Reports

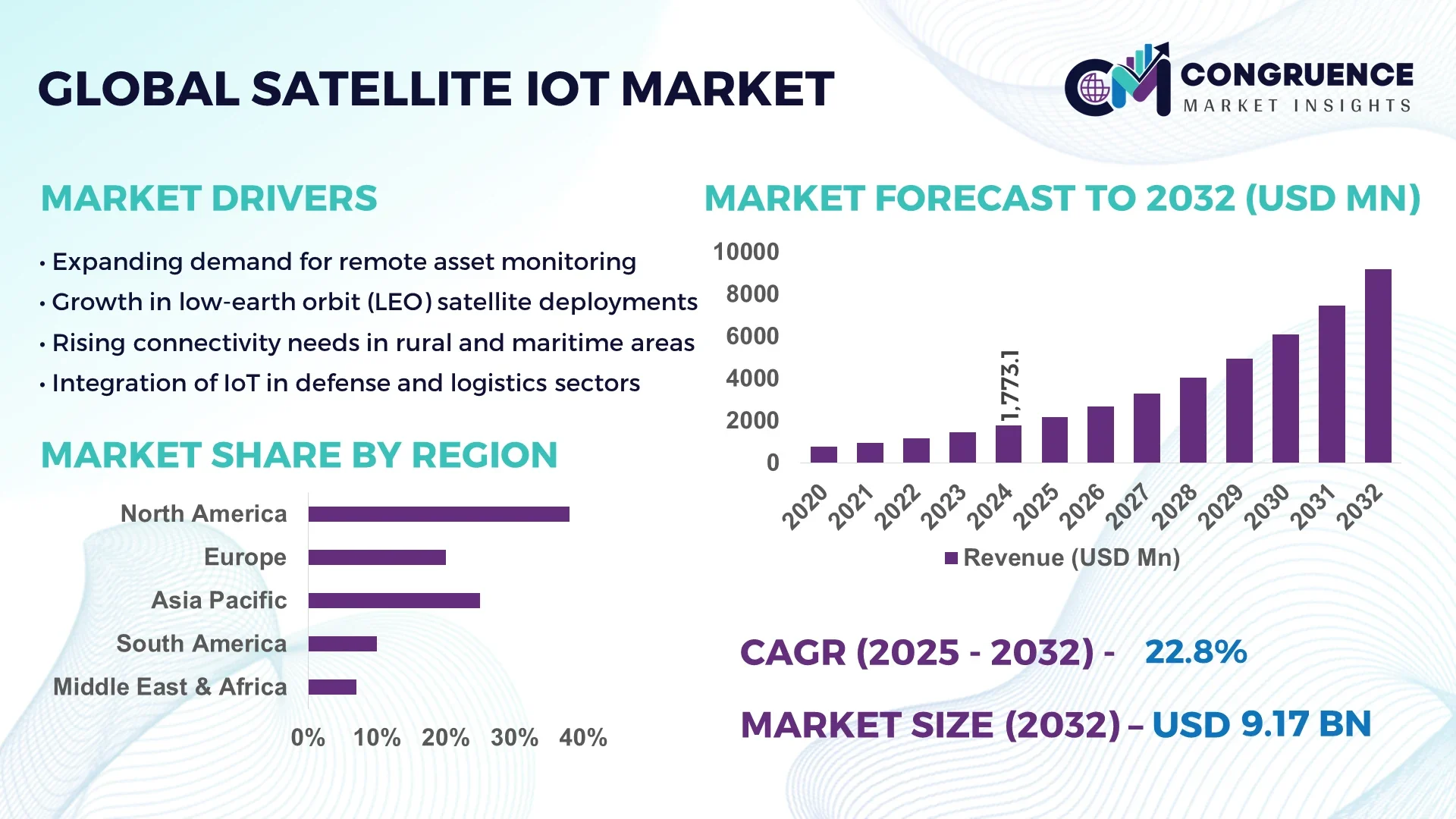

The Global Satellite IoT Market was valued at USD 1773.08 Million in 2024 and is anticipated to reach a value of USD 9168.89 Million by 2032, expanding at a CAGR of 22.8% between 2025 and 2032. This expansion is primarily driven by increasing demand for uninterrupted connectivity across remote industrial zones and geographically challenging regions beyond terrestrial network coverage.

The United States dominates the Satellite IoT landscape with extensive investments in low Earth orbit (LEO) satellite constellations and IoT infrastructure integration. In 2024, the country accounted for more than 7.5 million global satellite IoT connections, supported by strong involvement from aerospace, defense, logistics, and agricultural industries. Major U.S. firms are advancing narrowband satellite IoT (NB-IoT) and 5G non-terrestrial network (NTN) technologies, achieving over 20% efficiency gains in remote asset monitoring and fleet management applications. Additionally, government-backed initiatives are promoting the deployment of hybrid satellite-terrestrial IoT systems to enhance data coverage and reliability across nationwide operations.

Market Size & Growth: Valued at USD 1.77 billion in 2024 and projected to reach USD 9.16 billion by 2032, expanding at a CAGR of 22.8%, driven by rapid IoT integration across remote connectivity applications.

Top Growth Drivers: Technological cost reduction (~30%), expansion of hybrid terrestrial-satellite networks (~25%), and increased adoption for remote asset tracking (~35%).

Short-Term Forecast: By 2028, satellite IoT connectivity costs expected to drop by ~18%, with device performance improving by ~22%.

Emerging Technologies: Integration of 5G NTN frameworks, hybrid LEO-GEO constellations, and AI-enabled ground processing and edge computing.

Regional Leaders: North America projected at USD 3.5 billion by 2032 (strong aerospace innovation); Asia-Pacific at USD 2.8 billion by 2032 (rural broadband expansion); Europe at USD 1.6 billion by 2032 (smart infrastructure and industrial automation).

Consumer/End-User Trends: High adoption in logistics and fleet tracking (24%), agriculture and remote monitoring (19%), and utilities (18%), driven by demand for reliable global communication.

Pilot or Case Example: In 2025, a global maritime logistics pilot using satellite IoT reduced container loss incidents by 17% and improved route visibility by 12%.

Competitive Landscape: Leading player holds ~28% market share; key participants include Iridium Communications, Inmarsat, Globalstar, Astrocast, and OQ Technology.

Regulatory & ESG Impact: NTN spectrum regulation and ESG-driven environmental monitoring initiatives support sustainable adoption and operational transparency.

Investment & Funding Patterns: Over USD 1 billion invested globally in the past 18 months, emphasizing venture capital, project finance, and satellite-as-a-service models.

Innovation & Future Outlook: Advancements in nanosatellite deployment, edge-AI analytics, and integrated data networks are shaping future satellite IoT scalability and global accessibility.

The Satellite IoT market is witnessing strong adoption across industrial sectors such as transportation, energy, maritime, and agriculture, each contributing substantially to device connectivity growth. Recent product innovations—like miniaturized LEO satellites, low-power IoT modems, and AI-driven telemetry systems—are transforming operational efficiency and data transmission capabilities. Regulatory incentives promoting NTN infrastructure, coupled with sustainability initiatives for environmental monitoring, are driving further market expansion. Rising demand from developing regions, advancing hybrid satellite-terrestrial ecosystems, and continuous innovation in data analytics collectively define the industry’s forward momentum and future growth trajectory.

The strategic relevance of the Satellite IoT Market lies in its capacity to deliver global connectivity in areas where terrestrial networks are insufficient, thereby enabling mission-critical monitoring and automation across industries. For instance, hybrid LEO satellite systems deliver up to 35% improvement in latency and coverage compared to legacy geostationary IoT links. North America dominates in volume of deployments, while Asia-Pacific leads in adoption with over 40% of enterprises integrating Satellite IoT solutions into remote operations by 2024. By 2027, the integration of AI-enabled edge analytics is expected to improve asset downtime detection by 22%. Leading firms are committing to ESG targets such as a 15% reduction in carbon-emissions from remote asset travel by 2028 through satellite-enabled remote monitoring. In one micro-scenario, in 2025 a major oil and gas operator in Brazil achieved a 17% reduction in unscheduled maintenance events by deploying narrowband Satellite IoT sensors across remote pipelines. Looking ahead, the Satellite IoT Market is poised to serve as a pillar of resilience, compliance, and sustainable growth for global enterprises navigating connectivity, regulatory and environmental demands.

The deployment of LEO and hybrid satellite-terrestrial networks is accelerating Satellite IoT growth by providing substantially improved latency and expanded geographic reach. According to industry data, deployment of hybrid connectivity frameworks has enabled global Satellite IoT network operators to reach over 7.5 million active devices by 2024. This capability allows enterprises to monitor assets in remote, underserved regions where cellular connectivity is absent. The integration of narrowband IoT protocols over satellite further reduces power and cost requirements for endpoint devices. As a result, logistics firms, agricultural operations and energy asset owners can deploy satellite-connected sensors affordably and at scale, unlocking operational visibility and efficiency that were previously unavailable.

High infrastructure costs and deployment complexity remain major restraints on Satellite IoT adoption. Launching, maintaining and operating satellite constellations—particularly in LEO/MEO environments—requires substantial capital investment and operational expertise. Some reports note initial deployment costs can exceed several million USD per satellite cluster. Further, regulatory requirements for spectrum licensing and clearance for non-terrestrial network operations add administrative burden and time to market. These factors limit participation to well-capitalised providers, slowing broader ecosystem entry and delaying adoption in certain regions. Enterprises may still perceive service cost premiums compared to terrestrial alternatives, which can dampen uptake in price-sensitive segments.

Expansion into emerging market geographies presents significant opportunities for the Satellite IoT market. Regions such as Sub-Saharan Africa, Latin America and parts of Southeast Asia remain underserved by terrestrial networks, creating openings for satellite-enabled connectivity solutions. With modular, low-power IoT sensors now supported by Satellite IoT platforms, industries like mining, forestry, agriculture and disaster-response are prime candidates for adoption. Additionally, the convergence of IoT with satellite platforms opens doors to new services such as remote-environment monitoring, wildlife tracking, and off-grid smart infrastructure, enabling service providers to extend revenue models beyond conventional enterprise telemetry. As device and access-service costs drop, previously inaccessible segments are becoming commercially viable.

Regulatory fragmentation and endpoint device standardisation present major challenges for the Satellite IoT market. Varying national regulations for spectrum allocation, space-licensing and non-terrestrial network integration create complexity for global deployments, adding cost and risk for providers. Meanwhile, many Satellite IoT solutions lack consistent global standards for IoT modules, connectivity protocols and cross-network interoperability. Industry analysis reveals that legacy satellite module technology held approximately 98% share in 2024, but is expected to fall to 49% by 2030 due to the adoption of 3GPP-based NTN protocols—a transition that requires ecosystem investment and coordination. Until standardisation matures, device fragmentation and integration complexity may slow enterprise adoption.

• Expansion of Direct-to-Device Connectivity with Advanced LEO Systems: The Satellite IoT industry is experiencing a measurable surge in direct-to-device connectivity as advanced Low Earth Orbit (LEO) satellite systems gain traction. These networks deliver approximately 45% lower latency than traditional geostationary satellites, enabling faster data transmission and near-real-time communication. By 2024, direct-to-device services accounted for nearly 64% of all Satellite IoT applications, supporting more than 7.5 million active connections. The adoption of compact terminals and low-power modems is facilitating deployment across logistics, energy, and environmental monitoring, particularly in remote and maritime sectors.

• Acceleration in 3GPP-Based NTN Module Adoption: The transition from legacy satellite modules to 3GPP-compliant Non-Terrestrial Network (NTN) modules is transforming interoperability and integration efficiency. In 2024, legacy modules represented about 98% of total shipments, yet the share of standardized NTN modules is expected to surpass 50% by 2026. This trend is driving large-scale device deployments across industries such as agriculture, utilities, and logistics, with over 10 million connected IoT devices anticipated in global circulation by 2025. The shift is resulting in approximately 25% lower integration costs and improved device compatibility across satellite and terrestrial networks.

• Rise of Non-Traditional Industrial Adopters and Smart Infrastructure Applications: Non-traditional sectors like maritime, agriculture, and smart cities are emerging as key growth frontiers for Satellite IoT. In 2024, maritime tracking and shipping operations accounted for 34.5% of total market use, while agricultural monitoring and environmental sensing collectively grew at over 20% annually. These industries are achieving measurable gains such as 20% improvement in asset visibility and 15% reduction in logistics downtime through IoT-enabled satellite telemetry. The diversification of adoption sectors is expanding the functional reach of Satellite IoT beyond traditional aerospace and defense domains.

• Hybrid Connectivity Ecosystems Enhancing Cost Efficiency and Accessibility: Hybrid satellite-terrestrial connectivity is reshaping network economics within the Satellite IoT market. The integration of dual-mode communication models has lowered the average cost per connection by nearly 30% compared to standalone satellite systems. Concurrently, satellite launch costs have declined below USD 5,000 per kilogram, fostering rapid expansion among small and medium satellite operators. The number of active commercial operators surpassed 100 globally in 2024, increasing innovation velocity and accessibility. These hybrid frameworks are accelerating the convergence of IoT, AI, and cloud analytics, driving scalable, cost-efficient satellite IoT ecosystems worldwide.

The segmentation of the Satellite IoT market encompasses three primary dimensions: type, application, and end-user. On the type front, the market includes direct-to-satellite, satellite backhaul, and hybrid service models—each addressing distinct operational and connectivity needs. Application-wise, sectors such as transportation and logistics, energy and utilities, maritime and shipping, oil and gas, agriculture, and environmental monitoring drive differentiated demand patterns. End-user segmentation covers large enterprises, small and medium enterprises (SMEs), government organizations, and sector-specific operators with varying adoption levels, investment scales, and technical integration strategies. Understanding these segmentation insights allows industry stakeholders to align their investments and R&D efforts with evolving technology standards and market demand patterns.

Within the Satellite IoT market, the leading product type is direct-to-satellite connectivity, which holds approximately 55.3% share across global deployments. This category’s dominance stems from its ability to support device communication directly via satellite without requiring terrestrial infrastructure—making it ideal for remote and infrastructure-deficient regions. The fastest-growing segment is hybrid satellite-backhaul solutions, driven by the integration of terrestrial 5G and low Earth orbit (LEO) satellite networks that enhance speed and reliability. Narrowband satellite IoT modules, multi-orbit service models, and backhaul systems together represent about 44.7% of the market, catering to specialized uses such as high-throughput telemetry and ultra-low-power sensing.

Transportation and logistics form the leading application segment of the Satellite IoT market, accounting for around 41.2% of the connected device base. The segment’s strength arises from its growing requirement for continuous tracking and supply-chain visibility, especially across remote maritime and land transport routes. The fastest-growing application segment is agriculture and forestry, which is expanding at over 20% annually as satellite-linked sensors enable precise soil, weather, and crop monitoring. Other applications—including maritime navigation, oil and gas exploration, and environmental monitoring—collectively represent about 38.8% of deployments. Each of these verticals contributes to global asset visibility and resource optimization.

Large enterprises currently dominate the end-user segment of the Satellite IoT market with an estimated 62.7% share in 2025, reflecting their capacity for large-scale system integration and cross-border operational networks. The fastest-growing segment is SMEs within agriculture, logistics, and utilities, expanding at double-digit annual rates due to declining module prices and improved interoperability. Government agencies and startups collectively contribute about 37.3% of the market, with rising adoption in areas such as defense communication, smart infrastructure, and environmental surveillance. Within logistics, enterprise adoption rates exceed 24%, while agriculture and energy sectors record adoption around 19% globally.

North America accounted for the largest market share at 38% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of approximately 25% between 2025 and 2032.

North America’s leading position is underpinned by its approximately 38% regional share in 2024, strong aerospace/space infrastructure, and widespread industrial IoT deployment across sectors such as transportation, energy, logistics and defence. By contrast, Asia-Pacific’s growth is driven by emerging economies such as China, India and Japan which together represent a vast untapped base, rapid infrastructure build-out, and deployment of more than 680 small satellites between 2023 and 2025 to support IoT connectivity across agriculture, logistics and rural markets. Europe maintained about 28% share in 2024, supported by regulatory and smart-infrastructure investment, while Latin America and Middle East & Africa together held the remainder of the market, reflecting slower adoption but significant upside in remote asset monitoring and connectivity expansion.

Is the advanced infrastructure ecosystem propelling high enterprise adoption?

In North America the Satellite IoT market holds roughly 38% of global share in 2024. Demand is led by industries such as oil & gas, transportation & fleet logistics, utilities and defence. Regulatory changes in the US and Canada — for example spectrum licensing reforms for non-terrestrial networks and government grants for rural broadband satellite initiatives — are accelerating deployment. Technological advances include integration of 5G NTN standards with satellite IoT platforms and edge computing at remote sites. One local player, Iridium Communications, is deploying LEO satellite-based IoT services tailored for maritime and energy-sector clients, enabling global tracking of remote assets. In terms of consumer behaviour, enterprises in healthcare and finance are adopting satellite-IoT modules less than heavy industry but show growing interest in hybrid satellite-terrestrial solutions for redundancy and compliance.

How are regulatory frameworks and sustainability mandates shaping adoption?

In Europe the Satellite IoT market represents approximately 28% share in 2024. Key country markets include Germany, the United Kingdom and France which are embracing satellite-enabled smart infrastructure, energy-grid monitoring and cross-border logistics tracking. Regulatory bodies and sustainability initiatives — such as requirement for environmental-monitoring data and digital-sovereignty mandates — are driving uptake of Satellite IoT solutions. Technological adoption in Europe includes advanced telemetry, AI analytics on satellite-collected data, and IoT-satellite integration for smart-cities. A European operator like Eutelsat S.A. is expanding its IoT-satellite services in cooperation with local utilities. Consumer behaviour in Europe is shaped by regulation-driven demand for explainable connectivity and secure IoT, rather than purely cost-driven deployments.

Why is this region becoming the fastest-growing Satellite IoT hotspot?

In Asia-Pacific the Satellite IoT market volume in 2024 is pegged at approximately 22% of global share, with China, India and Japan as top consuming countries. Manufacturing and infrastructure trends include mass deployment of small satellites, large scale IoT sensor rollout in agriculture and smart logistics corridors, and local production of satellite-IoT hardware. Tech-innovation hubs in China and India are focusing on low-power satellite IoT modules, rural connectivity systems and hybrid terrestrial-satellite networks. A local player such as Planet Labs (which signed a USD 230 million satellite deal for an Asian customer) exemplifies regional investment in satellite capacity and IoT infrastructure. In terms of consumer behaviour, adoption is propelled by e-commerce logistics, mobile AI-driven applications and rapid rural IoT sensor rollout rather than just enterprise legacy upgrades.

What growth levers exist in Latin-America’s Satellite IoT segment?

In South America, key countries such as Brazil and Argentina are advancing Satellite IoT deployment primarily in mining, agriculture and energy infrastructure. The regional market share is modest but growing; for example Latin America is estimated at around 7% share in 2024. Infrastructure trends include remote-asset monitoring in large mines, off-grid agriculture sites and logistics hubs in remote geography. Government incentives and trade policies supporting connectivity in underserved zones are fostering Satellite IoT adoption. A local player is partnering with satellite operators to deliver container-tracking and cold-chain monitoring in Brazilian ports. Consumer behaviour in this region reflects demand tied to media localisation, language-specific IoT interfaces, and integration of connectivity in agriculture and supply-chain solutions rather than purely industrial automation.

How are energy-rich and remote-infrastructure regions adopting Satellite IoT?

In the Middle East & Africa region the Satellite IoT market is driven by oil & gas, mining, construction and large-scale infrastructure renewal projects. Major growth countries include the UAE and South Africa which are modernising communications and deploying satellite-enabled IoT for remote field monitoring and logistics support. The region holds about 13% of global Satellite IoT market activity in 2024. Technological modernization trends include integration of satellite IoT with smart-grid and solar-farm networks and national IoT-satellite partnerships. Regulatory frameworks and trade partnerships are evolving to enable foreign satellite payload launches and local data-processing centres. Consumer behaviour varies: enterprises prioritise ruggedised sensor networks and multilingual support, and governments emphasise connectivity for remote asset management and disaster resilience rather than just consumer IoT.

United States – approximately 38% of global share; dominance due to advanced production capacity, strong end-user demand and regulatory support.

China – approximately 22% share; driven by large-scale investments in satellite infrastructure, massive rural-IoT roll-out and rapid manufacturing of satellite-IoT modules.

The global Satellite IoT market in 2024 comprises over 45 active competitors spanning satellite operators, IoT module manufacturers, and data analytics providers. The market remains moderately consolidated, with the top five companies—Iridium Communications, Inmarsat, Orbcomm, Globalstar, and Eutelsat—collectively accounting for around 58% of total market share. These leaders dominate through extensive LEO and MEO satellite networks, global connectivity coverage exceeding 90% of inhabited landmass, and established partnerships with telecom operators and IoT service providers. Competitive strategies center on low-cost small satellite launches, integration with 5G NTN networks, and AI-based data management for predictive maintenance and logistics optimization. More than 120 strategic collaborations and 35 satellite constellation expansions were recorded between 2023 and 2024, reflecting rapid investment in capacity and low-latency services. Innovation is increasingly shaped by hybrid satellite–terrestrial architectures, spectrum-sharing frameworks, and open IoT platforms allowing interoperability across devices and regions. The entry of new players from Asia and private space technology startups has intensified competition, while established Western operators are focusing on network densification and service differentiation through analytics, cybersecurity, and device miniaturization.

Globalstar Inc.

Eutelsat S.A.

Thuraya Telecommunications Company

SES S.A.

Astrocast SA

Swarm Technologies

Kepler Communications Inc.

Myriota Pty Ltd.

Kineis

Fleet Space Technologies Pty Ltd.

Lacuna Space

OQ Technology S.A.

The Satellite IoT market is undergoing a rapid technological transformation driven by advancements in low-earth orbit (LEO) constellations, 5G non-terrestrial networks (NTN), and miniaturized sensor systems. As of 2024, over 4,200 active IoT-enabled satellites are operational globally, with more than 65% operating in LEO to deliver enhanced latency below 50 milliseconds. The integration of 5G NTN architecture enables continuous connectivity across maritime, aviation, and remote industrial sectors, facilitating data rates exceeding 150 Mbps and expanding real-time monitoring capabilities across previously unreachable geographies.

Software-defined satellites (SDS) and edge-computing payloads are reshaping in-orbit data management, reducing data relay latency by up to 35%. Artificial intelligence is increasingly integrated into satellite data analytics for predictive maintenance, environmental monitoring, and fleet optimization, with more than 40% of commercial operators deploying AI-assisted ground control systems. Cloud-native ground stations further enhance scalability and lower operational costs by automating data routing between satellite and terrestrial networks.

Emerging technologies such as quantum communication links, multi-orbit interoperability, and IoT sensor miniaturization below 10 mm are setting new standards in secure, energy-efficient communication. Moreover, advancements in nanosatellite production—expected to surpass 1,800 annual launches by 2026—are accelerating the transition toward cost-efficient, scalable constellations. Collectively, these innovations position the Satellite IoT ecosystem as a critical infrastructure for global connectivity, data intelligence, and industrial automation in the coming decade.

In January 2024, Iridium Communications Inc. unveiled “Project Stardust,” its new standards-based NB-IoT and 5G NTN offering designed to support direct satellite connections for smartphones, tablets and cars. The initiative builds on Iridium’s global LEO constellation and ecosystem of about 500 partners.

In December 2024, Iridium launched the Iridium Certus 9704 IoT module and accompanying development kit, which is 34% smaller than its previous 9603 platform, reduces idle power consumption by 83%, and supports larger file-transfer sizes and two-way messaging for industrial IoT and remote asset applications.

In April 2023, Inmarsat Global Limited and MediaTek Inc. announced a partnership to bring two-way satellite services into smartphones and IoT devices, enabling bidirectional connectivity beyond conventional terrestrial networks for connected cars and smart devices.

In 2024, Globalstar Inc.’s UK partner reported a 35% year-on-year growth in device sales—over 10,800 satellite IoT transmitters were sold in 2024 through the reseller channel—including units for oil & gas pipeline monitoring and remote workers, signalling accelerated device uptake.

The Satellite IoT Market Report offers a comprehensive analysis covering product types (such as direct-to-satellite modules, satellite backhaul systems and hybrid satellite-terrestrial solutions), key applications (transportation & logistics, agriculture & forestry, energy & utilities, maritime, oil & gas and environmental monitoring), and end-user segments (large enterprises, SMEs, government agencies and infrastructure operators). Geographically, the report examines regional markets across North America, Europe, Asia-Pacific, South America and Middle East & Africa, with country-level breakdowns for major players such as the United States, China, India, Germany, Brazil and UAE. Technology focus areas include LEO/MEO satellite constellations, NB-IoT and NTN standards, hybrid connectivity architectures, miniaturised sensor modules and edge-AI integration. The report also investigates emerging and niche sectors such as direct-to-device (D2D) satellite IoT, autonomous asset-tracking platforms in remote landscapes, and environmental-monitoring networks leveraging satellite links. Coverage includes competitive dynamics, regulatory and spectrum-licensing frameworks, ESG and sustainability use-cases, and investment trends in both hardware and service ecosystems. The breadth and depth of the report are designed to support decision-makers and industry professionals in understanding strategic pathways, technology deployment, regional opportunities, risks and segmentation performance to inform market entry, partnership strategies and capital allocation across the satellite IoT landscape.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 1773.08 Million |

Market Revenue in 2032 | USD 9168.89 Million |

CAGR (2025 - 2032) | 22.8% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Iridium Communications Inc., Inmarsat Global Limited, Orbcomm Inc., Globalstar Inc., Eutelsat S.A., Thuraya Telecommunications Company, SES S.A., Astrocast SA, Swarm Technologies, Kepler Communications Inc., Myriota Pty Ltd., Kineis, Fleet Space Technologies Pty Ltd., Lacuna Space, OQ Technology S.A. |

Customization & Pricing | Available on Request (10% Customization is Free) |