Reports

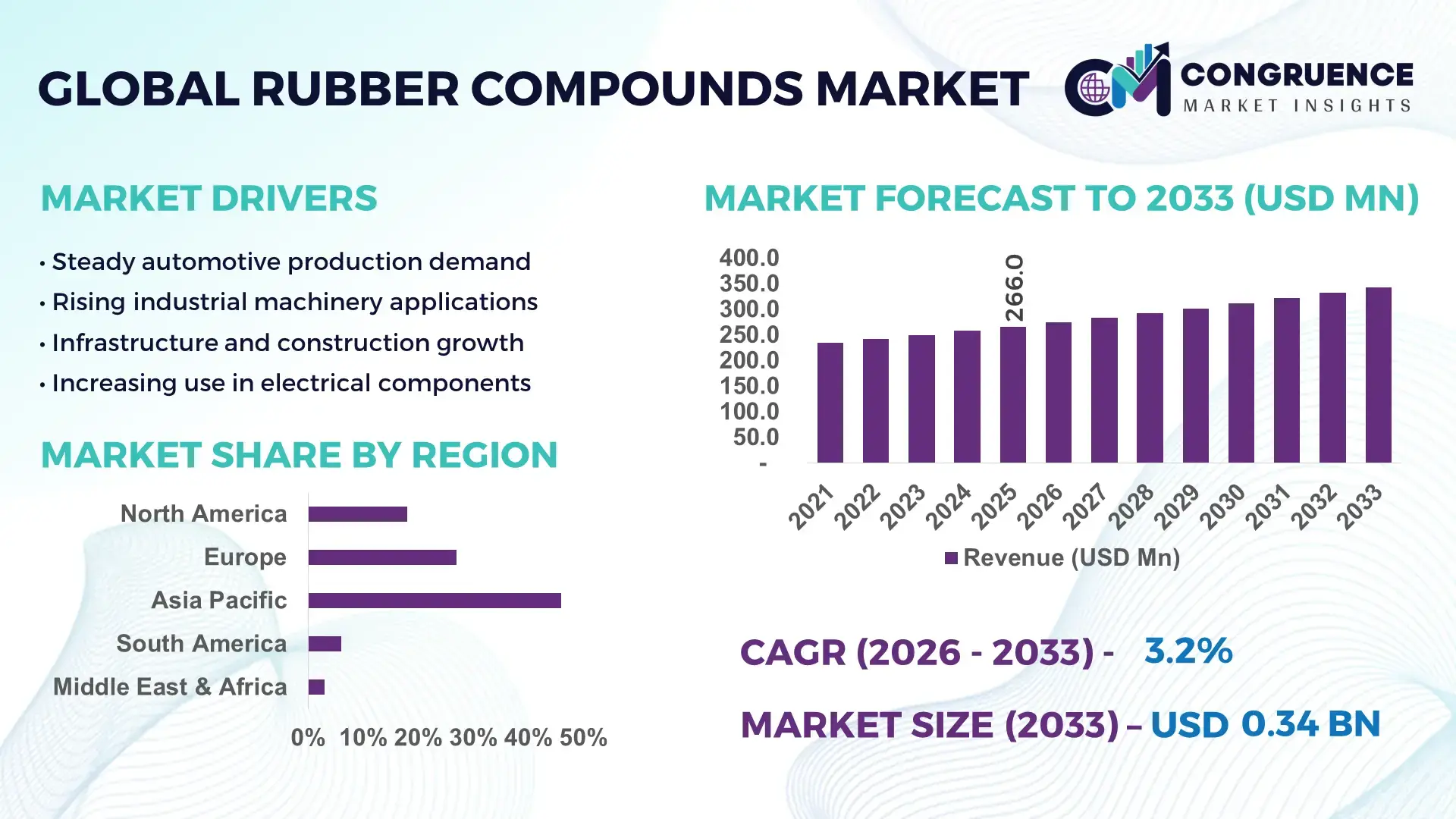

The Global Rubber Compounds Market was valued at USD 266.0 Million in 2025 and is anticipated to reach a value of USD 342.2 Million by 2033 expanding at a CAGR of 3.2% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is supported by steady demand from automotive, industrial manufacturing, and infrastructure applications requiring customized, performance-enhanced elastomer formulations.

China represents the dominant country in the Rubber Compounds Market, supported by large-scale production infrastructure and sustained capital investment in elastomer processing facilities. The country operates over 1,500 rubber compounding units with an estimated annual processing capacity exceeding 12 million metric tons. More than 60% of domestic rubber compound output is directed toward automotive tires, hoses, seals, and vibration-control components. In 2024, China invested over USD 4.5 billion in advanced polymer processing equipment, including automated mixing systems and AI-enabled quality control lines. Technological advancements such as silica-reinforced compounds and low-VOC formulations have seen adoption rates above 45% among tier-1 suppliers, while electric vehicle component applications account for nearly 18% of compound consumption.

Market Size & Growth: Valued at USD 266.0 Million in 2025, projected to reach USD 342.2 Million by 2033 at a CAGR of 3.2%, driven by rising demand for high-performance elastomers in mobility and industrial systems.

Top Growth Drivers: Automotive lightweighting adoption at 38%, industrial equipment durability improvement of 27%, and EV component integration growth of 22%.

Short-Term Forecast: By 2028, advanced compounding techniques are expected to improve material efficiency by 19%.

Emerging Technologies: AI-assisted compound formulation, silica-reinforced elastomers, and bio-based rubber additives.

Regional Leaders: Asia Pacific projected at USD 145.0 Million by 2033 with EV demand acceleration; Europe at USD 92.0 Million driven by sustainability mandates; North America at USD 71.0 Million with high adoption of specialty compounds.

Consumer/End-User Trends: Automotive OEMs account for nearly 52% of demand, followed by industrial machinery at 28%.

Pilot or Case Example: In 2024, a Japanese tire manufacturer achieved 21% wear-resistance improvement using nano-filler compounds.

Competitive Landscape: Market leader holds approximately 18% share, followed by LANXESS, Cabot Corporation, Kumho Petrochemical, and JSR Corporation.

Regulatory & ESG Impact: Compliance with REACH and carbon-reduction mandates has increased low-emission compound adoption by 31%.

Investment & Funding Patterns: Over USD 6.8 billion invested globally in compounding facility upgrades and automation.

Innovation & Future Outlook: Integration of recycled rubber content and digital twin-based formulation is shaping next-generation products.

The Rubber Compounds Market serves automotive (52%), industrial machinery (28%), construction (12%), and consumer goods (8%). Recent innovations include low-rolling-resistance compounds, bio-fillers, and high-temperature elastomers. Environmental regulations, energy-efficiency mandates, and regional manufacturing shifts influence demand, with Asia Pacific leading consumption and Europe driving sustainable compound development. Emerging trends indicate increased adoption of recycled and smart elastomer formulations.

The Rubber Compounds Market plays a strategic role in enabling durability, safety, and performance across transportation, industrial, and infrastructure value chains. Advanced compounding directly impacts product lifecycle efficiency, with high-dispersion filler technologies delivering up to 24% improvement in abrasion resistance compared to conventional carbon black blends. Silica-reinforced rubber compounds deliver 18% lower rolling resistance compared to older standard formulations, supporting fuel efficiency and electric vehicle range optimization.

Asia Pacific dominates in volume due to extensive manufacturing capacity, while Europe leads in adoption with nearly 42% of enterprises integrating sustainable and low-VOC rubber compounds. By 2028, AI-driven formulation optimization is expected to reduce material waste by 26% and shorten development cycles by 30%. Firms are committing to ESG improvements such as 35% recycled rubber content and 40% emission reduction in compounding operations by 2032.

In 2024, Germany achieved a 22% energy-use reduction in industrial rubber processing through digital mixing controls and predictive maintenance systems. Looking ahead, the Rubber Compounds Market is positioned as a pillar of resilience, compliance, and sustainable growth, enabling next-generation mobility, circular manufacturing, and regulatory-aligned industrial development.

The Rubber Compounds Market is shaped by evolving material performance requirements, regulatory compliance pressures, and shifts in end-use demand. Automotive electrification, industrial automation, and infrastructure modernization are influencing compound design priorities such as heat resistance, wear durability, and chemical stability. Manufacturers are increasingly focusing on customized formulations to meet application-specific standards, while global supply chains are adapting to raw material volatility and environmental compliance. Technological integration in mixing, dispersion, and quality monitoring continues to redefine operational efficiency and product consistency across the Rubber Compounds Market.

The automotive sector accounts for over half of rubber compound consumption, driven by demand for lightweight, durable, and heat-resistant components. Electric vehicles require specialized compounds for battery seals, thermal insulation, and vibration dampening, increasing per-vehicle rubber usage by nearly 17%. Advanced tire formulations alone have improved wear life by 25% while reducing rolling resistance by 14%. This shift toward performance-oriented mobility solutions continues to accelerate demand for engineered rubber compounds.

Natural rubber and synthetic elastomer prices fluctuate by 20–30% annually due to climate variability, petrochemical feedstock instability, and trade restrictions. These fluctuations increase procurement risk and compress manufacturer margins. Additionally, compliance with chemical safety regulations increases formulation costs by an estimated 12–15%, limiting adoption among small and mid-scale compounders and constraining market scalability.

Bio-based fillers, recycled rubber content, and low-emission additives present significant growth opportunities. Compounds incorporating recycled elastomers have demonstrated 20% lower carbon intensity while maintaining over 90% performance parity. Government incentives for sustainable materials and circular manufacturing are encouraging large-scale adoption, particularly in Europe and East Asia, creating new value streams for compound developers.

Advanced compounding requires precise dispersion control, temperature management, and regulatory compliance, increasing operational complexity. Quality deviations above 3% can lead to rejection in automotive applications. Compliance testing, certification, and environmental audits add up to 18% additional operational cost, challenging scalability and time-to-market for new formulations.

Digitalized Mixing and Process Automation: Over 48% of large rubber compound manufacturers have implemented automated mixing systems, reducing batch variability by 32% and improving throughput by 21%. AI-enabled sensors now monitor viscosity and dispersion in real time, cutting defect rates below 2%.

Growth in Sustainable and Recycled Compounds: More than 37% of newly developed compounds now include recycled or bio-based content. These formulations achieve up to 28% lower lifecycle emissions while maintaining tensile strength above 95% of conventional compounds, supporting compliance-driven procurement.

Expansion of EV-Specific Elastomer Applications: Electric vehicle platforms use 15–20% more specialized rubber compounds per unit than internal combustion vehicles. Demand for flame-retardant and high-thermal-stability elastomers has increased adoption rates by 34% since 2022.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Rubber Compounds Market. Around 55% of new projects report cost benefits through prefabrication, increasing demand for precision-engineered seals, gaskets, and vibration-control components used in off-site manufactured structures.

The Rubber Compounds Market is segmented based on type, application, and end-user industries, reflecting the diversity of performance requirements across manufacturing ecosystems. Different compound formulations are engineered to meet specific needs such as abrasion resistance, thermal stability, chemical compatibility, and elasticity. Demand patterns vary significantly depending on end-use exposure to stress, temperature, and regulatory compliance. Automotive and industrial manufacturing continue to drive high-volume consumption, while construction, electrical insulation, and consumer goods demand specialized formulations. Across segments, manufacturers increasingly favor customized and application-specific rubber compounds, supported by advanced mixing technologies, filler optimization, and sustainability-driven material selection. This segmentation structure highlights how innovation and end-user performance benchmarks directly shape material adoption trends.

The Rubber Compounds Market is categorized into natural rubber compounds, synthetic rubber compounds, and specialty/blended rubber compounds. Synthetic rubber compounds represent the leading type, accounting for approximately 58% of total adoption, driven by their superior resistance to heat, oil, and chemicals, making them suitable for automotive tires, hoses, seals, and industrial components. In comparison, natural rubber compounds account for around 27%, favored in applications requiring high elasticity and tensile strength, such as vibration dampeners and conveyor belts. However, adoption in specialty and blended rubber compounds—including EPDM, NBR, and silicone-based blends—is rising fastest, with an estimated fastest-segment growth rate of about 4.6%, supported by increasing demand for electric vehicle components, renewable energy systems, and high-temperature industrial environments.

Specialty and blended compounds, though currently holding a smaller share, are gaining traction due to their tailored performance attributes and compliance with environmental standards. The remaining niche formulations collectively contribute roughly 15% of overall usage, serving medical, aerospace, and advanced electronics applications where precision performance is critical.

In 2024, a national automotive standards agency reported the large-scale deployment of silica-reinforced synthetic rubber compounds in commercial vehicle tires, resulting in a documented 14% improvement in wear resistance and measurable reductions in rolling friction across fleet trials.

By application, automotive applications dominate the Rubber Compounds Market with nearly 52% of total usage, reflecting extensive demand for tires, weather seals, hoses, gaskets, and vibration-control components. Industrial machinery applications follow with approximately 26%, supported by demand for belts, rollers, and sealing systems exposed to mechanical stress and chemical environments. While construction and infrastructure applications currently account for about 14%, adoption in this segment is expanding rapidly, driven by modular construction, prefabricated systems, and the need for durable sealing and insulation materials. Construction-related rubber compound applications are the fastest-growing, advancing at an estimated 4.1% growth rate, supported by urbanization and infrastructure modernization trends.

Other applications, including consumer goods, electrical insulation, and healthcare products, collectively represent around 8% of demand but remain strategically important due to higher specification requirements. Consumer adoption trends indicate that over 45% of global automotive suppliers have increased the use of advanced rubber compounds to improve component longevity, while nearly 33% of industrial manufacturers report prioritizing chemically resistant elastomers to reduce maintenance cycles.

In 2025, a government-backed infrastructure development program documented the use of high-durability rubber sealing compounds in more than 1,200 prefabricated bridge and transit projects, achieving a 20% reduction in maintenance interventions.

From an end-user perspective, automotive OEMs and tier-1 suppliers represent the largest segment, accounting for approximately 49% of overall compound consumption, due to stringent performance, safety, and durability requirements. In comparison, industrial manufacturing firms contribute around 29%, driven by demand from heavy equipment, processing plants, and material-handling systems. However, adoption among construction and infrastructure developers is growing fastest, with an estimated 4.3% growth rate, as rubber compounds are increasingly specified for expansion joints, waterproofing systems, and vibration isolation in large-scale projects.

Other end-users—including consumer goods manufacturers, electrical equipment producers, and medical device companies—collectively represent about 22% of market participation. Industry adoption data shows that over 40% of large manufacturing enterprises now integrate customized rubber formulations to meet application-specific performance benchmarks, while nearly 35% of construction firms report increased usage of engineered elastomers to extend asset lifecycles.

In 2024, a national manufacturing innovation council highlighted that industrial equipment manufacturers adopting advanced rubber compounds achieved an average 18% reduction in unplanned downtime due to improved sealing and wear performance.

Asia-Pacific accounted for the largest market share at 46% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 4.4% between 2026 and 2033.

Asia-Pacific benefits from high-volume automotive manufacturing, dense industrial clusters, and large-scale rubber processing capacity, particularly across China, India, and Japan. Europe followed with an estimated 27% share, supported by sustainability-led material substitution and advanced elastomer engineering. North America captured approximately 18%, driven by high-value specialty compounds and strict performance standards in automotive and healthcare. South America and the Middle East & Africa together accounted for the remaining 9%, with rising infrastructure investments, energy-sector demand, and import substitution policies contributing to incremental growth. Regional variations in regulation, technology adoption, and end-use intensity continue to shape localized demand patterns across the Rubber Compounds Market.

North America accounts for approximately 18% of the global Rubber Compounds Market, characterized by strong demand for high-performance and specialty elastomer formulations. Key industries driving consumption include automotive manufacturing, healthcare equipment, industrial machinery, and construction. Regulatory frameworks emphasizing low-emission materials and workplace safety have increased the use of non-toxic and low-VOC rubber compounds by over 30% across manufacturing facilities. Technological advancements such as automated mixing lines, digital quality monitoring, and predictive maintenance systems are now deployed in more than 45% of large compounding plants. A leading regional compounder expanded its silicone and EPDM production lines in 2024 to support electric vehicle sealing systems, increasing output capacity by 22%. Regional consumer behavior reflects higher enterprise adoption in healthcare and finance-linked infrastructure projects, where durability and compliance are critical purchasing criteria.

Europe represents nearly 27% of global demand in the Rubber Compounds Market, with Germany, France, and the UK acting as key consumption and innovation hubs. Stringent environmental regulations and circular economy policies have accelerated the adoption of recyclable and bio-based rubber compounds, now used in approximately 38% of newly specified industrial applications. European manufacturers are early adopters of advanced filler technologies, including silica and nano-additives, improving abrasion resistance by up to 20%. Digital traceability systems for material compliance are implemented across 40% of production facilities. A major European elastomer producer introduced recycled-content tire compounds in 2025, enabling OEM partners to reduce lifecycle emissions by 25%. Regional consumer behavior shows that regulatory pressure directly drives demand for transparent, certified, and environmentally compliant rubber materials.

Asia-Pacific is the largest regional market, accounting for about 46% of total volume consumption, led by China, India, and Japan. The region hosts more than 60% of global rubber compounding facilities, supported by integrated supply chains and competitive manufacturing costs. Automotive, industrial machinery, electronics, and infrastructure projects dominate demand, with China alone consuming over 12 million metric tons of rubber compounds annually. Manufacturing automation adoption exceeds 50% in tier-1 facilities, while innovation hubs in Japan and South Korea focus on high-temperature and EV-specific elastomers. A large Asian compound manufacturer commissioned a new AI-controlled mixing plant in 2024, improving batch consistency by 28%. Regional consumer behavior reflects strong growth tied to industrial expansion, export-oriented manufacturing, and rapid infrastructure development.

South America holds an estimated 6% share of the Rubber Compounds Market, with Brazil and Argentina as the primary consuming countries. Demand is closely linked to infrastructure development, mining operations, and energy-sector equipment requiring abrasion- and oil-resistant compounds. Government incentives supporting local manufacturing have increased domestic rubber processing capacity by nearly 15% since 2022. Trade policies encouraging import substitution have also boosted regional compound blending activities. A Brazilian industrial supplier expanded conveyor belt compound production in 2024 to serve mining clients, reducing equipment failure rates by 18%. Regional consumer behavior indicates demand patterns closely aligned with construction cycles and industrial maintenance requirements rather than consumer goods.

The Middle East & Africa region accounts for roughly 3% of global demand but shows the highest growth momentum. Construction, oil & gas, and infrastructure megaprojects are key demand drivers, particularly in the UAE, Saudi Arabia, and South Africa. Rubber compounds used in sealing systems, hoses, and vibration isolation are increasingly specified for extreme temperature and chemical exposure conditions. Technological modernization initiatives have led to the adoption of advanced elastomers in over 35% of new industrial installations. Trade partnerships and regional manufacturing incentives are encouraging local compounding activity. A Gulf-based manufacturer introduced high-temperature-resistant rubber formulations in 2025 to support refinery upgrades, extending component lifespan by 20%. Regional consumer behavior favors durable, long-life materials with minimal maintenance requirements.

China – 34% Market Share: Dominates the Rubber Compounds Market due to extensive production capacity, integrated automotive manufacturing, and large-scale industrial demand.

United States – 16% Market Share: Maintains a strong position driven by high adoption of specialty and performance-grade rubber compounds across automotive, healthcare, and industrial sectors.

The Rubber Compounds Market is moderately fragmented, with a diverse competitive landscape comprising more than 150 active global and regional manufacturers competing on innovation, product differentiation, and geographic reach. Top-tier companies focus on advanced compounding capabilities, sustainability solutions, and strategic partnerships to enhance positioning. The combined share of the top 5 companies—including Hexpol Compounding, PHOENIX Compounding, Cooper Standard, Hutchinson, and AirBoss of America—constitutes around 35–38% of global compound output, leaving substantial room for mid-size and regional players to capture niche demand. Leading competitors are investing heavily in digital transformation, with over 40% of plants implementing automated mixing, real-time quality monitoring, and AI-assisted formulation tools to improve consistency and reduce defect rates. Strategic initiatives in 2024–2025 include new product launches of bio-based and recycled rubber compounds, capacity expansions in Asia-Pacific and North America, and partnerships between chemical suppliers and OEMs to co-develop tailored materials for electric vehicle and industrial applications. The market’s competitive dynamics are further shaped by regional players like Dongjue Silicone Group and Chunghe Compounding in China, which leverage cost leadership and government-supported expansion programs to penetrate export markets. Innovation trends such as sustainable elastomers, functionalized fillers, and precision formulations are key differentiators driving long-term competitiveness.

PHOENIX

Hutchinson

Polymer-Technik Elbe

Elastomix

Chunghe Compounding

Dongjue Silicone Group

KRAIBURG Holding GmbH

Dongguan New Orient Technology

Guanlian

American Phoenix

Dyna-Mix

The Rubber Compounds Market is experiencing a profound technological evolution, driven by the need for performance optimization, sustainability compliance, and production efficiency. Automated mixing and processing technologies are increasingly adopted, with over 22% of global plants integrating digital quality monitoring, predictive maintenance, and real-time process analytics to maintain uniform dispersion and minimize batch variability. Smart manufacturing systems leveraging sensors and IoT connectivity enhance process control, reducing defect rates and enabling faster scale-up of customized formulations.

Emerging technologies such as AI-assisted compound design are transforming R&D workflows. These platforms analyze historical formulation databases with performance outcomes to accelerate new compound development cycles and optimize balance between elasticity, abrasion resistance, and thermal stability. Adoption of AI frameworks has significantly reduced formulation validation cycles, improving go-to-market speed for high-performance compounds used in electric vehicle (EV) components and industrial machinery.

Another key innovation is the use of advanced fillers and functionalized additives, including silica, nanocarbon, and graphene masterbatches, which enhance mechanical strength, reduce weight, and improve energy efficiency in end-use applications. For example, graphene-enhanced masterbatches are being piloted for tire and conveyor belt applications, delivering measurable improvements in wear resistance and tensile properties.

Sustainability technology integration is also gaining momentum. Closed-loop recycling systems, which reclaim and reintroduce rubber scrap into new compound batches, help reduce dependency on virgin feedstocks. Digital traceability systems provide chain-of-custody transparency for bio-based and recycled materials, supporting compliance with environmental regulatory frameworks. These innovations collectively position the Rubber Compounds Market at the intersection of advanced material science, digital transformation, and sustainable manufacturing, reinforcing its capacity to meet evolving industrial and regulatory demands.

• In March 2025, Hexpol Compounding announced it has commercially introduced its Hexgreen sustainable rubber compound series containing a minimum of 10% sustainable raw materials and is ramping production at its devulcanization-enabled Lesina facility in Europe to increase recycled content offerings and capacity. Source: www.european-rubber-journal.com

• In early 2024, Hexpol Compounding began installation of an in-house devulcanization line at its Czech Republic plant, enabling mechanical recycling of cured rubber into new compound feedstock and supporting circular economy production workflows. Source: www.mesgo.it

• In late 2024, AirBoss of America Corp. secured a $55 million senior secured term loan facility as part of an aggregated $180 million financing package, reinforcing its financial base to expand rubber compounding operations and strategic growth initiatives in North America. Source: www.european-rubber-journal.com

• In March 2025, AirBoss of America reported its Q4 and full-year 2024 results, highlighting the launch of a new silicone production line in Michigan, expanded specialty compounding focus, and improved Rubber Solutions margin performance driven by product and capability enhancements.

The scope of the Rubber Compounds Market Report encompasses a comprehensive evaluation of global segmentation by product type, applications, end-users, and geographic regions. It systematically analyzes multiple product categories, including EPDM, SBR, BR, NBR, natural rubber, and silicone and specialty blended compounds, articulating performance characteristics, formulation specifics, and application relevance across automotive, industrial, construction, wire & cable, consumer goods, and other sectors. The report assesses regional markets across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, detailing production capacities, consumption patterns, regulatory influences, and technological adoption levels.

Technological dimensions are covered extensively, with insights into automation, digital processing technologies, AI-assisted compound design, and emerging sustainable material innovations such as recycled and bio-based elastomers. Strategic focuses include product differentiation, performance benchmarks (e.g., wear resistance, thermal stability, chemical compatibility), and the evolution of formulations tailored to electric vehicle systems, industrial machinery, infrastructure components, and high-performance consumer products.

In addition to macro trends, the report highlights competitive dynamics, profiling leading manufacturers and mapping strategic initiatives such as collaborations, capacity expansions, product launches, and sustainability investments. It also includes emerging niches like graphene-enhanced masterbatches and high-temperature silicone elastomers, reflecting opportunities in aerospace, medical equipment, and renewable energy applications. Through detailed segmentation and forward-looking analysis, the scope provides decision-makers with a nuanced understanding of the market’s breadth, depth, and future strategic pathways, supporting investment planning, product development, and competitive positioning.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 266.0 Million |

| Market Revenue (2033) | USD 342.2 Million |

| CAGR (2026–2033) | 3.2% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | HEXPOL Compounding; PHOENIX Compounding; Cooper Standard; Hutchinson; Polymer-Technik Elbe; Elastomix; AirBoss of America; Chunghe Compounding; Dongjue Silicone Group; KRAIBURG Holding GmbH; Dongguan New Orient Technology; Guanlian; American Phoenix; Dyna-Mix |

| Customization & Pricing | Available on Request (10% Customization Free) |