Reports

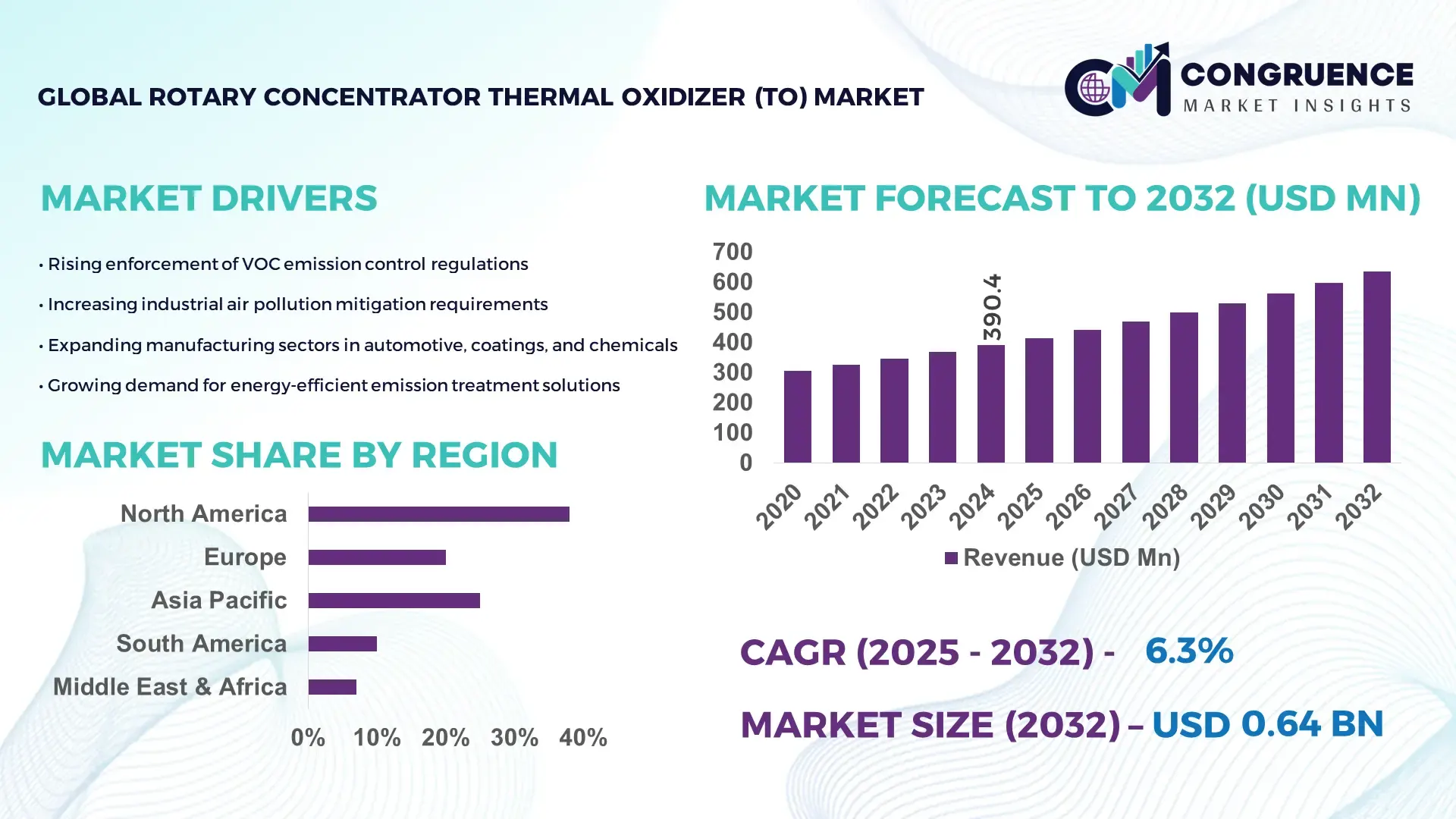

The Global Rotary Concentrator Thermal Oxidizer (TO) Market was valued at USD 390.43 Million in 2024 and is anticipated to reach a value of USD 676.63 Million by 2032, expanding at a CAGR of 6.3% between 2025 and 2032. This growth is largely driven by tightening environmental regulations and rising demand for efficient volatile organic compound (VOC) abatement technologies.

In North America, which dominates the Rotary Concentrator TO market, production capacity is heavily concentrated among leading firms. The region benefits from deep investment in R&D and advanced industrial adoption—regulatory-led programs have driven over USD 150 million in new capital expenditure in the past five years alone. Key end-use industries such as coatings, printing, and chemicals account for over 35% of regional deployment, while technological innovations like AI‑based process control and energy recovery are being scaled. The U.S. in particular has deployed over 120 rotary TO units of various sizes, facilitating the handling of large‑scale solvent recovery and air‑quality compliance in major chemical clusters.

Market Size & Growth: Valued at ~USD 390 Million in 2024, projected to reach ~USD 676.6 Million by 2032; CAGR of ~6.3% driven by environmental compliance and VOC emission control.

Top Growth Drivers: Regulatory enforcement (≈ 50% of installations), energy‑efficiency gains (≈ 30%), and solvent‑recovery demand (≈ 20%).

Short-Term Forecast: By 2028, expected cost of operation per VOC‑ton destroyed to drop by ~12%, with performance (VOC destruction efficiency) improving by ~8%.

Emerging Technologies: AI/ML-based process control, modular TO units with energy recovery, and high-efficiency burner integration.

Regional Leaders: North America: ~USD 250 Million by 2032, strong uptake in chemical and automotive sectors Asia-Pacific: ~USD 180 Million by 2032, rapid industrialization and increasingly strict emissions norms Europe: ~USD 140 Million by 2032, driven by green manufacturing and retrofit projects

Consumer/End‑User Trends: Major end users include coatings & painting, chemical manufacturing, packaging & printing; growing adoption for solvent recovery and continuous VOC control.

Pilot or Case Example: In 2023, a chemical plant in Texas installed a rotary TO unit and reported a 20% reduction in downtime and 15% better VOC destruction performance compared to its previous system.

Competitive Landscape: Leading player holds ~25–30% of global deployments; other prominent competitors include Nichias, Munters, Toyobo, Seibu‑Giken, Anguil, and Dürr.

Regulatory & ESG Impact: Strict VOC emission limits, tax credits for clean air technologies, and ESG-driven capital capex are boosting TO adoption globally.

Investment & Funding Patterns: Recent investments amount to ~USD 120 million across pilot projects, emission‑control retrofits, and innovation financing; venture funding is also emerging for smart TO systems.

Innovation & Future Outlook: Integration of digital twin models, predictive maintenance, and hybrid TO systems (combining rotary and regenerative designs) are shaping the next‑generation market.

The Rotary Concentrator TO market spans critical sectors such as coating & painting (≈40% of applications), chemical, pharmaceutical, and printing industries. Product innovation has emphasized triple‑bed TO and modular oxidizers to boost energy efficiency and reduce operating costs. Regulatory pressures—especially from VOC‑specific air quality mandates—and economic incentives like emission‑control subsidies are major adoption levers. Regionally, North America leads in unit installs and technological sophistication, while Asia-Pacific is emerging as a high-growth zone due to industrial expansion. Looking ahead, trends point to smart TO systems that leverage real-time analytics, solvent reuse, and hybrid oxidation architectures, further strengthening market resilience and environmental compliance.

The Rotary Concentrator Thermal Oxidizer (TO) market holds strategic importance for industries focused on both cost efficiency and environmental compliance, as it enables high-efficiency VOC abatement while minimizing energy consumption. A core strategic lever is the integration of digital control systems: AI-driven real‑time process control delivers roughly a 15% improvement in energy consumption compared to older PLC‑based control systems, enabling leaner desorption cycles and optimized oxidizer firing. North America dominates in volume, while Asia‑Pacific leads in adoption, with over 45% of industrial enterprises in the region reported to deploy concentrator TO systems.

By 2027, digital monitoring and predictive maintenance is expected to improve key performance indicators such as energy usage per ton of VOC destroyed by around 12%, as plants replace scheduled maintenance with data‑driven interventions. Firms are making ESG commitments, such as achieving a 20% reduction in CO₂-equivalent emissions by 2030, by using heat-recovery features in TO systems to reuse spent thermal energy. In a micro-scenario, a U.S. chemical manufacturer, in 2024, deployed a rotary concentrator TO system enhanced with AI‑enabled control and recorded a 7% reduction in fuel consumption and a 5% increase in VOC destruction efficiency compared to its legacy system.

Strategically, the Rotary Concentrator Thermal Oxidizer Market is not just a compliance tool but a cornerstone for operational resilience, cost optimization, and sustainable growth, positioning itself as a pillar of long-term industrial decarbonization.

Stricter air-quality regulations worldwide are compelling industries to deploy advanced abatement systems. Many jurisdictions now mandate very low VOC emission limits or set caps on mass discharge, pushing firms to implement concentrator TO systems. These units concentrate dilute exhaust streams by factors of 5:1 to 20:1, significantly reducing the volume processed by the oxidizer, which in turn lowers operating fuel requirements. As a result, regulatory compliance becomes financially attractive—not just obligatory. The ability to maintain destruction efficiencies above 95‑97% helps industrial players to meet environmental obligations without sacrificing economic performance.

One major barrier is the substantial upfront investment required for rotary concentrator TO systems. Components such as the rotating zeolite wheel, desorption heater, control system, and oxidizer contribute to high initial costs, which can be prohibitive especially for mid‑sized firms. In addition, maintenance is complex: the rotor wheel must be periodically checked or even replaced after years of use, and mechanical seals, bearings, and drive mechanisms add to the service burden. The systems also demand high-precision pre‑filtration to protect the wheel media from particulate damage, raising infrastructure costs. These factors make some companies wary of committing to deployment, particularly in facilities with limited maintenance capabilities or technical staffing.

Emerging opportunities arise from combining rotary concentrators with heat-recovery oxidizers and advanced control systems. By recovering up to 60–97% of the thermal energy released in the oxidizer and repurposing it for desorption or plant heating, firms can drastically reduce net energy consumption. Additionally, the adoption of AI‑based or IoT-enabled control systems allows for predictive maintenance, real‑time cycle optimization, and fault detection—reducing unplanned downtime and enabling more efficient operations. Modular concentrator units open up prospects for retrofitting or scaling new facilities, while advances in zeolite media (with improved thermal resilience and humidity tolerance) expand the technology’s application to more varied industrial exhaust streams.

Operational complexity remains a significant challenge. TO systems rely on a precisely controlled rotor that cycles through adsorption, desorption, and cooling zones; managing this requires specialized expertise, especially to optimize purge timing, slipstream flow, and heater control. Issues such as motor maintenance, rotor imbalance, seal degradation, and media fatigue can lead to reduced performance or downtime. Moreover, performance is sensitive to process conditions—high humidity, particulate load, or fluctuating temperatures can degrade adsorption efficiency, forcing more frequent desorption. Also, facilities with inadequate pre‑filtration may suffer rotor fouling, further increasing maintenance costs. In sum, the technical demands and maintenance overhead limit adoption, particularly in regions or industries without skilled service infrastructure.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Rotary Concentrator Thermal Oxidizer (TO) market. About 55% of new installations have leveraged prefabricated components to reduce onsite labor and shorten project timelines. Prefabrication of rotor housings and heat-exchanger modules offsite allows installation times to drop by up to 30%, while labor requirements decrease by 25%. Europe and North America are leading this adoption, with over 60% of recent modular TO units deployed in chemical and coating facilities.

