Reports

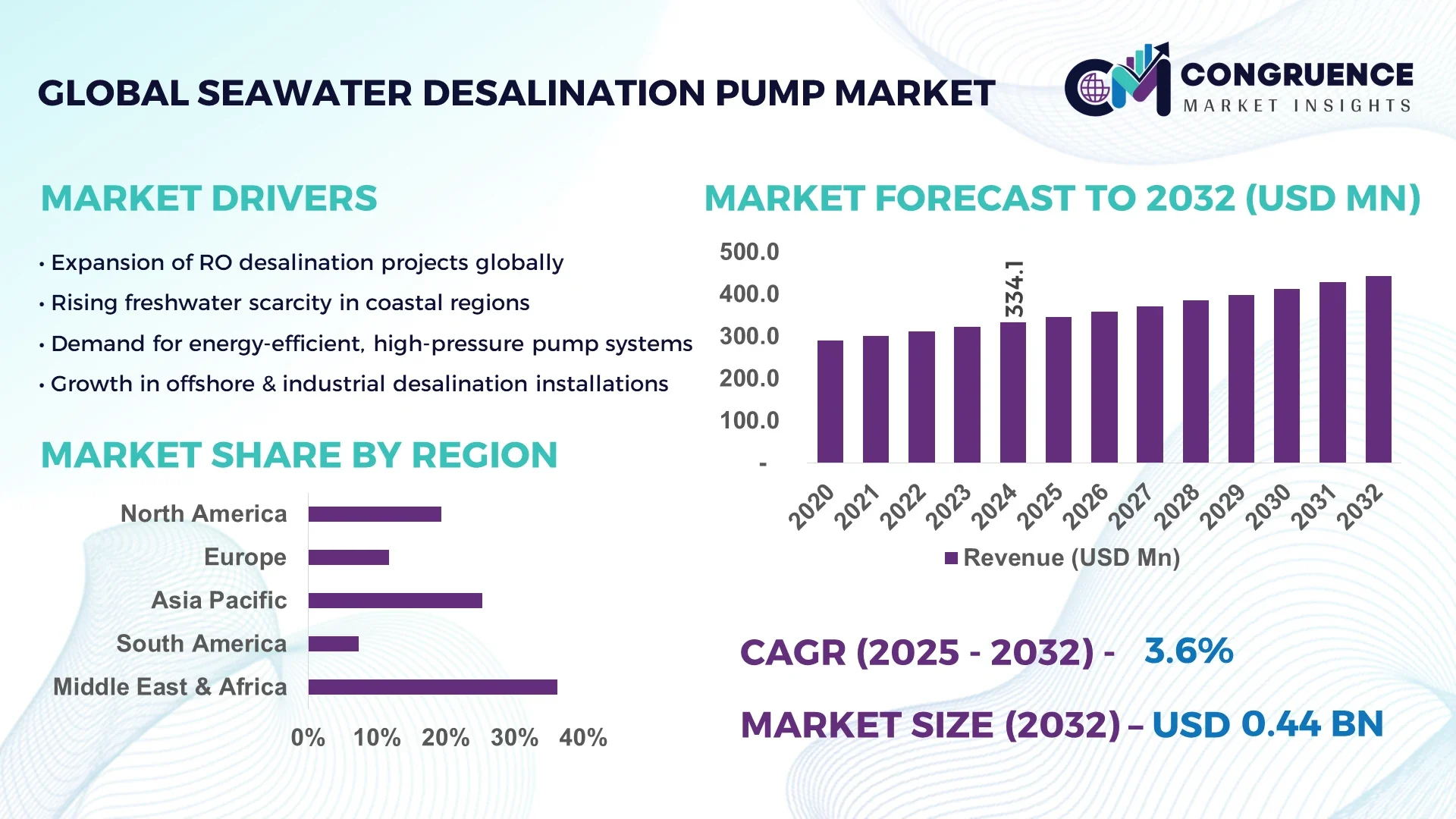

The Global Seawater Desalination Pump Market was valued at USD 334.11 Million in 2024 and is anticipated to reach a value of USD 443.37 Million by 2032 expanding at a CAGR of 3.6% between 2025 and 2032.

In Saudi Arabia, the seawater desalination pump industry has seen robust advancements in high-capacity pump systems integrated with solar-powered desalination facilities, supported by sustained investments in modular desalination plants and precision-engineered pump assemblies for municipal and industrial water supply networks.

The Seawater Desalination Pump Market is witnessing strong momentum across multiple end-user sectors, including municipal water treatment, power generation cooling systems, petrochemical plants, and offshore water injection operations. Recent innovations such as corrosion-resistant alloy pump materials, energy recovery-enabled pumps, and advanced seal technologies are influencing system longevity and maintenance reduction trends within desalination infrastructure projects. Environmental regulations are encouraging energy-efficient and low-carbon pump technologies across coastal desalination sites, while economic incentives in emerging coastal regions are enabling rapid project deployment. The market is further shaped by consistent demand for advanced high-pressure pumps required for reverse osmosis systems, with regional consumption growing in Asia-Pacific, the Middle East, and North Africa. Additionally, emerging trends indicate increasing integration of IoT-enabled pump monitoring, predictive maintenance systems, and smart operational controls for optimizing water production costs in large-scale desalination plants.

Artificial intelligence is driving transformative change across the Seawater Desalination Pump Market, enabling predictive maintenance, performance optimization, and energy consumption reduction within desalination facilities. AI-powered control systems are being deployed to monitor vibration, pressure, and flow metrics across high-capacity pump arrays in real-time, reducing unplanned downtimes by automating diagnostics and failure prediction. Machine learning algorithms are enhancing operational efficiency by dynamically adjusting pump speed and energy usage to match fluctuating feedwater salinity levels, thereby lowering operational costs and extending equipment life. The Seawater Desalination Pump Market is also leveraging AI-integrated digital twins to simulate desalination operations, allowing engineers to identify inefficiencies in pump operations before implementing system-wide changes.

Advanced AI models are further facilitating optimization of membrane cleaning cycles by monitoring fouling levels and adjusting pump operations to prevent unnecessary stress on pump components, reducing both chemical consumption and energy load. Within the Seawater Desalination Pump Market, AI is also improving integration with renewable energy sources, enabling intelligent scheduling and operation of pumps based on grid demand and solar or wind power availability, which reduces energy dependency during peak hours. Additionally, AI-based anomaly detection tools are allowing desalination operators to remotely monitor pump health across multiple sites, improving system reliability and ensuring compliance with stringent water quality standards. This strategic integration of AI is positioning the Seawater Desalination Pump Market to align with global sustainability goals while enhancing operational resilience and reducing the environmental footprint of desalination facilities.

“In 2024, a major desalination facility in Abu Dhabi implemented an AI-powered pump management platform that reduced pump energy consumption by 14% while extending seal replacement cycles by 18% through predictive vibration and temperature analytics, demonstrating measurable operational efficiencies within the Seawater Desalination Pump market.”

The Seawater Desalination Pump Market is experiencing significant evolution driven by increasing coastal water scarcity, technological advancements, and the adoption of energy-efficient desalination infrastructure. The expansion of reverse osmosis and multi-stage flash desalination facilities is propelling demand for high-pressure, corrosion-resistant pump systems capable of handling challenging saline environments while maintaining operational reliability. Government initiatives in water-stressed regions are stimulating investments in advanced desalination plants, directly influencing the Seawater Desalination Pump Market across municipal, industrial, and offshore applications. Additionally, trends such as integrating digital monitoring systems, predictive maintenance, and modular pump skids for scalable projects are shaping market competitiveness while aligning with sustainability and water conservation strategies.

Growing investments in large-scale desalination facilities in water-scarce regions are a primary driver for the Seawater Desalination Pump Market. Countries in the Middle East, including Saudi Arabia and the UAE, are commissioning mega-scale desalination plants requiring high-capacity, energy-efficient pump systems to support municipal water supplies and industrial operations. For example, the ongoing development of integrated desalination projects along the Red Sea coast and industrial clusters in the GCC has led to a rising demand for pumps that can handle high salinity while ensuring low maintenance requirements. Additionally, the increasing deployment of advanced reverse osmosis technology in China and India is expanding pump utilization across new desalination facilities, with consistent replacement and retrofit demand supporting long-term market momentum.

High energy consumption and operational costs remain significant restraints for the Seawater Desalination Pump Market. Seawater desalination processes inherently require substantial energy, with pump systems contributing to a large portion of this consumption due to high-pressure requirements in reverse osmosis and multi-stage flash operations. Operational costs further increase due to maintenance challenges associated with saline environments, including corrosion and scaling, which necessitate frequent component replacement and inspection. Additionally, the cost of anti-fouling measures, advanced seal systems, and specialized materials such as duplex and super duplex stainless steels required in pump construction adds to capital and operational expenditures, creating a barrier for budget-constrained water utilities and smaller desalination project developers.

Integration of energy recovery devices and renewable power sources presents a substantial opportunity for the Seawater Desalination Pump Market. By incorporating pressure exchanger technology and energy recovery turbines, desalination facilities can significantly reduce the energy load on high-pressure pumps, lowering operational costs and improving sustainability profiles. Countries with high solar and wind energy potential, such as Morocco and Australia, are advancing hybrid desalination facilities that pair renewable generation with optimized pump operations, reducing dependence on conventional grid electricity. Furthermore, the integration of smart control systems to synchronize pump operations with renewable energy availability allows desalination plants to enhance efficiency and environmental compliance while supporting global decarbonization goals.

Maintenance complexities in harsh saline environments represent a critical challenge for the Seawater Desalination Pump Market. Pumps operating in seawater desalination systems face constant exposure to high salinity, resulting in corrosion, biofouling, and abrasive wear on critical components such as impellers and seals. These conditions increase the frequency of maintenance interventions, leading to unplanned downtimes and operational inefficiencies across desalination facilities. The need for specialized coatings, corrosion-resistant alloys, and advanced mechanical seals to withstand such harsh conditions raises procurement and maintenance costs. Additionally, remote desalination facilities face logistical challenges in accessing skilled technicians and spare parts, further complicating routine maintenance schedules and impacting operational continuity within the Seawater Desalination Pump Market.

• Rise in Modular and Prefabricated Construction: Modular and prefabricated desalination systems are driving a shift in the Seawater Desalination Pump market, enabling rapid deployment and scalability of desalination facilities across coastal regions. Pump manufacturers are aligning with this trend by supplying skid-mounted, pre-tested high-pressure pump units that can be installed with reduced on-site labor and commissioning time, aligning with the need for urgent water solutions in the Middle East and North Africa. This approach significantly reduces civil works costs and minimizes downtime during installation.

• Integration of Energy Recovery Devices: The increasing use of energy recovery devices within desalination facilities is shaping the demand for pumps capable of seamless integration with these systems. Pressure exchangers and isobaric chambers are now installed in over 60% of newly commissioned RO desalination plants, reducing the energy load on high-pressure pumps by up to 40%. This trend is pushing pump manufacturers to innovate in terms of precision pressure control, anti-cavitation designs, and compatible material usage to align with energy-efficient desalination processes.

• Adoption of Advanced Corrosion-Resistant Materials: There is a growing emphasis on utilizing duplex and super duplex stainless steel, as well as titanium alloy components, in high-pressure seawater pumps to withstand saline environments and extend operational lifespan. This trend is particularly noticeable in offshore and coastal plants in Southeast Asia, where aggressive salinity and biofouling conditions require durable pump components to reduce maintenance frequency and improve system reliability, ensuring stable freshwater production.

• Smart Monitoring and Predictive Maintenance Integration: The Seawater Desalination Pump market is witnessing rapid implementation of IoT-enabled sensors for real-time monitoring and AI-driven predictive maintenance systems within pump assemblies. Facilities adopting these technologies have reported up to a 15% reduction in unscheduled downtime due to early detection of vibration anomalies and seal failures. This trend is aligning with the broader digital transformation of water treatment operations, enhancing operational continuity and cost-effectiveness across desalination plants globally.

The Seawater Desalination Pump market segmentation encompasses a detailed analysis across types, applications, and end-user industries, reflecting evolving project demands and operational requirements in desalination systems. Type-based segmentation reveals a diverse landscape including centrifugal pumps, positive displacement pumps, and axial flow pumps catering to varying capacity needs and process requirements. In terms of application, the market serves high-pressure reverse osmosis systems, seawater intake, brine recirculation, and post-treatment distribution. End-user segmentation indicates strong demand from municipal water utilities, followed by industrial sectors such as oil and gas, power generation, and hospitality industries operating in coastal environments. The segmentation framework provides stakeholders and analysts with structured insights for strategic decisions in capacity planning, procurement, and system upgrades within desalination operations globally.

Centrifugal pumps lead the Seawater Desalination Pump market, driven by their suitability for high-capacity, continuous operations required in reverse osmosis desalination systems. These pumps are widely adopted in municipal desalination facilities for their efficiency in handling large water volumes under high pressure, while maintaining lower operational complexity. Positive displacement pumps are emerging as the fastest-growing segment due to their capability to handle varying flow rates with high precision in brine recirculation and chemical dosing applications, especially within modular desalination units and pilot-scale systems. Axial flow pumps, though niche, maintain relevance in seawater intake systems and low-head, high-flow scenarios, ensuring operational flexibility for large-scale coastal desalination facilities. The diversity in type-based segmentation underscores the critical role of matching pump selection with specific operational demands and water quality management needs in desalination facilities.

Reverse osmosis high-pressure feedwater systems represent the leading application in the Seawater Desalination Pump market, reflecting the widespread adoption of RO technology globally due to its operational efficiency and lower energy requirements compared to thermal methods. The fastest-growing application is in seawater intake and pre-treatment systems, where increasing project developments across coastal regions necessitate reliable intake pumping to manage varying tidal and salinity conditions effectively. Brine recirculation and disposal applications are also gaining traction, driven by regulatory compliance needs for managing brine discharge while minimizing environmental impacts. Post-treatment and freshwater distribution within integrated desalination facilities also form a critical application area, ensuring treated water delivery to municipal or industrial networks while maintaining system pressure and quality standards. The evolving application landscape reflects a need for versatile, efficient, and durable pumping solutions in desalination facilities worldwide.

Municipal water utilities remain the dominant end-user segment in the Seawater Desalination Pump market, attributed to the growing implementation of large-scale desalination facilities to address urban water scarcity across the Middle East, Africa, and parts of Asia-Pacific. The fastest-growing end-user segment is the industrial sector, particularly within oil and gas refineries and power generation facilities in coastal areas, driven by the need for process water and utility water independence to support continuous operations. The hospitality industry, including coastal resorts and island developments, is also utilizing compact desalination systems with integrated high-pressure pumps to secure sustainable water supply in remote regions. Additionally, private infrastructure operators involved in building and managing modular desalination units for community-level water supply projects are contributing to the market’s expansion, reflecting the versatility and critical role of high-performance pump systems in diverse end-user applications across the seawater desalination landscape.

Middle East & Africa accounted for the largest market share at 36.2% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 4.1% between 2025 and 2032.

The Seawater Desalination Pump Market across the Middle East & Africa is driven by large-scale desalination projects to support municipal water supply and industrial operations across Saudi Arabia, UAE, and Oman, with a strong focus on integrating high-capacity pump systems within reverse osmosis plants and hybrid renewable desalination projects. Asia-Pacific’s growth is fueled by rising investments in India, China, and Southeast Asia, where expanding coastal urbanization and manufacturing clusters require stable freshwater supplies, boosting advanced pump system deployment in desalination facilities while aligning with regional water sustainability goals.

Smart Pump Integration Driving Sustainable Water Solutions

North America holds a 19.4% market share in the Seawater Desalination Pump Market, with demand fueled by the increasing adoption of desalination systems in coastal states facing persistent drought conditions, including California and Texas. Key industries driving this demand include municipal water utilities, offshore oil and gas facilities, and coastal industrial clusters seeking secure water sources. Notable regulatory support, such as funding incentives for water infrastructure modernization and desalination pilot projects, is aiding project developments. Technological advancements in the region include the integration of IoT-enabled pump monitoring systems and energy recovery solutions to reduce energy consumption in high-pressure pumps, while digital transformation initiatives support predictive maintenance and optimized operational scheduling in desalination plants.

Advanced Pump Technologies Supporting Circular Water Management

Europe accounts for an 11.8% share of the Seawater Desalination Pump Market, led by key markets including Spain, Italy, and the United Kingdom, which are expanding desalination capacity to address seasonal water shortages. Regulatory bodies across the EU are pushing for sustainable water management and low-carbon desalination operations, prompting investments in high-efficiency pumps with low energy consumption profiles. Sustainability initiatives under the European Green Deal are encouraging advanced pump technology integration, including high-alloy corrosion-resistant materials and modular skid-mounted pumps for rapid project deployment. Adoption of emerging technologies such as smart monitoring systems, energy recovery devices, and predictive maintenance platforms is gaining momentum across desalination facilities, ensuring efficient water production with reduced operational costs.

High-Volume Desalination Infrastructure Fueling Pump Market Expansion

Asia-Pacific ranks highest in volume consumption within the Seawater Desalination Pump Market, driven by significant investments in China, India, and Japan to expand freshwater production capacity amid rising coastal urbanization. China and India, in particular, are leading large-scale desalination infrastructure projects to address regional water scarcity, while Japan is focusing on modernizing its coastal desalination facilities with advanced pump systems. The region is witnessing trends in modular and mobile desalination plant deployments, supported by local manufacturing advancements in high-pressure, corrosion-resistant pump systems. Regional tech hubs across Singapore and South Korea are advancing IoT integration and AI-driven monitoring solutions within desalination plants, ensuring operational efficiency and optimized water production in large-capacity facilities across coastal industrial corridors.

Emerging Water Infrastructure Investments Driving Pump Market Growth

In South America, Brazil and Chile are the key contributors within the Seawater Desalination Pump Market, with the region holding a 7.3% share in 2024. Brazil is advancing desalination capacity along its northeastern coast to support urban and industrial water demands, while Chile is deploying desalination facilities to sustain its mining sector operations in arid zones. The region is seeing growing interest in integrating renewable-powered desalination systems, which drives the need for energy-efficient pump technologies compatible with variable power inputs. Infrastructure developments supported by government incentives and regional trade agreements are fostering desalination project expansion, aligning with efforts to mitigate water stress across urban centers and industrial hubs in coastal South American regions.

Mega Desalination Projects Accelerating Market Demand

The Middle East & Africa region demonstrates strong demand across the Seawater Desalination Pump Market, led by countries such as Saudi Arabia, UAE, and South Africa. In 2024, the region accounted for a commanding 36.2% share, driven by continuous investment in large-scale desalination plants to ensure water security for municipal and industrial applications. The oil and gas and construction sectors are major drivers of pump demand, requiring advanced pump systems for stable water supply and process cooling. Technological modernization trends include the adoption of high-capacity pumps with integrated energy recovery systems, digital twin technologies for monitoring, and AI-based predictive maintenance systems to enhance reliability. Local regulations supporting water sustainability and regional trade partnerships for advanced pump technologies are further fueling market expansion.

Saudi Arabia – 21.7% market share

High production capacity in large-scale desalination facilities and continuous investments in pump infrastructure.

China – 14.9% market share

Strong end-user demand for industrial and municipal desalination supporting expansion of high-capacity pump deployment.

The Seawater Desalination Pump market features a moderately fragmented competitive environment with over 45 active global and regional players delivering high-pressure, energy-efficient pump systems tailored for desalination operations. Key competitors are strategically positioning themselves through targeted product launches of corrosion-resistant, low-maintenance pump solutions for reverse osmosis and multi-stage flash desalination plants. The market is witnessing partnerships between pump manufacturers and desalination EPC contractors to integrate advanced pumping solutions with energy recovery systems and smart monitoring technologies within turnkey desalination projects.

Mergers and acquisitions are shaping competition as manufacturers seek to expand geographic reach and strengthen technology portfolios in high-growth regions, particularly the Middle East, Asia-Pacific, and coastal North America. Innovation trends influencing competition include the integration of IoT-based predictive maintenance systems and digital twins, enabling operators to enhance efficiency and extend pump lifespan. Companies are increasingly focusing on manufacturing pumps with duplex and super duplex stainless steel materials to address harsh saline conditions while maintaining operational reliability. Additionally, competitive differentiation is driven by the ability to deliver modular, skid-mounted pump systems supporting fast-track desalination plant deployments for municipal and industrial water supply projects.

Grundfos

Sulzer Ltd.

Torishima Pump Mfg. Co., Ltd.

KSB SE & Co. KGaA

Flowserve Corporation

Ebara Corporation

Wilo SE

SPX FLOW, Inc.

DESMI A/S

Ruhrpumpen Group

Technological advancements in the Seawater Desalination Pump market are focusing on energy efficiency, durability, and digital integration to meet the operational demands of high-capacity desalination facilities. Advanced high-pressure pumps designed with duplex and super duplex stainless steel and titanium alloys are increasingly used to handle corrosive saline environments while minimizing maintenance needs. Energy recovery integration is becoming standard, with over 65% of new reverse osmosis desalination facilities incorporating pressure exchanger technologies that reduce pump power requirements by up to 40%. Variable frequency drive (VFD) integration within pump systems is optimizing flow and pressure control, allowing for precise adjustments based on salinity and intake fluctuations, while reducing operational stress and extending pump life.

Smart monitoring and IoT-enabled predictive maintenance are transforming operational practices across desalination plants, with sensors monitoring vibration, temperature, and pressure to identify potential failures before unplanned downtimes occur. Digital twin technology is being implemented within large-scale desalination facilities, allowing simulation of pump performance under varying conditions to optimize maintenance and operational schedules. Furthermore, modular pump skid systems are gaining traction for fast-track desalination projects, allowing plug-and-play installation, reducing civil work costs, and enabling scalable capacity additions. These emerging technologies align with sustainability targets by reducing energy consumption, improving operational efficiency, and supporting the resilience of desalination plants in coastal and offshore environments.

• In February 2023, Grundfos launched its CR 255 high-pressure pump designed for large-scale desalination plants, featuring a 500 cubic meters per hour capacity with a 30% smaller footprint, addressing operational space limitations in modular desalination facilities.

• In May 2023, Torishima commissioned high-pressure pumps for a new reverse osmosis plant in Oman, increasing freshwater production capacity by 120,000 cubic meters per day while integrating energy recovery devices to reduce energy consumption by 32%.

• In March 2024, Sulzer introduced its latest energy-efficient axial flow pump for seawater intake, optimized for low NPSH and improved anti-corrosion coating, extending operational life by 25% in harsh saline environments and reducing lifecycle maintenance costs.

• In June 2024, Ebara delivered a smart monitoring system integrated with high-capacity pumps to a desalination facility in India, enabling real-time vibration and temperature monitoring and reducing unplanned pump downtime by 18% through predictive analytics.

The Seawater Desalination Pump Market Report comprehensively analyzes the evolving landscape of high-pressure and seawater intake pump systems used in desalination processes across municipal, industrial, and offshore sectors. The report covers pump types, including centrifugal, axial flow, and positive displacement pumps, highlighting their operational roles within reverse osmosis, multi-stage flash, and hybrid desalination systems. It includes insights into technological innovations, such as energy recovery integration, IoT-enabled monitoring, predictive maintenance, and modular skid-mounted pump systems, reflecting the market’s transition toward energy-efficient and sustainable desalination operations.

Geographically, the report covers key regions including the Middle East & Africa, Asia-Pacific, North America, Europe, and South America, analyzing trends in infrastructure investments, water security initiatives, and pump deployment patterns across high-growth countries such as Saudi Arabia, China, India, and Brazil. The report evaluates the market’s alignment with environmental regulations and sustainability objectives, emphasizing the adoption of advanced materials and digital transformation within desalination projects. It also covers emerging niche market segments, including renewable-powered desalination systems and offshore modular desalination units, offering stakeholders clear insights for capacity planning, procurement strategy, and investment decisions in the seawater desalination sector while supporting long-term water sustainability goals.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 334.11 Million |

|

Market Revenue in 2032 |

USD 443.37 Million |

|

CAGR (2025 - 2032) |

3.6% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Grundfos, Sulzer Ltd., Torishima Pump Mfg. Co., Ltd., KSB SE & Co. KGaA, Flowserve Corporation, Ebara Corporation, Wilo SE, SPX FLOW, Inc., DESMI A/S, Ruhrpumpen Group |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |