Reports

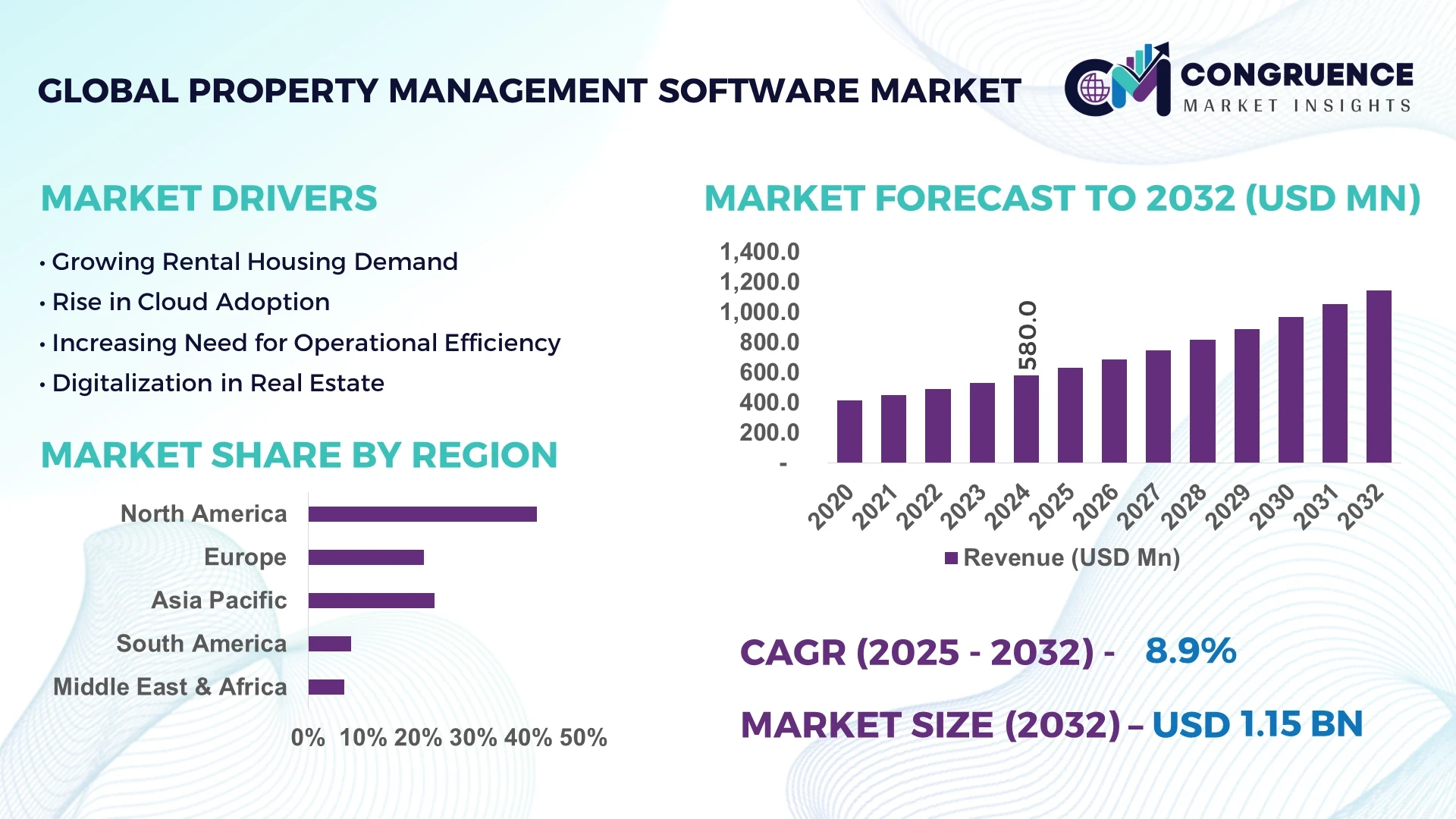

The Global Property Management Software Market was valued at USD 580.0 Million in 2024 and is anticipated to reach a value of USD 1,147.2 Million by 2032 expanding at a CAGR of 8.9% between 2025 and 2032.

North America, particularly the United States, leads in innovation and capacity within the Property Management Software Market. Leading U.S.-based firms continually invest hundreds of millions annually into cloud-native platforms with integrated AI modules, automating tasks such as lease administration and maintenance coordination. Advanced offerings include built-in IoT data control, predictive alerts in building automation systems, and embedded mobile-first user interfaces deployed across large commercial housing portfolios to enhance tenant engagement and streamline vendor workflows.

The Property Management Software Market spans residential, commercial, and hospitality sectors, with residential applications currently generating approximately two-thirds of global system deployments. Recent innovations include AI-driven lease abstraction tools and voice-enabled maintenance request systems, enhancing operational throughput and tenant satisfaction. Regulatory momentum toward energy-efficiency and digital compliance (for example, e-signatures and document archives) is reshaping product enhancements. In North America and Europe, mobile-enabled cloud solutions are the standard, while the Asia-Pacific region is accelerating adoption driven by government-backed smart-city projects. Emerging trends include modular integration of energy-management and tenant experience analytics into core PMS platforms, with future outlooks highlighting a shift toward full-stack service ecosystems—incorporating in-app fintech, dynamic pricing engines, and ESG compliance modules.

AI technologies are fast becoming central to the Property Management Software Market, offering measurable efficiency gains and operational optimizations. For instance, leading platforms now automate routine tasks—rent reminders, lease renewals, and vendor scheduling—freeing property teams to focus on strategic operations. Studies from 2024 reveal that AI lease abstraction tools reduce data-extraction processes by over 70%, accelerating onboarding by several hours per document. AI-powered maintenance modules leverage predictive analytics to forecast system failures, with real-world implementations showing a 25–30% reduction in emergency repair costs.

AI-enhanced tenant communication bots operate 24/7, handling FAQs and routing complex queries to human teams—cutting response times by up to 50% and increasing tenant satisfaction scores in pilot programs. AI-driven data analytics also empower property managers with deeper insights: occupancy forecasting, dynamic price adjustments, and portfolio optimization, all based on real-time multi-source data inputs. Integration of voice-command systems and IoT sensor networks further enhances energy management and maintenance responsiveness.

As AI continues to mature, Property Management Software Market offerings are evolving into intelligent ecosystems—where decision-support tools, process automation, and tenant experience converge within unified SaaS platforms. This evolution is driving faster adoption among mid- to enterprise-level property operators seeking operational scalability, cost controls, and enhanced service quality.

“In 2024, AppFolio launched Realm‑X Assistant, enabling automated vendor coordination and tenant report generation; implementation pilots recorded a 40% decrease in time spent on account reconciliation within three months.”

The Property Management Software Market Dynamics reflect a rapidly evolving ecosystem influenced by digital transformation, regulatory needs, and tenant expectations. Key market trends include increased adoption of SaaS and mobile-first deployment models. Decision-makers in real estate prioritize platforms offering integrated analytics, predictive maintenance, and tenant communication tools. Shifts in global rental markets—especially in urban centers—are driving demand for scalable solutions managing large portfolios. Sustainability and ESG compliance trends are provoking product enhancements such as energy benchmarking modules and digital audit trails. Across regions, consumption patterns vary: North American markets lead in innovation and premium adoption, whereas emerging markets in Asia-Pacific show accelerated uptake propelled by smart-city investments.

The surge in cloud computing and mobile-enabled solutions is catalyzing transformation in the Property Management Software Market. By 2024, over 80 % of newly deployed PMS systems were SaaS-based, enabling real-time access by field staff and tenants. Mobile app integrations for maintenance requests and rent payments have driven operational efficiency improvements—tenant satisfaction scores have increased by 30% and task resolution times have dropped by nearly 50% in several city-wide portfolio trials. This technology stack shift also supports integrations with payment gateways, IoT sensor networks, and third-party service providers. These developments position cloud and mobile tools as a critical driver of the Market’s continuing modernization and user-focused enhancements.

A significant constraint within the Property Management Software Market is the difficulty of integrating new systems with legacy infrastructure. Many property managers still rely on disparate on-premise databases, Excel-based records, and siloed financial tools. Consolidating these into unified cloud platforms often requires extensive data migration, API development, and training. Reports indicate over 40% of mid-size operators experienced integration delays of 6–12 months, with technical support costs rising by up to 25%. Furthermore, resistance from IT departments around data security and disruption to existing workflows remains a barrier to broad adoption, especially in regions where digital transformation is still emerging.

There is growing demand in the Property Management Software Market for embedded ESG and energy-efficiency analytics. In 2024, several platforms added modules to track carbon emissions, water usage, and green-certification compliance. Pilot programs showed that properties using ESG-integrated tools achieved utility cost reductions of 10–15%, with portfolio-wide energy audits decreased by 40%. Additionally, landlords are leveraging these modules to appeal to environmentally conscious tenants and investors. With tightening sustainability regulations in regions like the EU and North America, PMS providers have a timely opportunity to differentiate through built-in environmental reporting and automated compliance features.

Cybersecurity presents a critical challenge for the Property Management Software Market, as platforms increasingly handle sensitive tenant and financial data. In 2024, reported breaches in several multi-property databases exposed tenant personal information and rent payment histories. These incidents triggered compliance reviews under regulations like GDPR and CCPA. Following the breaches, average insurance premiums for cyber coverage rose by 20%, and internal audit requirements increased by 35%. Software vendors are now required to deploy advanced encryption, multi-factor authentication, and automated audit logs. Failure to meet these standards risks both legal and reputational harm—an ongoing obstacle for widespread, trust-based system adoption.

Modular Integrations for Energy Management: Property management platforms are increasingly incorporating modular energy-analytics and IoT sensor integration. In 2024, more than 60% of large-scale SaaS platforms included dynamic energy-tracking dashboards, enabling facility managers to benchmark consumption across portfolios. Test implementations showed up to a 12% reduction in monthly utility expenses within six months.

AI-Driven Lease Abstraction: Automated lease processing tools are reducing manual data extraction by over 70%. Pilots in North America and Europe have slashed onboarding times per lease from an average of four hours to under one hour, significantly lowering administrative overhead.

Voice-Enabled Tenant Engagement: Voice-bot systems deployed in select U.S. markets now answer rental inquiries and maintenance reports 24/7, cutting tenant call volume by 45%. These platforms support natural language understanding and multilingual workflows to enhance service availability.

Embedded Fintech Solutions: Built-in rent payment portals and dynamic pricing engines are becoming standard. Some platforms now support instant rent disbursement and API-backed credit checks, improving rent collection rates by 15% and reducing late payments by 20%.

The Property Management Software Market is segmented based on type, application, and end-user, with each segment addressing distinct operational demands within the property ecosystem. Types of software include on-premise, cloud-based, and hybrid systems, offering varying degrees of control, scalability, and integration capability. Application-wise, property management software is deployed in residential, commercial, industrial, and special-use facilities. Each application requires unique feature sets, from rent collection and maintenance scheduling to lease compliance and asset tracking. The end-user base ranges from property managers and real estate agencies to housing associations and facility management firms, each driving software adoption for specific operational efficiencies and tenant engagement strategies. The segmentation reveals distinct growth patterns, with cloud-based systems, residential applications, and real estate enterprises demonstrating elevated adoption due to their scalability, user-centric interfaces, and regulatory compliance functionality.

The Property Management Software Market includes several major types: cloud-based, on-premise, and hybrid systems. Among these, cloud-based property management software holds the leading position due to its accessibility, lower upfront infrastructure costs, and seamless integration with third-party services. Enterprises prefer cloud systems for their real-time data access, remote task management, and automatic updates—critical capabilities in multi-location or decentralized property operations.

The fastest-growing type is hybrid software, which blends cloud accessibility with local server control, offering flexibility and enhanced security. This type is gaining traction among firms with strict compliance needs or partial internet availability. Hybrid deployments allow real estate firms to benefit from cloud scalability while retaining critical data within in-house infrastructure.

On-premise solutions, although declining in popularity, remain essential for institutions that prioritize data control and have established IT infrastructure. These are often used in public housing bodies or corporate real estate arms with legacy systems. Overall, the market demonstrates a shift toward flexible, scalable, and secure deployment types, shaped by operational complexity and digital maturity.

In terms of application, the Property Management Software Market is segmented into residential, commercial, industrial, and special-use property management. Residential property management remains the leading application due to the large volume of multifamily housing units, apartment complexes, and rental homes requiring automated solutions for tenant communication, rent collection, and maintenance tracking. The widespread use of online rental platforms and digital leasing has further driven software adoption in this category.

The fastest-growing application area is commercial property management, including office buildings, retail spaces, and mixed-use developments. The growing complexity of lease structures, facility services, and multi-tenant environments fuels demand for automation, analytics, and integration with energy-management systems. Smart-building initiatives and post-pandemic workplace restructuring are also accelerating commercial adoption.

Other notable applications include industrial facilities, where software supports equipment maintenance and asset tracking, and special-use properties like student housing and senior living communities, which require niche features such as community scheduling or compliance tools. These specialized applications, though smaller in share, play a critical role in diversifying the market landscape.

The end-user segmentation of the Property Management Software Market comprises property management firms, housing associations, real estate agencies, facilities management providers, and individual landlords. Among these, property management firms dominate usage, particularly mid- to large-scale enterprises that manage multiple residential or commercial units. These organizations rely heavily on software platforms to handle operations at scale, automate repetitive tasks, and centralize data for performance monitoring.

The fastest-growing end-user group is real estate agencies, which are increasingly integrating property management capabilities into their brokerage services. This expansion is driven by the growing convergence of leasing, tenant management, and property maintenance within a single service offering. Agencies adopt modular software features to offer value-added services to landlords and investors.

Housing associations and government entities use these platforms to manage subsidized or community housing projects, ensuring compliance and transparency. Facilities management firms deploy these systems to streamline service scheduling and vendor management, especially in commercial assets. Lastly, individual landlords are gradually embracing lightweight SaaS platforms for rent automation and digital communication, contributing to the expanding base of software users.

North America accounted for the largest market share at 41.6% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12.6% between 2025 and 2032.

The dominance of North America stems from its widespread adoption of SaaS platforms, highly digitized property markets, and mature real estate ecosystems. Meanwhile, Asia-Pacific's growth is being propelled by rising urbanization, smart city infrastructure programs, and expanding real estate investments in countries such as China, India, and Southeast Asia. Regional variations in platform functionalities, regulatory frameworks, and tenant expectations are also shaping the deployment strategies of vendors. With growing demand for automated lease tracking, real-time maintenance systems, and cloud-enabled asset performance management, global players are localizing offerings to align with the needs of each regional market, creating a dynamic competitive landscape. As governments in emerging markets encourage digital adoption in the property sector, these trends are expected to accelerate.

North America leads the global Property Management Software Market with a market share of approximately 41.6% in 2024. The United States is the primary driver, supported by a vast inventory of residential and commercial properties managed through digital-first platforms. Key industries influencing demand include multi-family housing, commercial real estate, and institutional property management. The region benefits from established government-backed housing programs that increasingly mandate digital compliance and reporting standards. Notably, regulatory emphasis on tenant rights and rent transparency has fueled upgrades to software systems. In addition, the proliferation of AI, IoT integration, and mobile-native applications is reshaping operational workflows. Companies are adopting predictive analytics, smart building dashboards, and automated lease documentation to reduce costs and improve tenant engagement, making North America a benchmark for digital real estate management.

Europe represents a significant share in the global Property Management Software Market, with key contributions from countries such as Germany, the United Kingdom, and France. In 2024, the region held approximately 27.3% of the total market volume. Europe’s property sector is increasingly shaped by the region’s strong regulatory focus on sustainability and energy efficiency. The European Commission’s directives on green building compliance and tenant data protection have prompted widespread adoption of secure, ESG-compliant software platforms. Countries like Germany are investing in centralized digital platforms for social housing oversight, while the UK is pushing for standardized digital lease management in private rentals. Adoption of emerging technologies, including automated energy audits and tenant-facing mobile apps, is growing steadily. The integration of property software with broader Smart City initiatives is also on the rise, especially in Scandinavian and Western European markets, reinforcing the region’s innovation-driven growth.

Asia-Pacific is emerging as the fastest-growing region in the Property Management Software Market, holding a market volume share of 18.5% in 2024. Key contributors include China, India, and Japan, with China leading in platform expansion across tier-1 cities. Government-led smart city infrastructure projects and private investments in large-scale real estate portfolios are significantly influencing adoption. India’s rising rental economy and demand for mid-tier SaaS platforms are also reshaping the competitive landscape. Advanced property tech hubs in Singapore and South Korea are driving innovation, with startups launching AI-powered leasing, e-payment, and facility scheduling systems. Cloud deployment is becoming the norm, with localized offerings tailored to regional languages and regulatory nuances. As the region urbanizes rapidly, real estate operators are turning to software tools to optimize asset performance and ensure compliance with evolving tenancy regulations, making Asia-Pacific a critical driver of future market expansion.

South America is gradually expanding its presence in the Property Management Software Market, with Brazil and Argentina serving as the region’s primary growth engines. In 2024, the region accounted for approximately 6.1% of global market share. Urban infrastructure modernization, particularly in Brazil, is generating demand for digital property solutions to manage large-scale residential and commercial complexes. The energy sector’s growth and redevelopment of urban zones are encouraging developers to adopt integrated asset and tenant management platforms. Government initiatives to streamline property registration and automate rent control policies are further boosting market momentum. Despite challenges around broadband access and digital literacy in rural zones, metropolitan areas are embracing cloud-based property platforms with mobile-first interfaces. Software vendors are partnering with local telecom providers to improve accessibility and compliance, reinforcing South America's steady transition toward digital property governance.

The Middle East & Africa (MEA) region is witnessing growing demand within the Property Management Software Market, driven by major economies like the UAE and South Africa. In 2024, the region held a market share of 6.5%, supported by investments in real estate and hospitality infrastructure. The UAE is leading transformation efforts through digitization mandates across construction and housing sectors. Saudi Arabia’s Vision 2030 initiative has further accelerated property system upgrades in planned urban developments. In Africa, South Africa’s commercial real estate sector is digitizing lease and facility management in response to regional security and operational transparency needs. The rise of smart city zones, especially in the Gulf region, has created a need for sophisticated software that integrates with energy monitoring and IoT-based maintenance solutions. Local regulations emphasizing e-registration and digital service delivery are encouraging adoption of advanced property tech tools across both public and private sectors.

United States – 41.2% Market Share

Dominance driven by high platform penetration across residential and commercial property sectors, with robust demand from institutional landlords and digital-native enterprises.

China – 15.7% Market Share

Rapid urban expansion and government-supported smart city infrastructure fueling widespread adoption of cloud-based property management platforms.

The Property Management Software Market is marked by intense competition, with over 250 active vendors operating globally. The competitive environment is dominated by a mix of established software companies, specialized SaaS providers, and new-age PropTech startups. Key players are continuously enhancing platform capabilities with AI-based analytics, mobile-first interfaces, and integrations with IoT-enabled smart building systems. Strategic collaborations and partnerships are frequent, especially with fintech and digital payment service providers, enabling companies to offer comprehensive solutions covering tenant billing, rent collection, and compliance management.

Mergers and acquisitions have also intensified, as larger firms acquire niche players to expand their feature portfolios and strengthen regional presence. For instance, some vendors have acquired inspection automation startups or digital ID verification tools to improve leasing and maintenance workflows. Innovation is another key driver, with several companies investing in virtual tour capabilities, predictive maintenance algorithms, and voice-activated tenant communications. Market participants are focusing on scalability and cloud-native solutions to serve both SMBs and large-scale real estate portfolios, creating a highly dynamic and evolving market landscape.

AppFolio Inc.

Yardi Systems Inc.

RealPage Inc.

MRI Software LLC

Buildium LLC

Entrata Inc.

ResMan LLC

SimplifyEm Inc.

TenantCloud

Hemlane Inc.

TurboTenant Inc.

Rentec Direct

Innago

RentRedi Inc.

ManageCasa Inc.

Technology plays a transformative role in the evolution of the Property Management Software Market. The industry has shifted decisively toward cloud-based, mobile-compatible platforms, enabling property managers to operate remotely and maintain real-time visibility across asset portfolios. AI and machine learning are now core to automating rent pricing, tenant screening, and predictive maintenance. In 2024, over 60% of new software deployments include AI-powered recommendation engines for lease optimization and personalized tenant engagement.

The rise of IoT-enabled buildings has led to a growing demand for software that can seamlessly integrate with smart meters, access controls, and energy management systems. This has enabled real-time monitoring of building performance, reduced downtime, and streamlined operational costs. Blockchain technology is being explored for lease authentication, secure transactions, and transparent ownership records, particularly in commercial properties.

Another emerging trend is voice-enabled interfaces, allowing property managers and tenants to interact with the system via virtual assistants for quick updates or maintenance requests. Additionally, digital twin technologies are enabling 3D visualizations and simulations of entire properties, supporting real-time asset monitoring and planning. The integration of fintech features such as embedded payments, tenant credit scoring, and automated tax filings further enhances the value proposition of modern platforms. Collectively, these advancements are driving greater efficiency, transparency, and user experience in property operations.

In March 2024, AppFolio launched its next-generation AI assistant, RealmX, designed to automate tenant interactions and streamline maintenance request processing. The tool is already being piloted across 1,500 properties, showing a 30% drop in manual workload.

In January 2024, MRI Software announced the acquisition of a tenant engagement platform specializing in mobile apps and digital concierge services. The integration aims to improve resident retention and brand loyalty for large property portfolios.

In September 2023, RealPage introduced an automated rent optimization module powered by behavioral analytics, helping landlords adjust prices based on real-time demand and historical occupancy patterns across metro areas.

In October 2023, Yardi Systems expanded its fintech integrations to include in-app rent payment via major digital wallets, with early adoption seeing a 25% improvement in on-time payments in multifamily units.

The Property Management Software Market Report delivers a comprehensive analysis of the industry's structure, segmentation, technological trends, and geographic footprint. Covering over 25 countries across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, the report evaluates both mature and emerging regional markets. It examines the market by type (cloud-based, on-premise), application (residential, commercial, industrial), and end-users (property managers, housing associations, corporate real estate operators, etc.).

The study investigates core functionalities including lease administration, rent collection, maintenance scheduling, tenant screening, and reporting dashboards. It also addresses evolving technologies like AI-driven automation, IoT-enabled building management, blockchain for contracts, and mobile apps for tenant engagement. Special attention is given to the integration of digital payment systems, ESG compliance modules, and virtual tour solutions.

In addition to standard applications, the report highlights niche segments such as student housing, senior living communities, and co-working property management. It also explores adoption trends among small and mid-sized property operators, which are increasingly turning to SaaS platforms to streamline operations. The market scope is defined by its rapid digitization, increasing regulatory complexity, and growing demand for real-time data and centralized control, making this analysis essential for investors, vendors, and policy stakeholders alike.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 580.0 Million |

| Market Revenue (2032) | USD 1,147.2 Million |

| CAGR (2025–2032) | 8.9% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape, Technological Insights, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | AppFolio Inc., Yardi Systems Inc., RealPage Inc., MRI Software LLC, Buildium LLC, Entrata Inc., ResMan LLC, SimplifyEm Inc., TenantCloud, Hemlane Inc., TurboTenant Inc., Rentec Direct, Innago, RentRedi Inc., ManageCasa Inc. |

| Customization & Pricing | Available on Request (10% Customization is Free) |