Reports

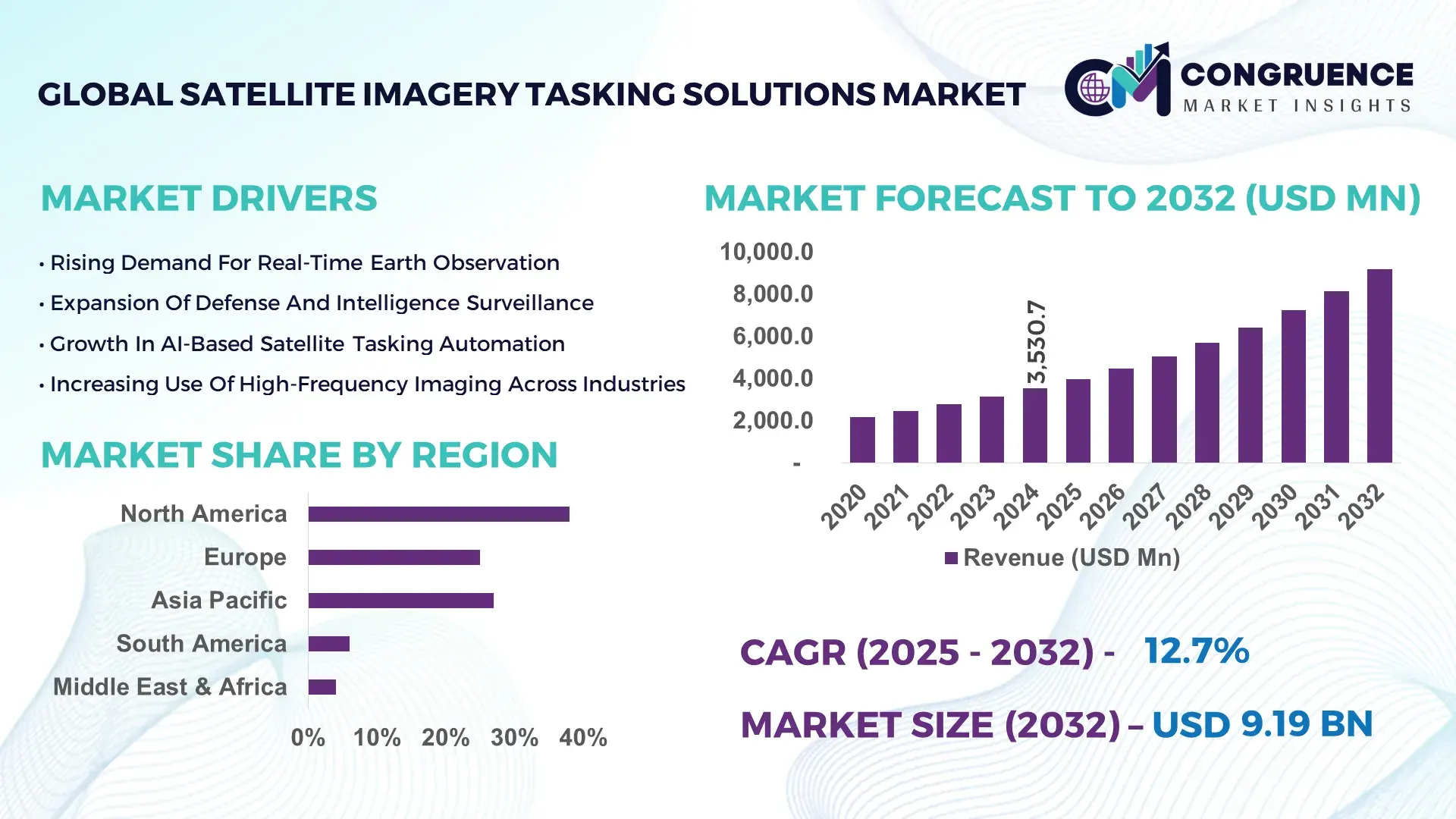

The Global Satellite Imagery Tasking Solutions Market was valued at USD 3,530.7 Million in 2024 and is anticipated to reach a value of USD 9,188.7 Million by 2032 expanding at a CAGR of 12.7% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is driven by rising demand for rapid-response imaging, multi-orbit constellation expansions, and AI-enhanced tasking automation.

The United States retains a dominant position due to its advanced satellite manufacturing ecosystem, deep federal investment in geospatial intelligence, and strong adoption of real-time Earth observation systems across defense, environmental management, and infrastructure sectors. In 2024 alone, over 2,800 U.S. enterprises utilized tasking-enabled geospatial tools, and federal programs supported more than 120 active satellites with next-generation imaging capabilities exceeding 15–30 cm resolution thresholds.

Market Size & Growth: Valued at USD 3.53 Billion in 2024 and projected to reach USD 9.18 Billion by 2032 with a 12.7% CAGR, driven by expanding demand for rapid-response satellite imaging and AI-led orchestration.

Top Growth Drivers: 48% rise in demand for near-real-time monitoring; 36% improvement in automated tasking efficiency; 52% surge in defense and environmental applications.

Short-Term Forecast: By 2028, automated tasking platforms expected to reduce operational latency by 28%.

Emerging Technologies: Multi-sensor fusion models, AI-driven constellation scheduling, and hyperspectral tasking automation.

Regional Leaders: North America expected to reach USD 3.1 Billion by 2032; Europe projected at USD 2.4 Billion with strong environmental adoption; Asia-Pacific to hit USD 2.8 Billion driven by high-volume imaging deployments.

Consumer/End-User Trends: Defense, energy, and environmental regulators show rising adoption of real-time geospatial workflows for predictive analytics and compliance tracking.

Pilot or Case Example: In 2024, a national emergency-response program using automated tasking achieved a 31% reduction in disaster-mapping time.

Competitive Landscape: Market leader holds approx. 18% share; major competitors include Airbus Intelligence, Planet Labs, Maxar Intelligence, and ICEYE.

Regulatory & ESG Impact: Enhanced environmental compliance mandates accelerating demand for satellite-based monitoring and 20–30% improvements in emission tracking accuracy.

Investment & Funding Patterns: Over USD 1.6 Billion invested in satellite and geospatial automation programs in the last two years, with growing venture activity in AI-driven constellations.

Innovation & Future Outlook: Advancements in autonomous tasking engines, quantum-enhanced imaging pipelines, and collaborative multi-orbit networks shaping next-decade opportunities.

Global demand is increasingly shaped by defense, environmental agencies, and precision-driven commercial sectors. Recent innovations in AI tasking, hyperspectral imaging, and low-latency downlink services are accelerating adoption. Supportive regulations, sustainability mandates, and regional consumption growth—particularly in Asia-Pacific—continue to strengthen the market’s forward trajectory.

The Satellite Imagery Tasking Solutions Market holds strategic relevance as governments, enterprises, and environmental bodies increasingly rely on high-frequency, analytics-ready geospatial data to drive operational intelligence. Advanced tasking platforms enable precision monitoring, rapid decision-making, and predictive insights across defense reconnaissance, climate response, critical infrastructure management, agriculture, and mining. AI-enabled scheduling improves task allocation accuracy by more than 40%, enabling responsive imaging across diverse orbital configurations. Comparative benchmarks show that AI-driven automation delivers a 35% improvement compared to legacy manual tasking standards.

Regional market dynamics differ: North America dominates in volume, supported by extensive satellite fleets and federal geospatial programs, while Europe leads in adoption with 61% of enterprises integrating satellite-based monitoring solutions for compliance and environmental governance. By 2027, constellation-wide AI orchestration is expected to reduce average imagery acquisition delays by 32%, strengthening real-time decision support systems. ESG commitments also shape strategic direction, with agencies and enterprises targeting 20–25% improvements in environmental monitoring accuracy by 2030.

A notable micro-scenario was recorded in 2024, when a European environmental authority achieved a 29% enhancement in deforestation detection accuracy through automated satellite tasking integrated with AI-based land analytics. These measurable outcomes underscore the sector’s significance. Looking ahead, the Satellite Imagery Tasking Solutions Market is positioned as a foundational pillar supporting national resilience strategies, regulatory compliance, and sustainable infrastructure growth worldwide.

The Satellite Imagery Tasking Solutions Market is characterized by strong demand for high-resolution imagery, rapid tasking responsiveness, and AI-enhanced scheduling frameworks. Growing deployment of multi-orbit constellations—including LEO, MEO, and GEO satellites—drives increasing imaging frequency, while industries seeking precision-driven insights fuel broader adoption. Government programs, environmental regulations, and security modernization initiatives further accelerate market evolution. Enhanced sensor capabilities, automated ground systems, and hybrid cloud geospatial platforms continue to influence operational workflows. Despite robust momentum, the market faces rising data-processing demands, evolving privacy considerations, and the need for scalable infrastructure to support expanding analytics pipelines.

Rising demand for high-frequency monitoring is a primary driver of the Satellite Imagery Tasking Solutions Market, particularly across defense, environmental, and commercial sectors. Organizations increasingly require sub-daily observations to track real-time changes, with over 58% of global Earth observation users requesting increased revisit rates for operational continuity. Advanced constellations now deliver imaging intervals below 3 hours, enhancing actionable intelligence for border management, wildfire detection, and asset monitoring. Automated tasking systems reduce manual intervention by 40–50%, improving mission throughput. The expansion of multi-sensor constellations, including SAR and hyperspectral satellites, further strengthens responsiveness. These capabilities contribute to significantly higher adoption among agencies requiring rapid situational awareness and precision-driven insights.

The Satellite Imagery Tasking Solutions Market faces constraints due to growing data volumes, limited bandwidth capacity, and evolving ground-station processing requirements. As constellations expand imaging frequency, daily data output has increased by more than 65%, putting pressure on existing infrastructure. Many regions lack adequate downlink stations, causing delays in imagery delivery. High-resolution data requires advanced processing engines and large storage capabilities, creating integration challenges for enterprises with legacy systems. Regulatory barriers tied to cross-border data transmission also restrict operational flexibility. Additionally, manual verification processes remain prevalent in certain applications, slowing workflow automation. These combined factors influence deployment timelines and operational efficiency, representing a significant restraint.

AI-driven constellation management and hyperspectral tasking present major opportunities by enabling adaptive, analytics-rich imaging pipelines. AI-based orchestration can enhance task scheduling accuracy by over 35%, optimizing satellite resource utilization and reducing idle time. Hyperspectral tasking unlocks use cases in agriculture, mineral exploration, and environmental diagnostics by capturing hundreds of spectral bands, driving demand from industries requiring high-fidelity analytics. Expanding national climate programs, smart city initiatives, and precision mapping projects amplify the opportunity. Additionally, the integration of edge processing on satellites—expected to increase by 28% over the next three years—improves real-time data output and accelerates decision cycles across commercial and government end-users.

Regulatory and security restrictions challenge the Satellite Imagery Tasking Solutions Market due to strict policies governing high-resolution imagery, orbital coordination, and cross-border data exchange. Governments impose detailed compliance requirements limiting access to sensitive imaging, particularly below specific resolution thresholds. Over 42% of enterprises report delays in tasking approvals due to regulatory bottlenecks. Cybersecurity threats also influence investment priorities, requiring advanced encryption, protected communication links, and secure data-storage frameworks. Additionally, varying national policies complicate international coverage requests, affecting multi-region tasking operations. These regulatory pressures, combined with stringent security standards, increase operational costs and prolong onboarding timelines for new users.

• Expansion of Multi-Orbit Constellation Integration: Multi-orbit configurations combining LEO, MEO, and GEO satellites are reshaping tasking strategies. Over 45% of new constellation programs are adopting hybrid-orbit approaches to enhance revisit intervals and coverage depth. These integrated architectures enable responsive tasking windows, improving continuous monitoring capabilities for defense, maritime, and climate applications.

• Growth of AI-Orchestrated Tasking Pipelines: AI-driven tasking engines are experiencing rapid adoption, with automated orchestration improving task scheduling efficiency by 38% across active constellations. These systems support predictive imaging, enabling automated prioritization of hotspots. Enterprises deploying AI-enhanced tasking reported a 27% reduction in operational delays in 2024, significantly improving data-access speed.

• Accelerated Adoption of Hyperspectral Imaging: Hyperspectral tasking demand surged by 33% as sectors such as agriculture, mining, and environmental research require data-rich spectral insights. Over 70 new hyperspectral satellites launched or planned between 2024 and 2027 indicate rising investment, especially in applications requiring chemical composition detection and precision diagnostic imaging.

• Expansion of Real-Time Downlink and Edge Processing: Real-time downlink growth of 41% is improving delivery speed for disaster response, surveillance, and logistics monitoring. The integration of edge processing on satellites allows filtering and compressing data in orbit, enabling 24–35% faster intelligence delivery. This trend is particularly evident in modernization programs across the U.S., Japan, and Europe.

The Satellite Imagery Tasking Solutions Market is segmented across types, applications, and end-users based on operational needs and technological capabilities. Tasking solutions span on-demand platforms, automated scheduling engines, AI-driven orchestration systems, and predictive tasking tools, each supporting distinct imaging frequencies and mission types. Applications include defense intelligence, environmental monitoring, disaster management, agriculture, infrastructure planning, and maritime domain awareness, driven by varied requirements for resolution, revisit time, and data integration. End-users encompass defense agencies, environmental regulators, energy companies, logistics operators, and research institutions, each leveraging tasking-enabled imagery to enhance situational awareness, regulatory compliance, and operational decision-making.

The market includes on-demand tasking platforms, automated scheduling systems, AI-driven orchestration engines, and predictive tasking algorithms. On-demand satellite tasking platforms lead the segment with 46% adoption, driven by their ability to support rapid-response imaging and high-frequency monitoring needs across defense, emergency response, and environmental agencies. Automated scheduling systems hold 29% adoption, supporting routine imaging workflows across large-scale commercial operations. Comparatively, AI-enabled orchestration engines currently account for 18%, while predictive tasking and other emerging categories represent a combined 7% share.

While on-demand platforms dominate, AI-driven orchestration engines are the fastest-growing type, expanding at 18.4% CAGR, supported by rising demand for automated priority assignment, multi-satellite coordination, and dynamic scheduling. Adoption comparisons indicate that “On-demand platforms account for 46% of usage, while automated scheduling systems hold 29%. However, AI-driven orchestration engines are rising fastest and expected to exceed 25% adoption by 2032.”

Other types, including predictive tasking algorithms and specialized niche tools, contribute to mission-specific operations such as agricultural spectral analysis, wildfire detection, and mineral exploration.

Applications include defense intelligence, environmental surveillance, disaster response, maritime monitoring, agriculture, and infrastructure assessment. Defense intelligence leads with 41% adoption, supported by strong demand for rapid-response, high-resolution imaging and integration with command intelligence systems. Environmental monitoring holds 27%, supported by rising climate risk analysis requirements. Agriculture, maritime, and infrastructure applications together account for 20%, while disaster management represents the remaining share.

Disaster response is the fastest-growing application, expanding at 17.8% CAGR due to increasing climate extremes and the need for immediate situational intelligence. Comparatively: “Defense tasking accounts for 41%, environmental monitoring 27%. However, disaster response imagery is growing fastest and expected to surpass 20% adoption by 2032.”

Key end-users include defense agencies, environmental authorities, energy & utilities, agriculture technology firms, logistics providers, and academic research bodies. Defense agencies remain the largest end-user group with 44% adoption, driven by mission-critical intelligence requirements. Environmental regulators follow with 23%, leveraging high-frequency imaging for conservation, emissions monitoring, and land management. Commercial sectors, including energy, agriculture, logistics, and infrastructure operators, collectively account for the remaining 33%.

Energy & utilities are the fastest-growing segment, expanding at 16.9% CAGR due to requirements for methane detection, pipeline surveillance, and predictive maintenance. Comparative insight: “Defense agencies account for 44%, environmental agencies 23%. However, energy & utilities adoption is rising fastest and expected to exceed 20% by 2032.”

North America accounted for the largest market share at 38%in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of ~14–16% between 2025 and 2032.

In 2024, North America registered over 38% of global satellite imagery tasking demand, primarily driven by defense agencies, commercial operators, and large-scale Earth-observation enterprises. The United States alone contributes hundreds of recurring tasking requests annually, supported by more than 150 ground stations. Meanwhile, Asia-Pacific is seeing surging interest from China, India, and Southeast Asia, with national space programs planning to task more than 120 new small satellites between 2025–2032. European nations (e.g., Germany, France, UK) also account for about 25% of the tasking volume, increasingly using imagery for environmental and infrastructure monitoring. Latin America and Middle East & Africa together contribute the remaining ~10–12%, with emerging markets like Brazil and UAE investing in tasking-enabled geospatial intelligence for climate and resource management.

How Is the Geospatial Intelligence Leadership Reinforcing Real-Time Tasking Demand?

North America commands approximately 38% of the global satellite imagery tasking market, with strong demand from defense, intelligence, and commercial surveillance sectors. In the U.S., major satellite operators and intelligence agencies collaborate on priority tasking, while private firms offer on-demand APIs. Regulatory and government support are evident in the modernization of downlink infrastructure and secure geospatial data policies. Technological transformation includes adoption of AI-driven orchestration, multi-constellation scheduling, and cloud-native tasking platforms. For example, U.S.-based providers are scaling low-latency scheduling to support critical infrastructure and disaster-response use cases. Regional users also exhibit high enterprise adoption of real-time imagery workflows, particularly in sectors like energy, agriculture, and smart city planning.

Why Are ESG and Compliance Driving Tasking Adoption Across European Space Programs?

Europe holds roughly 25% of the imagery tasking market, with major hubs in Germany, France, and the UK. National space agencies and the European Space Agency (ESA) promote shared tasking infrastructure to support environmental monitoring and urban planning. European customers increasingly demand explainable AI in scheduling frameworks, and tasking platforms must conform to strict data-privacy and ESG mandates. Emerging technologies in this region include federated learning across satellite networks and advanced scheduling engines for sustainability missions. A European provider recently launched a priority tasking service for renewable energy monitoring across multiple EU states. Institutional decision-makers in Europe favor high-transparency, regulation-ready tasking platforms that align with climate and security policy.

How Is Rapid Satellite Launch Activity Driving Tasking Innovation in Key Asia-Pacific Nations?

Asia-Pacific is emerging as the fastest-growing region for satellite imagery tasking, with major demand from China, India, and Japan. With hundreds of small satellites being planned or launched, the region’s tasking volume is growing rapidly. National space programs are investing heavily in ground-station infrastructure, cloud-based geospatial services, and AI-powered tasking software. Local players are building responsive tasking systems for agriculture mapping, urban development, and disaster resilience. In China, tasking companies are providing automated revisit scheduling for farmland and mining surveillance, while Indian geospatial firms are integrating tasking APIs with flood-monitoring platforms. Regional consumer behavior shows a clear preference for integrated platforms that combine imagery request, analysis, and delivery in a single cloud-native interface.

How Are Latin American AgTech and Infrastructure Firms Accelerating Tasking Use in Emerging Markets?

In South America, countries like Brazil and Argentina are driving the adoption of satellite imagery tasking for precision agriculture, deforestation tracking, and infrastructure monitoring. The region accounts for approximately 6% of global tasking volume. Governments are incentivizing satellite-tasked imagery for land-use planning and natural-resource management, supported by trade policies and public-private partnerships. Local satellite service providers offer low-cost imaging packages tailored for agricultural cooperatives. Consumer behavior is shaped by language localization, with providers building Spanish- and Portuguese-language tasking interfaces, plus mobile-accessible dashboards for rural stakeholders.

How Are Emerging Economies in the Middle East & Africa Leveraging Tasked Imagery for Resource Management?

Middle East & Africa represent around 4% of the global satellite imagery tasking market, with emerging adoption in the UAE, Saudi Arabia, and South Africa. Regional demand is driven by sectors such as oil & gas, construction, urban planning, and environmental sustainability. Key technological modernization efforts involve cloud-native tasking platforms, AI-based prioritization, and cross-border data-sharing agreements. Local players are teaming with governments to provide secure tasking for infrastructure surveillance and natural resource mapping. Behavioral patterns show increasing adoption among state agencies and private enterprises focused on sustainable development and strategic investment in space-enabled intelligence.

United States – ~38% share: Dominance due to advanced taskable constellations, high governmental demand, and mature geospatial infrastructure.

China – ~15% share: Rapid expansion driven by national space program, strong commercial tasking ecosystem, and large-scale Earth observation initiatives.

The Satellite Imagery Tasking Solutions market features over 30 active global providers, including legacy operators and rapidly scaling small-satellite firms. The market is moderately concentrated: the top five players—such as Maxar Technologies, Planet Labs, Airbus Intelligence, ICEYE, and BlackSky—together command an estimated 45–55% of the total tasking capacity. Strategic initiatives seen in 2023–2024 include several major partnerships, such as satellite operators collaborating with cloud-service companies to deliver on-demand tasking APIs and integrating AI orchestration into scheduling engines. Providers are also expanding ground-station coverage, enhancing multi-orbit coordination, and launching subscription-based tasking services. Innovation trends emphasize onboard AI scheduling, federated tasking frameworks across satellite constellations, and low-latency downlinks. Some firms are targeting ESG-driven tasking use cases, such as emissions monitoring and deforestation tracking, teaming with public agencies and investors. Meanwhile, emerging constellations from startups are competing by offering low-cost tasking bundles and flexible revisit packages.

Maxar Technologies

ICEYE

Satellogic

Capella Space

L3Harris Technologies

Yahsat / Al Yah Satellite Communications

Albedo Space

HawkEye 360

Satrec Initiative

Spire Global

Surrey Satellite Technology Ltd.

Satellite Imagery Tasking Solutions are being revolutionized by a number of cutting-edge technologies that greatly enhance precision, responsiveness, and cost-efficiency. A key technology is on-board artificial intelligence, which enables satellites to filter and prioritize scenes in real time, reducing downlink burden and improving the value of the data transmitted. Federated learning frameworks further optimize the system by enabling shared learning across multiple satellites and ground stations without centralized data transfer, preserving data sovereignty and lowering latency.

Edge computing aboard satellites is reducing the volume of data that must be transmitted to earth, with up to 30–40% of imagery being filtered pre-downlink. This not only lowers bandwidth costs but also accelerates mission-critical data delivery for time-sensitive applications like emergency response or defense surveillance. Meanwhile, AI-based scheduling algorithms, deployed on cloud platforms or ground-station control systems, dynamically allocate tasking requests based on priority, orbital geometry, and user-defined criteria — increasing tasking efficiency significantly.

Another important innovation is multi-sensor fusion, where tasking platforms coordinate across optical, synthetic aperture radar (SAR), and hyperspectral satellites to generate richer, complementary data sets. This fusion supports better target detection, analytics, and context-aware tasking for industries like agriculture, infrastructure, and climate science. Security and encryption technologies are also critical, with modern tasking platforms implementing end-to-end encryption, secure API access, and provenance tracking to meet the stringent requirements of defense and intelligence users.

Finally, real-time orchestration platforms powered by predictive analytics allow users to submit tasking requests, model satellite availability, and simulate revisit windows via web interfaces. These platforms often support multi-constellation integration, enabling optimized task routing across different satellite providers. Combined, these technologies are redefining how organizations request, prioritize, and consume satellite imagery, enabling scalable, responsive, and mission-driven tasking solutions.

• In July 2024, Planet Labs launched its latest priority tasking API for its high-revisit Pelican constellation, reducing user wait time for directed imaging by 25%. Source: www.planet.com

• In August 2023, ICEYE introduced an enhanced radar-tasking product that supports guaranteed revisit windows for its SAR satellites over disaster-prone regions. Source: www.iceye.com

• In November 2023, BlackSky partnered with a global cloud provider to integrate its real-time tasking engine into a shared geospatial data platform, enhancing global task planning. Source: www.blacksky.com

• In May 2024, Airbus Intelligence deployed a multi-orbit tasking orchestration system that coordinates LEO and GEO satellites to optimize revisit efficiency for environmental and intelligence missions. Source: www.space-solutions.airbus.com

The scope of this market report encompasses tasking solution types (on-demand, automated scheduling, AI orchestration, predictive prioritization), applications (defense/intelligence, environmental monitoring, agriculture, disaster response, infrastructure), and end-user segments (government agencies, commercial geospatial analytics firms, energy, utilities, academic and research institutions). It evaluates enabling technologies such as onboard AI, edge computing, federated learning, and multi-sensor fusion, as well as ground infrastructure including global ground stations and cloud platforms for task orchestration.

Geographically, the report analyzes demand across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, scrutinizing satellite fleet density, ground-station capacity, regulatory frameworks, and user adoption patterns in each region. The business models studied include subscription-based tasking, pay-as-you-go scheduling, managed priority service tiers, and enterprise integration of tasking APIs. Strategic insights address vendor positioning, investment activity, partnership trends, and future developments in autonomy, sustainable tasking, and real-time intelligence. The report is tailored for decision-makers in satellite operations, defense agencies, environmental organizations, and commercial enterprises seeking scalable, responsive, and data-driven imagery tasking solutions.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 3,530.7 Million |

|

Market Revenue in 2032 |

USD 9,188.7 Million |

|

CAGR (2025 - 2032) |

12.7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Planet Labs, Maxar Technologies, Airbus Intelligence, ICEYE, BlackSky, Satellogic, Capella Space, L3Harris Technologies, Yahsat / Al Yah Satellite Communications, Albedo Space, HawkEye 360, Satrec Initiative, Spire Global, Surrey Satellite Technology Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |