelling organizations across BFSI, healthcare, government, and critical infrastructure sectors to prioritize SOC deployment as a foundational security capability.

A persistent shortage of skilled cybersecurity professionals remains a significant restraint for the Security Operation Center Market. SOC operations require specialized expertise in threat analysis, incident response, malware investigation, and compliance reporting. However, the global cybersecurity talent gap exceeds 3 million professionals, limiting organizations’ ability to staff and scale SOCs effectively. High analyst attrition rates and burnout caused by alert fatigue further strain operational continuity. Smaller enterprises often lack the resources to recruit and retain qualified personnel, leading to delayed SOC adoption or reliance on limited monitoring solutions. Additionally, the complexity of integrating multiple security tools increases training and operational overhead. These workforce-related challenges can slow SOC deployment timelines and increase operational risk, particularly for organizations without access to managed security service providers.

AI-driven automation presents substantial growth opportunities for the Security Operation Center Market by enabling scalable, efficient, and cost-effective security operations. Automated threat detection, correlation, and response reduce manual workloads and allow SOC analysts to focus on high-value investigations. Organizations implementing AI-powered SOC platforms report up to 50% reductions in false-positive alerts and significant improvements in response consistency. The growing adoption of SOC-as-a-Service models further expands market opportunities, particularly among SMEs seeking enterprise-grade security without large capital investments. Emerging markets are also investing in national and sector-specific SOC initiatives to protect digital infrastructure. As AI models mature and integrate predictive analytics, SOCs will transition from reactive monitoring centers to proactive risk management hubs, unlocking new service models and long-term growth potential.

Integration complexity remains a key challenge for the Security Operation Center Market, particularly for organizations operating legacy IT and security infrastructures. Many enterprises rely on fragmented security tools that generate siloed data, making unified threat visibility difficult. Integrating legacy systems with modern AI-enabled SOC platforms often requires extensive customization, increasing deployment time and operational risk. Data normalization across heterogeneous environments also presents challenges, especially for multinational organizations with diverse compliance requirements. Additionally, the cost and effort associated with migrating from traditional on-premise SOC models to hybrid or cloud-based architectures can delay modernization initiatives. These integration and transformation challenges require careful planning, investment, and change management, posing obstacles to rapid SOC adoption despite strong underlying demand.

Acceleration of AI-Driven Automation in SOC Operations: Enterprises are rapidly embedding artificial intelligence and machine learning into SOC workflows to manage growing alert volumes and analyst shortages. In 2024, more than 60% of enterprise SOCs deployed AI-based alert triage, achieving up to 48% reduction in false positives and nearly 35% faster incident prioritization. Automated correlation engines now process over 10 million security events per day in large SOC environments, significantly improving detection accuracy and operational consistency while reducing manual analyst intervention.

Expansion of Managed and Hybrid SOC Models Across Enterprises: The shift toward managed SOC and hybrid delivery models is intensifying, particularly among mid-sized organizations. Approximately 58% of enterprises with fewer than 5,000 employees now rely on partially or fully outsourced SOC services, compared to 41% in 2021. Hybrid SOC models combining in-house governance with third-party monitoring have demonstrated up to 32% improvement in coverage continuity and 28% lower operational workload for internal security teams, supporting scalable security management.

Integration of Cloud-Native and XDR Platforms: Cloud-native SOC architectures and Extended Detection and Response (XDR) platforms are reshaping technology stacks. Over 65% of newly deployed SOC platforms in 2024 were cloud-based, enabling unified visibility across endpoints, networks, and workloads. Organizations using XDR report up to 44% faster threat correlation compared to legacy multi-tool environments, while cloud-native SOC deployments have improved system scalability by more than 50% during peak attack periods.

Rising Emphasis on Compliance, ESG, and Energy-Efficient SOC Infrastructure: Compliance-driven monitoring and sustainability initiatives are influencing SOC design and operations. Nearly 46% of enterprises upgraded SOC infrastructure in 2024 to meet stricter data protection and incident reporting mandates. At the same time, organizations adopting energy-efficient SOC platforms and optimized data centers achieved up to 27% reductions in energy consumption. ESG-aligned SOC strategies are increasingly prioritized, with 40% of large enterprises setting measurable targets for reduced operational footprint by 2027.

The Security Operation Center Market is segmented based on type, application, and end-user, reflecting the diverse operational models and deployment needs across industries. Market segmentation highlights a clear shift toward advanced, automated, and service-oriented SOC structures as organizations respond to rising cyber risks, regulatory complexity, and infrastructure expansion. Type-based segmentation captures variations in SOC deployment architecture and service delivery, while application-based segmentation reflects how SOC capabilities are used across threat monitoring, compliance, and operational resilience. End-user segmentation demonstrates differing maturity levels, budget priorities, and risk exposure across industries such as BFSI, government, IT & telecom, healthcare, and manufacturing. Adoption patterns show that larger enterprises prioritize integrated and AI-enabled SOC platforms, whereas mid-sized organizations increasingly favor managed or hybrid models. Across all segments, measurable factors such as alert volume handled, response time reduction, compliance coverage, and automation levels play a decisive role in SOC selection and deployment strategies.

The Security Operation Center Market by type includes In-House SOC, Managed SOC, Co-Managed SOC, Virtual SOC, and Cloud-Native SOC platforms. In-house SOCs currently account for approximately 38% of total adoption, driven by large enterprises and government agencies that require full control over sensitive data, internal workflows, and national security operations. Managed SOCs represent around 29% of adoption, offering cost-efficient, 24/7 monitoring capabilities, particularly attractive to mid-sized enterprises. However, Cloud-Native and Virtual SOC models are the fastest-growing types, expanding at an estimated CAGR of 14.8%, supported by cloud adoption, remote workforce expansion, and scalable monitoring requirements. These models are expected to surpass 30% combined adoption by 2032. Co-managed SOCs and sector-specific SOCs together contribute nearly 33% of the market, serving organizations that balance internal oversight with third-party expertise.

By application, threat detection and incident response remains the leading segment, accounting for approximately 46% of SOC deployments, as organizations prioritize rapid identification and containment of cyber incidents. Compliance monitoring and reporting follows with nearly 21% adoption, driven by regulatory mandates across finance, healthcare, and critical infrastructure sectors. However, proactive threat intelligence and advanced threat hunting applications are growing fastest, recording an estimated CAGR of 13.2%, as enterprises seek predictive capabilities rather than reactive defense. Security analytics and vulnerability management applications together contribute about 33% of total adoption, supporting continuous risk assessment and posture management. Organizations integrating SOCs for real-time threat intelligence have reported up to 45% improvement in early threat detection accuracy.

End-user segmentation shows that the BFSI sector leads the Security Operation Center Market with approximately 28% adoption, driven by high transaction volumes, stringent regulatory oversight, and continuous fraud and threat monitoring requirements. Government and defense organizations follow closely with around 22% share, operating large-scale SOCs for national infrastructure and public service protection. IT & telecom end-users account for nearly 18% of adoption, managing complex, high-traffic digital ecosystems. Healthcare and manufacturing together contribute about 32% of total adoption, with increasing focus on data protection and operational continuity. The fastest-growing end-user segment is healthcare, expanding at an estimated CAGR of 15.1%, fueled by digitization of patient records and rising ransomware incidents.

North America accounted for the largest market share at 41% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.2% between 2025 and 2032.

North America continues to lead due to high enterprise cybersecurity spending, large-scale SOC deployments, and mature digital infrastructure, with more than 60% of Fortune 1000 companies operating dedicated or hybrid SOCs. Europe follows with approximately 27% market share, driven by strict regulatory enforcement and compliance-led SOC adoption across financial services, public sector, and critical infrastructure. Asia-Pacific currently represents nearly 23% of the global market, supported by rapid digitalization, cloud adoption, and rising cyber incidents across emerging economies. South America and the Middle East & Africa together account for the remaining 9%, with adoption concentrated in telecom, energy, and government sectors. Regional variations are strongly influenced by regulatory maturity, enterprise digital readiness, sectoral risk exposure, and availability of managed SOC services, shaping differentiated growth trajectories across global markets.

The North America Security Operation Center Market holds approximately 41% of global adoption, supported by widespread SOC penetration across BFSI, healthcare, defense, and IT & telecom sectors. Financial institutions alone account for nearly 30% of regional SOC demand, driven by high transaction volumes and regulatory oversight. Government initiatives focused on critical infrastructure protection and cyber resilience have accelerated SOC modernization programs. Advanced technologies such as AI-driven SIEM, SOAR, and XDR are deployed in over 65% of enterprise SOCs in this region. Local players such as IBM continue to expand AI-enabled SOC platforms, enabling faster incident response and integrated threat intelligence. Consumer behavior shows higher enterprise adoption in healthcare and finance, with large organizations favoring in-house or co-managed SOCs, while mid-sized firms increasingly opt for managed SOC services to address skills shortages.

Europe accounts for nearly 27% of the global Security Operation Center Market, with strong demand across Germany, the United Kingdom, and France, which together represent over 55% of regional deployments. Regulatory frameworks focused on data protection, operational resilience, and critical infrastructure security are key adoption drivers. More than 60% of large European enterprises operate SOCs aligned with regulatory audit and reporting requirements. Emerging technologies such as explainable AI and compliance-centric analytics are increasingly integrated into SOC platforms. Regional players like Atos are strengthening managed SOC capabilities to support cross-border compliance and multilingual threat monitoring. Consumer behavior in Europe reflects a strong preference for transparent, auditable SOC operations, with demand driven by regulatory pressure and risk governance priorities rather than purely operational efficiency.

Asia-Pacific ranks as the third-largest market by volume, contributing around 23% of global SOC adoption, with China, India, and Japan collectively accounting for over 60% of regional demand. Expanding digital infrastructure, cloud migration, and large-scale e-commerce platforms are significantly increasing SOC deployment across enterprises. Telecom, banking, and manufacturing sectors are leading adopters, with over 45% of new SOC implementations linked to cloud-native environments. Regional innovation hubs in India, Singapore, and South Korea are driving AI-enabled SOC development and cybersecurity talent growth. Local providers are expanding managed SOC offerings to serve SMEs and fast-growing digital businesses. Consumer behavior in Asia-Pacific is driven by mobile-first platforms, e-commerce growth, and increasing cyber exposure from connected devices.

South America represents approximately 5% of global SOC adoption, with Brazil and Argentina accounting for nearly 65% of regional demand. Growth is concentrated in telecom, energy, and financial services sectors, where digital infrastructure upgrades are increasing cybersecurity requirements. Government-led digital transformation initiatives and cross-border trade expansion are encouraging SOC deployment for fraud prevention and data protection. Regional service providers are focusing on managed SOC solutions to support organizations with limited internal security expertise. Consumer behavior shows rising SOC demand tied to media platforms, digital banking, and language-localized security services, particularly in Portuguese and Spanish-speaking markets.

The Middle East & Africa region accounts for roughly 4% of global SOC adoption, with demand driven by oil & gas, utilities, government, and large construction projects. The UAE and South Africa together contribute over 50% of regional SOC deployments, supported by national cybersecurity strategies and smart infrastructure initiatives. Enterprises are increasingly modernizing SOCs with cloud-based platforms to monitor geographically distributed assets. Local regulations focused on data sovereignty and national security are influencing SOC architecture choices. Regional consumer behavior reflects strong demand for SOCs supporting critical infrastructure protection, industrial control systems, and large-scale public-sector digital services.

United States – 34% market share: Strong enterprise cybersecurity spending, large SOC infrastructure base, and extensive adoption across BFSI, healthcare, and government sectors.

Germany – 9% market share: High regulatory compliance requirements and widespread SOC adoption across manufacturing, automotive, and financial services industries.

The Security Operation Center Market is characterized by a moderately fragmented competitive structure, with a mix of global cybersecurity vendors, IT service providers, telecom operators, and specialized managed security service providers. More than 120 active companies operate globally, offering in-house SOC platforms, managed SOC services, hybrid SOC models, and cloud-native security operations. The top five companies collectively account for approximately 46% of total market presence, indicating strong competition beyond the leading tier. Market leaders differentiate through AI-driven analytics, SOAR integration, and Extended Detection and Response capabilities, while mid-tier players focus on regional customization, sector-specific compliance, and cost-efficient managed services.

Strategic initiatives are a defining feature of competition. Over 55% of leading providers launched AI-enhanced SOC upgrades between 2023 and 2024, targeting alert reduction rates above 40% and faster response workflows. Partnerships between SOC providers and cloud hyperscalers have increased by nearly 30%, enabling scalable, cloud-native SOC deployments. Mergers and acquisitions remain selective, with consolidation primarily focused on acquiring threat intelligence platforms, automation engines, and regional SOC providers. Innovation trends include predictive threat analytics, generative AI for incident investigation, and SOC-as-a-Service models designed for SMEs. Competitive positioning increasingly depends on automation depth, compliance readiness, and the ability to manage multi-cloud and hybrid environments at scale.

IBM Corporation

Accenture

Secureworks

AT&T Cybersecurity

Palo Alto Networks

Cisco Systems

DXC Technology

Capgemini

Atos

Tata Consultancy Services

Wipro

HCLTech

Check Point Software Technologies

Fortinet

Fujitsu

Technology evolution is a central force shaping the Security Operation Center Market, as organizations modernize security operations to address escalating cyber threats, expanding attack surfaces, and workforce constraints. Advanced Security Information and Event Management (SIEM) platforms remain foundational, with over 70% of enterprise SOCs relying on next-generation SIEM systems capable of processing billions of events per day and supporting real-time analytics across hybrid environments. These platforms increasingly integrate behavioral analytics and contextual correlation to reduce alert fatigue and improve detection accuracy.

Artificial intelligence and machine learning are now deeply embedded in SOC workflows. More than 60% of SOCs have deployed AI-driven alert triage and prioritization, achieving reductions of up to 45% in false-positive alerts and enabling faster analyst response. Security Orchestration, Automation, and Response (SOAR) technologies are gaining widespread adoption, with nearly half of large enterprises automating at least 30% of routine incident response actions, resulting in response time improvements exceeding 35%. Extended Detection and Response (XDR) platforms are also transforming SOC architectures by unifying endpoint, network, cloud, and identity telemetry into a single investigative view, delivering up to 40% faster threat correlation compared to siloed toolsets.

Cloud-native SOC platforms are expanding rapidly, with approximately 65% of new SOC deployments built on cloud infrastructure to support scalability, remote access, and cost optimization. These platforms enable elastic processing during peak attack periods and facilitate centralized monitoring across geographically distributed assets. Additionally, the adoption of threat intelligence platforms and shared intelligence frameworks has increased by over 30%, allowing SOCs to proactively identify emerging attack patterns. Looking ahead, generative AI, predictive analytics, and autonomous response capabilities are expected to further enhance SOC efficiency, positioning technology as a critical enabler of resilient, compliant, and scalable security operations.

• In April 2024, Cisco completed its $28 billion acquisition of Splunk, integrating Splunk’s SIEM, SOAR, and observability technologies to expand AI‑driven threat detection and automated incident response across its enterprise SOC solutions, positioning Cisco to deliver unified security operations at scale. (Wikipedia)

• In October 2025, Palo Alto Networks launched enhanced AI‑driven security platforms, including Cortex Cloud 2.0 and Prisma AIRS 2.0, incorporating Protect AI technology to secure AI applications throughout development and deployment, reinforcing SOC capabilities against evolving threat vectors. (Reuters)

• In August 2025, Accenture acquired Australian cybersecurity firm CyberCX in a deal valued at over $1 billion, strengthening its SOC services portfolio and expanding managed security operations across Asia‑Pacific to meet rising demand for advanced threat detection and response. (The Australian)

• In 2024, Fortinet completed acquisition of Lacework, adding cloud‑native application protection into its SOC‑as‑a‑Service offerings and enhancing automated cloud threat mitigation, particularly for hybrid and multi‑cloud deployments.

The Security Operation Center Market Report provides a comprehensive framework for understanding the breadth and depth of SOC solutions, technologies, deployment models, and applications across global enterprises. It encompasses segmentation by type (in‑house, managed, co‑managed, cloud‑native, virtual), reflecting how organizations tailor SOC capabilities to internal security strategies or outsource operations to specialist providers. The report examines applications such as real‑time threat detection and incident response, compliance monitoring, threat intelligence integration, advanced analytics, and vulnerability management, highlighting measurable operational impacts like alert reduction percentages, response time improvements, and automation adoption rates.

Geographically, the report covers regional dynamics across North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, with detailed insights into adoption patterns, regulatory influences, digital infrastructure readiness, and sectoral demand such as BFSI, government, healthcare, IT & telecom, energy, and manufacturing. Technology focus areas include next‑generation SIEM and SOAR platforms, AI‑driven analytics, XDR integrations, cloud‑native SOC architectures, and SOC‑as‑a‑Service models designed for scalability and multi‑cloud environments. The report also addresses niche segments such as industry‑specific SOC deployments, small and mid‑sized enterprise (SME) managed services, and emerging autonomous response technologies.

Market intelligence in this report includes competitive landscapes, partnership and innovation trends, measurable adoption rates, and operational benchmarks that enable decision‑makers to align cybersecurity investments with threat patterns, compliance requirements, and enterprise digital transformation goals. It frames the SOC domain as essential for resilient security operations, proactive risk mitigation, and strategic cybersecurity governance across diverse industry sectors.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 30203.4 Million |

Market Revenue in 2032 | USD 49986.49 Million |

CAGR (2025 - 2032) | 6.5% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | IBM Corporation, Accenture, Secureworks, AT&T Cybersecurity, Palo Alto Networks, Cisco Systems, DXC Technology, Capgemini, Atos, Tata Consultancy Services, Wipro, HCLTech, Check Point Software Technologies, Fortinet, Fujitsu |

Customization & Pricing | Available on Request (10% Customization is Free) |