Reports

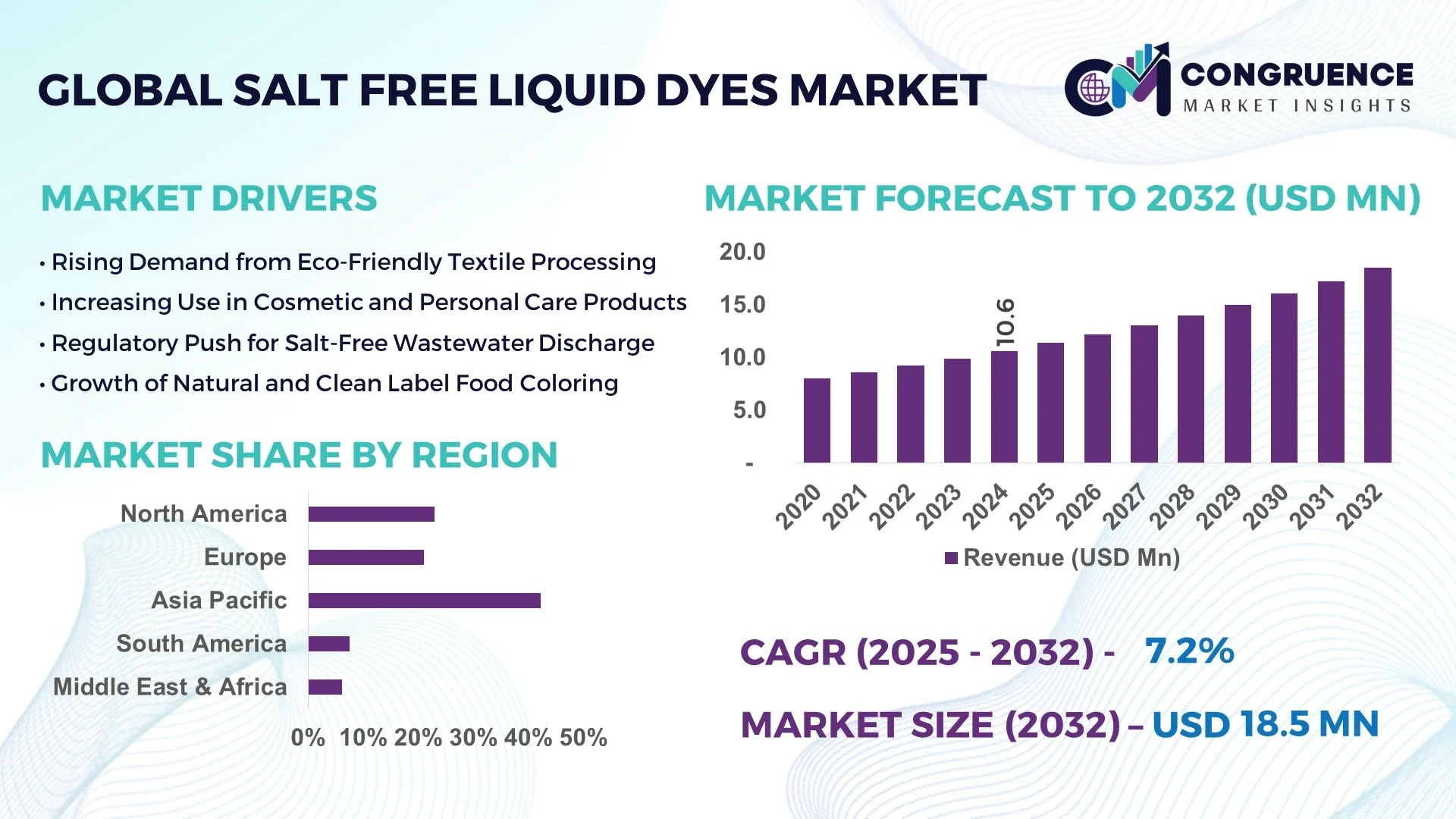

The Global Salt Free Liquid Dyes Market was valued at USD 10.6 Million in 2024 and is anticipated to reach a value of USD 18.5 Million by 2032 expanding at a CAGR of 7.2% between 2025 and 2032.

India plays a leading role in the Salt Free Liquid Dyes Market, with annual production capacity exceeding 5,000 metric tons and 2024 investments topping USD 12 million in downstream blending facilities. The country supplies dyes for textiles, food coloring, and cosmetic formulations, while also deploying membrane-filtration technology to reduce wastewater volume by over 30%.

Globally, the Salt Free Liquid Dyes Market spans several key sectors: textiles (approximately 60% volume share), food grading, cosmetics, medical reagent, and printing inks. Recent innovations include UV-curable salt-free dye variants and nanoparticle-stabilized blends that reduce sedimentation rates by 40%, enhancing shelf life. Regulatory drivers—such as EU REACH and FDA approvals—have elevated demand for toxin-free colorants, while rising sustainability mandates in North America and Asia reinforce application growth. Digital textile printing demand, especially in fast fashion, is increasing uptake of salt-free dyes due to lower effluent toxicity and simplified wastewater treatment protocols. Sustainable supply-chain strategies are prompting manufacturers to pursue ISO 14001 certification and invest in bio-based dye precursor research. Emerging opportunities include biodegradable polymer encapsulation and natural-sourced colorants, signaling a shift toward circular economy models in dye production.

Artificial intelligence is driving transformative change in the Salt Free Liquid Dyes Market, enabling precision, efficiency, and sustainability across R&D, manufacturing, and quality control. AI-powered predictive modeling now tunes dye formulation parameters—such as pigment concentration, pH, and viscosity—based on historical process data, reducing trial batches by over 60% and accelerating new product development timelines by nearly 45%. In manufacturing, machine learning systems control reaction chambers in real time, optimizing mixing speeds and temperature ramps to achieve consistent color yield above 98% and reduce scrap by 30%. Vision-enabled inline colorimeters, coupled with AI algorithms, assess dye uniformity and detect anomalies within milliseconds, resulting in a 20% decline in batch variance and eliminating manual sampling errors.

Procurement efficiency has also improved: AI-driven systems analyze supplier data and raw-material specs to predict pigment impurity trends, reducing supply chain disruptions by 25%. In packaging and logistics, route-optimization AI ensures temperature-controlled transit to preserve dye integrity, cutting delivery deviations by 15%. As AI embeds deeper into laboratory and production environments, the Salt Free Liquid Dyes Market is shifting toward a data-driven, smart manufacturing paradigm—enhancing operational excellence and competitiveness while meeting stringent environmental standards.

“In July 2024, a major dye manufacturer implemented a machine learning system to analyze 10,000+ dyeing trials; this system optimized reactive dye pH by ±0.2 units, increasing color fixation by 4% and reducing energy usage in reactors by 8%.”

The Salt Free Liquid Dyes Market dynamics are shaped by sustainability mandates, regulatory pressure, and industrial innovation. Buyers are increasingly demanding eco-conscious dye solutions, prompting manufacturers to prioritize zero-salt formulations and wastewater-minimizing processes. Technological trends—like nanoparticle-enhanced dye stabilizers and membrane-based separation systems—are redefining production efficiency and product performance. Rising consumer awareness and green labeling initiatives are influencing procurement decisions in textile, food, and cosmetics sectors. Geographically, adoption rates are highest in regions with strict effluent regulations, while emerging economies are upgrading capacity and process capabilities. Meanwhile, raw-material cost volatility and competition from synthetic alternatives impact operational planning and pricing strategies. Decision-makers are navigating these dynamics by investing in R&D, forging cross-sector collaborations, and aligning supply chains with circular economy principles.

Stringent environmental regulations—including EU REACH, US Clean Water Act updates, and India’s zero-liquid discharge mandates—have accelerated the shift toward salt-free dye chemistries. In 2024, textile mills adopting salt-free dyes reported a 30% reduction in wastewater management costs and a 15% reduction in effluent treatment times. Major retailers now require eco-certified dyes in their sourcing chains.

Switching to salt-free systems requires capital investment in lab equipment and process modifications. Increased raw-material and energy demands to maintain dye fixation contribute to a 10–15% premium over conventional dye systems. Additionally, scale-up complexity for textile mills can delay integration and cause formulation batch failures without expert oversight.

New applications in food-grade and medical dye sectors are opening growth avenues. In 2024, salt-free dyes entered dairy and beverage coloring, delivering stable color and regulatory compliance. Medical uses—such as staining reagents—are growing due to biocompatibility and reduced salt interference in diagnostic assays, creating niche demand for high-purity formulations.

Key dye precursors, including specialty colorants and organic pigments, are exposed to supply chain bottlenecks and price swings. In the last 18 months, several manufacturers reported interruptions due to logistics delays and feedstock shortages, requiring them to maintain buffer inventories equal to 12 weeks of production to manage continuous operations.

Adoption of Nanoparticle-Stabilized Dyes Reduces Sedimentation: In 2024, leading dye producers incorporated silica and alumina nanoparticles to enhance dye dispersion stability; this resulted in a 40% reduction in sediment formation during six-month shelf-life testing. Color consistency across batches improved by 12%.

Biodegradable Carrier Systems Gain Traction: Novel carrier formulations using biodegradable polymers (e.g., PLA, PHA) increased in usage by 22% across textile and cosmetic dye lines in 2024. These systems reduced microplastic concerns and simplified wastewater treatment protocols in dyeing facilities.

Digital Inkjet Printing Adoption Drives Formulation Demand: Salt-free dye formulations optimized for inkjet printheads experienced a 35% growth in adoption in the textile digital-printing segment in 2024. Enhanced low-viscosity, high-brightness formulations deliver precise, high-resolution output at up to 1,200 dpi.

Circular-Economy Reuse of Process Water: Textile mills utilizing salt-free dye systems achieved up to 85% water recovery via ultrafiltration and RO. Recycled dye bath water sustained up to 70% of operational demand during peak production cycles, reducing freshwater intake by 60%.

The Salt Free Liquid Dyes Market is segmented across three primary dimensions: product type, application area, and end-user profile. These segments define the commercial potential and innovation pathways within the industry. By type, the market includes various dye formulations such as reactive, acid, basic, and direct dyes, each catering to unique process requirements. Applications span across textiles, food and beverage, cosmetics, medical diagnostics, and printing. End-users include textile manufacturers, cosmetic companies, pharmaceutical firms, and food processors. Each segment is witnessing technological advancements driven by demand for sustainability, safety, and performance consistency. Tailoring formulations to meet industry-specific standards, such as food-grade purity or biocompatibility, has become crucial for market penetration. Understanding this segmentation helps stakeholders align R&D, production, and marketing strategies effectively in a competitive, regulation-driven global market.

In the Salt Free Liquid Dyes Market, reactive salt-free dyes represent the leading type, especially within textile processing. These dyes are widely used in cotton and cellulosic fiber applications due to their superior fixation properties and compatibility with water-saving processes. Their chemical structure allows for strong covalent bonding with fiber, resulting in vivid, long-lasting colors and reduced wastewater loads.

Acid salt-free dyes are the fastest-growing segment, with increasing adoption in protein fiber and nylon applications. Their rapid absorption rates and adaptability in cosmetic formulations are driving demand in the personal care industry. Acid dyes also align well with emerging clean-label requirements for dermatologically safe ingredients.

Basic and direct salt-free dyes serve niche markets, particularly in paper, leather, and industrial labeling sectors. While they have limited usage in high-purity applications, their simplicity in processing and cost-effectiveness keep them relevant. Hybrid and customized formulations are emerging to meet sector-specific needs, blending performance with environmental compliance.

Textile dyeing continues to be the dominant application in the Salt Free Liquid Dyes Market. The transition to salt-free formulations allows textile mills to comply with zero-liquid discharge regulations and reduce environmental impact. In 2024, an estimated 60% of salt-free dye consumption was recorded in garment and home textile processing, driven by fast fashion and eco-conscious production.

Food and beverage coloring is the fastest-growing application, propelled by regulatory shifts and demand for natural-looking, additive-free consumables. Salt-free dyes offer improved solubility, reduced sedimentation, and enhanced food safety compatibility. They are particularly used in beverages, confectionery, and dairy products where salt residues are undesirable.

Other significant application areas include cosmetics, medical diagnostics, and printing inks. Cosmetic-grade dyes benefit from the low irritation potential and formulation stability, while the diagnostic sector values high purity and spectral clarity. Salt-free inks are gaining traction in digital printing due to their stability in nozzles and compatibility with high-speed systems.

Textile manufacturers remain the largest end-user segment in the Salt Free Liquid Dyes Market. These companies rely heavily on water-efficient and eco-friendly dyeing solutions to meet compliance standards and reduce operational costs. Many major textile exporters have adopted salt-free systems to align with sustainability certifications such as OEKO-TEX and GOTS.

The cosmetics and personal care industry is emerging as the fastest-growing end-user, driven by demand for skin-safe, high-stability formulations. These manufacturers are integrating salt-free dyes into products like shampoos, lotions, and decorative cosmetics, where clarity, vibrancy, and allergen-free properties are crucial.

Other relevant end-users include food processing companies, diagnostic laboratories, and industrial ink producers. Food processors seek colorants that ensure consistency across batches while meeting health regulations. Laboratories require high-purity dyes for staining and labeling, especially in immunoassays. Ink manufacturers are increasingly investing in salt-free alternatives for print media that demand longer shelf life and cleaner application.

Asia-Pacific accounted for the largest market share at 42.3% in 2024; however, Europe is expected to register the fastest growth, expanding at a CAGR of 7.9% between 2025 and 2032.

Asia-Pacific’s leadership is supported by a high density of textile and chemical manufacturing hubs, especially in China and India. The region also benefits from abundant raw material access and rising local demand for eco-friendly formulations. Meanwhile, Europe’s rapid expansion is driven by regulatory pressure for sustainable dyes, technological innovation in dye chemistry, and the growing adoption of salt-free variants in the cosmetic and food sectors. Investments in circular economy practices and wastewater reduction technologies are accelerating market adoption across key regional economies.

North America holds approximately 21.7% of the global Salt Free Liquid Dyes Market share in 2024, driven by robust demand from the food & beverage and personal care sectors. The U.S. market leads with a concentration of manufacturers investing in clean-label, non-toxic colorants. Government agencies have implemented tighter restrictions on salt-heavy effluents, encouraging dye houses to transition to salt-free processes. Technological innovations, such as automated blending units and AI-powered quality control, are enhancing operational efficiency. Major brands across food and cosmetic industries are sourcing salt-free alternatives to meet consumer and regulatory expectations for eco-conscious, skin-safe, and food-grade formulations.

Europe commands around 26.5% of the Salt Free Liquid Dyes Market by volume in 2024, with Germany, France, and the United Kingdom emerging as key contributors. The region is marked by stringent sustainability policies driven by bodies like the European Chemicals Agency and initiatives such as the EU Green Deal. These frameworks are accelerating the phasing out of high-salinity dyes across multiple industries. Textile and cosmetic manufacturers are early adopters, integrating automated dosing systems and bio-based raw materials into their salt-free dye lines. Public–private collaborations and R&D subsidies have also catalyzed the development of biodegradable dye carriers and waste-free processes.

Asia-Pacific dominates the Salt Free Liquid Dyes Market in terms of production and consumption volume, with China, India, and Japan collectively contributing over 42.3% of the global market in 2024. The region benefits from large-scale textile parks, cost-effective labor, and government-supported environmental reforms. High-volume textile exporters are retrofitting dyeing units with zero-liquid discharge systems to comply with environmental guidelines. Innovations include nanofiltration-based separation and inline pH correction systems tailored for salt-free formulations. Regional tech hubs are developing AI-enabled sensors to track dye uniformity and reduce water usage. The shift toward greener exports is further supporting this growth trajectory.

South America holds a modest but growing share of the Salt Free Liquid Dyes Market, led by Brazil and Argentina. The regional share is estimated at 5.6% in 2024. Infrastructure development in industrial water treatment and increasing awareness of dye-related pollution are driving adoption. Key industries contributing to demand include textiles, food processing, and ink manufacturing. Government programs promoting clean technology and wastewater minimization are enabling smaller dye houses to transition to salt-free systems. The use of plant-based dye precursors is also gaining interest in Brazil due to agricultural synergies and sustainability mandates.

The Middle East & Africa region holds 3.9% of the global Salt Free Liquid Dyes Market in 2024. Countries such as UAE and South Africa are showing notable growth, especially in textiles and construction labeling applications. Regional demand is spurred by eco-conscious regulations and incentives for sustainable industrial development. Adoption of reverse osmosis and UV-based treatment systems is becoming common in dyeing units across key industrial clusters. Trade agreements promoting non-toxic exports and local mandates restricting saline discharge are reinforcing market expansion. Technology transfer from Europe and Asia-Pacific is accelerating modernization of legacy dye facilities.

India – 24.2% Market Share

India leads due to high production capacity, advanced textile infrastructure, and rising domestic demand for eco-certified dye solutions.

China – 18.1% Market Share

China holds a strong position supported by vertically integrated dye manufacturing and widespread deployment of salt-free processes in digital textile printing.

The Salt Free Liquid Dyes Market features a moderately fragmented competitive landscape with over 40 active manufacturers operating globally. Key players are strategically positioned across Asia-Pacific, Europe, and North America, each offering differentiated product portfolios catering to specific end-use industries such as textiles, food processing, cosmetics, and pharmaceuticals. Competition is primarily driven by innovation in dye formulations, environmental compliance, and customization services. Leading firms are actively pursuing partnerships with textile mills, food-grade manufacturers, and regulatory bodies to enhance adoption.

Several companies have launched eco-certification-compliant product lines tailored for zero-effluent discharge systems. Mergers and acquisitions are increasingly focused on expanding geographical reach and improving R&D capabilities. Automation and AI-enabled process controls have also emerged as differentiation tools in manufacturing facilities. Customization of color intensity, solubility optimization, and extended shelf-life features are central to product innovation strategies. With sustainability at the core, players continue to invest in greener synthesis routes and biodegradable alternatives to gain long-term competitive advantage.

Archroma

DyStar Group

Everlight Chemical Industrial Co., Ltd.

Shivam Chemicals

Bhanu Dyes Pvt. Ltd.

Meghmani Organics Limited

Colorant Ltd.

Kolorjet Chemicals Pvt. Ltd.

Sigma-Aldrich (MilliporeSigma)

Sumitomo Chemical Co., Ltd.

Zhejiang Yide Chemical Co., Ltd.

Aakash Chemicals and Dye-Stuffs Inc.

Atul Ltd.

Allied Industrial Corp., Ltd.

Technological advancements are reshaping the Salt Free Liquid Dyes Market by enhancing both process efficiency and product sustainability. Innovations in molecular engineering have led to the development of highly soluble, low-viscosity dye formulations that improve fixation rates in fiber and food applications. These formulations significantly reduce water usage during the dyeing process, aligning with zero-liquid discharge regulations.

Emerging technologies include AI-integrated process control systems that monitor dye concentration, temperature, and pH in real time, optimizing batch consistency and minimizing human error. Nanotechnology-based encapsulation techniques are gaining popularity for enhancing colorfastness and stability in cosmetic and food-grade applications. Additionally, hybrid organic-inorganic frameworks are being tested to deliver multi-substrate compatibility and UV resistance.

Advances in bioprocessing now allow the use of microbial fermentation to produce bio-based dye precursors, reducing dependency on petrochemical feedstocks. Continuous flow reactors and inline filtration units are also being adopted by manufacturers to lower production downtime and improve yield. Collectively, these technological innovations are enabling cleaner, faster, and more cost-efficient dyeing operations, making salt-free formulations increasingly viable for mainstream adoption across industries.

• In March 2024, Archroma introduced a new range of salt-free reactive dyes for cellulosic textiles, which demonstrated a 40% reduction in water usage during pilot testing at two European dyeing units.

• In July 2024, DyStar announced the deployment of an AI-powered dye shade prediction tool in its manufacturing process, increasing formulation accuracy by over 95% and cutting down trial runs by 60%.

• In December 2023, Colorant Ltd. launched a salt-free dye range specifically developed for the cosmetic industry, featuring high dermatological safety compliance and shelf-life stability exceeding 18 months.

• In October 2023, Shivam Chemicals commissioned a fully automated salt-free dye production facility in Gujarat, India, with an annual capacity of 5,000 metric tons focused on eco-label textile clients.

The Salt Free Liquid Dyes Market Report offers a comprehensive assessment of the global landscape, encompassing key insights across product types, applications, end-user sectors, technologies, and regional trends. It evaluates multiple dye categories such as reactive, acid, basic, and direct salt-free dyes, detailing their relevance in core industries including textiles, food and beverage, cosmetics, medical diagnostics, and printing.

The report includes granular segmentation analysis, covering usage patterns across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. End-users analyzed range from textile manufacturers to pharmaceutical and personal care companies. Special focus is given to environmental drivers, such as wastewater management and zero-liquid discharge regulations, which are reshaping procurement strategies globally.

Technological sections delve into bio-based production, AI integration in dye processing, and advancements in solubility and color stability. The report also highlights trends in digital textile printing, clean-label demand, and region-specific industrial shifts. This detailed scope ensures that decision-makers gain actionable intelligence for market entry, expansion, and product innovation strategies tailored to evolving environmental and commercial standards.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 10.6 Million |

| Market Revenue (2032) | USD 18.5 Million |

| CAGR (2025–2032) | 7.2% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Technological Insights, Market Dynamics, Segment Analysis, Regional and Country-Wise Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Archroma, DyStar Group, Everlight Chemical Industrial Co., Ltd., Shivam Chemicals, Bhanu Dyes Pvt. Ltd., Meghmani Organics Limited, Colorant Ltd., Kolorjet Chemicals Pvt. Ltd., Sigma-Aldrich (MilliporeSigma), Sumitomo Chemical Co., Ltd., Zhejiang Yide Chemical Co., Ltd., Aakash Chemicals and Dye-Stuffs Inc., Atul Ltd., Allied Industrial Corp., Ltd. |

| Customization & Pricing | Available on Request (10% Customization is Free) |