Reports

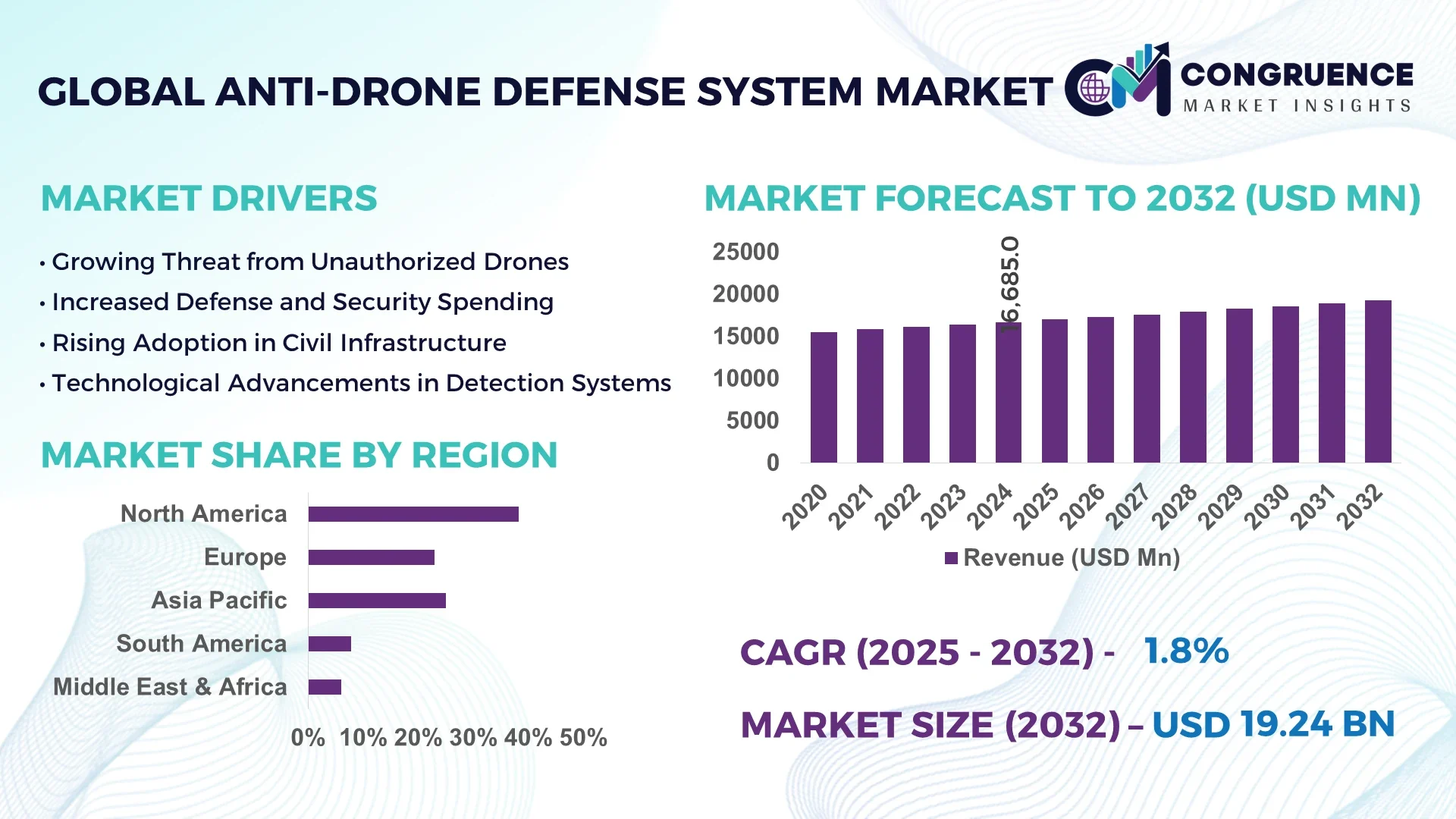

The Global Anti-drone Defense System Market was valued at USD 16,685.02 Million in 2024 and is anticipated to reach a value of USD 19,244.6 Million by 2032 expanding at a CAGR of 1.8% between 2025 and 2032.

The United States stands out in the Anti-drone Defense System market due to its extensive defense infrastructure, high military spending, and integration of AI-driven surveillance in border protection systems. U.S. defense agencies have significantly increased procurement of integrated counter-drone solutions equipped with radar, RF sensors, and optical tracking modules.

The Anti-drone Defense System Market is experiencing robust evolution across civil, commercial, and military sectors due to increasing threats posed by unauthorized drone usage. Key industry sectors driving demand include aerospace, homeland security, critical infrastructure, and event security. In recent years, compact mobile jamming systems and advanced laser interception technologies have disrupted the traditional market landscape. Additionally, government regulations have encouraged public and private stakeholders to invest in scalable and modular defense platforms. The demand for drone detection and neutralization systems is surging across urban areas, airports, and sensitive industrial zones. With the rise of drone swarms and AI-enabled reconnaissance threats, multi-layered defense strategies integrating kinetic and non-kinetic countermeasures are being widely adopted. Regional consumption is particularly high in North America, Europe, and parts of the Middle East, where critical infrastructure faces heightened risk. Emerging trends include the integration of machine learning algorithms, rapid-deployment systems, and real-time geofencing technologies. The future outlook points toward compact, cost-effective solutions with reduced false detection rates, tailored for both government and enterprise applications.

Artificial Intelligence (AI) is reshaping the Anti-drone Defense System Market by enabling faster, smarter, and more autonomous threat detection and neutralization processes. AI-powered systems are now capable of analyzing drone flight behavior, trajectory, and communication patterns in real time, allowing for highly accurate threat classification. These advanced solutions significantly reduce human intervention, minimizing response times during critical security breaches. Enhanced machine learning models are also being integrated into drone defense platforms to continually learn from new threats and adjust operational strategies dynamically.

Within the defense ecosystem, AI contributes to the development of multi-sensor fusion capabilities, where data from radar, RF detectors, visual sensors, and acoustic devices are aggregated and analyzed to improve situational awareness. This has led to the emergence of next-generation counter-unmanned aerial systems (C-UAS) capable of adapting to evolving threats such as autonomous swarms and stealth drones. AI has also enabled predictive threat analytics that forecast potential drone incursions, enhancing perimeter defense and surveillance accuracy.

Furthermore, AI’s role in signal recognition and deep learning has elevated the functionality of electronic jamming devices. These smart jammers selectively disrupt communication links without affecting surrounding systems. AI is also increasingly utilized in command and control (C2) systems, offering real-time decision support and streamlined communication between integrated defense components. As nations upgrade their security infrastructure, the integration of AI in the Anti-drone Defense System Market is becoming a standard practice, especially for mission-critical environments such as airports, power plants, and military bases. This AI-driven transformation is setting the foundation for autonomous, intelligent, and fully integrated airspace security networks worldwide.

“In 2024, a European defense contractor deployed an AI-integrated anti-drone solution that reduced false positive detection rates by 38% while improving threat interception accuracy by 52% through machine learning-enhanced sensor fusion in urban surveillance zones.”

The increasing frequency of unauthorized drone activities near critical infrastructure such as airports, nuclear facilities, and government buildings is a major factor driving the Anti-drone Defense System Market. These facilities face elevated risks from surveillance drones, potential sabotage, and disruption of operations. For instance, airports across the globe have reported dozens of flight delays due to drone incursions. As a result, there is growing demand for counter-UAV technologies capable of real-time detection and threat neutralization. Innovations like radar-integrated RF detection systems and AI-enabled vision modules have become vital in addressing these concerns. The defense and homeland security sectors are heavily investing in smart defense layers that offer automatic threat classification and rapid response capabilities, thereby elevating the deployment of anti-drone systems.

Despite the growing necessity for airspace defense, the high cost of deploying advanced Anti-drone Defense System technologies remains a limiting factor. Many defense-grade solutions require multi-sensor configurations, real-time data processing infrastructure, and high-performance software interfaces—all of which demand substantial investment. For countries or sectors with limited budgets, such as small airports, industrial parks, or remote power plants, full-scale integration remains economically challenging. Furthermore, terrain variability—urban vs. rural, flatlands vs. mountains—requires customized system setups, increasing costs related to calibration, deployment logistics, and post-installation testing. These financial and infrastructural complexities delay adoption, especially among developing nations and small-scale commercial operators.

The Anti-drone Defense System Market is experiencing rising demand for mobile and rapidly deployable systems suited for temporary or dynamic environments. Law enforcement agencies, security firms, and event organizers increasingly seek compact, transportable counter-drone solutions that can be set up within hours and adapted to diverse security scenarios. This demand opens avenues for manufacturers to innovate in lightweight, modular technologies powered by AI and battery-efficient electronics. For example, mobile jamming units and hand-held detection tools are being adopted for temporary public events, VIP protection zones, and border security operations. The portability trend is also gaining momentum in military contexts, particularly in tactical missions where fixed installations are impractical.

A key challenge in the Anti-drone Defense System Market is the lack of unified global regulations governing drone detection and mitigation. While some countries allow active countermeasures like signal jamming or drone takedown, others restrict such actions due to safety and privacy concerns. This inconsistency complicates cross-border deployment of anti-drone technologies and creates legal ambiguity for manufacturers and operators. Additionally, technological advancements often outpace legislative updates, resulting in gaps that expose users to liability risks. Commercial players operating in multiple jurisdictions must navigate complex approval processes and certification standards, which increases both compliance costs and market entry barriers.

Proliferation of AI-Enabled Counter-UAV Systems: AI integration is advancing the capabilities of Anti-drone Defense Systems, enabling precise threat identification and response automation. In 2024, over 40% of newly deployed counter-UAV systems featured AI-driven classification tools, which significantly reduced false detection rates in high-traffic zones. These intelligent systems are especially effective in complex environments like airports and stadiums, where distinguishing between benign and malicious drones is critical.

Growth in Directed Energy Weapons Deployment: There has been a notable increase in the deployment of directed energy weapons (DEWs), particularly high-energy lasers, as a non-kinetic drone mitigation method. Defense agencies across North America and the Middle East have accelerated procurement of DEW-equipped systems due to their low cost per engagement and precision capabilities. In recent tests, laser systems successfully neutralized micro-drones at a distance of up to 3 kilometers, marking a pivotal advancement in battlefield drone defense.

Rising Demand for Mobile and Handheld Systems: The need for flexible, field-ready Anti-drone Defense Systems is surging among tactical units and event security teams. Compact, handheld jamming devices and rapidly deployable radar systems are seeing adoption increases of over 30% in urban surveillance applications. This trend supports heightened demand from law enforcement and emergency response units operating in unpredictable environments.

Integration of 3D Geofencing and Advanced Tracking Analytics: 3D geofencing technologies are being adopted to define airspace zones vertically and horizontally, offering a multidimensional layer of protection. These systems are now used in over 25% of new installations at sensitive locations like correctional facilities and power plants. Coupled with advanced tracking analytics, they offer real-time drone path predictions and zone-specific alerts, improving defensive strategy precision.

The Anti-drone Defense System Market is segmented based on type, application, and end-user, each playing a significant role in shaping deployment strategies and innovation directions. Product types vary from detection-only modules to integrated neutralization systems, offering diverse capabilities for different threat scenarios. Application areas span across military defense, critical infrastructure protection, commercial facilities, and public event security. End-user segmentation reflects a wide adoption base, including defense agencies, government bodies, private enterprises, and public safety organizations. While military and defense remain dominant, the fastest-growing segments are within the civilian infrastructure and event security categories, where cost-effective, portable solutions are in demand. These segmentation insights enable tailored product development, targeted investment strategies, and refined go-to-market plans for vendors in the global Anti-drone Defense System Market.

Detection and tracking systems continue to lead the type-based segment of the Anti-drone Defense System Market due to their broad applicability and critical importance in early threat identification. These systems are widely used across defense and civilian installations and have evolved to incorporate radar, acoustic, and RF spectrum analysis tools. The fastest-growing type is integrated detection and neutralization systems, driven by increased demand for all-in-one solutions that offer both identification and response capabilities. Their rising deployment in urban and critical infrastructure sites highlights their expanding operational relevance. Radio frequency jamming units remain a preferred option in conflict zones and border patrols due to their reliability in intercepting communication links. Directed energy weapons and net-based physical capture systems, while niche, are seeing focused adoption in high-security applications, such as embassy protection and military convoys, where precision and reduced collateral impact are vital. Overall, the segment is witnessing a shift toward modular, adaptive, and intelligent system architectures.

The military and defense application segment leads the Anti-drone Defense System Market, given the escalating threat of hostile UAVs in conflict-prone zones and border areas. Defense forces are continuously upgrading counter-drone capabilities as part of broader airspace security modernization efforts. The fastest-growing application area is critical infrastructure protection, including airports, power stations, and water treatment facilities. Increased reports of drone intrusions near such locations have necessitated rapid deployment of surveillance and mitigation systems. Public event security is also emerging as a vital segment due to the rising use of drones for unauthorized media coverage or potential threat delivery. In addition, commercial properties like logistics centers and data hubs are adopting detection systems as part of their security protocols. This diversification in application use cases is propelling innovation in platform design, system portability, and automation to address highly variable operational requirements.

Military agencies remain the primary end-users in the Anti-drone Defense System Market due to their need for high-performance, battlefield-ready systems that can neutralize a wide range of drone threats. These agencies are increasingly incorporating multi-tiered defense strategies that blend kinetic and non-kinetic technologies. The fastest-growing end-user category is law enforcement and homeland security organizations, particularly in urban regions where drone sightings have increased near public institutions and transportation hubs. These users require fast-deployable, cost-efficient systems with minimal training needs. Private sector enterprises, such as airport operators, event management firms, and critical infrastructure operators, are also expanding their use of anti-drone solutions. Correctional facilities, notably in North America and Europe, are turning to advanced RF and radar systems to combat illicit drone-based contraband deliveries. This broad end-user base is shaping the market's demand profile, encouraging providers to offer customizable, scalable, and easy-to-integrate anti-drone systems.

North America accounted for the largest market share at 38.2% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 2.4% between 2025 and 2032.

The North American market has seen widespread integration of Anti-drone Defense Systems across military, critical infrastructure, and law enforcement agencies. Its leadership stems from advanced technological development and aggressive procurement by defense departments. Meanwhile, the Asia-Pacific region, led by China, India, and Japan, is accelerating adoption due to increased surveillance needs and urban security challenges. Rapid digital transformation, geopolitical tensions, and rising domestic defense manufacturing are fueling regional momentum. Europe, South America, and the Middle East & Africa are also expanding Anti-drone deployments, especially in response to growing concerns over airspace violations near sensitive government, commercial, and energy infrastructure. Across regions, the market continues to evolve, shaped by regional security strategies, budget allocations, and technology maturity levels.

Advanced Defense Procurement Driving Tactical Innovation

North America held a commanding 38.2% share of the global Anti-drone Defense System market in 2024. A strong defense and aerospace ecosystem, particularly in the United States and Canada, supports the region’s leadership. Key industries driving demand include military defense, homeland security, and aviation infrastructure. The U.S. Department of Defense continues to allocate significant funding toward advanced C-UAS programs, with increasing focus on AI-powered and mobile systems. New regulations from the FAA also permit more proactive drone mitigation at airports and public events. Technology trends show growing deployment of portable radar and RF jamming systems integrated with cloud-based threat intelligence networks. These innovations are transforming perimeter protection and public security protocols, reinforcing the region’s market dominance.

Smart Surveillance and Sustainability Shaping Airspace Defense

Europe accounted for approximately 27.4% of the global Anti-drone Defense System market in 2024, with Germany, the UK, and France leading in deployment and innovation. The region is leveraging defense modernization programs and strict airspace regulations to curb rising drone threats. Institutions like EASA and EUROCONTROL are actively pushing for harmonized drone traffic management and counter-drone standards. Technological progress is evident through adoption of laser-based interception systems and AI-powered detection networks. Additionally, sustainability initiatives are influencing the market as EU countries push for eco-efficient and energy-conscious security infrastructure. Civil airports, prisons, and national defense installations are driving demand, supporting Europe's continued investment in advanced anti-drone platforms.

Defense Modernization and Urban Security Needs Fueling Growth

The Asia-Pacific region ranks highest in projected growth, holding a strong volume share with rapid adoption in countries like China, India, and Japan. China is heavily investing in anti-drone solutions for both civilian and military use, supporting nationwide infrastructure protection. India’s border security forces have initiated localized development of AI-based counter-drone systems for surveillance along sensitive frontiers. Japan is deploying anti-drone technology in urban centers and for event security, particularly ahead of international gatherings. A robust manufacturing base and ongoing expansion of public safety infrastructure are accelerating adoption. The region also leads in innovation hubs focused on real-time drone detection, integrated with 5G and smart city frameworks.

Emerging Infrastructure Security Needs Creating Market Demand

In South America, Brazil and Argentina are at the forefront of the Anti-drone Defense System market, contributing to a regional share of 6.1% in 2024. Governments across the region are investing in protective technologies to secure energy infrastructure, correctional facilities, and border zones. Brazil has launched pilot programs to deploy counter-UAV systems at ports, oil refineries, and power plants. Argentina’s law enforcement agencies are incorporating portable detection units for stadium and public event surveillance. Infrastructure development and growing awareness of airspace violations are supporting gradual market penetration. With favorable trade policies and defense modernization support, demand for scalable and cost-efficient anti-drone systems is steadily increasing.

Strategic Investments Supporting Advanced Airspace Control

The Middle East & Africa region is witnessing rising adoption of Anti-drone Defense Systems, particularly in UAE, Saudi Arabia, and South Africa. Key drivers include the need to secure oil refineries, large-scale infrastructure, and high-profile events. The region accounted for 7.3% of global market share in 2024. Technological modernization is a priority, with nations investing in AI-integrated counter-UAV platforms capable of long-range detection and neutralization. Governments are also implementing stricter airspace control regulations, backed by defense partnerships with global vendors. Construction expansion, urbanization, and digital surveillance initiatives further boost the need for advanced perimeter and drone threat mitigation technologies.

United States – 34.7% market share

Strong military expenditure, large-scale defense contracts, and aggressive adoption of AI-powered anti-drone systems sustain the U.S. market lead.

China – 16.9% market share

High-volume domestic production and increasing deployment across public and military sectors make China a dominant force in the Anti-drone Defense System market.

The Anti-drone Defense System market is characterized by a dynamic and moderately consolidated competitive environment, with over 90 active vendors globally offering a wide array of detection and mitigation solutions. The competitive landscape includes a mix of established defense contractors, emerging technology firms, and specialized security solution providers. Leading companies are engaged in product differentiation through the integration of AI, machine learning, and modular system design, aiming to enhance accuracy, mobility, and real-time response capabilities.

Strategic collaborations have become central to market advancement, with several key players forming joint ventures with government agencies and private infrastructure operators to co-develop tailored counter-drone solutions. Notable trends include the launch of handheld jamming devices, autonomous tracking radars, and portable directed energy systems, all aimed at improving mobility and operational range. Mergers and acquisitions are also shaping competition, enabling firms to combine hardware expertise with advanced analytics platforms. The rise in drone swarm threats has encouraged R&D efforts focused on multi-layered response mechanisms, further intensifying the innovation race. Market players are additionally investing in global expansion strategies, particularly in Asia-Pacific and the Middle East, to address the growing regional demand for scalable airspace security technologies.

Dedrone GmbH

Rafael Advanced Defense Systems

Liteye Systems, Inc.

Thales Group

Leonardo S.p.A.

DroneShield Ltd.

Saab AB

Raytheon Technologies Corporation

Blighter Surveillance Systems Ltd.

Fortem Technologies Inc.

The Anti-drone Defense System market is undergoing rapid technological transformation, with new innovations redefining detection, identification, and neutralization capabilities. Among the most influential technologies are AI-driven threat recognition systems that enhance situational awareness by processing vast datasets from radar, RF sensors, and electro-optical devices. These systems employ machine learning algorithms to classify drones based on flight patterns, size, and signal characteristics, improving response accuracy and minimizing false alarms.

RF detection and jamming technologies remain widely adopted due to their non-lethal, scalable applications in both civilian and military settings. In 2024, over 60% of newly deployed systems incorporated RF-based modules, reflecting their cost-effectiveness and ease of deployment. Meanwhile, directed energy weapons (DEWs), including high-powered microwave and laser-based systems, are becoming increasingly viable for high-security sites due to their precision, silent operation, and ability to disable drones without physical projectiles.

3D geofencing and GPS spoofing tools have also gained traction, enabling security teams to define protected airspace zones and reroute or trap drones without causing collateral damage. These tools are supported by real-time command and control (C2) systems that integrate seamlessly into broader security networks. Additional advancements include portable counter-drone kits, wearable early warning devices, and cloud-based AI platforms for remote monitoring. Together, these innovations are equipping governments, industries, and commercial users with highly adaptive and modular anti-drone defense solutions tailored to specific threat environments.

• In March 2023, DroneShield introduced a new firmware upgrade for its DroneSentry-C2 platform, integrating enhanced AI algorithms that improved drone identification accuracy by 45% and extended multi-sensor integration capabilities for security-critical infrastructure.

• In October 2023, the Indian Air Force deployed an indigenous anti-drone system at key border locations, featuring portable jamming and radar modules capable of neutralizing drones up to 5 kilometers away in under 30 seconds from detection.

• In January 2024, Raytheon demonstrated a mobile, laser-based anti-drone weapon in field tests, successfully engaging multiple UAV targets simultaneously with a 100% kill rate across a 2.5 km radius, reflecting strong advancement in directed energy technologies.

• In May 2024, Leonardo launched a next-gen counter-UAV platform with embedded machine learning that dynamically adjusts jamming frequencies in real time, reducing collateral signal disruption and increasing response speed by 30% compared to prior models.

The Anti-drone Defense System Market Report comprehensively examines the global landscape of counter-UAV technologies and solutions, offering deep insights into key product types such as detection systems, mitigation devices, and integrated platforms. The report analyzes segmentation by type (e.g., RF jamming, radar, laser-based), application (military, infrastructure security, commercial facilities, public events), and end-users (defense, government agencies, private sector, law enforcement). It provides granular details on how various technologies are utilized in different operational contexts.

Geographically, the report spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, outlining region-specific trends, demand drivers, procurement initiatives, and technology adoption patterns. Emerging nations with evolving defense needs and expanding urban infrastructure are examined for their growing roles in shaping the market’s future.

The scope also includes insights into innovation trends such as AI-powered surveillance, portable drone jamming kits, autonomous C2 platforms, 3D geofencing, and hybrid kinetic-non-kinetic systems. Regulatory frameworks impacting system deployment, cross-border compliance issues, and investment trends in R&D are covered to provide a well-rounded view. Additionally, the report highlights niche segments such as event-based mobile deployments and corrections facility drone mitigation, offering decision-makers a forward-looking, data-driven understanding of strategic growth opportunities across the evolving anti-drone ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 16685.02 Million |

|

Market Revenue in 2032 |

USD 19244.6 Million |

|

CAGR (2025 - 2032) |

1.8% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Symantec (Broadcom Inc.), Forcepoint, Digital Guardian, McAfee, Trend Micro, GTB Technologies, Cisco Systems, Inc., Zscaler, Code42, Proofpoint, Inc., Trellix, Spirion, Safetica, Fidelis Cybersecurity, Netskope |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |