Reports

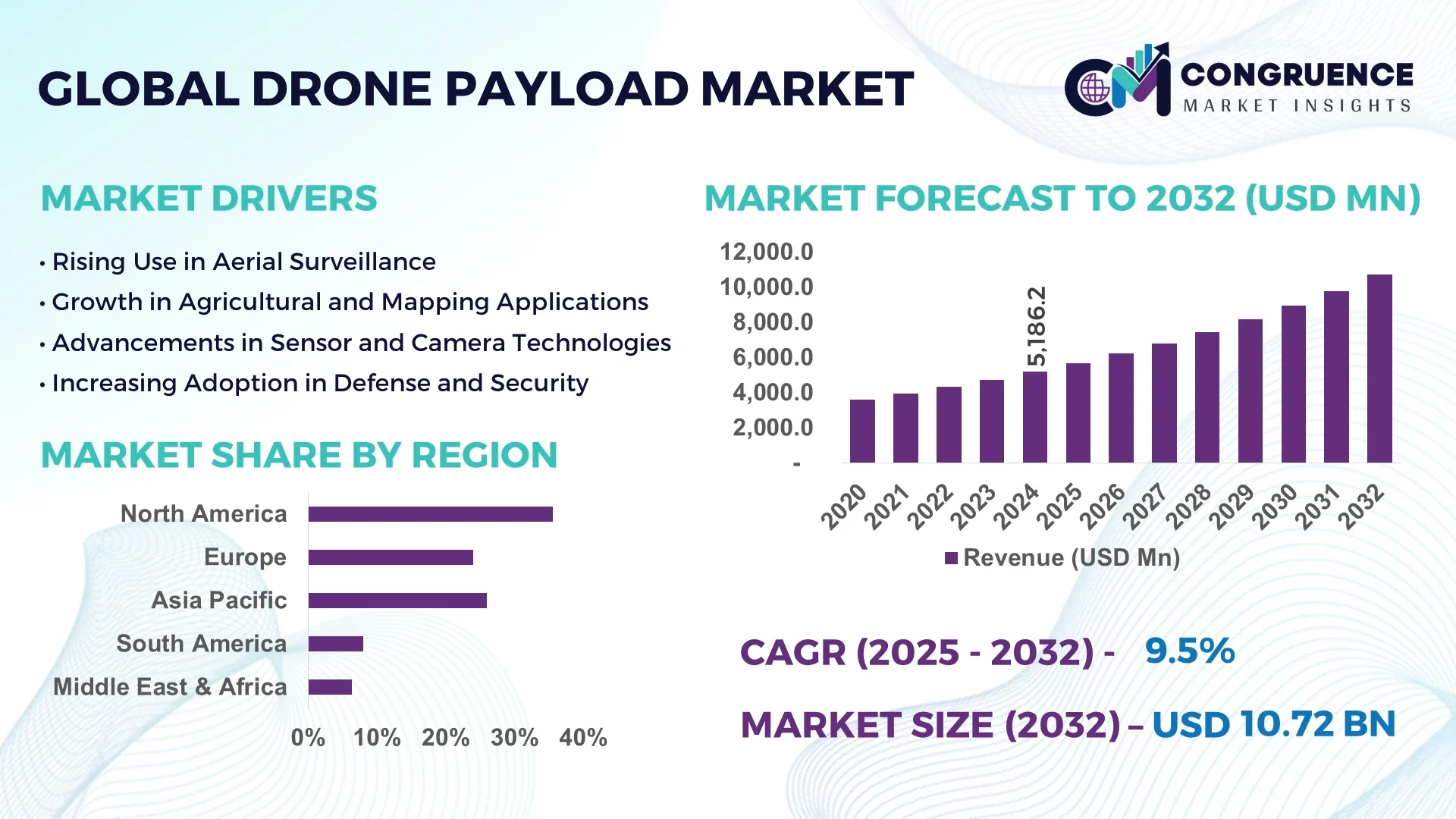

The Global Drone Payload Market was valued at USD 5,186.24 Million in 2024 and is anticipated to reach a value of USD 10,719.29 Million by 2032 expanding at a CAGR of 9.5% between 2025 and 2032.

To Learn More About This Report, Request A Free Sample Copy

In the United States, drone payload manufacturing has reached new heights with leading companies significantly ramping up their R&D investments, particularly in military-grade imaging sensors and precision-guided payloads. The nation’s ecosystem supports rapid innovation, with defense, agriculture, and logistics industries driving sustained demand for high-performance drone payload systems.

The Drone Payload Market is evolving rapidly across several sectors, including defense, agriculture, energy, and logistics. Defense applications remain dominant, leveraging advanced payloads such as ISR (intelligence, surveillance, and reconnaissance) sensors, communication systems, and laser designators to enhance operational capabilities. In agriculture, multispectral and hyperspectral imaging payloads are transforming crop monitoring and yield optimization. Recent advancements in miniaturized payloads, lightweight materials, and sensor fusion technologies are reshaping payload integration strategies. Regulatory developments in North America and Europe are fostering safer UAV operations, while favorable economic incentives in Asia-Pacific are fueling domestic drone manufacturing. Moreover, the adoption of AI-powered analytics tools embedded within payload systems is improving decision-making accuracy and real-time responsiveness. As global drone deployments rise, increasing payload customization and cross-industry use cases continue to shape a resilient and future-ready Drone Payload Market.

Artificial intelligence is reshaping the operational landscape of the Drone Payload Market, delivering revolutionary capabilities that redefine how drone systems function across multiple industries. AI integration has led to real-time data interpretation, target recognition, and autonomous navigation—drastically enhancing mission efficiency and precision. In military reconnaissance, AI-enhanced payloads are capable of detecting objects, classifying threats, and recommending responses autonomously, thereby accelerating situational awareness. In agriculture, AI algorithms embedded in imaging payloads process multispectral data to provide predictive crop health analytics, enabling farmers to reduce pesticide usage and optimize irrigation.

AI also brings measurable advancements in infrastructure inspections. Smart payloads with AI-enabled defect recognition software detect cracks or corrosion in hard-to-reach structures like wind turbines or pipelines, improving maintenance planning and minimizing human risk. Additionally, in environmental monitoring, AI-classified data from payloads streamlines pattern recognition for deforestation, wildlife tracking, and climate modeling. Logistics companies now deploy drones with AI-calibrated payloads for efficient route mapping and package delivery assessment, reducing fuel use and turnaround time.

From real-time object tracking to high-speed image classification, AI integration is transforming the Drone Payload Market from traditional sensor carriers into autonomous, data-driven aerial systems. This convergence of AI and payload design is not only optimizing performance but also opening new verticals for strategic expansion, positioning the market for a tech-driven evolution in the coming years.

“In April 2024, a leading aerospace firm deployed an AI-powered hyperspectral payload system capable of identifying over 25 vegetation indices in real time during crop surveillance missions. This technology reduced image processing times by 67% and increased actionable data output by 42%, setting a benchmark in precision agriculture payload performance.”

The surge in precision agriculture and environmental surveillance is a critical growth driver in the Drone Payload Market. High-resolution multispectral and hyperspectral imaging payloads now enable farmers to monitor crop health, detect pest infestations, and optimize irrigation strategies with pinpoint accuracy. These technologies are reducing operational inefficiencies and increasing agricultural yields. Additionally, environmental monitoring agencies are deploying drones equipped with air quality sensors, thermal cameras, and atmospheric payloads to track deforestation, monitor wildfire outbreaks, and assess biodiversity in remote areas. This expansion of functional applications is pushing payload innovation, encouraging the development of modular systems and adaptive sensor technologies.

Despite growing adoption, regulatory complexities remain a major barrier in the Drone Payload Market. Many countries enforce strict operational limits on drones, especially in urban areas, near airports, and over critical infrastructure. Payloads with advanced surveillance or communication features often fall under dual-use technology regulations, complicating export and cross-border usage. In addition, inconsistencies in licensing procedures, certification requirements, and no-fly zone policies delay commercial deployments. These regulatory hurdles are particularly challenging for startups and mid-sized manufacturers, restricting innovation and elongating product development cycles. The fragmented nature of global drone laws continues to hinder seamless payload adoption across markets.

The integration of AI and edge computing presents a substantial opportunity in the Drone Payload Market. Advanced payloads embedded with onboard AI processors are enabling real-time image recognition, threat detection, and autonomous decision-making without requiring cloud access. These intelligent payload systems are especially valuable in time-sensitive missions such as search and rescue, defense reconnaissance, and disaster response. Furthermore, edge computing allows for data encryption, privacy preservation, and latency reduction, making drones more secure and responsive. This opens new avenues for drone operations in privacy-sensitive sectors such as healthcare delivery, border security, and infrastructure surveillance.

The Drone Payload Market faces critical challenges associated with payload design limitations, particularly related to weight, energy consumption, and data transfer efficiency. Heavy or power-hungry payloads reduce drone flight time, limit operational range, and demand more robust airframes. Balancing payload capacity with drone endurance remains a persistent engineering hurdle. Furthermore, high-resolution imaging and LiDAR systems generate large volumes of data, requiring fast and secure transmission channels, which may not be viable in remote or bandwidth-limited environments. These technical constraints often lead to performance trade-offs and increased costs, making it difficult to meet operational demands in high-intensity mission profiles.

• Increased Adoption of Multispectral and Hyperspectral Imaging Payloads: Multispectral and hyperspectral imaging payloads are gaining traction, particularly in agriculture and environmental applications. These payloads enable highly detailed spectral analysis, allowing for real-time crop health assessments, disease detection, and precision fertilization. In 2024, over 38% of agricultural drone operations globally incorporated some form of multispectral imaging, a notable rise from 27% in 2022. Their adoption is also expanding into areas like water quality monitoring and coastal management, where fine spectral resolution is essential for detecting pollutants and underwater vegetation.

• Surge in Lightweight and Miniaturized Payload Innovations: The shift toward smaller drone platforms has accelerated the demand for lightweight, high-functionality payloads. Manufacturers are now integrating capabilities such as high-definition video capture, GPS, thermal sensors, and LiDAR into compact units under 1.5 kg. In 2024, over 60% of newly launched commercial drones featured payloads optimized for weight-efficiency, enabling longer flight times and greater range. This trend is especially evident in urban logistics, where drones must navigate tight spaces and carry lighter payloads across complex city environments.

• Expansion of Dual-Use Payloads for Civil and Defense Applications: The Drone Payload Market is witnessing growth in dual-use payload systems that serve both civilian and military missions. Technologies such as encrypted communication modules, thermal optics, and AI-driven surveillance tools are now being adapted for use across public safety, disaster management, and defense intelligence. For instance, thermal payloads originally developed for border surveillance are now used in wildfire detection and emergency response coordination. The versatility of these payloads is driving procurement efficiency and boosting demand across multiple government sectors.

• Rise in Real-Time Data Processing with Onboard AI Chips: Drones equipped with AI chips in their payloads are now capable of processing data in-flight, significantly reducing the need for post-mission analytics. This advancement supports high-speed object detection, behavioral analytics, and autonomous navigation, which are critical in sectors such as security, mining, and precision agriculture. In 2024, approximately 31% of enterprise-grade drones were fitted with payloads featuring real-time data processing capabilities, up from 18% in 2021. This trend is expected to continue as businesses prioritize operational responsiveness and data-driven decision-making.

The Drone Payload Market is strategically segmented into three core dimensions: type, application, and end-user. Each segment is experiencing distinct growth patterns, shaped by evolving technological capabilities and shifting demand dynamics across sectors. By type, payloads such as cameras, sensors, radars, and LiDAR systems are redefining operational capabilities in real-time imaging and environmental analysis. On the application front, surveillance, mapping, and delivery lead demand, particularly in sectors such as defense, agriculture, and logistics. Meanwhile, end-user segmentation highlights the dominance of the military and defense sectors, with commercial and environmental agencies emerging as dynamic growth drivers. As industries increasingly demand faster, lighter, and more intelligent payloads, customization and adaptability are becoming pivotal to capturing market share. This segmentation landscape reflects a robust mix of established use cases and evolving opportunities, guiding strategic investments and product innovation.

Payload types in the Drone Payload Market include cameras, sensors, radar systems, LiDAR modules, and others such as signal jammers and communication relays. Camera payloads remain the dominant type, favored for their essential role in surveillance, aerial photography, inspection, and media applications. High-definition video and real-time streaming capabilities are pushing demand, especially in infrastructure inspection and public safety missions. LiDAR payloads are the fastest-growing type, driven by increasing use in terrain mapping, forestry management, mining surveys, and autonomous vehicle navigation. Their precision in generating high-resolution 3D models with millimeter-level accuracy is making them indispensable in geospatial and construction sectors. Other payload types such as infrared and multispectral sensors have carved out niche roles in agriculture and disaster response. Radar payloads, although less common, are gaining importance in defense and all-weather navigation applications. The diversification in payload functionality is encouraging manufacturers to invest in modular payload systems for multi-role adaptability.

The Drone Payload Market is segmented by application into surveillance, mapping and surveying, delivery, disaster management, inspection, and others. Surveillance remains the leading application, especially within defense, law enforcement, and border security sectors. Payloads equipped with thermal and night-vision imaging support continuous monitoring, threat detection, and reconnaissance missions. Mapping and surveying applications are growing at the fastest pace, fueled by urban infrastructure development, smart agriculture practices, and mining operations. The integration of LiDAR and high-resolution photogrammetry cameras has enhanced the accuracy and speed of terrain modeling and asset management. Delivery applications are also expanding, especially in healthcare and e-commerce. Payloads designed for medical supplies and lightweight packages are in demand due to time-sensitive and remote delivery requirements. Meanwhile, inspection tasks—particularly for power lines, pipelines, and wind turbines—benefit from specialized sensors that improve safety and operational efficiency. Disaster management, though less frequent, plays a vital role during emergencies, with drones deploying thermal sensors and loudspeaker payloads for search and rescue operations.

End-user segmentation in the Drone Payload Market spans military and defense, commercial enterprises, environmental agencies, public safety departments, and research institutions. Military and defense remains the dominant end-user segment, with demand for advanced surveillance, reconnaissance, and targeting payloads. High-security missions rely on thermal, radar, and encrypted communication payloads for precision and reliability. The commercial segment is the fastest-growing, driven by adoption across agriculture, logistics, infrastructure, and real estate. Businesses are integrating drones into daily operations for inspection, crop analytics, delivery, and aerial imaging—enabled by compact, multi-functional payloads that provide real-time insights and cost reductions. Environmental agencies are increasingly deploying drones with gas sensors, atmospheric payloads, and imaging systems to monitor deforestation, pollution, and wildlife habitats. Public safety agencies are investing in payloads for crowd monitoring, emergency response, and crime scene mapping. Lastly, research institutions utilize scientific-grade payloads for climate studies, geological surveys, and exploratory missions, contributing valuable data to global knowledge systems.

North America accounted for the largest market share at 35.6% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.1% between 2025 and 2032.

To Learn More About This Report, Request A Free Sample Copy

North America's leading position stems from robust demand across defense, agriculture, and energy sectors, combined with aggressive innovation in payload technologies. Meanwhile, Asia-Pacific's rapid industrialization and government-led drone deployment initiatives are accelerating market expansion across China, India, and Southeast Asia. Globally, drone payload consumption is being influenced by rising demand for advanced aerial surveillance, infrastructure inspection, and smart agriculture, along with increasing payload customization. Regions are also leveraging AI-enabled payloads and cloud-based analytics to enhance decision-making and mission performance. Regulatory advancements and increased R&D spending are further fostering innovation in lightweight, multifunctional payload systems globally.

Adoption of Intelligent Payloads Across Enterprise and Military Applications

The North American Drone Payload Market held a commanding 35.6% share in 2024, driven by defense and enterprise applications. The U.S. Department of Defense continues to invest in drones with encrypted communication and thermal imaging payloads, while commercial sectors—especially agriculture, logistics, and construction—are incorporating AI-powered multispectral sensors for operational efficiency. Recent regulatory support, including FAA’s expanded BVLOS (Beyond Visual Line of Sight) guidelines, is boosting commercial drone usage. Furthermore, Canadian energy firms are deploying drones equipped with LiDAR and gas detection payloads for pipeline monitoring. Technological modernization, including onboard edge processing and sensor miniaturization, is facilitating more diverse and scalable drone applications across the continent.

Smart City Projects and Green Tech Fuel Drone Sensor Demand

The European Drone Payload Market accounted for approximately 24.1% of the global share in 2024, with strong demand from Germany, France, and the United Kingdom. Key applications include environmental monitoring, urban planning, and infrastructure assessment, where LiDAR and hyperspectral payloads are widely deployed. The European Union Aviation Safety Agency (EASA) continues to streamline drone operation protocols, while regional sustainability goals encourage the use of drones for emissions monitoring and forest preservation. Germany leads in drone manufacturing, while the UK is spearheading AI integration into payload designs. Ongoing investment in 5G infrastructure and data-driven governance is amplifying the adoption of intelligent drone payload solutions.

Infrastructure Expansion and R&D Propel Payload Integration

The Asia-Pacific Drone Payload Market emerged as the fastest-growing segment in 2024, with a market share of 21.7%. China remains the largest contributor, followed by India and Japan, due to massive investments in infrastructure, agriculture tech, and public safety solutions. Government-backed programs in India and South Korea are supporting drone adoption in agriculture and mining, spurring demand for LiDAR and multispectral payloads. Japan is leveraging drones with AI-powered sensors for disaster response and aging infrastructure inspection. Regional tech hubs such as Shenzhen and Bengaluru are leading payload innovation, focusing on miniaturization and real-time edge computing. The market is further bolstered by strong manufacturing capabilities and competitive drone exports.

Public Sector Projects and Energy Surveillance Drive Payload Use

In South America, the Drone Payload Market is expanding with a regional share of 8.2%, led by Brazil and Argentina. Brazil has adopted drones for agricultural surveying and hydrological mapping, often using thermal and multispectral payloads to manage crop cycles and water resources. The region’s growing energy infrastructure—particularly in wind and hydroelectric power—has prompted the use of drones equipped with high-resolution imaging systems for turbine and transmission line inspections. Governments are also incentivizing the use of drone technology through reduced import duties and R&D grants. Argentina is investing in drone-based logistics, deploying payload-equipped UAVs for remote medical deliveries and disaster response operations.

Energy Infrastructure and Security Needs Boost Sensor Utilization

The Middle East & Africa Drone Payload Market continues to evolve, supported by oil and gas surveillance, construction projects, and national security measures. The region accounted for approximately 10.4% of global market share in 2024. The UAE is advancing AI-integrated payload technology for surveillance and smart city applications, while South Africa utilizes LiDAR systems for mining operations and environmental management. Saudi Arabia has launched drone-focused digital transformation programs, increasing payload adoption across its Vision 2030 agenda. Furthermore, favorable drone regulations and foreign technology partnerships are helping to enhance the quality and functionality of locally deployed payloads.

United States – 30.4% market share

High demand from military and enterprise sectors, along with strong domestic production capacity, drives dominance in the Drone Payload Market.

China – 18.7% market share

Leadership in drone manufacturing and heavy integration of advanced payloads across agriculture and infrastructure sectors supports its market strength.

The Drone Payload Market is characterized by intense competition, shaped by a mix of global drone manufacturers, payload technology innovators, and niche solution providers. As of 2024, the market comprises over 120 active competitors, ranging from established aerospace players to emerging sensor developers. Companies are increasingly focusing on multi-sensor payload integration, edge AI capabilities, and data interoperability to differentiate themselves. The competitive landscape is being reshaped through strategic alliances, such as cross-industry partnerships with telecom providers for 5G-enabled payload communication and collaborations with agritech firms to co-develop specialized imaging payloads.

Several players are prioritizing miniaturization and modular payload designs, allowing for increased flexibility and mission-specific customization. Recent product launches include next-generation LiDAR systems, thermal imaging sensors with improved range, and AI-enabled cameras for real-time data analytics. Additionally, mergers and acquisitions have surged, especially in North America and Europe, where companies are consolidating payload manufacturing with drone platform capabilities. The growing emphasis on intellectual property protection, patent filings, and R&D investments is intensifying the innovation race, especially in areas like advanced signal processing, cybersecurity for data transmission, and autonomous decision-making payloads.

DJI Innovations

FLIR Systems Inc.

Lockheed Martin Corporation

Teledyne Technologies Incorporated

Parrot Drones SAS

Northrop Grumman Corporation

PrecisionHawk Inc.

AgEagle Aerial Systems Inc.

AeroVironment Inc.

Delair SAS

The Drone Payload Market is undergoing rapid technological transformation, driven by advancements in sensor capabilities, miniaturization, and AI integration. One of the most significant developments is the adoption of edge AI processing units within payloads, enabling real-time decision-making without requiring continuous connectivity to ground stations. These smart payloads can analyze visual and thermal data onboard, significantly improving response times in applications like disaster monitoring and surveillance. Another critical innovation is the evolution of multispectral and hyperspectral imaging systems, now widely used in precision agriculture, mining, and environmental monitoring. These payloads deliver high-resolution data across multiple wavelengths, allowing for more accurate vegetation health analysis, mineral detection, and water quality monitoring. Improvements in spectral resolution and sensor sensitivity are allowing drones to conduct complex analytical tasks that previously required satellite or manned aircraft support.

LiDAR technology continues to grow in adoption, particularly for infrastructure inspection and topographic mapping. New-generation LiDAR payloads are more compact and lightweight, offering centimeter-level accuracy with reduced power consumption. Additionally, thermal imaging sensors are being refined for industrial inspections and search-and-rescue missions, offering better frame rates, extended range, and enhanced contrast under varied lighting conditions. The integration of secure wireless communication protocols and encrypted data links is also gaining traction, ensuring safer transmission of mission-critical information. Meanwhile, modular payload systems are allowing end-users to switch between different sensor types easily, expanding operational flexibility across diverse missions. The convergence of drone payloads with cloud-based analytics and IoT ecosystems is opening new frontiers for remote diagnostics, predictive maintenance, and cross-platform data integration.

• In March 2024, DJI launched the Zenmuse L2 LiDAR payload, featuring a high-precision IMU and enhanced point cloud accuracy. The system supports dense forest mapping and infrastructure scanning with improved real-time data collection and post-processing efficiency.

• In September 2023, Northrop Grumman introduced a modular multispectral payload for its tactical UAVs, designed for military and emergency response missions. The payload supports real-time terrain mapping, threat detection, and environmental analysis under varied weather conditions.

• In February 2024, Teledyne FLIR unveiled its Boson+ thermal camera core upgrade with a sensitivity of <20mK and enhanced image processing capabilities, enabling more accurate thermal inspections in industrial and public safety applications.

• In November 2023, Parrot launched a new 4G-connected payload system embedded with edge-AI analytics, allowing agricultural and construction drones to process multispectral imagery in-field without relying on cloud connectivity.

The Drone Payload Market Report offers a comprehensive evaluation of the global industry, covering a wide range of payload technologies, application sectors, and regional landscapes. This detailed analysis encompasses over 15 key payload types, including imaging systems, LiDAR modules, multispectral sensors, radar systems, gimbals, and communication equipment. It also addresses the rapid growth of AI-enabled payloads and modular systems that are enabling multifunctional drone capabilities across industrial and commercial operations. The report provides segmentation insights into major application areas, such as defense and security, agriculture, construction, environmental monitoring, energy and utilities, logistics, and emergency response. Each application is evaluated for its adoption rate, integration challenges, and current technological alignment, with a special focus on how real-time data acquisition and advanced analytics are enhancing decision-making processes across industries.

Geographically, the report analyzes five core regions: North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. Regional assessments include demand concentration, regulatory environment, infrastructure readiness, and innovation dynamics in countries such as the U.S., China, Germany, India, Brazil, and the UAE. Additionally, the report explores emerging segments such as drone payloads for healthcare deliveries, mining surveillance, and smart city infrastructure monitoring. These niche segments are gaining traction due to advancements in compact sensor design and drone autonomy, making them attractive to forward-looking businesses and governments seeking scalable and sustainable aerial solutions.

North America accounted for the largest market share at 35.6% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.1% between 2025 and 2032.

North America's leading position stems from robust demand across defense, agriculture, and energy sectors, combined with aggressive innovation in payload technologies. Meanwhile, Asia-Pacific's rapid industrialization and government-led drone deployment initiatives are accelerating market expansion across China, India, and Southeast Asia. Globally, drone payload consumption is being influenced by rising demand for advanced aerial surveillance, infrastructure inspection, and smart agriculture, along with increasing payload customization. Regions are also leveraging AI-enabled payloads and cloud-based analytics to enhance decision-making and mission performance. Regulatory advancements and increased R&D spending are further fostering innovation in lightweight, multifunctional payload systems globally.

Adoption of Intelligent Payloads Across Enterprise and Military Applications

The North American Drone Payload Market held a commanding 35.6% share in 2024, driven by defense and enterprise applications. The U.S. Department of Defense continues to invest in drones with encrypted communication and thermal imaging payloads, while commercial sectors—especially agriculture, logistics, and construction—are incorporating AI-powered multispectral sensors for operational efficiency. Recent regulatory support, including FAA’s expanded BVLOS (Beyond Visual Line of Sight) guidelines, is boosting commercial drone usage. Furthermore, Canadian energy firms are deploying drones equipped with LiDAR and gas detection payloads for pipeline monitoring. Technological modernization, including onboard edge processing and sensor miniaturization, is facilitating more diverse and scalable drone applications across the continent.

Smart City Projects and Green Tech Fuel Drone Sensor Demand

The European Drone Payload Market accounted for approximately 24.1% of the global share in 2024, with strong demand from Germany, France, and the United Kingdom. Key applications include environmental monitoring, urban planning, and infrastructure assessment, where LiDAR and hyperspectral payloads are widely deployed. The European Union Aviation Safety Agency (EASA) continues to streamline drone operation protocols, while regional sustainability goals encourage the use of drones for emissions monitoring and forest preservation. Germany leads in drone manufacturing, while the UK is spearheading AI integration into payload designs. Ongoing investment in 5G infrastructure and data-driven governance is amplifying the adoption of intelligent drone payload solutions.

Infrastructure Expansion and R&D Propel Payload Integration

The Asia-Pacific Drone Payload Market emerged as the fastest-growing segment in 2024, with a market share of 21.7%. China remains the largest contributor, followed by India and Japan, due to massive investments in infrastructure, agriculture tech, and public safety solutions. Government-backed programs in India and South Korea are supporting drone adoption in agriculture and mining, spurring demand for LiDAR and multispectral payloads. Japan is leveraging drones with AI-powered sensors for disaster response and aging infrastructure inspection. Regional tech hubs such as Shenzhen and Bengaluru are leading payload innovation, focusing on miniaturization and real-time edge computing. The market is further bolstered by strong manufacturing capabilities and competitive drone exports.

Public Sector Projects and Energy Surveillance Drive Payload Use

In South America, the Drone Payload Market is expanding with a regional share of 8.2%, led by Brazil and Argentina. Brazil has adopted drones for agricultural surveying and hydrological mapping, often using thermal and multispectral payloads to manage crop cycles and water resources. The region’s growing energy infrastructure—particularly in wind and hydroelectric power—has prompted the use of drones equipped with high-resolution imaging systems for turbine and transmission line inspections. Governments are also incentivizing the use of drone technology through reduced import duties and R&D grants. Argentina is investing in drone-based logistics, deploying payload-equipped UAVs for remote medical deliveries and disaster response operations.

Energy Infrastructure and Security Needs Boost Sensor Utilization

The Middle East & Africa Drone Payload Market continues to evolve, supported by oil and gas surveillance, construction projects, and national security measures. The region accounted for approximately 10.4% of global market share in 2024. The UAE is advancing AI-integrated payload technology for surveillance and smart city applications, while South Africa utilizes LiDAR systems for mining operations and environmental management. Saudi Arabia has launched drone-focused digital transformation programs, increasing payload adoption across its Vision 2030 agenda. Furthermore, favorable drone regulations and foreign technology partnerships are helping to enhance the quality and functionality of locally deployed payloads.

United States – 30.4% market share

High demand from military and enterprise sectors, along with strong domestic production capacity, drives dominance in the Drone Payload Market.

China – 18.7% market share

Leadership in drone manufacturing and heavy integration of advanced payloads across agriculture and infrastructure sectors supports its market strength.

The Drone Payload Market is characterized by intense competition, shaped by a mix of global drone manufacturers, payload technology innovators, and niche solution providers. As of 2024, the market comprises over 120 active competitors, ranging from established aerospace players to emerging sensor developers. Companies are increasingly focusing on multi-sensor payload integration, edge AI capabilities, and data interoperability to differentiate themselves. The competitive landscape is being reshaped through strategic alliances, such as cross-industry partnerships with telecom providers for 5G-enabled payload communication and collaborations with agritech firms to co-develop specialized imaging payloads.

Several players are prioritizing miniaturization and modular payload designs, allowing for increased flexibility and mission-specific customization. Recent product launches include next-generation LiDAR systems, thermal imaging sensors with improved range, and AI-enabled cameras for real-time data analytics. Additionally, mergers and acquisitions have surged, especially in North America and Europe, where companies are consolidating payload manufacturing with drone platform capabilities. The growing emphasis on intellectual property protection, patent filings, and R&D investments is intensifying the innovation race, especially in areas like advanced signal processing, cybersecurity for data transmission, and autonomous decision-making payloads.

DJI Innovations

FLIR Systems Inc.

Lockheed Martin Corporation

Teledyne Technologies Incorporated

Parrot Drones SAS

Northrop Grumman Corporation

PrecisionHawk Inc.

AgEagle Aerial Systems Inc.

AeroVironment Inc.

Delair SAS

The Drone Payload Market is undergoing rapid technological transformation, driven by advancements in sensor capabilities, miniaturization, and AI integration. One of the most significant developments is the adoption of edge AI processing units within payloads, enabling real-time decision-making without requiring continuous connectivity to ground stations. These smart payloads can analyze visual and thermal data onboard, significantly improving response times in applications like disaster monitoring and surveillance. Another critical innovation is the evolution of multispectral and hyperspectral imaging systems, now widely used in precision agriculture, mining, and environmental monitoring. These payloads deliver high-resolution data across multiple wavelengths, allowing for more accurate vegetation health analysis, mineral detection, and water quality monitoring. Improvements in spectral resolution and sensor sensitivity are allowing drones to conduct complex analytical tasks that previously required satellite or manned aircraft support.

LiDAR technology continues to grow in adoption, particularly for infrastructure inspection and topographic mapping. New-generation LiDAR payloads are more compact and lightweight, offering centimeter-level accuracy with reduced power consumption. Additionally, thermal imaging sensors are being refined for industrial inspections and search-and-rescue missions, offering better frame rates, extended range, and enhanced contrast under varied lighting conditions. The integration of secure wireless communication protocols and encrypted data links is also gaining traction, ensuring safer transmission of mission-critical information. Meanwhile, modular payload systems are allowing end-users to switch between different sensor types easily, expanding operational flexibility across diverse missions. The convergence of drone payloads with cloud-based analytics and IoT ecosystems is opening new frontiers for remote diagnostics, predictive maintenance, and cross-platform data integration.

• In March 2024, DJI launched the Zenmuse L2 LiDAR payload, featuring a high-precision IMU and enhanced point cloud accuracy. The system supports dense forest mapping and infrastructure scanning with improved real-time data collection and post-processing efficiency.

• In September 2023, Northrop Grumman introduced a modular multispectral payload for its tactical UAVs, designed for military and emergency response missions. The payload supports real-time terrain mapping, threat detection, and environmental analysis under varied weather conditions.

• In February 2024, Teledyne FLIR unveiled its Boson+ thermal camera core upgrade with a sensitivity of <20mK and enhanced image processing capabilities, enabling more accurate thermal inspections in industrial and public safety applications.

• In November 2023, Parrot launched a new 4G-connected payload system embedded with edge-AI analytics, allowing agricultural and construction drones to process multispectral imagery in-field without relying on cloud connectivity.

The Drone Payload Market Report offers a comprehensive evaluation of the global industry, covering a wide range of payload technologies, application sectors, and regional landscapes. This detailed analysis encompasses over 15 key payload types, including imaging systems, LiDAR modules, multispectral sensors, radar systems, gimbals, and communication equipment. It also addresses the rapid growth of AI-enabled payloads and modular systems that are enabling multifunctional drone capabilities across industrial and commercial operations. The report provides segmentation insights into major application areas, such as defense and security, agriculture, construction, environmental monitoring, energy and utilities, logistics, and emergency response. Each application is evaluated for its adoption rate, integration challenges, and current technological alignment, with a special focus on how real-time data acquisition and advanced analytics are enhancing decision-making processes across industries.

Geographically, the report analyzes five core regions: North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. Regional assessments include demand concentration, regulatory environment, infrastructure readiness, and innovation dynamics in countries such as the U.S., China, Germany, India, Brazil, and the UAE. Additionally, the report explores emerging segments such as drone payloads for healthcare deliveries, mining surveillance, and smart city infrastructure monitoring. These niche segments are gaining traction due to advancements in compact sensor design and drone autonomy, making them attractive to forward-looking businesses and governments seeking scalable and sustainable aerial solutions.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 5186.24 Million |

|

Market Revenue in 2032 |

USD 10719.29 Million |

|

CAGR (2025 - 2032) |

9.5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End‑User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

John Deere Forestry, Komatsu Forest, Ponsse Plc, Tigercat Industries Inc., Doosan Infracore, Kesla Oyj, Caterpillar Inc., Eco Log Sweden AB, Husqvarna Group, Sennebogen Maschinenfabrik GmbH |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |