Reports

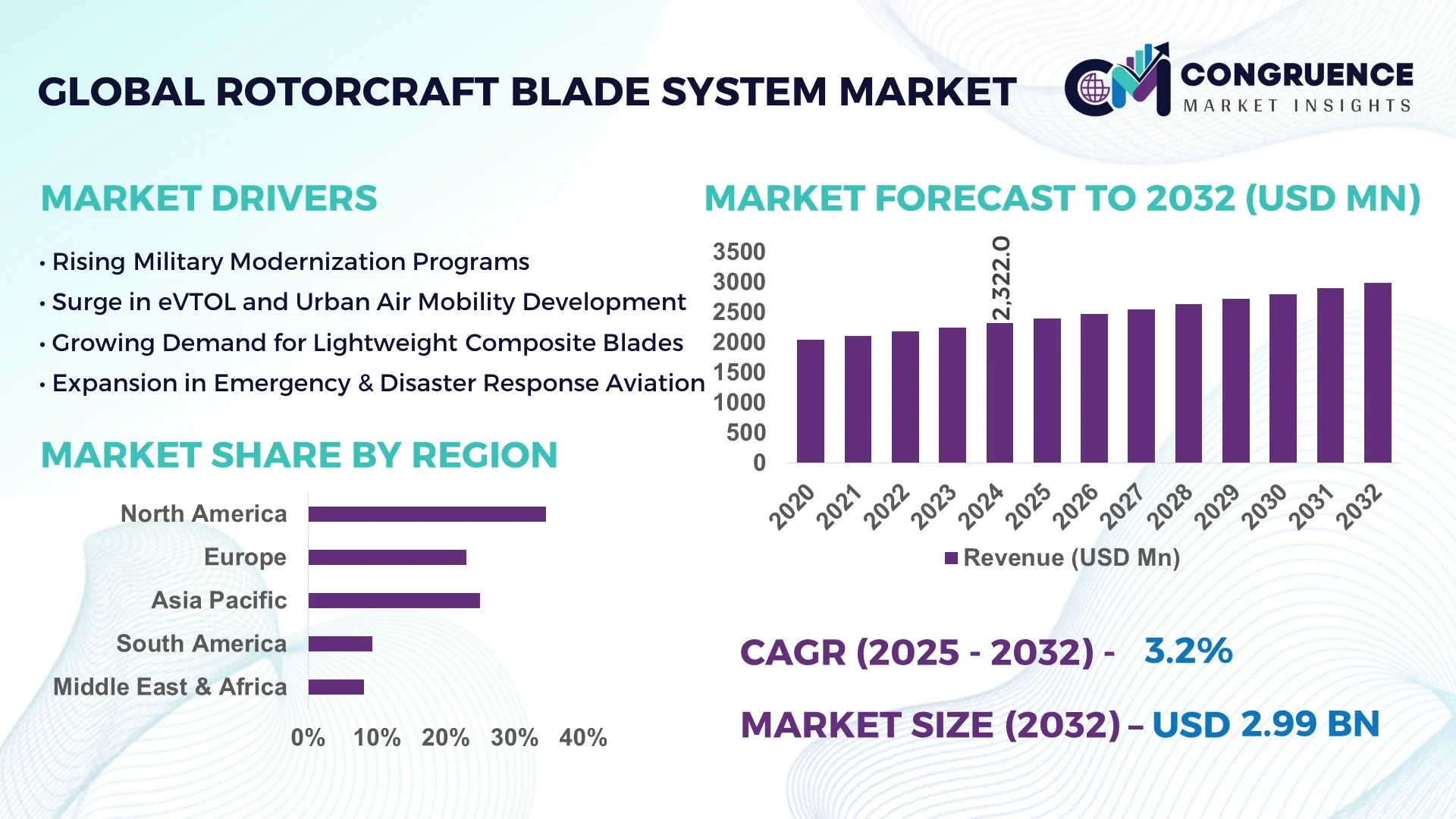

The Global Rotorcraft Blade System Market was valued at USD 2322 Million in 2024 and is anticipated to reach a value of USD 2987.44 Million by 2032 expanding at a CAGR of 3.2% between 2025 and 2032.

In the United States, the market for rotorcraft blade systems benefits from advanced defense manufacturing infrastructure, with high production capacity driven by sustained Department of Defense investments in rotary-wing aircraft. The country also leads in integrating composite materials and automated blade fabrication technologies across military and commercial rotorcraft applications.

Rotorcraft blade systems play a critical role in aviation performance, particularly in helicopters, tiltrotors, and other vertical lift aircraft. The market spans multiple sectors including defense, emergency medical services, offshore oil and gas transport, and law enforcement aviation. Recent innovations include active blade control technologies, lightweight carbon fiber-reinforced blades, and noise-reduction designs, all contributing to enhanced aerodynamic efficiency and fuel performance. Regulatory mandates on emissions and noise are prompting the adoption of advanced materials and hybrid-electric propulsion compatibility. Economically, emerging regions in Asia-Pacific and the Middle East are accelerating demand due to growing investments in defense and civil rotorcraft fleets. Environmental considerations and rising demand for urban air mobility solutions are shaping future trends, emphasizing the need for lighter, quieter, and more sustainable rotorcraft blade systems.

Artificial Intelligence is significantly reshaping the Rotorcraft Blade System Market by introducing smarter design, maintenance, and manufacturing processes that improve performance and lifecycle efficiency. AI-powered simulations are now integral in optimizing blade geometry for reduced drag, increased lift, and minimized vibration, resulting in enhanced flight dynamics and improved fuel economy. In manufacturing, AI-integrated robotics and predictive analytics are revolutionizing composite blade fabrication, ensuring consistency, precision, and reduced production downtime.

In operational environments, AI-driven sensors and onboard diagnostic systems analyze flight data in real-time to anticipate blade fatigue or wear, enabling predictive maintenance. This minimizes unplanned downtimes and extends rotor blade life cycles, making fleet operations more efficient and cost-effective. Furthermore, machine learning algorithms are helping engineers simulate real-world flight scenarios to validate new rotorcraft blade designs under varying environmental and mission-specific conditions, significantly reducing time-to-market.

AI is also enhancing safety in the Rotorcraft Blade System Market through adaptive control systems capable of responding to turbulence, wind shear, or blade icing conditions in real time. This dynamic control is particularly critical in military and emergency response applications where reliability is non-negotiable. As AI continues to evolve, its integration into design optimization, structural health monitoring, and smart materials is expected to drive significant innovation across the global rotorcraft blade ecosystem.

"In March 2024, an AI-powered edge computing system was deployed by a leading aerospace manufacturer to enable real-time stress and vibration monitoring on rotorcraft blades, resulting in a 23% increase in structural lifespan prediction accuracy and a 17% reduction in unscheduled maintenance incidents."

The growing adoption of advanced composite materials is a significant driver fueling the Rotorcraft Blade System Market. Composite rotor blades, especially those made from carbon fiber-reinforced polymers, offer superior strength-to-weight ratios, corrosion resistance, and improved fatigue performance compared to traditional metallic blades. These materials enable rotorcraft to operate more efficiently with better payload capacities and extended range. For example, newer military helicopters such as the Sikorsky CH-53K incorporate composite blades that improve lift capability by 20% while reducing weight. Moreover, the use of composites allows for tailored blade geometries that reduce vibration and noise during flight, addressing both performance and regulatory requirements. This material evolution is also supporting the integration of smart sensors within blades for real-time condition monitoring, further enhancing operational reliability.

One of the key restraints affecting the Rotorcraft Blade System Market is the high cost and complexity associated with rotor blade manufacturing. Producing advanced composite blades requires precision engineering, specialized tooling, and autoclave processing, all of which drive up manufacturing expenses. Moreover, the global supply chain for raw materials like aerospace-grade carbon fiber and resin systems is limited and often affected by geopolitical disruptions and fluctuating demand. These factors contribute to extended lead times and increased pricing pressure, especially for smaller OEMs and MRO providers. The certification process for new blade designs, particularly in civil aviation, adds further time and cost, often delaying innovation deployment. As a result, some end users may delay upgrades or opt for refurbishment instead of acquiring advanced blade systems, slowing market adoption.

The global push toward Urban Air Mobility (UAM) and electric Vertical Take-Off and Landing (eVTOL) aircraft presents a significant opportunity for growth in the Rotorcraft Blade System Market. eVTOL platforms rely heavily on efficient, lightweight, and quiet rotor blade systems to meet urban operational standards. These aircraft require smaller-diameter, high-RPM blades with minimal acoustic footprint, fostering innovation in blade aerodynamics and active noise-canceling technologies. With over 200 eVTOL projects under development globally as of 2025, there is increasing demand for specialized rotor systems. Additionally, governments and private investors are accelerating UAM infrastructure, particularly in Asia-Pacific and North America. Blade system manufacturers that can deliver low-maintenance, modular, and scalable rotor designs tailored for eVTOL configurations are well-positioned to capitalize on this rapidly emerging segment.

One of the most pressing challenges in the Rotorcraft Blade System Market is the increasingly stringent regulatory landscape that governs blade design, testing, and certification. Aviation authorities, such as EASA and FAA, impose rigorous safety and performance standards to ensure airworthiness, requiring manufacturers to conduct extensive material validation, fatigue testing, and environmental stress analysis. This process often spans several years and involves significant investment in testing infrastructure, engineering manpower, and compliance documentation. For instance, new composite rotor blades must undergo full-scale dynamic testing and weather endurance simulations before they can be approved for commercial or military use. These prolonged certification cycles hinder the speed of innovation and delay time-to-market for next-generation blade systems. Additionally, varying international standards create complexity for manufacturers aiming to serve multiple regional markets, leading to duplication of testing protocols and increased operational burdens.

• Integration of Smart Materials for Real-Time Monitoring: Rotorcraft blade manufacturers are increasingly integrating smart materials like piezoelectric sensors and shape-memory alloys into blade structures. These materials enable real-time monitoring of stress, temperature, and vibration during flight, enhancing structural health diagnostics. As of 2025, over 40% of new rotorcraft platforms under development globally incorporate some form of embedded sensing for proactive maintenance and improved operational safety.

• Increased Focus on Noise-Reduction Technologies: Noise pollution regulations are pushing the Rotorcraft Blade System Market toward quieter blade designs. Innovations such as anhedral blade tips, swept-back geometries, and active blade pitch modulation have shown to reduce rotor noise by up to 30%. These technologies are particularly relevant for urban air mobility and EMS helicopters operating in densely populated zones where noise control is critical.

• Growing Use of Additive Manufacturing in Prototyping: Additive manufacturing (3D printing) is transforming the prototyping process in blade development. Engineers can now produce complex blade models using high-strength thermoplastics and metal composites within days, significantly cutting down R&D cycles. This trend is helping aerospace firms accelerate design iterations while minimizing waste and tooling costs.

• Expansion of Blade Retrofit and Upgrade Programs: Legacy rotorcraft platforms are increasingly being upgraded with modern blade systems featuring improved materials and aerodynamic profiles. Retrofit programs are particularly active in military fleets across Asia and Latin America, where budget constraints delay full platform replacements. These upgrades often lead to a 10–15% increase in lift capacity and reduced fuel consumption, offering measurable performance gains without full aircraft overhauls.

The Rotorcraft Blade System Market is segmented based on type, application, and end-user, each reflecting diverse operational demands and technological advancement. Rotor blade types range from main rotor blades to tail rotor variants, each built for specific aerodynamic and control purposes. Applications are segmented into military, commercial, and civil aviation, with military usage dominating due to rising global defense investments. End-user insights highlight original equipment manufacturers (OEMs), aftermarket service providers, and fleet operators, with OEMs playing the most dominant role due to their integration capabilities. Notably, the aftermarket segment is gaining momentum with increasing retrofitting needs and digitized maintenance strategies. These segmentation categories offer strategic visibility into how market players align their R&D and manufacturing priorities.

Main rotor blades account for the dominant share in the Rotorcraft Blade System Market due to their critical role in providing lift and maneuverability. Their complex design requirements—balancing aerodynamic efficiency, structural strength, and vibration control—make them the focus of most R&D efforts. Tail rotor blades follow in usage, designed for yaw control and often engineered with noise-reducing geometries and lightweight materials. The fastest-growing segment is composite rotor blades, driven by the aviation industry's push for fuel efficiency, weight reduction, and low-maintenance components. Their increasing integration across both new and retrofit platforms highlights their growing importance. Additionally, special-purpose blades such as those used in drones or eVTOL systems are emerging, offering niche value for surveillance, delivery, and urban transport applications. Innovations in tip design, blade pitch control, and surface coatings further distinguish types within this evolving segment.

Military applications continue to dominate the Rotorcraft Blade System Market, supported by ongoing modernization of defense rotorcraft fleets and investments in attack and utility helicopters. Blade systems used in military platforms require advanced composite materials, stealth features, and performance in extreme environmental conditions. The fastest-growing application is urban air mobility, propelled by technological advancements in electric propulsion and regulatory support for low-altitude air transport. UAM rotorcraft demand ultra-lightweight and low-noise blades, pushing innovation at both material and design levels. Commercial transport applications—particularly offshore oil & gas and cargo logistics—also contribute significantly, favoring rotorcraft with high endurance and operational efficiency. Emergency medical services, border patrol, and firefighting operations make up other growing application areas, each requiring specialized blade characteristics like quick response to control input and reduced acoustic footprint.

Original Equipment Manufacturers (OEMs) are the leading end-users in the Rotorcraft Blade System Market due to their direct role in design, certification, and system integration. OEMs invest heavily in R&D to meet the evolving needs of military and commercial aviation, often collaborating with material science firms and AI developers to improve blade technology. The fastest-growing end-user segment is maintenance, repair, and overhaul (MRO) service providers, fueled by the surge in global rotorcraft fleets requiring regular upgrades and blade replacements. MRO companies are leveraging digital twin technologies and AI diagnostics to provide cost-efficient, condition-based maintenance services. Fleet operators, including private aviation companies and government agencies, also contribute significantly to market demand as they increasingly prioritize performance optimization, fuel efficiency, and compliance with environmental standards. The rising trend of leasing rotorcraft in developing markets further extends the influence of fleet operators on the blade system ecosystem.

North America accounted for the largest market share at 34.6% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 4.7% between 2025 and 2032.

The North American region's dominance stems from extensive defense procurement programs, technological leadership in aerospace, and a highly integrated rotorcraft supply chain. Meanwhile, Asia-Pacific’s rapid growth is driven by rising investments in domestic helicopter manufacturing and increasing demand for civilian and military rotorcraft platforms. Globally, the Rotorcraft Blade System Market shows strong regional divergence influenced by economic development, defense policies, and infrastructure capabilities. Emerging economies are boosting demand through modernization of emergency medical, military, and oil & gas aviation fleets. Advanced economies are pushing technological frontiers in active blade control, noise suppression, and smart materials. Regional disparities in certification processes and raw material access are shaping supply chain strategies, with global OEMs localizing production. This trend is expected to continue as geopolitical and environmental considerations drive innovation and regional manufacturing expansion in the rotorcraft blade system sector.

Defense Modernization and Composite Blade Innovation Drive Growth

North America held a commanding 34.6% share of the global Rotorcraft Blade System Market in 2024, driven primarily by its large-scale defense procurement and modernization initiatives. Military contracts for advanced helicopters like the UH-60 Black Hawk and CH-53K are fueling high-volume demand for next-generation rotor blades featuring noise-reducing tip designs and smart sensors. Additionally, robust support from the U.S. government through R&D grants and military innovation hubs is accelerating the adoption of carbon fiber-reinforced blade materials. The Federal Aviation Administration's updated certification standards are streamlining compliance for rotorcraft component upgrades. Digital transformation across OEMs and MRO providers is enabling predictive maintenance capabilities, while the integration of AI-driven diagnostics into blade lifecycle management has become a standard in new aircraft programs.

Eco-Efficient Blade Design and Multi-Nation Defense Programs Fuel Market Activity

Holding a 26.3% market share in 2024, the region is a hub for sustainable aviation innovations and collaborative defense efforts. Key markets like Germany, France, and the UK are advancing rotorcraft blade technology under multilateral programs such as the European Future Combat Air System. Regulatory pressure from the European Union to reduce aviation emissions is pushing manufacturers toward noise-reducing and lightweight composite blade systems. Germany’s push for net-zero aerospace and France’s Blade Technology Initiative are reshaping R&D priorities. Adoption of emerging technologies such as laser-guided blade shaping and digital twin systems for fatigue analysis is rapidly increasing across OEMs and Tier 1 suppliers.

Defense Expansion and Indigenous Manufacturing Spur Blade System Growth

Asia-Pacific emerged as the fastest-growing region in the Rotorcraft Blade System Market in 2024, with countries like China, India, and Japan rapidly scaling rotorcraft fleets for both defense and commercial applications. China’s expansion of indigenous helicopter programs such as the Z-20 is boosting demand for locally produced rotor blades, while India’s Light Combat Helicopter and LUH programs are creating opportunities for blade system suppliers. Regional OEMs are investing in advanced blade molding and bonding facilities, supported by government-driven aerospace corridors. Innovation hubs in Japan and South Korea are focusing on AI-integrated blade diagnostics and high-speed tiltrotor platforms, contributing to increased localization and supply chain resilience.

Fleet Modernization and Offshore Oil Demand Shape Market Trajectory

South America represented approximately 6.9% of the global Rotorcraft Blade System Market in 2024, with Brazil and Argentina leading regional demand. Brazil’s strong aerospace infrastructure and its domestic rotorcraft production under Embraer and Helibras are pivotal to blade system requirements. Fleet modernization in oil & gas and utility sectors is driving retrofitting of rotor blades with lighter materials and corrosion-resistant coatings. Argentina is witnessing a rise in the use of rotorcraft for border surveillance and emergency services, supporting increased procurement of durable blade systems. Government trade policies encouraging aerospace imports and local blade assembly are enhancing regional manufacturing efficiency.

Oil Sector Demand and Strategic Defense Investments Bolster Market Growth

The Middle East & Africa accounted for 4.2% of the global Rotorcraft Blade System Market in 2024, led by growth in UAE and South Africa. Rotorcraft demand in the oil & gas, construction, and defense sectors is significantly boosting blade system procurement. The UAE’s focus on autonomous helicopter development and partnerships with global OEMs are catalyzing technological modernization in blade design and performance tracking. South Africa’s investments in paramilitary rotorcraft fleets are stimulating demand for high-durability, all-weather rotor blades. Local governments are also streamlining certification and trade partnerships to attract foreign investments in regional MRO and blade component production facilities.

United States – 30.8% Market Share

High production capacity, advanced defense procurement programs, and leading aerospace OEM infrastructure.

China – 14.6% Market Share

Strong end-user demand in defense and civil aviation, supported by national rotorcraft manufacturing initiatives and rapid fleet expansion.

The Rotorcraft Blade System market features a moderately consolidated competitive landscape with over 35 active manufacturers and Tier 1 suppliers operating globally. Leading players are differentiated by their technological capabilities, vertically integrated production models, and strong relationships with defense and civil aviation OEMs. Market competition is intensifying as companies focus on expanding their product portfolios with advanced composite blade technologies, noise-reduction features, and smart sensor integration. Strategic alliances and long-term contracts with military and commercial aviation entities are common, particularly among manufacturers in the United States, France, and Japan.

Key players are increasingly investing in R&D to develop lightweight, durable, and aerodynamically optimized blade systems for emerging rotorcraft types, including eVTOL platforms and unmanned aerial vehicles. Mergers and acquisitions have become a critical route for market expansion, enabling companies to access new technologies and enter underserved geographic regions. Additionally, the growing demand for aftermarket blade replacements and retrofitting is prompting established companies to enhance their MRO service capabilities. Competitive dynamics are further shaped by compliance with international airworthiness regulations and the ability to meet the customization needs of military procurement agencies.

Kaman Aerospace Corporation

Airbus Helicopters

The Boeing Company

Leonardo S.p.A.

Korea Aerospace Industries Ltd. (KAI)

MD Helicopters, LLC

Bell Textron Inc.

Hindustan Aeronautics Limited (HAL)

AVIC Helicopter Company

Enstrom Helicopter Corporation

Technological advancements are rapidly transforming the Rotorcraft Blade System Market, with a strong emphasis on materials science, manufacturing automation, and integrated digital systems. One of the most significant developments is the widespread adoption of advanced composite materials such as carbon fiber-reinforced polymers and glass fiber laminates. These materials enhance blade strength, reduce overall weight, and offer superior fatigue and corrosion resistance, making them essential for both military and commercial rotorcraft platforms.

Active rotor blade technologies are gaining traction, particularly with the integration of blade pitch modulation and tip deflection systems. These innovations improve aerodynamic efficiency and reduce acoustic signatures, addressing the growing demand for quieter urban air mobility solutions. The use of embedded piezoelectric sensors and fiber-optic strain gauges within blades is enabling real-time health monitoring, allowing predictive maintenance that minimizes downtime and enhances fleet reliability.

Additive manufacturing is also playing an important role in prototyping and tooling, enabling quicker development cycles and customized blade configurations. Furthermore, AI and machine learning algorithms are now being employed for simulating airflow dynamics and predicting stress loads during high-speed maneuvers. These technologies are not only improving performance but are also contributing to cost control and safety compliance in an increasingly regulated aviation environment.

• In February 2024, Airbus Helicopters successfully tested a new composite blade system on the H160 platform, achieving a 15% reduction in vibration levels and enhanced durability under adverse weather conditions.

• In October 2023, Bell Textron unveiled a modular rotor blade upgrade kit for the Bell 412 series, incorporating lighter carbon materials and reducing maintenance time by approximately 18% per flight hour.

• In May 2024, KAI introduced a smart blade diagnostics solution integrated with AI sensors to monitor real-time blade stress and fatigue, enabling earlier fault detection across military helicopter fleets.

• In December 2023, Leonardo completed the installation of an automated blade manufacturing line in Italy, capable of producing high-tolerance rotor blades with a 20% increase in production efficiency.

The Rotorcraft Blade System Market Report offers an in-depth analysis of key components, technologies, and strategic developments across the global rotorcraft blade industry. The report comprehensively covers market segments including main rotor blades, tail rotor blades, and advanced composite variants used in military, commercial, and emerging eVTOL applications. It outlines technological evolution, such as the shift toward noise-reducing blade geometries, smart sensor integration, and AI-assisted condition monitoring tools.

Geographically, the report includes analysis across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, identifying region-specific demand drivers such as defense modernization, indigenous rotorcraft production, and infrastructure growth. It also includes segmentation based on end-user types such as OEMs, MRO providers, and fleet operators, highlighting their respective roles and investment priorities.

Key areas of focus include advancements in materials, like thermoplastics and fiber-reinforced composites, as well as the adoption of automated and additive manufacturing in blade fabrication. The report evaluates current market dynamics, competitive landscapes, and regulatory frameworks influencing development and distribution. Additionally, it explores emerging opportunities in retrofitting legacy platforms and supplying rotor blades for unmanned aerial systems, providing valuable strategic insights for manufacturers, investors, and government stakeholders.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 2,322 Million |

|

Market Revenue in 2032 |

USD 2,987.44 Million |

|

CAGR (2025 - 2032) |

3.2% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Kaman Aerospace Corporation, Airbus Helicopters, The Boeing Company, Leonardo S.p.A., Korea Aerospace Industries Ltd. (KAI), MD Helicopters, LLC, Bell Textron Inc., Hindustan Aeronautics Limited (HAL), AVIC Helicopter Company, Enstrom Helicopter Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |