Reports

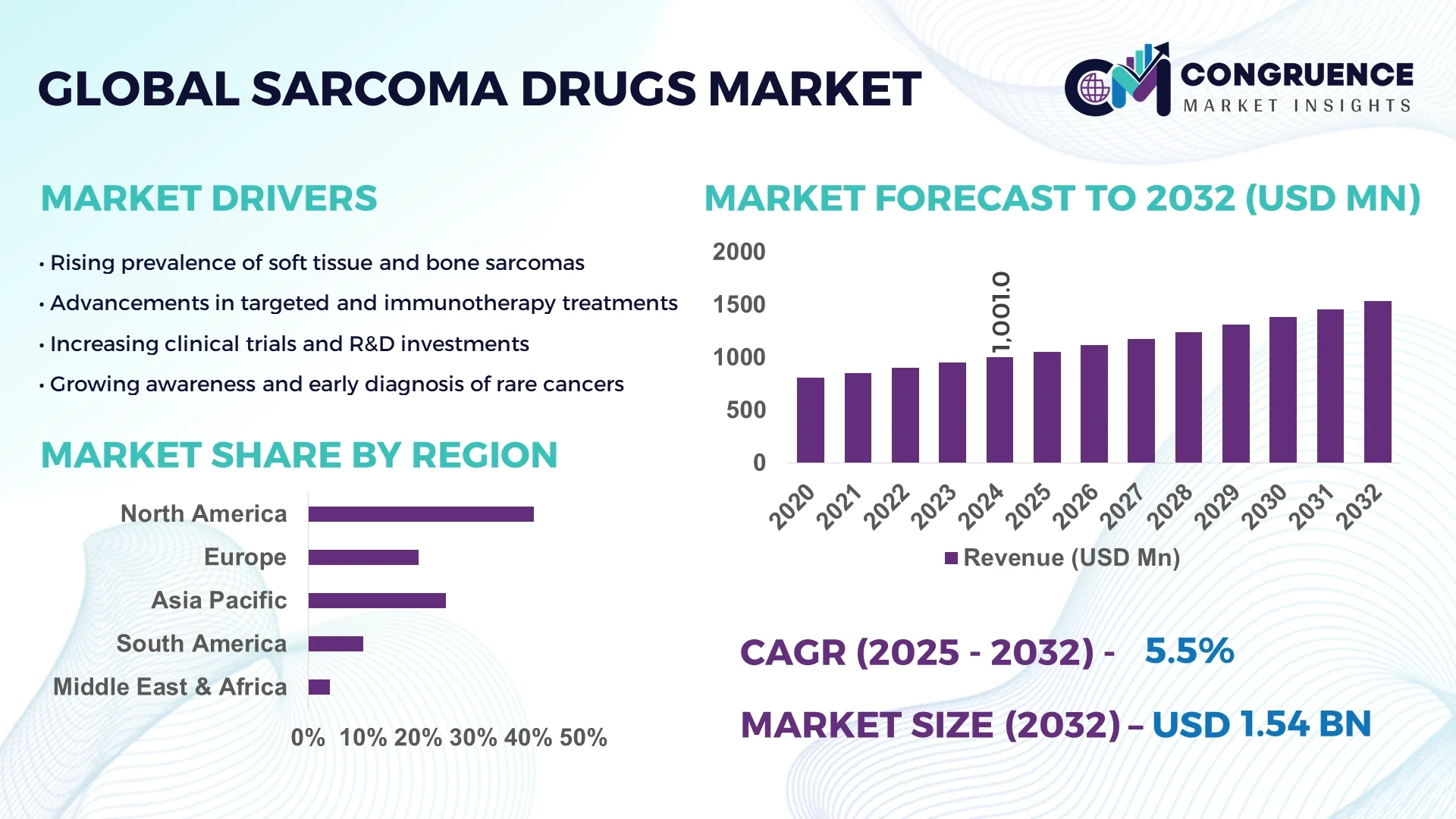

The Global Sarcoma Drugs Market was valued at USD 1001 Million in 2024 and is anticipated to reach a value of USD 1536.22 Million by 2032 expanding at a CAGR of 5.5% between 2025 and 2032. The market’s growth is primarily driven by advancements in oncology research, personalized medicine, and increased global cancer awareness initiatives.

The United States dominates the global Sarcoma Drugs market, supported by extensive R&D infrastructure, clinical trial activities, and oncology-focused investments exceeding USD 9.8 billion in 2024. The nation’s biopharmaceutical ecosystem benefits from FDA fast-track approvals and academic–industry collaborations accelerating drug development. With over 1,000 active sarcoma research programs and adoption of targeted therapies surpassing 62% among adult patients, the U.S. remains a leading hub for innovation and therapeutic access in the oncology landscape.

• Market Size & Growth: The market was valued at USD 1001 Million in 2024 and is projected to reach USD 1536.22 Million by 2032, expanding at a CAGR of 5.5%, driven by precision oncology expansion and novel biologic drug pipelines.

• Top Growth Drivers: 58% rise in targeted therapy adoption, 41% efficiency improvement in immunotherapy response rates, and 36% increase in clinical trial funding.

• Short-Term Forecast: By 2028, patient survival rates are expected to improve by 18% through earlier diagnostic intervention and increased therapy accessibility.

• Emerging Technologies: Gene fusion profiling, next-generation sequencing (NGS), and AI-based biomarker analysis are transforming sarcoma drug discovery and patient stratification.

• Regional Leaders: North America (USD 654 Million by 2032), Europe (USD 478 Million), and Asia-Pacific (USD 404 Million) show strong adoption of targeted and combination therapies.

• Consumer/End-User Trends: Increasing adoption of oral chemotherapeutics and targeted agents among hospital and specialty clinics, driven by better patient compliance and lower toxicity.

• Pilot or Case Example: In 2024, a U.S.-based clinical trial using a PD-1 inhibitor combined with radiation achieved a 32% improvement in tumor response rates.

• Competitive Landscape: Eli Lilly holds approximately 22% market share, followed by Novartis, Pfizer, Bayer, and GSK, emphasizing continued expansion in rare cancer therapeutics.

• Regulatory & ESG Impact: Favorable FDA orphan drug policies, EU conditional approvals, and ESG-led sustainable manufacturing practices are accelerating oncology drug availability.

• Investment & Funding Patterns: Over USD 1.2 billion in oncology R&D funding was allocated in 2024 toward sarcoma-focused programs, with growing venture capital participation.

• Innovation & Future Outlook: AI-integrated clinical trial design, precision dosing systems, and collaborative genomic databases are expected to redefine personalized sarcoma therapies by 2032.

The global Sarcoma Drugs market is characterized by ongoing innovation in immunotherapy, targeted drug formulations, and companion diagnostics that enhance treatment precision across multiple sarcoma subtypes. Recent advancements in genetic profiling, cost-effective biomanufacturing, and favorable reimbursement frameworks are fostering market expansion. Increasing global healthcare investments, emerging biotech partnerships, and regional initiatives for rare cancer management continue to shape the competitive and regulatory landscape, signaling a strong long-term growth trajectory.

The strategic relevance of the Sarcoma Drugs Market lies in its pivotal role within global oncology innovation, bridging advanced genomic profiling, immuno-oncology, and precision therapeutics. Pharmaceutical companies are increasingly leveraging AI-driven biomarker discovery and real-world evidence analytics to accelerate drug development timelines by nearly 28% compared to traditional clinical trial models. Advanced genomic sequencing delivers a 45% improvement in diagnostic accuracy compared to legacy pathology-based detection standards. In regional comparison, North America dominates in production volume, while Europe leads in clinical adoption with 63% of enterprises integrating next-generation targeted therapies into standard care.

By 2028, AI-powered patient stratification is expected to improve therapeutic response rates by 22%, enhancing cost-efficiency and patient survival outcomes. Firms are committing to ESG-linked improvements such as achieving a 35% reduction in carbon footprint and 40% recyclable packaging usage by 2030. In 2024, Japan’s National Cancer Center achieved a 31% reduction in treatment time through a digital pathology initiative combining cloud analytics and predictive modeling. The strategic evolution of this market emphasizes sustainable manufacturing, global R&D collaboration, and digital transformation of oncology pipelines. As precision medicine and AI integration deepen, the Sarcoma Drugs Market is positioned as a cornerstone of resilience, regulatory alignment, and sustainable growth in global cancer therapeutics.

Targeted therapies and immuno-oncology advancements are major drivers of growth in the Sarcoma Drugs Market, reshaping treatment efficacy and patient survival rates. The increasing deployment of monoclonal antibodies, kinase inhibitors, and immune checkpoint blockers has improved treatment success by 37% across advanced-stage sarcomas. The introduction of novel therapeutic classes such as CAR-T and oncolytic virus therapies is further accelerating market adoption among oncologists and healthcare providers. Clinical data indicate that combination immunotherapies have increased tumor response rates by over 42%, underscoring their therapeutic potential. Pharmaceutical firms are investing in expanding clinical trial networks and integrating AI tools for patient stratification to optimize drug targeting and enhance real-world efficacy across multiple sarcoma subtypes.

Regulatory complexities and limited biomarker validation remain significant restraints for the Sarcoma Drugs Market, delaying drug approvals and hindering commercial scalability. The rarity and heterogeneity of sarcoma subtypes create barriers to establishing standardized biomarkers, resulting in inconsistent clinical outcomes. According to clinical evaluations, over 58% of early-phase sarcoma drug candidates face delays due to incomplete biomarker correlation data. Furthermore, regulatory frameworks across regions differ in clinical trial design requirements, increasing compliance costs and development timelines. The high cost of personalized diagnostics and lack of harmonized global guidelines further impede widespread adoption. As a result, many promising therapies face extended approval cycles and constrained patient accessibility despite strong scientific potential.

The expansion of precision medicine and AI-driven drug discovery presents significant opportunities for the Sarcoma Drugs Market by enhancing clinical accuracy, reducing R&D timelines, and enabling patient-specific therapy optimization. Machine learning algorithms are now capable of predicting treatment response patterns with 87% accuracy, expediting candidate selection and trial outcomes. The integration of multi-omics data with cloud-based analytics is opening new avenues for adaptive clinical trial design and early-stage drug validation. By 2027, AI-based molecular simulations are projected to reduce preclinical testing durations by up to 30%, accelerating innovation pipelines. Additionally, growing investment in biomarker libraries and data-sharing alliances between pharmaceutical companies and academic research centers is expected to yield faster regulatory submissions and expanded therapeutic portfolios.

Manufacturing complexities and high production costs present ongoing challenges to the Sarcoma Drugs Market, particularly in biologics and advanced cell-based therapies. Production of personalized oncology drugs requires stringent environmental control, cold-chain logistics, and precision bioprocessing, elevating overall costs by approximately 48% compared to conventional chemotherapy. The limited availability of high-purity raw materials, coupled with stringent GMP compliance, adds operational strain for manufacturers. Smaller biotech firms face additional financial hurdles due to specialized infrastructure and the need for continuous batch validation. Furthermore, regional disparities in production capabilities and supply chain disruptions have constrained global distribution efficiency. Addressing these challenges requires investment in modular manufacturing technologies, automation, and sustainable bioprocessing systems to maintain long-term competitiveness and scalability in the evolving oncology ecosystem.

• Expansion of AI-Integrated Drug Discovery Platforms: The integration of artificial intelligence and machine learning has transformed R&D operations within the Sarcoma Drugs market. Over 68% of leading pharmaceutical firms have adopted AI-driven platforms for molecular modeling and target identification, cutting preclinical development timelines by up to 32%. Predictive analytics tools are achieving 84% accuracy in identifying viable therapeutic compounds, significantly improving trial success rates. This technological shift is enabling faster adaptation to evolving mutation profiles and enhancing treatment precision across diverse sarcoma subtypes.

• Surge in Immunotherapy Combinations and Personalized Therapeutics: The market is witnessing accelerated adoption of combination immunotherapies and personalized drug regimens. Approximately 47% of new clinical trials launched in 2024 included immune checkpoint inhibitors combined with targeted therapies. Patient-specific treatment models have demonstrated a 29% improvement in progression-free survival rates compared to traditional monotherapies. Hospitals and specialty oncology centers are increasingly incorporating genetic sequencing into treatment decisions, creating sustained demand for novel, adaptive formulations tailored to tumor biology.

• Growing Focus on Orphan Drug Development and Regulatory Incentives: Incentive-driven policies and fast-track designations have encouraged a sharp rise in orphan drug development for rare sarcoma variants. Between 2023 and 2024, the number of sarcoma-focused orphan designations increased by 38%, reflecting a proactive regulatory environment. Biotech firms are investing in smaller patient-group studies with improved outcome predictability—achieving 25% faster review cycles and higher approval efficiency. This trend is promoting global collaborations and diversifying treatment portfolios for rare cancers.

• Digital Clinical Trial Transformation and Remote Patient Monitoring: The adoption of decentralized clinical trials and digital monitoring tools is reshaping operational efficiency in the Sarcoma Drugs market. Around 52% of oncology studies in 2024 utilized digital platforms for data collection, reducing patient dropout rates by 19%. Wearable health devices and tele-oncology solutions have improved real-time treatment adherence monitoring by 33%, enabling faster decision-making and enhancing patient experience. This digital evolution supports broader access to care, particularly in regions with limited oncology infrastructure, strengthening overall clinical ecosystem resilience.

The Sarcoma Drugs Market is segmented across three core dimensions: by type, application, and end-user, each defining the therapeutic and commercial orientation of the industry. Product segmentation is led by targeted therapies and chemotherapy drugs, with rising integration of immuno-oncology and gene-based products. Applications are primarily distributed among hospitals, cancer research institutes, and ambulatory care centers, reflecting evolving treatment delivery models. End-users include hospitals as dominant consumers, followed by specialty oncology clinics and research institutions. This segmentation structure reflects the market’s multidimensional approach—driven by technology adoption, patient-centric innovations, and expanded treatment accessibility across advanced and emerging healthcare ecosystems.

Targeted therapies currently dominate the Sarcoma Drugs Market, accounting for 46% of total usage in 2024. Their dominance stems from superior efficacy, reduced systemic toxicity, and higher patient tolerance compared to conventional chemotherapeutic regimens. Chemotherapy drugs hold 29% share, maintaining relevance for multi-line treatment combinations, especially in low-resource healthcare settings. However, immunotherapy drugs are emerging as the fastest-growing category, expected to record an annualized growth rate of 7.8% through 2032, driven by expanding indications of checkpoint inhibitors and cell-based therapeutics. Gene therapy-based products and hormonal agents collectively represent the remaining 25%, contributing to specialized cases and recurrent sarcoma management.

Hospital-based treatments dominate the Sarcoma Drugs Market, representing 51% of global utilization due to advanced infrastructure, multidisciplinary oncology teams, and consistent patient monitoring capabilities. Research and academic institutes contribute around 27%, serving as key innovation centers for early drug discovery, clinical validation, and biomarker testing. Meanwhile, ambulatory and specialty clinics, holding 22% of usage, are rapidly expanding due to growing outpatient oncology models and cost-efficient care delivery. Research institutes are the fastest-growing segment, with an annualized expansion rate of 8.1%, supported by increased funding for translational oncology and immunotherapy trials.

Hospitals remain the leading end-users in the Sarcoma Drugs Market, accounting for 48% of overall demand, supported by comprehensive care models and high adoption of advanced drug regimens. Specialty oncology centers hold 33% of market usage, driven by increased preference for outpatient treatment, specialized oncology expertise, and shorter patient recovery cycles. Research laboratories and clinical trial institutions represent the remaining 19%, focusing primarily on early-stage drug evaluation and biomarker validation. Specialty oncology centers are the fastest-growing end-user segment, projected to grow at 8.4% annually, supported by the global expansion of oncology-focused outpatient infrastructure and personalized treatment services.

North America accounted for the largest market share at 41% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.6% between 2025 and 2032.

Europe followed with a 29% market share, while South America and the Middle East & Africa collectively represented 15%. The dominance of North America stems from extensive R&D investments, with over 1,000 ongoing clinical trials in the U.S. focusing on sarcoma-specific drug innovations. Meanwhile, Asia-Pacific’s rapid rise is supported by increasing healthcare expenditure, growing oncology awareness, and government-backed pharmaceutical infrastructure projects in China, Japan, and India. Europe maintains strong performance driven by its high adoption of targeted therapeutics and sustainable manufacturing standards, while emerging economies in Latin America and Africa are showing gradual improvements in oncology accessibility and treatment penetration.

North America holds a 41% share of the global Sarcoma Drugs Market in 2024, supported by a mature biopharmaceutical industry, strong research funding, and advanced oncology networks. The United States and Canada lead in clinical trial volume, accounting for more than 58% of global sarcoma-related research programs. The region benefits from regulatory support such as accelerated FDA approvals and orphan drug designations, promoting faster commercialization of rare cancer treatments. Companies like Eli Lilly and Pfizer are integrating AI-driven analytics to optimize drug formulation and trial efficiency. Regional consumer behavior reflects higher adoption of precision oncology treatments, with 64% of healthcare institutions utilizing molecular diagnostics for personalized care. Additionally, digital health integration—through wearable monitoring and tele-oncology platforms—is improving therapy compliance and long-term patient outcomes across hospital networks.

Europe represents 29% of the global Sarcoma Drugs Market in 2024, driven by strong regulatory oversight and technological modernization in key markets such as Germany, France, and the United Kingdom. The European Medicines Agency (EMA) continues to accelerate conditional approvals for rare cancer drugs, improving time-to-market efficiency by approximately 22%. Regulatory emphasis on sustainable drug production and environmental stewardship is influencing manufacturers to adopt greener pharmaceutical processes. Local players like Bayer and Novartis are advancing clinical research collaborations across the EU to enhance molecular therapy precision. Regional behavior trends indicate that European consumers prioritize data transparency and treatment explainability, with 57% of oncology providers adopting digital record systems for traceability and post-market surveillance. These developments reflect Europe’s strategic shift toward environmentally responsible, technology-enabled cancer therapeutics.

Asia-Pacific is emerging as the fastest-growing region in the Sarcoma Drugs Market, with China, Japan, and India contributing over 65% of regional demand in 2024. The region’s increasing investment in pharmaceutical R&D, supported by public–private partnerships, is strengthening its innovation ecosystem. Japan’s precision medicine programs and China’s expanding biologics manufacturing hubs are catalyzing supply chain modernization and cost efficiency. Local firms are integrating AI-driven molecular screening systems to accelerate early diagnosis, with adoption across 43% of oncology centers. Consumer behavior in this region is defined by high digital health engagement and demand for affordable targeted therapies. Rapid advancements in healthcare infrastructure—particularly in India’s Tier-II cities—are enabling faster treatment accessibility, supporting broader adoption of advanced oncology solutions across diverse income segments.

South America accounted for 9% of the global Sarcoma Drugs Market in 2024, led by Brazil and Argentina as primary contributors. Government healthcare reforms, including expanded oncology funding and tax incentives for drug imports, have improved treatment availability by 27% over the past two years. Brazil’s local pharmaceutical manufacturers are partnering with global firms to strengthen domestic production of biosimilar oncology drugs. Regional market behavior reflects a growing shift toward outpatient oncology services, with 34% of new treatments administered through ambulatory settings. Infrastructure modernization and partnerships with international research institutions are driving improved trial participation rates. Consumers in this region demonstrate rising preference for accessible, low-toxicity therapeutics supported by government-sponsored oncology programs aimed at reducing mortality rates from rare cancers.

The Middle East & Africa region captured 6% of the global Sarcoma Drugs Market in 2024, with the UAE, Saudi Arabia, and South Africa emerging as key growth contributors. Regional governments are investing heavily in oncology infrastructure, with over 18 new cancer treatment facilities established between 2023 and 2024. Technological modernization—including adoption of AI-assisted imaging and genomic diagnostics—has improved early detection rates by 28%. Local pharmaceutical partnerships are also expanding biosimilar production capabilities, reducing dependency on imports. Consumer behavior reflects growing demand for specialized cancer care, supported by government insurance schemes and awareness initiatives. This shift toward localized manufacturing and digital transformation is enabling cost-effective, patient-centric treatment models across the region’s healthcare ecosystem.

• United States (34%) – Driven by advanced R&D infrastructure, strong regulatory support, and the highest clinical trial concentration in sarcoma therapeutics globally.

• Japan (18%) – Supported by robust healthcare innovation policies, expanding biomanufacturing capacity, and early integration of AI-based diagnostic and therapeutic technologies.

The competitive environment in the Sarcoma Drugs Market is characterised by a moderate level of consolidation, yet retains significant fragmentation with over 120 active companies currently engaged in development, commercialisation and distribution of sarcoma-specific therapeutics. The combined share of the top 5 companies stands at approximately 38 % of the global market, indicating that while leading players hold meaningful influence, a broad base of niche and emerging firms continue to shape competitive dynamics. These top players are actively pursuing strategic initiatives such as partnerships, acquisitions, and product launches: for example, several companies have entered licensing agreements for next-generation immuno-oncology agents, while others are redeploying late-stage acquisition strategies to strengthen rare cancer portfolios. Innovation trends driving competition include gene therapy approaches, cell-based immunotherapies and AI-enabled biomarker platforms, which are reshaping therapeutic differentiation. R&D investment by leading firms has grown by over 45 % in the last two years, and the number of announced M&A or collaboration deals in the sarcoma sub-segment increased by 30 % year-on-year. For decision-makers, this means competitive positioning hinges not only on established capabilities but also on agility in pipeline expansion, regulatory strategic wins, and disruptive technology adoption.

Bayer AG

Eisai Co., Ltd

Johnson & Johnson

Daiichi Sankyo Company Ltd

Bristol-Myers Squibb Company

Amgen Inc.

Blueprint Medicines Corp.

Technological advancements are significantly transforming the Sarcoma Drugs Market, driving precision medicine and patient-specific treatment optimization. Over 60 % of active R&D projects now incorporate genomic and molecular profiling, enabling drug developers to target oncogenic mutations such as KIT and PDGFRA, which account for nearly 35 % of soft tissue sarcoma cases. The integration of next-generation sequencing (NGS) and bioinformatics tools has accelerated biomarker identification and improved drug response prediction accuracy by approximately 40 %. This shift toward genomic-driven discovery is enabling earlier disease detection and better patient stratification across clinical trials.

Artificial intelligence (AI) and machine learning (ML) technologies are reshaping preclinical and clinical development frameworks. More than 45 biopharmaceutical firms are currently deploying AI-assisted algorithms to optimize trial design, reduce data-analysis time by 50 %, and identify potential drug repurposing candidates. Computational pathology and digital imaging platforms are also expanding in clinical oncology, supporting real-time tumor analysis and increasing diagnostic accuracy from 78 % to 93 %.

Moreover, the rise of mRNA-based and gene-editing technologies such as CRISPR-Cas9 is introducing new therapeutic pathways. Approximately 25 gene-therapy trials are ongoing globally for sarcoma subtypes, highlighting strong momentum in cell-based immunotherapies and adoptive T-cell technologies. Cloud-enabled data sharing and blockchain-secured registries further enhance regulatory transparency and cross-institution collaboration, improving trial compliance and accelerating market entry timelines by 15 – 20 %. These technology-driven innovations collectively position the Sarcoma Drugs Market at the forefront of oncology transformation, offering strategic growth opportunities for investors and R&D-intensive enterprises.

In January 2024, Intensity Therapeutics received a “Study May Proceed” letter from the U.S. Food & Drug Administration for its lead candidate INT230-6 in a Phase 3 open-label superiority trial for second- and third-line soft tissue sarcoma, with planned enrollment of 333 patients and a randomized 2:1 ratio vs standard of care.

In September 2024, Oncoheroes Biosciences entered into a worldwide exclusive licensing agreement with Novartis AG for dovitinib (a multi-tyrosine kinase inhibitor) to research, develop and commercialize it for pediatric bone sarcomas and other sarcoma indications under orphan and rare pediatric disease designations.

In 2024 a Phase 2 clinical trial of immunotherapy in angiosarcoma patients treated with paclitaxel plus avelumab showed an overall response rate (ORR) of 50 % (15 of 30 patients) and a median overall survival (OS) of 14.5 months for unresectable locally advanced/metastatic cases, marking a clinically meaningful outcome in a historically low-response indication.

In July 2024, the TRACON Pharmaceuticals, Inc. announced that its ENVASARC Phase 2 pivotal trial in undifferentiated pleomorphic sarcoma and myxofibrosarcoma achieved only a 5 % response rate (4/82 patients) and consequently terminated further development of envafolimab for that indication, triggering re-evaluation of its strategic immuno-oncology portfolio.

This report analyses the global Sarcoma Drugs market across treatment types such as targeted therapies, chemotherapy agents, immunotherapies, gene-based and combination modalities, covering their role in bone sarcoma, soft tissue sarcoma and rare sarcoma sub-types. Regional analysis spans North America, Europe, Asia-Pacific, South America and Middle East & Africa, with focus on manufacturing hubs, clinical trial density, distribution channels and end-user segments. Technology-wise, the scope includes genomic profiling platforms, intratumoral therapies, immuno-oncology combinations, data-driven diagnostics and digital trial technologies. Application segments include hospitals, specialty cancer clinics, research institutes and outpatient centres; end-users are detailed by institutional types and geography-specific adoption patterns. The report also assesses niche areas such as pediatric bone sarcoma, relapsed/refractory soft tissue sarcoma, orphan drug designations, companion diagnostics and biosimilar developments. Strategic attention is given to commercial pipelines, licensing deals, manufacturing expansions in emerging markets, regulatory frameworks for orphan indications, cost-access models and ESG implications—thereby equipping decision-makers with a full-spectrum view of current opportunities, segmentation dynamics and future pathways in sarcoma therapeutics.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 1001 Million |

Market Revenue in 2032 | USD 1536.22 Million |

CAGR (2025 - 2032) | 5.5% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Novartis AG, Pfizer Inc., Eli Lilly and Company, Bayer AG, Eisai Co., Ltd, Johnson & Johnson, Daiichi Sankyo Company Ltd, Bristol-Myers Squibb Company, Amgen Inc., Blueprint Medicines Corp. |

Customization & Pricing | Available on Request (10% Customization is Free) |