Reports

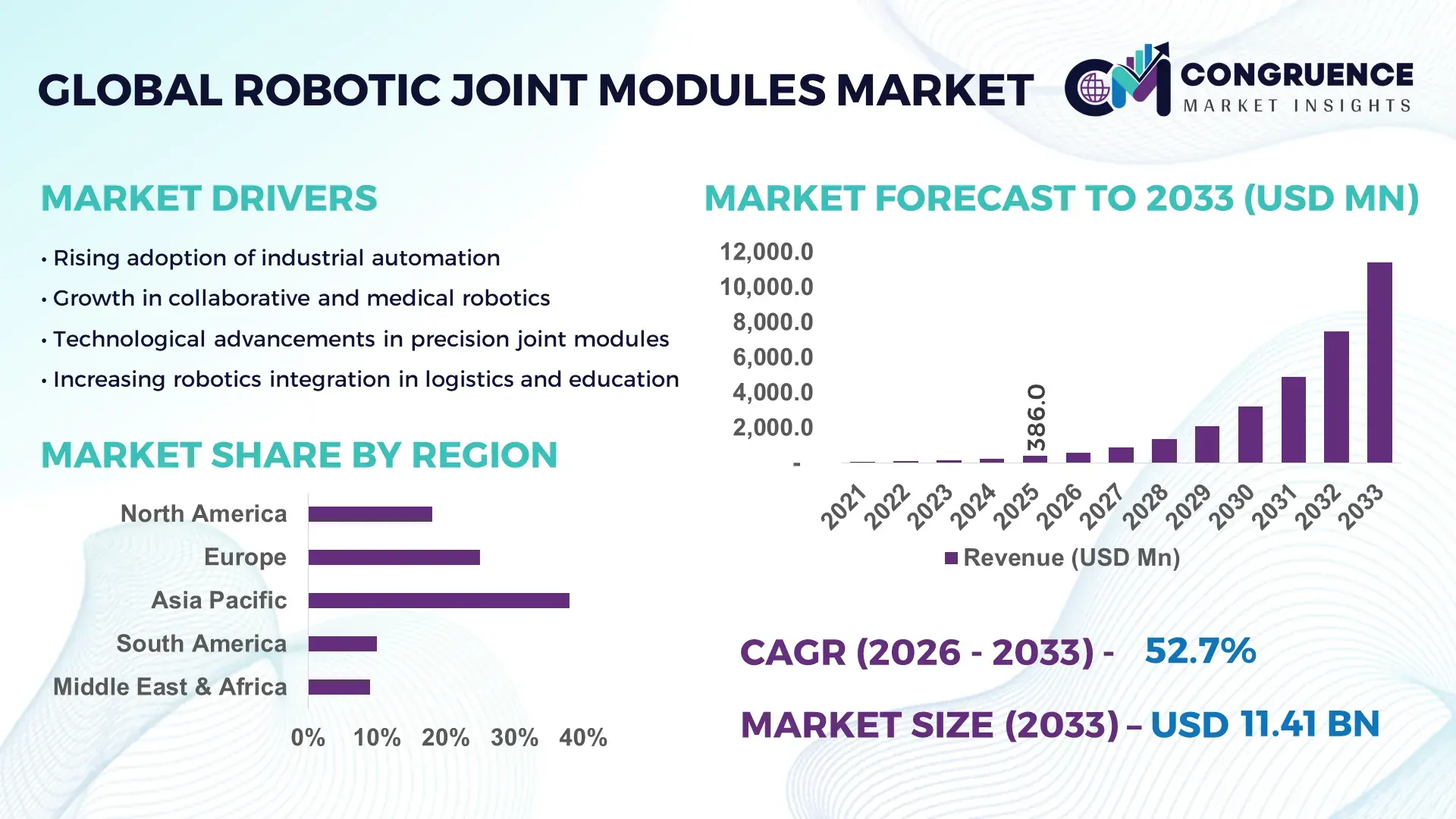

The Global Robotic Joint Modules Market was valued at USD 386.0 Million in 2025 and is anticipated to reach a value of USD 11,410.4 Million by 2033, expanding at a CAGR of 52.7% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is driven by rapid adoption of automation across industrial sectors and technological advancements in robotics.

Japan is a leading hub for robotic joint modules, demonstrating substantial production capacity with over 120,000 industrial robots deployed in 2025. Significant investments exceeding USD 500 million have been allocated to advanced manufacturing facilities, while applications in automotive assembly, electronics manufacturing, and medical robotics showcase high utilization rates. Cutting-edge developments include AI-integrated actuators, precision torque control, and modular joint designs, supporting more flexible and efficient robotic systems. Consumer adoption in precision manufacturing is increasing, with over 70% of automotive factories integrating robotic joint modules into assembly lines.

Market Size & Growth: Valued at USD 386.0 Million in 2025; projected USD 11,410.4 Million by 2033; growth fueled by automation demand and precision manufacturing.

Top Growth Drivers: Increased industrial automation adoption 68%; AI integration for precision control 55%; enhanced operational efficiency 47%.

Short-Term Forecast: By 2028, robotics performance efficiency expected to improve by 42% in assembly operations.

Emerging Technologies: AI-assisted joint calibration, modular joint designs, torque-sensing actuators.

Regional Leaders: Japan USD 4,120 Million, Germany USD 2,870 Million, USA USD 1,950 Million by 2033; unique trends include modular adoption in Japan, industrial automation in Germany, and collaborative robotics in the USA.

Consumer/End-User Trends: Automotive, electronics, and healthcare sectors increasingly integrating high-precision robotic joints with real-time monitoring.

Pilot or Case Example: In 2025, a Japanese automotive plant reduced assembly downtime by 35% through AI-controlled joint modules.

Competitive Landscape: Market leader approx. 28%; other major players include ABB, FANUC, KUKA, Yaskawa, and Nachi-Fujikoshi.

Regulatory & ESG Impact: Adoption supported by energy efficiency mandates and safety compliance; ESG initiatives target 20% waste reduction by 2030.

Investment & Funding Patterns: Recent investments totaling USD 520 million; trend toward venture-backed robotics startups and project finance for advanced joint modules.

Innovation & Future Outlook: Focus on AI integration, modular expansion, and predictive maintenance to enhance performance and reliability.

The Robotic Joint Modules Market spans automotive, electronics, healthcare, and logistics sectors. Recent technological innovations include AI-driven torque sensing, self-calibrating joints, and modular architectures that reduce downtime by up to 30%. Environmental and regulatory standards are fostering energy-efficient designs, while emerging regional demand in Asia and Europe drives production expansion and adoption of next-generation joint modules.

The Robotic Joint Modules Market is strategically vital for industrial automation, manufacturing efficiency, and advanced robotics integration. AI-enabled joint modules deliver up to 45% higher precision compared to traditional mechanical actuators. Japan dominates in volume, while Germany leads in adoption with 62% of automotive and electronics enterprises utilizing advanced joint systems. By 2028, predictive maintenance algorithms are expected to reduce equipment downtime by 28% across key industrial sectors. Firms are committing to ESG improvements such as a 20% reduction in energy consumption per unit of production by 2030. In 2025, a Japanese robotics manufacturer achieved a 33% assembly time reduction through modular AI-controlled joint deployment. Forward-looking strategies indicate that robotic joint modules will remain a cornerstone of resilient, compliant, and sustainable industrial growth, ensuring operational efficiency and technological leadership across multiple regions.

The Robotic Joint Modules Market is shaped by increased adoption of automated production systems, rising demand for high-precision robotics, and advancements in AI-enabled motion control. Integration of modular and collaborative joint modules is redefining flexibility in automotive, electronics, and medical manufacturing. Innovation in torque-sensing actuators, lightweight materials, and AI-based predictive maintenance has enhanced system reliability and reduced operational downtime. Regional investments and government incentives for robotics adoption further accelerate market expansion, while industries increasingly focus on efficiency, energy savings, and environmental compliance, driving ongoing market evolution.

Industrial automation is a primary driver of the Robotic Joint Modules Market. The adoption of robotic joint modules in automotive assembly lines has increased operational efficiency by 55%, while electronics manufacturing has seen precision improvements of 48% in micro-assembly tasks. AI-assisted calibration and torque control enable faster production cycles and reduce human error, supporting higher output levels. Enterprises integrating modular joint systems report a 32% decrease in maintenance downtime, highlighting how automation adoption directly accelerates market expansion.

The Robotic Joint Modules Market faces challenges from significant upfront investment requirements for high-precision joint modules. Initial costs for AI-enabled or modular systems can exceed USD 150,000 per unit. Integration complexity, including calibration and software compatibility, delays deployment timelines by up to 18%. Additionally, maintenance and skilled labor shortages contribute to operational bottlenecks. Industries with limited automation budgets may delay adoption, slowing overall market penetration despite rising demand for advanced robotics solutions.

Collaborative robotics creates significant opportunities for robotic joint module growth. Integration into small-scale production, healthcare, and logistics applications is increasing, with over 40% of mid-sized enterprises planning adoption by 2027. Modular joint designs enable rapid configuration changes, reducing setup times by 25%. AI-driven joint modules also support predictive maintenance and enhanced safety features, opening opportunities for sectors requiring high adaptability, precision, and low human intervention, thereby expanding the total addressable market.

High costs of advanced joint modules, complex AI integration, and regulatory compliance create challenges for market growth. Specialized materials and actuators increase production expenses, while software integration demands skilled engineers. Compliance with safety and energy efficiency regulations adds additional costs and testing requirements. For example, implementing predictive torque control can delay deployment by up to 15%, and smaller manufacturers may struggle to meet capital and technical requirements, limiting broader market adoption.

Expansion of Modular Designs: Modular joint modules now account for 58% of new industrial deployments in Japan and Germany, enabling quicker assembly line reconfiguration and a 22% reduction in setup times.

AI-Integrated Motion Control: AI-assisted torque and calibration systems enhance precision by 35%, especially in automotive and electronics manufacturing, reducing defect rates and operational downtime.

Adoption in Healthcare Robotics: Hospitals and surgical centers in Europe and North America are increasingly using robotic joint modules, achieving 28% higher efficiency in robotic-assisted surgeries and laboratory automation.

Sustainability and Energy Efficiency: Energy-efficient actuators reduce electricity consumption by 20% per unit, with ESG-compliant facilities in Japan and Germany implementing green manufacturing practices, supporting both operational cost savings and regulatory adherence.

The Robotic Joint Modules Market is strategically segmented to address diverse industrial needs across types, applications, and end-users. Type segmentation highlights various robotic joint configurations such as articulated, SCARA, parallel, and collaborative modules, each tailored to specific operational requirements. Applications range from automotive and electronics assembly to healthcare, logistics, and research automation, reflecting wide industry integration. End-user segmentation focuses on manufacturers, hospitals, research institutions, and service providers, providing insights into adoption patterns, operational efficiency improvements, and technology-driven productivity gains. Adoption rates are particularly high in precision manufacturing sectors, while modular designs are increasingly implemented in research and healthcare robotics, supporting agile and scalable deployment. Regional variations emphasize advanced deployment in Asia and Europe, with integration strategies increasingly tailored to local industry practices. Consumer adoption trends indicate that enterprises leveraging robotic joint modules report measurable improvements in production throughput, accuracy, and safety compliance, demonstrating the market’s growing strategic importance.

The Robotic Joint Modules Market includes articulated, SCARA, parallel, and collaborative joint types. Articulated joint modules currently account for 45% of adoption due to their versatility in multi-axis movement, high payload capacity, and compatibility with automotive and electronics assembly lines. Collaborative joint modules are the fastest-growing type, driven by demand for safe human-robot interaction in small-scale production and medical applications, with adoption expected to expand rapidly across industrial and healthcare sectors. SCARA modules maintain a 20% share, offering high-speed, precision motion for electronics manufacturing. Parallel joint modules contribute around 10% of the market, mainly in research and specialized automation tasks. The remaining 25% encompasses niche types including delta and hybrid modules used in packaging and light assembly.

Applications in the Robotic Joint Modules Market span automotive, electronics, healthcare, logistics, and research sectors. Automotive assembly leads with 42% adoption, supported by requirements for high-precision, multi-axis movements in engine and body assembly. Healthcare robotics is the fastest-growing application, driven by increasing adoption of surgical robots and laboratory automation, expected to expand rapidly through 2033. Electronics manufacturing contributes 28% of usage, enabling micro-assembly and inspection tasks, while logistics and research applications collectively account for 30%, supporting high-speed handling and experimental automation.

In 2025, over 38% of electronics manufacturers globally reported piloting robotic joint modules for assembly lines. In Europe, 45% of hospitals tested robotic modules for surgical assistance and laboratory automation.

End-users of robotic joint modules include manufacturers, hospitals, research institutions, and service providers. Manufacturers dominate with 50% adoption, particularly in automotive and electronics, leveraging robotic modules for assembly, inspection, and material handling. Hospitals represent the fastest-growing end-user segment, fueled by rising adoption of surgical robots, laboratory automation, and patient care applications, with expansion expected across developed regions. Research institutions contribute 15% of the adoption landscape, primarily for prototyping and high-precision experimentation. Service providers, including logistics and industrial maintenance companies, account for 20%, utilizing joint modules for warehousing and operational efficiency.

In 2025, more than 42% of European hospitals deployed robotic joint modules to automate laboratory workflows. Over 60% of automotive manufacturers in Japan reported enhanced production accuracy and reduced downtime after integrating articulated joint modules.

Asia-Pacific accounted for the largest market share at 38% in 2025; however, North America is expected to register the fastest growth, expanding at a CAGR of 52.7% between 2026 and 2033.

Asia-Pacific leads in volume due to high industrial automation adoption, with over 220,000 robotic joint modules deployed across automotive, electronics, and e-commerce sectors. Europe holds 25% of the market, driven by precision manufacturing and regulatory compliance. North America accounts for 18%, South America 10%, and Middle East & Africa 9%. The region-wise adoption reflects differences in industrial investment, technological advancement, and sector-specific demands, with Asia-Pacific focusing on manufacturing automation, Europe on sustainable industrial practices, and North America on AI-enabled robotics integration.

North America represents 18% of the global market share, with adoption concentrated in automotive, healthcare, and electronics sectors. Government incentives and tax benefits support the deployment of advanced robotics, while regulatory changes around workplace safety accelerate the adoption of collaborative robotic joint modules. Technological advancements include AI-assisted motion control, predictive maintenance, and modular joint integration. Local players like Boston Dynamics are piloting collaborative joint systems for logistics automation, achieving up to 30% improvement in operational efficiency. Enterprises in healthcare and finance show higher adoption rates, leveraging joint modules for precision tasks and risk reduction. Digitalization trends are boosting enterprise interest in integrating robotic joint modules across multiple industrial applications.

Europe accounts for 25% of the global robotic joint modules market. Leading markets include Germany, the UK, and France, where industries focus on automotive, electronics, and medical robotics. Regulatory frameworks such as ISO safety standards and sustainability initiatives promote energy-efficient robotics. Adoption of AI-based joint control, predictive maintenance, and modular designs is accelerating in manufacturing hubs. Local companies, including KUKA in Germany, are developing collaborative robotic joints to optimize assembly line performance. Regulatory pressure drives demand for explainable robotics, while end-users increasingly value energy efficiency and reliability. European enterprises report 35% improved production precision when deploying AI-enabled joint modules in manufacturing.

Asia-Pacific holds 38% of the global market, with Japan, China, and India as top-consuming countries. Manufacturing modernization, including automotive and electronics production lines, drives demand. Advanced industrial hubs in Japan and China are integrating AI-assisted torque control and modular joint systems to enhance productivity and reduce downtime. Local players such as Fanuc Japan are expanding high-precision joint modules in automotive assembly, achieving up to 40% faster throughput. Consumer behavior varies with strong enterprise adoption in high-tech manufacturing sectors, while e-commerce and mobile AI applications in logistics also stimulate deployment across the region.

South America accounts for 10% of the global market, led by Brazil and Argentina. Industrial automation in manufacturing and energy sectors, coupled with government incentives for technology adoption, is boosting robotic joint module deployment. Infrastructure upgrades and renewable energy initiatives increase demand for precise robotic systems. Local companies are introducing modular joint modules for automotive assembly, reducing manual labor requirements. Consumer behavior is driven by sector-specific adoption, including media, logistics, and industrial applications, with increasing emphasis on language localization and operational efficiency to meet regional market needs.

Middle East & Africa hold 9% of the global robotic joint modules market, with major growth in the UAE and South Africa. Demand is led by oil & gas, construction, and logistics industries, with modernization programs incorporating AI-assisted robotics. Trade partnerships and local regulations incentivize the adoption of modular and collaborative joint modules. Local players are piloting automation projects in manufacturing and energy, achieving improved operational efficiency and safety compliance. Regional consumer behavior reflects adoption in large industrial enterprises and infrastructure projects, emphasizing high precision and reliability for complex operations.

Japan – 20% Market Share: High production capacity and advanced manufacturing facilities drive market leadership.

Germany – 18% Market Share: Strong end-user demand and regulatory support for precision manufacturing enable sustained adoption.

The competitive environment in the Robotic Joint Modules Market is dynamic and moderately fragmented, with active participation from a diverse mix of multinational automation giants, specialized component manufacturers, and agile robotics startups. In total, over 50 active competitors operate globally, spanning established firms to niche innovators. The market’s top five companies collectively account for approximately 36% combined market share, indicating that no single player dominates, but rather that competition is spread across multiple strong innovators and regional specialists. Key players such as Yiyou Robotic, Maxon, Ningbo Tuopu Group, Elephant Robotics, and Kollmorgen have strategically positioned themselves through continuous R&D investment, broad product portfolios, and geographic reach. Market positioning ranges from high-precision industrial joint modules to compact, lightweight units for collaborative robots and service robotics applications.

Strategic initiatives shaping competition include expanded product launches of high-torque, sensor-integrated modules; partnerships between established automation manufacturers and AI/controls specialists; and mergers and acquisitions that consolidate technological capabilities and expand service networks. Innovation trends center on enhanced sensor integration, advanced motion control algorithms, harmonic drive systems with minimal backlash, and modular designs that facilitate rapid integration and predictive maintenance. New entrants are actively targeting niche applications such as humanoid robotics and medical robotics, where precision and reliability are key differentiators. The competitive intensity is increasing as regional manufacturers, particularly in Asia-Pacific, challenge traditional leaders with cost-competitive offerings and localized solutions, reinforcing the market’s evolving landscape.

Elephant Robotics

Kollmorgen

Ti5 Robot

Nanjing ENCOS

Main Drive Corporation

Techsoft Robots

DEEP Robotics

RobStride Dynamics

TC Drive

Guangzhou Haozhi Industrial

Estun Codroid

RealMan Robotics

SITO Robotics

The Robotic Joint Modules Market is witnessing a rapid evolution of technologies that are reshaping precision, control, and integration capabilities for industrial and service robotics. Advanced actuation systems, including high-torque density motors, harmonic drive systems, and compact servo drives, form the backbone of modern joint modules, enabling higher power-to-weight ratios and precise motion control essential for multi-axis robotics tasks.— These technologies are crucial for applications from heavy manufacturing to fine-detail medical procedures. Integrated sensor technologies, such as high-resolution encoders, torque sensors, and embedded temperature monitoring, are increasingly standard, allowing real-time feedback and adaptive control that significantly enhances operational reliability and reduces unplanned downtime through predictive diagnostics.

The ongoing shift toward smart joint modules integrates control electronics and embedded software within the module itself, which simplifies system architecture and reduces integration complexity for end-users. Robotics platforms leveraging AI-based motion planning and adaptive force control are driving improvements in human-robot collaboration, enabling safer and more efficient operations in environments with humans and machines working in close proximity. Modular design principles are enabling manufacturers to offer plug-and-play joint solutions that dramatically reduce installation time and facilitate reconfiguration of robotic workcells for variable tasks. These technological advancements are critical for sectors such as automotive, electronics, logistics, and healthcare, where precision, uptime, and system flexibility are key operational metrics. Additionally, innovations in low-backlash drive systems and compliant joint mechanisms support next-generation robot architectures like humanoids and collaborative robots, expanding capability ranges across industry sectors and pushing the frontier of robotic autonomy and dexterity.

• In January 2026, EYOU Robot Technology launched the world’s first fully automated robotic joint production line at Shanghai’s Zhangjiang Robot Valley, enabling end‑to‑end automated assembly and calibration to support mass production and improve manufacturing consistency. Source: www.corporateleadersmagazine.com

• In July 2025, HONPINE inaugurated a new robotic joint module factory, investing USD 15 million to add two new production lines and advanced testing centers designed for high‑precision harmonic drive and humanoid applications. Source: www.honpine.com

• In December 2025, Elephant Robotics published a year-in-review outlining a landmark 2025 innovation cycle, including new offerings such as the myGripper H100 dexterous gripper, myAGV Pro mobile platform, and 6-DOF collaborative robot myCobot Pro 450, alongside global adoption cases and participation in over 50 international events. Source: www.shop.elephantrobotics.com

• In December 2025, RealMan Robotics introduced three new servo joint modules featuring high torque density and fast dynamic response designed for industrial and service robots, enhancing precision and reliability for automated systems. Source: www.therobotreport.com

The scope of the Robotic Joint Modules Market Report encompasses a comprehensive examination of technology, product types, application areas, and geographic regions to provide decision‑relevant insights into this critical robotics component sector. Coverage includes detailed segmentation across types of joint modules — such as rotary, linear, high-torque, and sensor‑integrated designs — and explores their distinct mechanical and control characteristics, deployment contexts, and performance benchmarks. Application analysis spans industrial automation, collaborative robotics, healthcare and medical robotics, service robotics, logistics automation, and emerging humanoid systems, illustrating how different segments employ joint modules to fulfill specific motion, precision, and reliability requirements.

Geographic insights cover North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, detailing production capabilities, supply chain dynamics, and region-specific adoption trends tied to industrial policy, manufacturing intensity, and technological ecosystems. The report also assesses technological enablers such as embedded sensors, AI‑augmented control systems, harmonic drive technology, and modular architectures that facilitate ease of integration and scalability. Competitive analysis highlights market positioning, innovation pipelines, and strategic moves by key participants, while future outlooks consider niche segments like humanoid robotics and compact service robotics. The scope further includes emerging opportunities in predictive maintenance, human‑robot collaboration safety features, and customization frameworks that allow rapid configuration of joint modules for varied end‑user needs, ensuring a holistic view that informs investment, operational, and strategic decisions across the robotics industry.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 386.0 Million |

| Market Revenue (2033) | USD 11,410.4 Million |

| CAGR (2026–2033) | 52.7% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Yiyou Robotic, Maxon Group, Ningbo Tuopu Group, Elephant Robotics, Kollmorgen, Ti5 Robot, Nanjing ENCOS, Main Drive Corporation, Techsoft Robots, DEEP Robotics, RobStride Dynamics, TC Drive, Guangzhou Haozhi Industrial, Estun Codroid, RealMan Robotics, SITO Robotics |

| Customization & Pricing | Available on Request (10% Customization Free) |