Reports

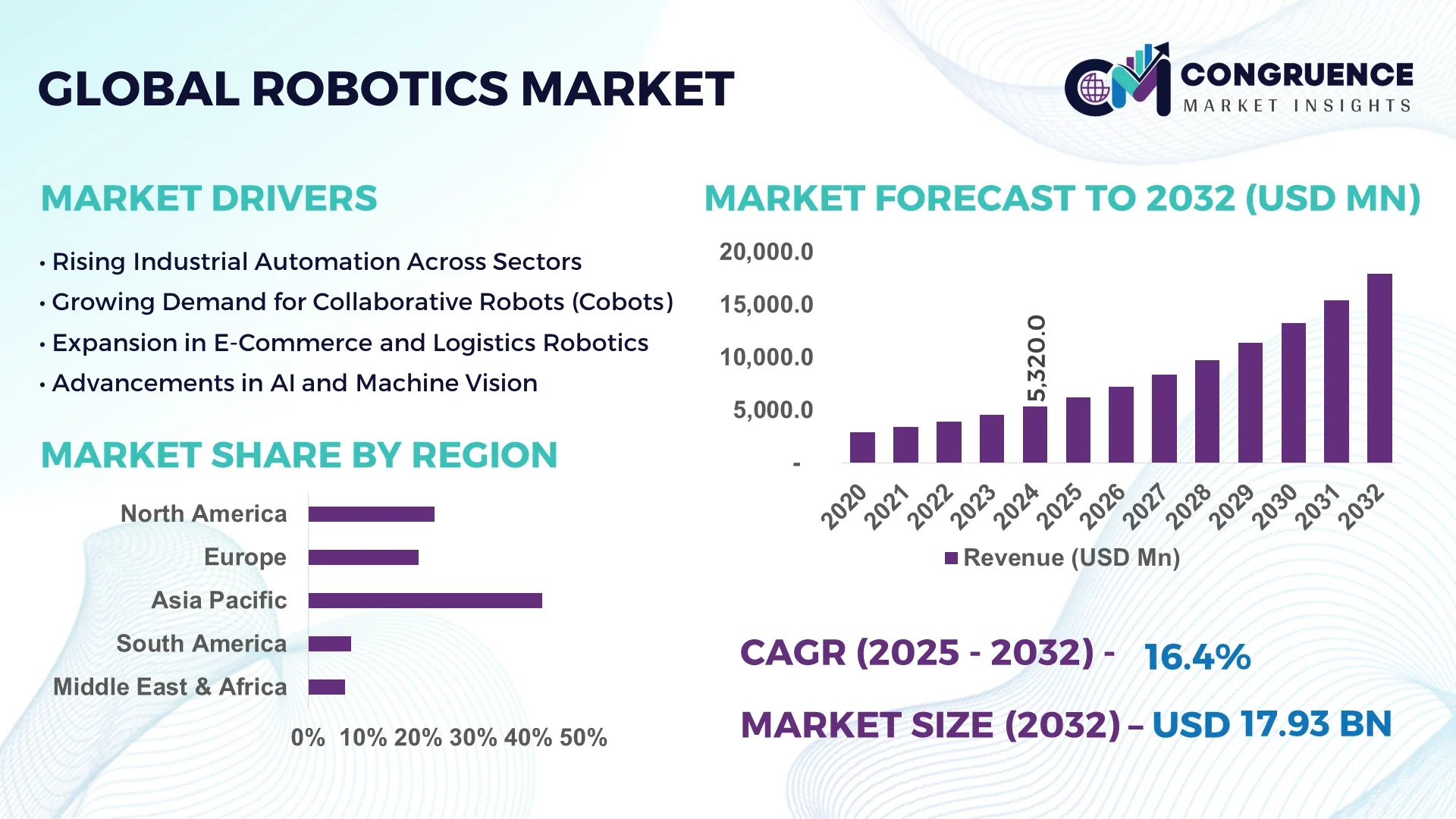

The Global Robotics Market was valued at USD 5,320.0 Million in 2024 and is anticipated to reach a value of USD 17,866.6 Million by 2032 expanding at a CAGR of 16.35% between 2025 and 2032.

China leads global production capacity with nearly 1.8 million industrial robots operational in its factories by the end of 2023. The country installed 276,288 robots in 2023, with domestic manufacturers supplying approximately 47% of these units. Its high-capacity facilities serve key sectors such as electrical/electronics, automotive, and metal/machinery. Massive public and private investments support continuous deployment in logistics, assembly, and precision automation, backed by advances in humanoid robotics and affordable, locally produced models with strong technical integration.

Beyond raw market value, the Robotics Market spans diverse industry verticals including manufacturing automation, logistics, healthcare, pharmaceuticals, food & beverage, and consumer electronics. In industrial robotics, articulated robots dominate applications such as welding, painting, and material handling, while SCARA and Cartesian robots serve high-precision assembly lines. The automotive sector accounts for the largest share, followed by electrical/electronics, pharmaceuticals, and food & beverage. Recent innovations include modular robotic arms with adaptive end-effectors, AI-enabled inspection systems, and cobots with advanced safety sensors for human-robot collaboration. Regulatory and economic drivers include Industry 4.0 mandates, automation incentives in manufacturing hubs, and emissions standards that demand precision production. Environmental directives are prompting use of energy-efficient robots and recyclable materials. Regional consumption is strongest in Asia-Pacific manufacturing zones, with growth also emerging in nearshore regions in Europe and North America. Key future trends include robotics-as-a-service uptake, edge-AI integration, flexible production lines, and deployment of mobile warehousing robots in logistics centers.

AI is fundamentally transforming the Robotics Market by enabling systems to sense, learn, optimize operations, and adapt in real time. In manufacturing, AI-powered robots are improving production efficiency, reducing defect rates by up to 25 percent through advanced vision systems and predictive maintenance protocols. Robotics Market systems are now equipped with machine learning modules that analyze process data and dynamically adjust robotic motion paths, lowering cycle times by 15 percent in assembly and packaging lines. In logistics, AI-driven robots optimize warehouse traversal and routing, increasing throughput by 20 percent while minimizing idle time. Service robots in healthcare combine AI-based image recognition with robotics to perform repetitive tasks, freeing human staff and cutting operational delays; one hospital deployment showed a 30 percent reduction in turnaround for specimen delivery.

The Robotics Market is also witnessing AI-enabled demand prediction tools integrated into robotic production systems, allowing factories to better coordinate manufacturing schedules and minimize inventory waste. This integration has enabled just-in-time deployments and optimized resource allocation across heterogeneous fleets of robots. Customer-facing service robots now use natural language processing, dialogue-generation modules, and adaptive behavioral AI to enhance user interaction in retail and hospitality. AI-driven energy management within robotic cells is reducing energy usage per operational hour by up to 18 percent, aligning with sustainability benchmarks. In sum, the Robotics Market is transitioning from preprogrammed automation toward intelligent, adaptive systems underpinned by AI, driving gains in productivity, reliability, and flexibility while unlocking new applications across sectors.

“In 2025, a major automotive plant integrated vision-based AI into six robotic welding cells, reducing weld rework by 22% over six months while increasing output by 8 percent.”

The overall market dynamics specific to the keyword Robotics Market emphasize shifts toward intelligence-driven automation, modular deployments, and flexible scaling aligned to industrial needs. Demand momentum is driven by digital transformation strategies across manufacturing, logistics, healthcare, and retail sectors. Enterprises are shifting away from rigid, single-function robots toward multi-purpose, AI-enabled platforms. Supply chains are responding by creating locally adaptable manufacturing ecosystems, while regulatory frameworks and energy standards are influencing design requirements. Competition is intensifying as established robotics manufacturers face new entrants offering turnkey cobots and autonomous mobile platforms. The Robotics Market also reflects increasing interest in service-oriented models and subscription-based deployment. Decision-makers are prioritizing ROI through operational efficiency, predictive maintenance, and reduced labor dependency, shaping procurement strategies and long-term capital planning.

Demand for robotic automation in the automotive and electronics industries significantly boosts the Robotics Market. In Asia-Pacific, automotive production rose over 10 percent in 2023, generating high demand for material handling, welding, and painting robots. In China and Japan, robotics installations continue at record pace, with the electrical/electronics sector being a primary user. Robots increase throughput while improving quality control in high-mix, low-volume environments. Investments in smart manufacturing initiatives further accelerate robot deployment across assembly lines, resulting in consistent demand for advanced robotics solutions.

Global supply chain issues and tariffs are restraining Robotics Market growth. Robotics systems depend on critical components such as actuators, sensors, and rare-earth magnets, often sourced from limited suppliers. Tariff regimes—especially goods imported from China—have introduced uncertainty, delaying buyer decisions and reducing capital investments in robotic upgrades. Manufacturers report shipment delays of key components by several weeks, disrupting integration schedules. This supply-side friction limits the pace at which new robotic systems can be commissioned and integrated into existing production lines.

Adoption of RaaS models presents a major opportunity in the Robotics Market. Enterprises can deploy robotics solutions without large upfront capital investment, instead paying monthly subscription fees for installation, maintenance, and upgrades. This model is particularly compelling for mid-sized manufacturers and logistics providers. RaaS enables rapid scaling—robot fleets are quickly leased to meet seasonal demands in e-commerce—and supports flexible configuration across multiple sites. Early adopters report a 30 percent faster implementation timeline compared to traditional procurement.

The Robotics Market continues to face challenges associated with the high cost of deployment and customization. Tailoring robotic systems to specific production environments—especially for bespoke automation tasks—requires specialized engineering and integration services. Costs for high-precision end-effectors, safety-certified enclosures, and AI-augmented sensing modules can escalate by up to 40 percent above standard unit prices. These high initial costs and integration risks often act as barriers for small and medium-sized enterprises evaluating automation investments.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Robotics Market. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Growth of Cobots in Manufacturing Environments: Collaborative robots are increasingly integrated into mixed human-robot workcells. Cobots with enhanced force sensing and AI-based vision allow precise assembly tasks alongside human operators. Adoption in automotive and electronics plants rose sharply in 2024, with reported double-digit increases in deployment across mid-tier manufacturers.

Surge in Mobile Robots for Logistics Automation: Autonomous mobile robots (AMRs) are seeing accelerating uptake in warehouses and fulfillment centers. Logistics hubs now deploy fleets of AMRs to automate picking and sorting, improving order fulfillment up to 25 percent faster than traditional conveyor systems. Regions in North America and Asia-Pacific lead this transformation.

Integration of Edge AI and Real-Time Analytics: Robotics Market systems are incorporating edge-based AI analytics modules to collect sensor data in real time and execute control decisions locally. This trend enables predictive maintenance, environment-aware navigation, and adaptive motion control. Real-time feedback loops reduce downtime by over 15 percent and improve utilization rates in production and logistics applications.

The Robotics Market is broadly segmented based on type, application, and end-user, reflecting the multifaceted nature of robotic integration across global industries. The segmentation helps stakeholders understand distinct growth drivers and operational challenges specific to each category. In terms of types, the market comprises articulated robots, SCARA robots, delta robots, cartesian robots, and collaborative robots (cobots), each offering varying degrees of flexibility, precision, and payload capacity. Applications are spread across material handling, welding, assembly, painting, inspection, and packaging, with emerging uses in service and medical robotics. End-users include automotive, electrical & electronics, healthcare, logistics, food & beverage, aerospace, and other industrial sectors. Understanding these segmentations allows manufacturers and solution providers to align product development with sector-specific requirements and investment trends. This segmentation also reflects regional technology maturity, workforce dynamics, and automation objectives across economies transitioning toward Industry 4.0 practices.

The Robotics Market encompasses several distinct robot types, each tailored to specific operational tasks and industry needs. Articulated robots hold the leading position due to their wide adoption in automotive and general manufacturing sectors. Their multi-joint configuration offers excellent versatility for welding, material handling, and assembly, making them a default choice in environments demanding high flexibility and precision. Collaborative robots (cobots) represent the fastest-growing type, driven by their ability to work safely alongside human operators without requiring extensive safety enclosures. Their ease of deployment, compact size, and suitability for small and medium-sized enterprises are further accelerating adoption in light manufacturing and electronics assembly.

SCARA robots remain essential in high-speed, high-precision assembly operations, particularly in electronics and semiconductor sectors. Delta robots, known for their speed and agility, are gaining traction in the food and beverage industry for sorting and packaging tasks. Cartesian robots, while less flexible, serve niche applications requiring linear movement and heavy payload handling. The diversity of robot types allows organizations to choose optimal solutions based on operational needs, scalability, and integration feasibility.

The leading application within the Robotics Market is material handling, owing to its widespread use across industries such as automotive, logistics, and consumer goods. Robotic material handling systems enhance throughput, reduce labor costs, and ensure consistent quality in repetitive and high-volume environments. The fastest-growing application is robotic inspection, fueled by advancements in AI-powered vision systems and increasing demand for quality assurance in electronics, pharmaceuticals, and precision manufacturing. Enhanced visual recognition and defect detection are enabling manufacturers to achieve higher product standards with lower human error.

Welding remains a critical application, especially in heavy industries and automotive plants where precision and repeatability are essential. Assembly robots are frequently used in electronics and small-part manufacturing due to their speed and fine-motor capabilities. Robotic painting systems are also seeing stable demand in automotive and appliance manufacturing, providing consistent finishes and reducing environmental waste through controlled spraying. These application categories reflect the market’s evolution toward multifunctional robotic systems capable of executing multiple tasks within a single production cycle.

Among end-users, the automotive sector dominates the Robotics Market, driven by long-standing investments in robotic automation for welding, painting, and assembly processes. Automotive manufacturers rely heavily on articulated and SCARA robots for precision manufacturing and repeatability, achieving high-volume output with minimal downtime. The fastest-growing end-user is the logistics and e-commerce sector, where robotic systems are revolutionizing warehouse operations through autonomous mobile robots, sorting systems, and robotic picking technologies. The surge in online shopping and demand for rapid order fulfillment are fueling large-scale deployments across global distribution networks.

The electrical and electronics industry is another significant contributor, leveraging robotics for delicate assembly, circuit board testing, and high-speed inspection. The healthcare sector is expanding its robotic use for surgery, diagnostics, and hospital logistics, particularly as service robots gain traction in patient support and sterilization. Aerospace and food & beverage sectors are also investing in robotics to enhance production quality and compliance. These diverse end-users underscore the Robotics Market’s wide applicability and potential for long-term integration across both industrial and service-driven domains.

Asia-Pacific accounted for the largest market share at 42.5% in 2024, however, North America is expected to register the fastest growth, expanding at a CAGR of 18.2% between 2025 and 2032.

The dominance of Asia-Pacific stems from its strong manufacturing ecosystems, high-volume electronics and automotive production, and aggressive national investments in automation. Countries like China, Japan, and South Korea are at the forefront of industrial robot deployment and innovation. North America, on the other hand, is experiencing a rapid increase in automation in logistics, healthcare, and defense sectors, coupled with growing investment in robotics-as-a-service and AI-based robotic systems. The surge in e-commerce fulfillment centers and the push toward smart factories further support this region's accelerated adoption. Europe follows closely, driven by sustainability mandates and widespread implementation of collaborative robotics in small and medium-sized enterprises. Regional growth variations are influenced by digital infrastructure maturity, policy incentives, labor market dynamics, and enterprise automation strategies.

North America held a significant share of approximately 23.7% in the global Robotics Market in 2024. The region’s robust demand is fueled by its advanced manufacturing base, expansion of warehouse automation in the logistics industry, and rising healthcare robotics integration. The U.S. leads the region in both industrial and service robotics installations, with strong penetration in automotive, electronics, and medical equipment manufacturing. Regulatory incentives, such as advanced manufacturing tax credits and investment in domestic semiconductor production, are further encouraging robotic deployment. Canada and Mexico are also adopting robotics across logistics, mining, and food processing. The growing shift toward digitized and AI-powered robotic solutions, supported by cloud connectivity and real-time analytics, is transforming operational efficiency across sectors. North America’s strong innovation ecosystem and government backing for digital manufacturing ensure continued advancement and adoption of next-generation robotic platforms.

Europe represented approximately 26.1% of the global Robotics Market in 2024, with Germany, France, and the UK being the primary contributors. Germany remains the regional hub for high-precision industrial robots, largely due to its leading position in automotive and machinery production. France is expanding robotics use in pharmaceuticals and aerospace, while the UK is witnessing increased adoption in food & beverage and logistics automation. European Union regulations focused on safety, energy efficiency, and environmental compliance are shaping robotics design and integration. The region has also seen a surge in collaborative robot implementation among small and mid-sized manufacturers aiming to improve flexibility and safety. Technological integration of AI and edge computing into robotics is accelerating the adoption of smart factories and autonomous mobile solutions. Sustainability initiatives and circular economy mandates are promoting investment in energy-efficient and recyclable robotic systems across member countries.

Asia-Pacific accounted for the largest share of the Robotics Market in 2024, holding approximately 42.5% of the global total. This region leads in both robot production and consumption, with China, Japan, and South Korea driving growth. China’s manufacturing sector continues to dominate industrial robot deployment, particularly in electronics, automotive, and metalworking. Japan is a global leader in precision robotics and automation technologies, while South Korea maintains a high robot density in its industrial base. India is emerging rapidly, with investments in smart manufacturing zones and automation infrastructure. The proliferation of innovation hubs, government automation initiatives, and localized production capacities are enabling the region to scale robotics adoption efficiently. Additionally, Asia-Pacific is witnessing fast growth in service robots across healthcare and retail sectors, further expanding the scope and application of robotic technologies in both industrial and consumer domains.

In 2024, South America represented an estimated 4.6% of the global Robotics Market, with Brazil and Argentina leading regional adoption. Brazil is the largest market due to its expanding industrial base, automation needs in the mining and automotive sectors, and increasing investment in smart logistics. Argentina is following closely with robotics applications in agriculture and renewable energy. The region is experiencing gradual digital transformation driven by infrastructure modernization and urban development projects. Government policies offering import incentives for automation equipment and support for energy efficiency programs are fostering growth. Despite infrastructure and economic challenges, sectors such as oil & gas, utilities, and agritech are actively adopting robotic solutions to improve safety, reduce operational costs, and enhance productivity.

Middle East & Africa captured about 3.1% of the global Robotics Market in 2024, with UAE, Saudi Arabia, and South Africa at the forefront. The UAE is actively integrating robotics into construction, logistics, and hospitality through smart city initiatives, while Saudi Arabia’s Vision 2030 has spurred automation in manufacturing and energy. South Africa is adopting industrial and service robots in mining and healthcare. Demand across the region is influenced by the need for precision, labor optimization, and digital transformation in resource-intensive sectors. Technological modernization is gaining momentum, with AI-powered surveillance drones, robotic inspection units, and automated building solutions. Local governments are forming partnerships to encourage robotic innovation, offering favorable regulatory environments and supporting international technology investments to bridge gaps in skills and infrastructure.

China – 27.8% Market Share

High production capacity, widespread industrial automation, and extensive domestic deployment of robotics across manufacturing sectors.

Germany – 11.4% Market Share

Strong end-user demand in precision engineering, automotive manufacturing, and smart factory implementations.

The Robotics Market is characterized by a highly competitive environment with over 200 active global and regional companies vying for market share. The competitive landscape includes a mix of established industrial automation giants and specialized players in service robotics, autonomous systems, and artificial intelligence integration. Market leaders are positioning themselves through strategic acquisitions, global partnerships, and investments in R&D to enhance product innovation and performance. In recent years, major players have launched advanced collaborative robots, AI-driven robotic platforms, and scalable robotics-as-a-service (RaaS) solutions targeting SMEs and emerging industries.

Competition is also intensifying due to rapid technological convergence—robotics firms are increasingly integrating vision systems, machine learning algorithms, and cloud connectivity to deliver more intelligent and adaptable robotic systems. Key players are expanding their manufacturing footprints and after-sales support infrastructure across high-growth regions such as Asia-Pacific and North America. Additionally, the emergence of local startups offering affordable, application-specific robotics is adding to the market dynamism, prompting global players to enhance their innovation speed and customization capabilities. Regulatory compliance, sustainability standards, and interoperability features are becoming significant differentiators in competitive positioning.

ABB Ltd.

FANUC Corporation

Yaskawa Electric Corporation

KUKA AG

Mitsubishi Electric Corporation

Universal Robots A/S

Kawasaki Heavy Industries, Ltd.

Nachi-Fujikoshi Corp.

Denso Corporation

Staubli Robotics

Omron Corporation

Techman Robot Inc.

Siasun Robot & Automation Co., Ltd.

Comau S.p.A.

Teradyne Inc.

The Robotics Market is undergoing a significant transformation fueled by advancements in artificial intelligence, machine vision, cloud robotics, and edge computing. One of the most transformative trends is the integration of AI and deep learning in robotic systems, enabling real-time decision-making, self-optimization, and adaptive motion control. AI-powered robots are now being deployed in unstructured environments such as hospitals, retail spaces, and homes, performing complex tasks with minimal human intervention.

Another key technology trend is the rapid rise of collaborative robots (cobots), designed to work safely alongside human operators. These systems are gaining traction across small and medium-sized enterprises due to their ease of programming, compact size, and operational flexibility. Meanwhile, autonomous mobile robots (AMRs) are becoming essential in logistics and warehousing, using simultaneous localization and mapping (SLAM) and sensor fusion for efficient navigation and task execution.

Cloud robotics is enabling centralized data analysis, fleet coordination, and remote updates, while edge computing improves latency and real-time processing capabilities. Additionally, advancements in robotic end-effectors, haptics, and tactile sensing are improving precision in surgical robotics and micro-assembly applications. Interoperability and modular design are also facilitating seamless integration of robotics into existing industrial workflows, thus broadening the adoption landscape.

• In April 2024, FANUC launched its CRX-20iA/L collaborative robot with an extended payload capacity of 20 kg and enhanced programming via tablet interface, targeting automotive and general assembly sectors for high-mix production lines.

• In March 2024, ABB unveiled a new AI-enabled vision system integrated with its IRB 1300 robot for improved object recognition in electronics and precision manufacturing, boosting pick-and-place efficiency by up to 25%.

• In October 2023, KUKA announced a strategic partnership with a global e-commerce player to deploy over 2,000 autonomous mobile robots (AMRs) across fulfillment centers in Asia-Pacific, accelerating last-mile logistics automation.

• In June 2023, Yaskawa Electric introduced its new Motoman GP12X robotic arm, featuring enhanced reach and IP67-rated protection for use in harsh environments such as chemical and pharmaceutical manufacturing.

The Robotics Market Report provides a comprehensive analysis of the global landscape, covering a wide array of technologies, applications, and industry verticals. The scope spans industrial, collaborative, and service robots, each serving distinct operational roles in sectors such as manufacturing, logistics, healthcare, agriculture, aerospace, and construction. It examines both traditional robotic systems like articulated and SCARA robots and emerging innovations such as autonomous mobile robots (AMRs), surgical robotics, and AI-integrated humanoid platforms.

Geographically, the report encompasses key regions—Asia-Pacific, North America, Europe, South America, and Middle East & Africa—highlighting regional trends, technology adoption rates, and country-level insights. It segments the market by type (e.g., articulated, Cartesian, SCARA, parallel, collaborative robots), application (e.g., material handling, assembly, welding, inspection, packaging, medical assistance, domestic services), and end-users (e.g., automotive, electronics, food & beverage, healthcare, logistics, defense).

The report also identifies niche growth areas, including robotics-as-a-service (RaaS) and smart robotics for agriculture and elderly care, offering actionable insights for stakeholders seeking emerging investment opportunities. It outlines technology evolution, competitive dynamics, supply chain strategies, and strategic imperatives shaping the future of robotics, enabling business leaders to align innovation with market demand.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 5,320.0 Million |

| Market Revenue (2032) | USD 17,866.6 Million |

| CAGR (2025–2032) | 16.35 % |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End‑User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia‑Pacific, South America, Middle East & Africa |

| Key Players Analyzed | ABB Ltd., FANUC Corporation, Yaskawa Electric Corporation, KUKA AG, Mitsubishi Electric Corporation, Universal Robots A/S, Kawasaki Heavy Industries, Ltd., Nachi-Fujikoshi Corp., Denso Corporation, Staubli Robotics, Omron Corporation, Techman Robot Inc., Siasun Robot & Automation Co., Ltd., Comau S.p.A., Teradyne Inc. |

| Customization & Pricing | Available on Request (10 % Customization is Free) |