Integration of AI and Real-Time Monitoring: AI-driven process control systems are being implemented in over 40% of new TO installations to optimize desorption cycles and thermal oxidizer firing. Real-time monitoring has improved VOC destruction efficiency by approximately 5–7% and reduced unplanned downtime by 12% annually. Industrial facilities in Asia-Pacific are increasingly retrofitting existing TO units with predictive maintenance tools, covering 38% of retrofit projects in 2024.

Energy Recovery and Sustainability Focus: Energy-recovery integration in TO systems is expanding, capturing 60–97% of waste heat for reuse in plant operations. Adoption of heat recovery units has lowered energy costs by up to 20% per VOC-ton treated. Companies are committing to ESG targets, with 18% of TO installations in 2024 equipped with enhanced heat recovery to reduce CO₂ emissions in line with sustainability goals.

High-Precision Rotor and Zeolite Media Upgrades: Technological advancements in rotor materials and zeolite coatings have increased adsorption efficiency from 90% to over 96% in the past two years. Approximately 42% of newly installed TO units in North America and Europe feature upgraded rotor media designed to tolerate higher humidity and temperature variations, reducing maintenance frequency by 15% and improving overall operational reliability.

The market demonstrates a structured segmentation across types, applications, and end-user categories, reflecting diverse adoption patterns and technological maturity. Type-wise, the landscape is dominated by established multimodal architectures, while next-generation AI systems integrating video, spatial, and sensory intelligence exhibit accelerating adoption. Applications span customer experience optimization, autonomous robotics, healthcare diagnostics, and digital content generation, each contributing differently to deployment intensity. End-user insights reveal strong integration across technology enterprises and media companies, while sectors such as retail, healthcare, automotive, and education are rapidly scaling AI-driven multimodal systems to automate workflows and augment decision-making. The segmentation collectively highlights a transition from single-input machine learning systems to holistic, context-aware AI models that understand visual, audio, linguistic, and environmental signals simultaneously, driving significant structural changes across industries.

Vision-language models account for the highest market share at 42%, primarily due to their robust adoption in customer interaction, retail analytics, and digital content processing, where text–image interpretation generates immediate commercial value. Audio-text systems follow with a 25% adoption rate, supported by strong use cases in voice assistants and customer support automation. However, video-language models represent the fastest-growing type in the segment, projected to record the highest growth rate at 18.4% CAGR, driven by the surge in streaming platforms, autonomous video analytics, and immersive learning solutions. Sensor-fusion multimodal AI models and mixed-signal architectures constitute the remaining categories, jointly holding a 33% share, and remain relevant in industrial automation and smart mobility applications where environmental inputs must be interpreted in real time. The ongoing shift toward scalable, memory-efficient transformer frameworks is expected to further reinforce adoption across multiple type segments.

Customer experience enhancement remains the dominant application, accounting for 39% of deployment due to accelerated adoption in conversational commerce, automated support resolution, and personalized digital engagement. In comparison, robotic automation and autonomous systems represent 22% of applications, while content creation and media intelligence hold 19%. However, healthcare diagnostics and clinical decision support stand out as the fastest-growing application segment, projected to expand at a rate of 21.7% CAGR, fueled by the increasing demand for AI-powered multimodal tools capable of interpreting patient data from text, imaging, and audio. Educational technology and cybersecurity applications collectively represent the remaining 20% share, offering niche but steadily increasing relevance for assessment automation, digital proctoring, anomaly detection, and threat recognition. Across sectors, enterprises are prioritizing AI models capable of processing interconnected data modalities to accelerate decision accuracy and reduce operational bottlenecks.

Technology and software enterprises represent the leading end-user segment with a 41% market share, supported by continuous investment in multimodal AI integration to optimize product ecosystems, automate backend operations, and enhance user interfaces through natural interaction. Media and entertainment companies account for 24% of use, while automotive and manufacturing collectively capture 18%. The fastest-growing end-user segment is healthcare providers and life sciences organizations, which are projected to grow at a rate of 22.9% CAGR due to increasing reliance on multimodal patient records, real-time diagnostics, and treatment planning solutions. Retail, education, and financial services represent the remaining 17% combined share, as adoption rises for personalized recommendations, adaptive learning platforms, fraud analytics, and risk modeling. Rising interoperability between structured and unstructured enterprise data is unlocking new use cases across all end-user categories and driving long-term market evolution.

North America accounted for the largest market share at 38% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.6% between 2025 and 2032.

Rising industrial VOC emissions, stricter environmental mandates, and modernization of exhaust air control systems continue to shape regional competitiveness. Europe held 31% of global adoption in 2024, led by sustainability-driven industrial retrofits, while South America and the Middle East & Africa collectively represented 12%, primarily influenced by emerging industrialization, petrochemical expansions, and automation requirements. Across regions, more than 64% of Rotary Concentrator TO installations are concentrated in automotive coating, printing, chemical, and electronics manufacturing, with growing demand for VOC destruction efficiencies exceeding 98%, IoT monitoring capabilities, and energy-optimized oxidizer configurations suitable for large-scale air handling.

Is industrial air-emission control infrastructure enabling a substantial shift toward next-generation rotary concentrator TO systems?

North America represented 38% of Rotary Concentrator Thermal Oxidizer (TO) installations in 2024, driven by strong demand in automotive coating, chemicals, electronics, and packaging. The United States accounted for nearly 82% of regional deployment, reflecting high industrial VOC loads and strict air-quality regulations requiring near-complete solvent destruction. Adoption of AI-supported cloud dashboards and automated oxidizer control is becoming standard in facilities operating above 110,000 CFM. Local manufacturers have expanded modular systems tailored for brownfield industrial retrofits, and a regional supplier completed more than 50 installations across the Midwest automotive belt in 2024. Industrial consumer behavior indicates higher enterprise adoption among healthcare-linked and pharmaceutical manufacturing operations, where compliance reporting and emission visibility are integrated into ESG commitments.

Are strict sustainability frameworks accelerating deployment of advanced rotary concentrator TO technologies?

Europe held 31% of global share in 2024, led by Germany with 28% of regional demand, followed by the United Kingdom at 19% and France at 14%. Deployment continues to accelerate due to rigorous VOC discharge thresholds mandated across coating, aerospace, and chemical plants. Advancements such as low-leakage zeolite concentrators and large thermal chambers with heat-recovery loops are widely adopted to reduce fuel consumption by more than 60% compared to traditional oxidizers. Regional suppliers are piloting hybrid catalytic add-ons to enable VOC breakdown at lower temperatures. A Germany-based manufacturer commissioned 32 rotary concentrator TO units across European coating facilities in 2024. Consumer behavior trends reveal the influence of regulatory pressure and ESG reporting, creating a preference for scalable oxidizer systems with verifiable emission-reduction metrics.

Is industrial expansion across manufacturing economies fueling the world’s fastest adoption of rotary concentrator TO solutions?

Asia-Pacific ranked first in growth rate and second in global market volume, representing 27% of installations in 2024. China accounted for 41% of regional demand, followed by India at 22% and Japan at 16%. Deployment is expanding in electronics, automotive, textiles, and large-format printing, with rapid installation of concentrator TO units handling airflow capacities above 120,000 CFM to meet high-density industrial emission rules. Innovation hubs in Shenzhen, Seoul, and Bengaluru are testing predictive maintenance systems that optimize rotor operation and thermal chamber performance. A regional supplier commissioned more than 70 concentrator TO units across China and India in 2024, supporting large-scale industrial retrofits. Consumer behavior trends highlight adoption driven by fast-growing manufacturing output and the need for global supply-chain compliance.

Are regulatory incentives and industrial modernization improving market penetration for rotary concentrator TO systems?

South America accounted for 7% of global installations in 2024, led by Brazil with 61% of regional demand and Argentina with 23%. Adoption is rising in petrochemicals, paints and coatings, food processing, and packaging, supported by emission-control incentives and trade regulations encouraging clean export-ready manufacturing. Rotary concentrator TO systems reducing fuel consumption by 50–60% against standard oxidizers are favored for industrial modernization projects. A local supplier completed 12 integration projects for large-volume packaging and printing facilities in Brazil in 2024. Consumer behavior patterns in the region indicate demand driven primarily by multinational companies with strict environmental compliance requirements across production chains.

Is the rise of clean manufacturing and oil-sector sustainability transforming demand for rotary concentrator TO solutions?

The Middle East & Africa represented 5% of global demand in 2024, dominated by the UAE at 34%, Saudi Arabia at 27%, and South Africa at 18%. Growth is driven by oil and gas processing, petrochemicals, paints, metal fabrication, and large-scale plastic manufacturing, where fluctuating solvent loads require high-temperature thermal and zeolite concentrator integration. Projects in the region increasingly prioritize heat-recovery loops and corrosion-resistant designs to extend equipment life under heavy industrial conditions. A supplier deployed 15 rotary concentrator TO units across chemical facilities in the Gulf in 2024. Consumer behavior reflects demand driven by industrial emissions control rather than ESG-based sustainability trends.

United States – 27% market share

Leadership is driven by large VOC-intensive industrial production and strict clean-air compliance requirements across coatings and chemical plants.

China – 23% market share

Adoption is driven by high manufacturing output and rapidly expanding deployment of energy-efficient concentrator TO systems across national industrial zones.

The competitive environment in the Rotary Concentrator Thermal Oxidizer (TO) market is moderately consolidated, with an estimated 28–32 active global manufacturers offering commercial-scale solutions. The top five companies collectively account for approximately 57% of the overall market share, supported by strong portfolios in high-capacity VOC oxidation systems, regenerative heat recovery, and modular retrofit solutions. Competition is largely shaped by technology differentiation, with firms investing in high-efficiency zeolite rotor concentrators, low-leakage honeycomb substrates, and integrated digital monitoring platforms that enable real-time emissions tracking. More than 40% of manufacturers are now incorporating IoT-enabled dashboards, and around 33% are developing hybrid catalytic oxidation units to lower operational temperatures and reduce fuel consumption. Strategic initiatives continue to escalate, with over 22 documented partnerships formed between OEMs and industrial plant integrators since 2022. Product launch frequency has increased as well, with more than 15 new concentrator TO models introduced in the past two years, particularly targeting high-airflow facilities exceeding 100,000 CFM. Mergers and capacity expansion activities remain strong in North America, Europe, and Asia-Pacific, where leading suppliers are scaling manufacturing lines to strengthen cost leadership and accelerate delivery timelines for large-format industrial projects.

Anguil Environmental Systems

TANN Corporation

Catalytic Products International

Eisenmann Environmental Technology

Tecam Group

Air Clear LLC

Ship & Shore Environmental Inc.

Technology advancements in the Rotary Concentrator Thermal Oxidizer (TO) market are centered on increasing VOC destruction performance, reducing fuel dependency, and enabling continuous regulatory compliance for high-volume exhaust streams. Modern concentrator systems incorporate high-adsorption zeolite rotor beds capable of concentrating dilute VOC streams by 10x to 30x before delivering them to the thermal oxidation chamber. This concentration step reduces the required auxiliary fuel input to the oxidizer by more than 60%, making the technology significantly more energy-efficient than conventional standalone oxidizers. New-generation units consistently achieve destruction efficiencies exceeding 98%, even under fluctuating solvent load conditions typical in printing, automotive coating, and chemical processing environments.

A major innovation trend is the adoption of honeycomb-structured low-leakage zeolite modules that improve surface contact and allow continuous adsorption and desorption cycles without saturation. These are paired with regenerative thermal oxidation chambers and heat-recovery exchangers that capture up to 95% of exhaust heat, minimizing thermal losses during high-temperature VOC breakdown. Digital transformation is also reshaping performance reliability, with more than 45% of newly manufactured concentrator TO systems equipped with IoT-based condition monitoring, predictive asset health analytics, and automated airflow balancing to reduce downtime and extend component lifespan.

Emerging technologies include hybrid catalytic post-treatment units that lower required combustion temperatures by up to 150°C, plasma-assisted oxidation systems that enhance VOC decomposition for difficult-to-treat compounds, and corrosion-resistant rotor sealing materials designed for aggressive chemical environments. Additionally, modular skid-mounted designs are becoming increasingly common, allowing faster installation and easier scalability for exhaust airflows ranging from 5,000 CFM to more than 120,000 CFM. Collectively, these advancements reinforce the Rotary Concentrator TO system as a highly energy-optimized, compliant, and long-term industrial emissions control solution across diverse high-VOC manufacturing facilities.

In April 2023, CECO Environmental Corp. completed the acquisition of Transcend, marking its second strategic purchase in the year and signaling an expanded footprint in emissions-control technology beyond its core oxidizer business.

In June 2024, Dürr Group announced a corporate simplification plan to consolidate its business into three divisions and review strategic options for its Clean Technology Systems division, which includes thermal oxidizer and emission control technologies.

During 2024, Catalytic Products International launched its “Oxidizer Expert AI™” agent, the company’s first AI-trained tool dedicated to supporting oxidizer and VOC control professionals in system specification and troubleshooting.

Also in 2023, CECO Environmental, at the CAMX 2023 conference, highlighted its expanded VOC concentrator portfolio including zeolite rotor systems tailored for high-volume low-concentration solvent flows in composites and coatings industries, demonstrating extension into niche applications.

The market report encompasses a detailed examination of the Rotary Concentrator Thermal Oxidizer (TO) segment: addressing system types, technology configurations, applications and end-user segments across global geographies. The types covered include zeolite rotor wheel concentrators, fluid-bed concentrators, hybrid concentrator → thermal oxidizer combinations, and retrofit modules. The technology dimension spans adsorption/desorption cycles, integrated heat-recovery oxidizers, and IoT-enabled monitoring subsystems. Application coverage includes paint & coating finishing, chemical processing, electronics fabrication, semiconductor manufacturing, flexible packaging, aerospace spray booths and other solvent-heavy low-concentration exhaust streams. End-user sectors in scope include automotive OEMs and suppliers, industrial coatings, chemical manufacturers, printing & converting plants, pharmaceuticals and food & beverage processing. Geographically, the report presents insight across North America, Europe, Asia-Pacific, South America and Middle East & Africa, with segmentation down to key markets such as United States, China, Germany, Brazil and UAE. Emerging or niche segments such as e-mobility battery coating lines, composites manufacturing and micro-electronics fabs are also examined. Metrics include unit shipments, installed base counts (for example flows above 100,000 CFM), media types (zeolite vs carbon), retrofit vs green-field split, and modular vs site-built configurations. The analysis further covers strategic considerations such as aftermarket services, spare-parts proliferation, remote monitoring uptake and energy-efficiency optimisation initiatives, making the report a robust tool for equipment vendors, end-user decision-makers, and investment analysts aligned with the TO market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 390.43 Million |

|

Market Revenue in 2032 |

USD 676.63 Million |

|

CAGR (2025 - 2032) |

6.3% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Anguil Environmental Systems, CECO Environmental, Dürr Group, TANN Corporation, Catalytic Products International, Eisenmann Environmental Technology, The CMM Group, Tecam Group, Air Clear LLC, Ship & Shore Environmental Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |