Reports

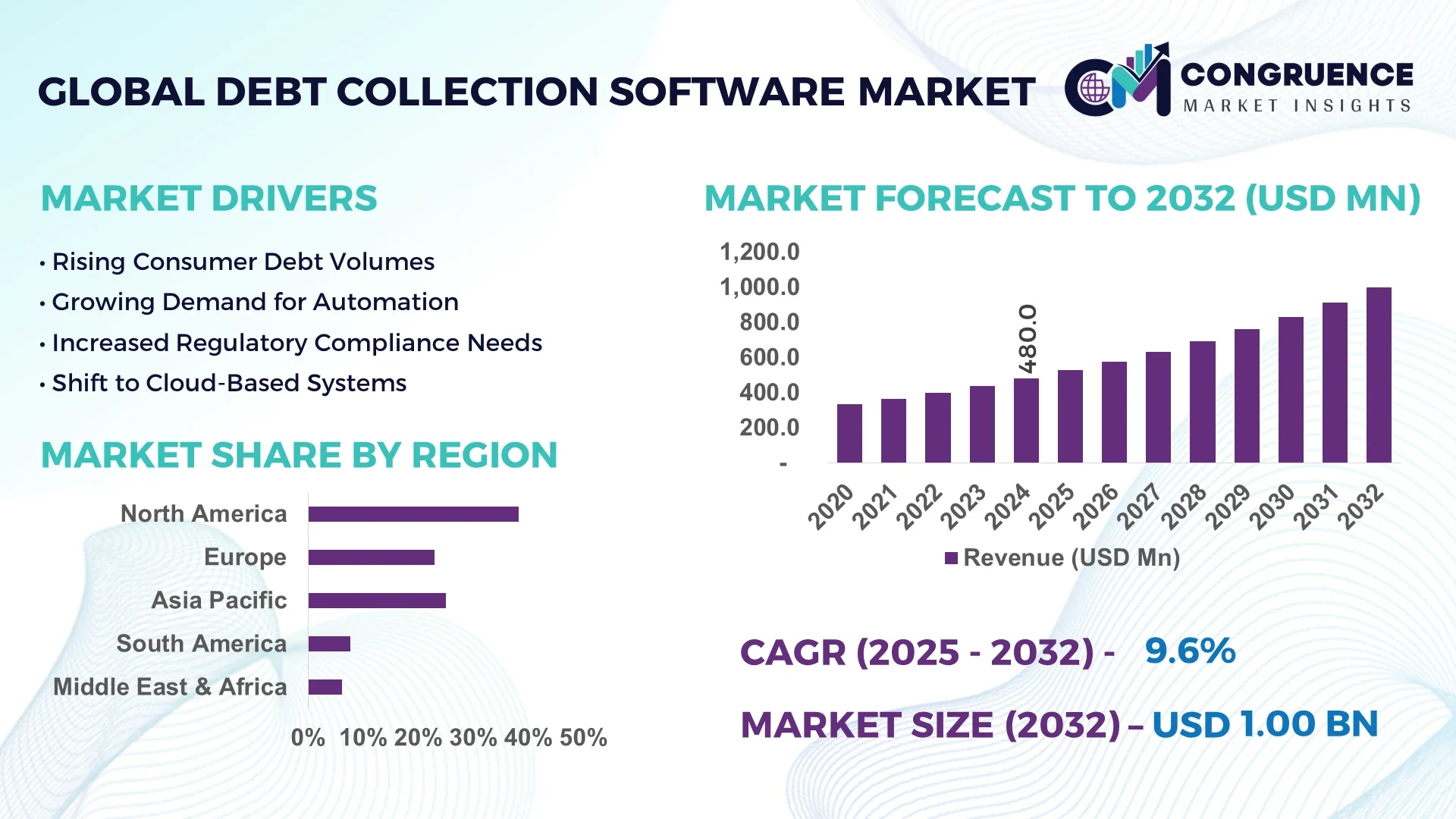

The Global Debt Collection Software Market was valued at USD 480.0 Million in 2024 and is anticipated to reach a value of USD 999.4 Million by 2032 expanding at a CAGR of 9.6% between 2025 and 2032.

The United States leads the Debt Collection Software Market, boasting a robust production ecosystem with over 40 dedicated software developers and third-party integrators. Investments exceed USD 200 million annually in R&D for automation, compliance, and analytics tools. Major industry applications include banking, telecom, and healthcare sectors. Leading providers are piloting next-gen conversational AI and blockchain-enabled audit trails to support secure, high-volume collections compliant with evolving federal data standards.

The Debt Collection Software Market spans diverse industry sectors including BFSI, healthcare, telecom & utilities, government, and SMEs. In 2024, BFSI contributed approximately 31%, followed by healthcare at 18%, and telecom & utilities at 12%. Product innovations include predictive analytics engines capable of analyzing 50+ behavioral variables, generative-AI-driven messaging, and embedded payment portals. Regulatory mandates such as GDPR, HIPAA, and FDCPA continue to drive adoption, encouraging systems to support audit logs and dynamic consent management. Economic pressures like rising NPLs and digital lending expansion reinforce software demand. Regionally, North America and Europe exhibit mature consumption patterns with high cloud deployments, while Asia‑Pacific shows accelerating growth due to fintech adoption. Emerging trends include agentic AI for human‑supervised automation, RPA-assisted data ingestion from invoices, and ethical AI-built compliance workflows. Looking ahead, industry professionals expect modular, API-first platforms enabling seamless integration into core banking and ERP systems, strengthening scalability and reducing onboarding timelines.

AI is fundamentally reshaping the Debt Collection Software Market by introducing sophisticated automation, operational optimization, and debtor-centric engagement. Leading platforms integrate AI modules for account prioritization—leveraging machine learning to rank cases by payment probability—enabling collectors to allocate resources to high-potential accounts. Adoption of natural language processing (NLP) and generative AI fortifies messaging workflows: automated outreach sequences now feature dynamically composed reminders and empathetic call prompts, increasing engagement rates by up to 32% and boosting liquidation success by 40% compared to legacy systems.

Operationally, AI-driven analytics accelerate debt cycles. Real-time decision engines can trigger next-step workflows based on debtor behavior signals—like payment history and interaction responses—cutting days sales outstanding (DSO) by an average of 5 days and delivering an 84% improvement in overall collection efficiency. AI also enhances compliance: rule-based AI layers automatically monitor communication tone and timing, flagging potential regulatory violations before outreach is dispatched. This reduces legal risk and manual audit overhead across diverse jurisdictions.

In addition, AI-powered chatbots and virtual agents handle routine debtor inquiries, freeing collectors to address complex cases. These chatbots leverage contextual learning to answer payment‑due questions, dispute balances, and schedule call-backs—streamlining operations and improving customer experience. Integration with robotic process automation (RPA) ensures seamless data extraction from incoming documents (e.g., invoices, payment confirmations), feeding predictive models without manual input and boosting data quality.

Overall, the incorporation of machine learning, generative AI, and RPA into the Debt Collection Software Market delivers quantifiable improvements in efficiency, compliance, and resource utilization—transforming legacy systems into proactive, scalable platforms capable of meeting increasingly complex collection demands.

“In 2024, HighRadius reported a 96% net recovery rate by applying AI-driven deductions resolution, reducing past‑due invoices by 13% and improving DSO by five days while achieving an 84% uplift in collection efficiency.”

The Debt Collection Software Market Dynamics reflect a complex interaction of evolving technological standards, regulatory imperatives, and shifting industry needs. Industry participants are embracing cloud migration, modular architectures, and API-first frameworks to align with digital transformation strategies. The expansion of fintech, BNPL, and embedded financing has intensified pressure on collection systems to manage consumer credit across fragmented channels. Simultaneously, regulatory bodies worldwide are tightening compliance demands—mandating audit trails, transparent communication, and consumer rights—necessitating software capable of adaptive rule‑management. Economic volatility and escalating delinquency rates are reinforcing debt recovery needs, pushing organisations toward data-driven, scalable solutions. With AI and RPA now core to next-gen offerings, vendors are competing on efficiency metrics such as DSO reduction and recovery rates. Decision-makers must therefore balance innovation, regulatory resilience, and operational scalability as market dynamics continue to push the Debt Collection Software Market into strategic centrality.

Rising use of BNPL, digital lending apps, and embedded finance has significantly increased debt volumes outside traditional banking. For instance, BNPL accounted for 8.6% of Indian e-commerce by 2025, up from 3% in 2021. These systems generate real-time credit accounts with short repayment cycles, requiring integrated, automated tools to track delinquencies, predict repayment patterns, and initiate recovery across channels. Debt collection platforms with built-in analytics and API connectivity now enable recovery teams to manage larger portfolios with minimal manual intervention, directly supporting decision-making frameworks in finance divisions.

CIT systems must adhere to strict regulations like GDPR, HIPAA, FDCPA, and regional data residency laws. Automated outreach must be context-aware to avoid tone violations or illegitimate timing. Mistakes can lead to fines over USD 100,000 per breach or regulatory censure. Providers must invest heavily in built-in compliance modules, audit logging, dynamic consent tools, and regional data hosting. These requirements drive up product development costs and limit the pace of feature roll-outs, particularly for smaller vendors.

Verticals such as healthcare, utility, and government billing have unique compliance needs—e.g., HIPAA for patient data or tariff‑based billing cycles. Vendors offering verticalized debt collection modules with built-in regulatory templates, consent management, and API connectors can capture these niches. For example, tailored healthcare modules can integrate with EHR systems and insurance adjudication engines. Such vertical specificity allows providers to charge premium subscription rates—20–30% above standard offerings—while delivering faster time-to-deploy and higher compliance assurance, representing an untapped segment for software vendors.

Large enterprises often require deep integration into existing ERP, CRM, billing, and legal systems. Custom connectors, audit modules, and on-premise deployment options contribute to implementation costs exceeding USD 500,000 per deployment and timelines of 6–12 months. These complexities increase total cost of ownership and deter mid-tier clients. Moreover, the need to maintain compliance across multiple jurisdictions leads to recurring legal and IT maintenance expenses, challenging ROI calculations and slowing enterprise sales cycles.

AI‑Driven Priority Sorting and Workflow Optimization: Debt Collection Software Market platforms now deploy predictive models to rank debtor accounts using over 50 behavioral indicators. This leads to prioritized workflows where collectors focus on top 20% of high-probability accounts, increasing first-contact resolution rates by 25% and reducing manual triage time by up to 40%.

Modular, API‑First Architecture: Adoption of modular, microservices‑based debt collection platforms enables clients to integrate discrete functions—such as payment plans, compliance, and chatbots—with legacy ERPs. This flexibility reduces deployment cycles by approximately 30%, accelerating time-to-value and easing vendor switch scenarios.

Agentic AI for On‑Call Assistive Support: Agentic AI tools are now guiding live collectors with real‑time call prompts based on conversational context. Early adopters report a 15% improvement in call quality scores and a 20% shorter call handling time, enhancing both effectiveness and customer experience within Debt Collection Software Market deployments.

Embedded Collection in Embedded Finance Systems: Debt collection workflows are increasingly embedded into digital lending apps, BNPL interfaces, and billing systems. This seamless integration enables proactive reminders, self-serve payment links, and dispute resolution—all within the same UI—enhancing user experience and increasing recovery success rates by up to 10% without direct collector involvement.

The Debt Collection Software Market is segmented by type, application, and end-user, each reflecting distinct operational needs and adoption patterns. Type-based segmentation includes software offerings ranging from standalone platforms to fully integrated cloud-based solutions. Applications span across various sectors such as first-party debt recovery, third-party collections, and government or legal collections. End-user insights reveal strong usage among financial institutions, healthcare providers, telecom operators, and government agencies. The segmentation indicates that decision-makers are increasingly prioritizing flexibility, regulatory compliance, and automation. Cloud-native and AI-augmented systems are gaining popularity due to their scalability and real-time analytics capabilities. This segmentation highlights how market participants tailor solutions to specific operational requirements, influencing software development, customization demand, and vendor competitiveness across regions.

In terms of product types, the Debt Collection Software Market is mainly categorized into on-premise software, cloud-based software, and hybrid platforms. Cloud-based solutions lead the segment due to their rapid scalability, ease of updates, and accessibility across multiple geographies. Organizations prefer cloud models to reduce infrastructure costs and enhance integration with existing CRMs, billing systems, and analytics engines. These platforms also allow real-time access and mobile compatibility, which is increasingly vital for distributed or remote collections teams.

The fastest-growing type is hybrid software, which combines the security and control of on-premise infrastructure with the flexibility and remote accessibility of cloud systems. Enterprises with strict data governance or region-specific compliance requirements are adopting hybrid deployments to align with regulatory frameworks while still benefiting from cloud functionalities.

On-premise solutions remain relevant for highly regulated industries such as government or healthcare, where data residency and control are paramount. However, their growth is limited due to high maintenance overhead and lower agility. Collectively, each type offers tailored benefits, allowing users to align their operational priorities with the right technology stack.

The major application areas in the Debt Collection Software Market include first-party collections, third-party debt recovery, legal and government collections, and dispute resolution workflows. First-party collections are currently the dominant application area, particularly in sectors like banking, retail credit, and telecom, where internal teams are responsible for early-stage recovery efforts. These systems automate outreach, segmentation, and reporting, enabling companies to reduce delinquencies proactively.

Third-party debt recovery is emerging as the fastest-growing application, driven by the surge in outsourcing strategies. Financial institutions, fintech platforms, and healthcare providers are increasingly leveraging third-party agencies to handle aging debts and non-performing loans. This shift demands advanced software with features like role-based permissions, real-time dashboards, and multi-client account segregation.

Government and legal collections form a niche but critical application area, focusing on regulatory compliance and long-term debt management. Dispute resolution applications are gaining ground in industries with frequent billing discrepancies, such as utilities or insurance. Together, these applications reveal a multi-dimensional use case environment, enabling organizations to deploy targeted, efficient debt recovery processes.

End-users of Debt Collection Software include financial institutions, healthcare organizations, telecom service providers, government entities, and debt collection agencies. Financial institutions represent the leading end-user segment, driven by the volume of consumer and commercial credit handled. These organizations require high-volume, secure, and regulation-compliant systems capable of processing millions of accounts with minimal manual intervention. Their demand is largely shaped by operational efficiency goals and rising default rates in unsecured lending.

Healthcare organizations are the fastest-growing end-user segment. Rising medical debt, insurance-related billing delays, and regulatory pressures around HIPAA compliance have pushed healthcare providers to invest in specialized debt collection software. These systems must be capable of managing sensitive patient data, automating payment plans, and integrating with hospital billing and EHR systems.

Telecom and utility companies use debt collection tools to manage recurring billing and non-payment scenarios efficiently. Government bodies leverage such software to handle tax delinquencies, fines, and municipal debts. Debt collection agencies, while traditionally dominant, now focus on adopting scalable tools that support multiple client verticals, enabling competitive differentiation in a heavily regulated landscape.

North America accounted for the largest market share at 38.2% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.8% between 2025 and 2032.

The dominance of North America is attributed to the region’s mature debt management infrastructure, high digital adoption, and regulatory enforcement in sectors like BFSI and healthcare. Meanwhile, Asia-Pacific is witnessing rapid fintech expansion, rising credit activity, and significant investments in cloud-based software. Countries such as China and India are experiencing high volumes of unsecured lending and digital commerce, which are propelling the demand for scalable, automated collection platforms. The increasing pressure to manage debt portfolios efficiently, coupled with advancements in AI-driven communication tools, is pushing organizations across all major regions to modernize their recovery processes. Additionally, Europe and the Middle East are observing strong momentum due to evolving compliance frameworks and cross-border digital collection mandates.

North America held the largest share in the Debt Collection Software Market at 38.2% in 2024, driven by highly automated financial and healthcare ecosystems. The U.S. and Canada are home to a mature network of software vendors, with many platforms offering AI-driven automation, real-time analytics, and cloud-native integrations. Key industries fueling demand include banking, telecom, healthcare, and education, each facing heightened regulatory scrutiny on debt servicing practices. Recent reforms such as the California Consumer Privacy Act (CCPA) have driven upgrades in data transparency, consent tracking, and communication monitoring. Digital transformation trends, such as API-first collections platforms and mobile-friendly self-service tools, are being adopted aggressively. Government support for data localization and secure digital finance further strengthens the region’s software development ecosystem. The region also benefits from high levels of R&D investment, helping enterprises remain compliant while improving operational performance in debt recovery processes.

Europe accounted for approximately 27.5% of the global Debt Collection Software Market in 2024, with Germany, the UK, and France serving as primary growth hubs. The market is defined by stringent regulatory oversight, including GDPR, MiFID II, and consumer protection laws that drive demand for traceable, compliant software platforms. Leading European organizations are increasingly deploying AI-enabled communication tools and audit-ready analytics to ensure regulatory compliance while enhancing recovery efficiency. Sustainability initiatives like the EU’s Digital Operational Resilience Act (DORA) are prompting organizations to adopt more resilient, modular debt collection systems. Automation and integration with banking and telecom systems are becoming standard, particularly in Northern and Western Europe. Cloud deployment, already widespread in the UK and Germany, is expanding into Southern and Eastern Europe as infrastructure improves. This push toward digital compliance and smart software is cementing Europe’s role as a key innovation hub within the global Debt Collection Software Market.

Asia-Pacific ranks as the fastest-growing region in the Debt Collection Software Market and accounted for nearly 19.6% of global volume in 2024. Major consumption is led by China, India, and Japan, where the combination of rising consumer credit, fintech expansion, and mobile-first platforms is reshaping debt recovery workflows. In India and Southeast Asia, the surge in digital lending and Buy Now Pay Later (BNPL) services is generating substantial demand for automated, multilingual debt collection software. Governments are investing in cloud infrastructure and secure digital finance platforms, making it easier for vendors to scale AI-driven solutions. Additionally, tech innovation hubs such as Bangalore, Shenzhen, and Tokyo are leading in deploying embedded payment systems and API-based collection automation. Telecom, healthcare, and SME sectors are emerging as top adopters due to growing billing complexity and rising delinquency rates. As infrastructure matures, Asia-Pacific is poised to become a long-term growth engine for the Debt Collection Software Market.

In 2024, South America contributed around 7.3% to the global Debt Collection Software Market, with Brazil and Argentina leading regional adoption. The growth is fueled by a rapidly expanding consumer credit base and rising non-performing loans in both public and private sectors. Key industries such as utilities, telecommunications, and financial services are facing increased pressure to improve recovery rates while adhering to evolving compliance standards. Governments are providing incentives to digitize public debt recovery systems and streamline tax collection processes. Infrastructure developments, such as regional cloud data centers in Brazil, are enabling SaaS-based software providers to scale operations locally. Trade agreements and updated digital finance regulations are further encouraging businesses to adopt flexible, AI-enhanced debt collection platforms. The region is showing increasing interest in multilingual, mobile-first solutions capable of adapting to diverse socio-economic conditions across urban and rural debt portfolios.

The Middle East & Africa (MEA) region represented approximately 7.4% of the global Debt Collection Software Market in 2024, with UAE, Saudi Arabia, and South Africa as key contributors. Demand is driven by sectors such as oil & gas, construction, government utilities, and retail finance. These industries require compliant, multi-lingual debt recovery systems to manage cross-border and domestic receivables. UAE’s push toward smart governance and digital finance is accelerating the adoption of AI-powered collection platforms. South Africa is investing in cloud-based IT infrastructure and enhancing digital ID verification to support secure collections. MEA markets are seeing notable shifts toward regulatory modernization, with countries like Saudi Arabia implementing fintech frameworks that require greater transparency and automation in debt management. Trade partnerships between GCC countries and international software providers are fostering technology transfer, further enriching the region’s debt recovery ecosystem. As digitization intensifies, MEA stands as a high-potential frontier for the Debt Collection Software Market.

United States – 36.1% Market Share

The U.S. leads the Debt Collection Software Market due to high adoption of digital banking, strong regulatory enforcement, and advanced software development capabilities.

China – 12.4% Market Share

China ranks second in the Debt Collection Software Market, supported by rapid fintech expansion and a massive volume of consumer credit transactions requiring automated recovery tools.

The competitive landscape of the Debt Collection Software Market is characterized by a dynamic mix of established players and emerging startups, with over 85 active competitors operating globally. Market leaders maintain dominance through robust product portfolios, global reach, and strong brand recognition, while newer entrants focus on niche technologies such as AI-driven communication, predictive analytics, and multilingual automation. Strategic initiatives such as partnerships with fintech providers, cloud service alliances, and acquisitions are common as companies seek to broaden their capabilities and client base. Product launches targeting regional compliance, industry-specific debt workflows, and mobile-first collections are becoming more frequent. Vendors are increasingly offering SaaS and API-first models to support integration into broader enterprise resource planning (ERP) and customer relationship management (CRM) platforms. The rise of embedded collections in digital payments and BNPL systems is further intensifying competition. Key innovation trends include low-code customization, AI-powered chatbots, omnichannel communication engines, and adaptive compliance tools tailored to cross-border debt collection needs.

FICO

Pegasystems Inc.

Experian Information Solutions, Inc.

CGI Inc.

Chetu Inc.

TietoEVRY

Katabat (a TransUnion Company)

Latitude by Genesys

Simplicity Collection Software

Codix

Advantage Software Factory

Collect!

EXUS

Loxon Solutions

Quantrax Corporation, Inc.

Technological advancements are playing a pivotal role in reshaping the Debt Collection Software Market. Artificial Intelligence (AI) and Machine Learning (ML) have become critical enablers, allowing platforms to predict debtor behavior, personalize collection strategies, and automate routine communications. AI-powered chatbots are increasingly used for first-level interactions, reducing manual workload and enhancing engagement rates. The integration of Natural Language Processing (NLP) and sentiment analysis tools enables companies to optimize messaging tone and timing, thereby improving repayment outcomes.

Cloud-native deployments are now standard, offering scalability, remote accessibility, and high uptime. Multi-tenant SaaS models are gaining preference, especially among small to mid-sized enterprises seeking cost efficiency and ease of maintenance. Integration with ERP, CRM, and digital payment gateways has become seamless due to widespread adoption of API-first architectures.

Data security technologies, including end-to-end encryption and advanced identity verification protocols, are being embedded to meet compliance standards such as GDPR, CCPA, and PCI-DSS. Advanced analytics dashboards with real-time KPIs and customizable reporting interfaces empower organizations to monitor performance dynamically and adjust strategies. Emerging technologies such as blockchain are being explored for transparent debt transfer tracking, while Robotic Process Automation (RPA) is reducing manual intervention in data entry and legal documentation. As digital lending and e-commerce platforms proliferate, tech innovation will remain central to competitive differentiation in the market.

In February 2024, Pegasystems launched its updated Pega Smart Dispute platform with AI-driven resolution features and expanded support for buy now, pay later (BNPL) programs, enhancing real-time dispute management for financial institutions.

In November 2023, FICO introduced new compliance modules within its Debt Manager platform, including multilingual support and dynamic policy adaptation for EU markets, boosting flexibility in cross-border collection operations.

In April 2024, CGI Inc. announced a strategic partnership with a leading European fintech firm to integrate CGI’s debt collection modules into next-generation digital banking ecosystems across Germany and the Nordics.

In August 2023, Chetu Inc. unveiled its next-gen collection software API suite offering enhanced mobile optimization, chatbot integration, and improved analytics targeting third-party collectors and law firms.

The Debt Collection Software Market Report offers a comprehensive and detailed overview of the industry's scope, focusing on multiple dimensions such as product type, application areas, deployment models, end-user verticals, and regional performance. It covers both traditional on-premise software and cloud-based SaaS platforms, with a growing emphasis on mobile, AI-enabled, and API-integrated solutions.

The report explores key application areas including banking and financial services, healthcare, telecom, government, retail, and education, highlighting the unique needs and adoption patterns within each sector. It also examines deployment preferences such as single-tenant vs. multi-tenant systems, automation levels, and integration capabilities with other enterprise platforms.

Geographically, the report spans five major regions—North America, Europe, Asia-Pacific, South America, and the Middle East & Africa—drilling down into country-level insights for top-performing markets such as the United States, China, Germany, and India.

Technology insights emphasize innovations like machine learning, cloud-native architecture, robotic process automation, and blockchain potential. Additionally, the report identifies emerging niches such as debt recovery solutions tailored for Buy Now Pay Later (BNPL), embedded finance, and small business lending platforms. The scope includes competitive mapping, regulatory trends, and strategic recommendations for market stakeholders across the global ecosystem.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 480.0 Million |

| Market Revenue (2032) | USD 999.4 Million |

| CAGR (2025–2032) | 9.6% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End‑User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Technological Insights, Market Dynamics, Segment Analysis, Regional and Country-Wise Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia‑Pacific, South America, Middle East & Africa |

| Key Players Analyzed | FICO, Pegasystems Inc., Experian Information Solutions, Inc., CGI Inc., Chetu Inc., TietoEVRY, Katabat (a TransUnion Company), Latitude by Genesys, Simplicity Collection Software, Codix, Advantage Software Factory, Collect!, EXUS, Loxon Solutions, Quantrax Corporation, Inc. |

| Customization & Pricing | Available on Request (10% Customization is Free) |