Reports

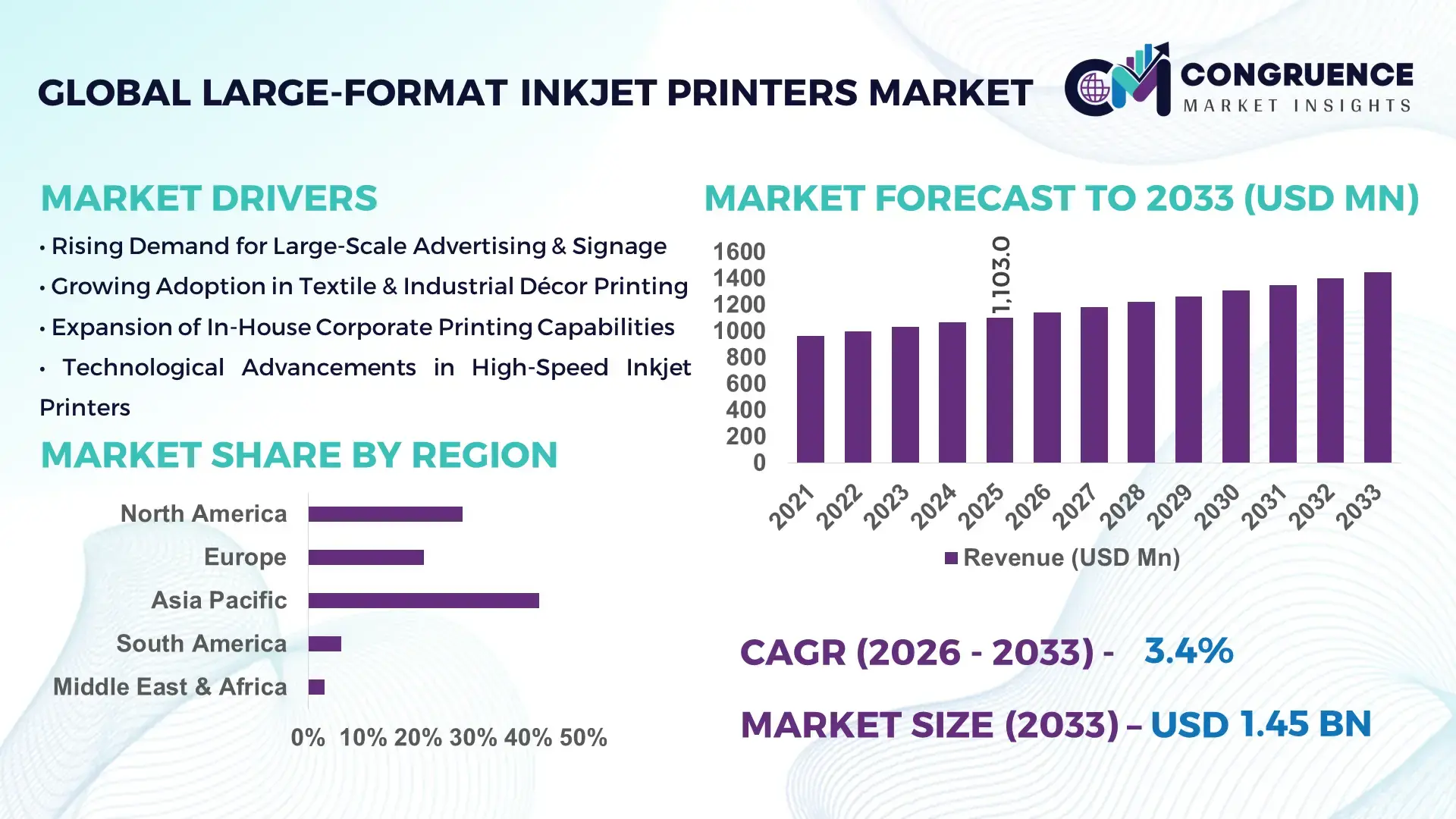

The Global Large-Format Inkjet Printers Market was valued at USD 1,103.0 Million in 2025 and is anticipated to reach a value of USD 1,445.7 Million by 2033 expanding at a CAGR of 3.44% between 2026 and 2033, according to an analysis by Congruence Market Insights, driven by rising use of high-resolution print solutions across advertising, signage, retail, and commercial sectors worldwide.

China leads the Large-Format Inkjet Printers marketplace with extensive production capacity backed by large industrial clusters and significant investments in digital print technology and smart manufacturing infrastructure. Chinese factories produce over hundreds of thousands of wide-format print engines annually and companies are deploying next-generation print heads with faster throughput and durability enhancements. Technology adoption spans textile, outdoor advertising, and interior décor applications, with automated workflow systems and integrated color management seeing adoption rates above 60% in major printing hubs.

Market Size & Growth: Market valued at USD 1,103.0 Million in 2025, expected at USD 1,445.7 Million by 2033, with a 3.44% CAGR driven by broader adoption in signage, eco-friendly inks, and digital customization demand.

Top Growth Drivers: Adoption of large-format printing for outdoor advertising (45%), increased demand for textile printing (32%), urban infrastructure signage expansion (28%).

Short-Term Forecast: By 2028, print resolution performance gains expected to improve output clarity by up to 22% across industrial LFP applications.

Emerging Technologies: Advancements in UV-curable ink systems, automated bulk ink delivery, and integrated cloud print workflows.

Regional Leaders: North America projected at ~USD 620M by 2033 with strong enterprise adoption, Asia Pacific ~USD 540M with rapid industrial uptake, Europe ~USD 410M with eco-sustainable solutions trend.

Consumer/End-User Trends: Signage and outdoor advertising remain primary users, while retail and exhibition print services show strong recurring purchase patterns.

Pilot or Case Example: In 2025, a U.S. print firm reported a 30% decrease in turnaround time using automated print head calibration technologies.

Competitive Landscape: Market leader with ~22% share (approx. U.S.-based OEM), followed by key competitors Canon, Epson, Roland, and Mimaki.

Regulatory & ESG Impact: Rising eco-ink standards and energy efficiency compliance influencing procurement decisions in Europe and North America.

Investment & Funding Patterns: Recent capex reaching over USD 1.2B globally in production and R&D expansions.

Innovation & Future Outlook: Focus on AI-enabled predictive maintenance and next-gen print heads to enhance uptime and color fidelity.

The market is shaped by robust adoption in advertising, retail, and textile sectors along with innovations in high-speed printhead technologies and eco-friendly ink solutions, while regional consumption patterns show Asia Pacific and North America driving growth due to infrastructure and commercial investments.

The Large-Format Inkjet Printers market has strategic relevance across commercial printing, outdoor advertising, textile décor, and retail display segments due to its capacity to deliver high-resolution, customizable output at scale. Businesses are aligning investments in automated ink delivery systems and digital workflows to reduce operational costs, with new UV-curable and eco-solvent ink systems improving substrate versatility. [Next-Gen Print Heads] deliver up to 18-25% improvement in speed and precision compared to older thermal print standards, reflecting measurable performance gains for high-volume printers. Regionally, North America dominates in volume due to established commercial printing infrastructure, while Asia Pacific leads in adoption rates with an increasing number of SMEs integrating large-format solutions into their service portfolios.

Short-term projections indicate that by 2028, AI-assisted predictive maintenance tools are expected to cut downtime by up to 30% in industrial print operations, enhancing return on investment for OEMs and service bureaus alike. Compliance with emerging environmental standards, such as VOC reduction measures, is prompting firms to commit to up to 20% reductions in solvent-based emissions by 2030, aligning with broader ESG commitments. In 2025, a European signage cooperative achieved a 25% reduction in material waste through automated nesting software combined with advanced head technology, showcasing how innovation delivers operational efficiencies. Looking forward, the sector is poised to be a pillar of sustainable, digitally enabled growth, integrating predictive analytics, advanced ink systems, and scalable solutions that meet evolving client specifications while maintaining cost competitiveness.

The Large-Format Inkjet Printers Market is characterized by rapid technological innovation, driven by growth in commercial advertising, retail display production, textile decoration, and urban infrastructure signage. Digital transformation is a key trend, with increasing use of automated print workflows, cloud-connected devices, and high-resolution UV-curable inks. Asia Pacific and North America account for the bulk of installations, and OEMs are prioritizing product portfolios that support sustainability, reduced waste, and versatility across substrates. Continued demand for eco-friendly and energy-efficient printing solutions is influencing product development roadmaps and procurement strategies across key industry users.

The surge in demand for high-precision output for outdoor advertising and branding is a significant driver in the Large-Format Inkjet Printers Market. As businesses seek larger, clearer signage with vivid colors and durability, investments in advanced inkjet technologies with improved print heads and ink formulations have risen, enabling production of complex graphics at faster speeds and superior detail. This driver correlates with expanding retail and urban development projects requiring large-scale visual communication. This trend has also pushed OEMs to integrate features like automated color calibration and bulk ink systems, enabling enterprises to achieve operational efficiencies with reduced downtime and consistent print quality.

High upfront costs for industrial-grade large-format inkjet printers and the associated maintenance complexities restrict adoption, especially among smaller print service providers. Advanced machines often require significant capital investment in hardware, software, and training, which can be prohibitive for emerging businesses. Additionally, maintenance and spare parts costs can accumulate, particularly for high-end UV or eco-solvent systems, challenging smaller operational budgets. These financial barriers often lead some users to delay upgrades or opt for lower-cost alternatives with fewer features, tempering overall market expansion.

The expanding demand for customized packaging and décor printing creates new opportunities for the Large-Format Inkjet Printers Market. Consumers increasingly seek personalized packaging for premium products, driving printers capable of handling diverse substrates and high-resolution outputs. This shift enables vendors to tailor offerings for niche applications in luxury retail, event décor, and bespoke interior graphics. Enterprises adopting specialized UV-curable and eco-friendly inks benefit from enhanced application ranges, opening revenue streams in sectors beyond traditional signage.

Stringent regulatory and environmental standards, such as limits on volatile organic compound emissions and energy efficiency requirements, present challenges for manufacturers and users of large-format inkjet printers. Compliance often necessitates redesigning ink formulations, upgrading hardware components, and meeting testing protocols, which can increase production costs. Additionally, environmental certification requirements may delay product launches and complicate supply chain logistics, posing obstacles for global market players striving to balance innovation with compliance.

Increased Adoption of UV-Curable and Eco-Solvent Technologies: Significant shift towards UV-curable and eco-solvent inks, with over 40% of new installations featuring these technologies, enabling broader substrate compatibility and longer outdoor durability.

The market is also seeing greater modularity in workflow automation, reducing setup time by up to 20% and enhancing throughput for high-volume print houses.

Growth in Asia Pacific Commercial Installations: Asia Pacific installations have grown sharply, with China and Japan leading in new machine deployments, accounting for more than 50% of regional unit growth. Regional enterprises increasingly incorporate smart print management systems that improve resource utilization by up to 25%.

Expansion in Textile and Decor Printing: Adoption of large-format inkjet systems in textile and décor sectors has risen, with specialized printers capable of printing on fabrics and rigid boards gaining traction; textile applications show year-over-year demand increases exceeding 30%.

Integration of Predictive Maintenance and AI Tools: Over 60% of new enterprise deployments include predictive maintenance sensors and AI-driven diagnostics, reducing unplanned downtime by approximately 30% and optimizing print head longevity.

The segmentation of the Large-Format Inkjet Printers Market reflects a technologically diverse and application-driven industry structure shaped by equipment architecture, print substrate requirements, and end-user production models. By type, the market is organized around roll-to-roll, flatbed, hybrid, and single-pass industrial systems, each aligned to specific throughput, precision, and material handling needs. By application, demand is concentrated in signage, textile printing, industrial décor, packaging prototyping, and architectural glass, with usage patterns strongly influenced by customization intensity and job turnaround requirements. End-user segmentation highlights the dominance of commercial print service providers and advertising firms, while industrial manufacturers and décor producers increasingly drive high-capacity installations. Across segments, automation adoption, defect tolerance thresholds, and regulatory compliance requirements determine equipment selection, with measurable differences in utilization rates, maintenance cycles, and digital workflow integration shaping purchasing behavior among enterprise buyers.

Roll-to-roll inkjet printers currently account for 41% of total system adoption, driven by their versatility in banners, wallpapers, vehicle wraps, and textile substrates. These systems dominate small and mid-size print operations due to lower floor-space requirements and average throughput exceeding 45 m²/hour in production settings. Flatbed printers represent 29% of adoption, favored for rigid media such as glass, wood, ceramics, and packaging boards, where registration accuracy below ±0.2 mm is critical. However, single-pass industrial inkjet systems are the fastest-growing type, expanding at an estimated 8.6% CAGR, driven by demand for continuous production lines in décor and packaging, with line speeds surpassing 90 m²/hour and labor input reduced by 35% per shift.

Hybrid systems combining flatbed and roll capabilities contribute a combined 30% share alongside niche UV-curable specialty platforms used in electronics and functional printing. Growth in single-pass systems is driven by factory automation, defect reduction targets below 0.6%, and rising adoption in laminate flooring, ceramic tiles, and corrugated packaging.

In 2024, a national standards laboratory validated a single-pass inkjet line used in ceramic tile printing that achieved 98.9% first-pass yield and reduced ink waste by 27% during continuous operation.

Signage remains the leading application, accounting for 38% of total deployments, supported by high replacement cycles in outdoor advertising, retail branding, and transit displays. Textile printing represents 24% of adoption, with digital penetration rising rapidly in soft signage and customized apparel. However, industrial décor printing is the fastest-growing application, expanding at an estimated 7.9% CAGR, driven by digital substitution in ceramic tiles, laminates, and architectural panels, where digital printing now covers over 31% of new décor production lines.

Packaging prototyping and short-run packaging account for a combined 21% share, while architectural glass and functional printing contribute the remaining 17% through specialized high-precision systems.

Consumer and enterprise adoption trends reinforce this shift. In 2025, over 44% of commercial print service providers reported increasing investment in décor and textile-capable platforms. In the US, 36% of retail chains now use digitally printed large-format graphics for in-store customization.

In 2024, a national construction research institute reported that digitally printed architectural panels were installed in over 120 large commercial buildings, reducing on-site finishing time by 32%.

Commercial print service providers are the leading end-user segment, accounting for 46% of total system installations, driven by signage, advertising, and retail branding demand. Industrial manufacturers, including décor producers and packaging converters, represent 28% of adoption, but this segment is the fastest-growing, expanding at an estimated 8.1% CAGR due to automation, inline inspection, and mass customization requirements. Advertising agencies and in-house corporate print units contribute 16%, while specialty users in electronics, glass, and functional materials represent the remaining 10%.

Industry adoption rates highlight structural shifts. In 2025, 39% of large manufacturing plants reported piloting single-pass inkjet systems for décor and packaging lines. More than 52% of global print enterprises now operate at least one UV-LED or water-based compliant system to meet emission regulations.

Commercial printers prioritize job flexibility and short-run efficiency, while industrial users focus on uptime above 95%, defect rates below 0.7%, and integration with MES platforms. These differentiated performance targets shape procurement strategies across end-user groups.

In 2025, a national manufacturing technology agency reported that over 600 industrial facilities deployed inline inkjet printing systems, achieving an average 24% reduction in manual finishing operations.

Asia-Pacific accounted for the largest market share at 42% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 4.1% between 2026 and 2033.

Asia-Pacific leads in volume with more than 185,000 active large-format systems installed across industrial and commercial sites, supported by high manufacturing density in China, Japan, and India. North America holds 28% of global installations, with over 62,000 enterprise-grade systems operating in signage, décor, and packaging lines. Europe represents 21% share, driven by sustainability-led upgrades and UV-LED adoption exceeding 57% of new systems. South America and the Middle East & Africa together contribute 9%, but unit shipments in these regions grew by 18% year-on-year in 2025. Regional differences in automation penetration, regulatory compliance, and industrial décor capacity strongly influence equipment replacement cycles and digital workflow adoption.

North America accounts for approximately 28% of global system installations, supported by strong demand from signage, retail branding, packaging prototyping, and architectural décor. The United States alone hosts over 35 large-format manufacturing and integration facilities, with enterprise adoption rates exceeding 61% among commercial print service providers. Regulatory pressure on solvent emissions has driven over 54% of new systems toward UV-LED and water-based platforms. Technological trends include AI-based nozzle monitoring adopted by 47% of new industrial lines and MES integration in over 40% of large print plants. A leading regional player expanded its automated flatbed production lines in 2024, increasing daily throughput by 32%. Consumer behavior shows higher enterprise adoption in retail, healthcare, and finance, where customized signage and compliance labeling drive consistent equipment utilization.

Europe represents nearly 21% of global installations, with Germany, the UK, France, and Italy accounting for over 68% of regional demand. Regulatory initiatives targeting VOC reduction have pushed 63% of new deployments toward low-emission ink systems. Industrial décor and ceramic printing dominate Southern Europe, while packaging and architectural glass lead in Germany and France. Adoption of inline vision inspection exceeds 52% of industrial systems, reflecting strict quality standards below 0.6% defect tolerance. A major European manufacturer invested in hybrid flatbed-roll platforms in 2025, expanding rigid media capacity by 28%. Regional consumer behavior shows regulatory pressure leading to accelerated adoption of traceable, low-emission digital print workflows.

Asia-Pacific holds the largest volume share with 42% of global installations, led by China, Japan, and India, which together operate more than 110,000 active systems. China alone accounts for nearly 48% of regional unit shipments, driven by textile printing and packaging conversion. Japan leads in precision industrial décor systems, while India shows the fastest installation growth in signage and soft signage. Manufacturing automation penetration exceeds 45% in large plants, with single-pass systems now used in over 31% of new décor lines. A leading regional supplier expanded ceramic tile inkjet capacity by 40 production lines in 2024. Consumer behavior reflects growth driven by e-commerce branding, mobile retail, and rapid customization demand.

South America contributes approximately 6% of global installations, with Brazil and Argentina accounting for over 72% of regional demand. Signage and retail branding dominate, representing 46% of active systems, while packaging prototyping is rising rapidly. Infrastructure investment in transport and urban development supported 17% growth in system shipments in 2025. Government incentives for digital manufacturing in Brazil accelerated automation upgrades across over 120 commercial print facilities. A regional player expanded textile printing capacity by 9,000 m² per day in 2024. Consumer behavior shows demand tied closely to media localization, political advertising cycles, and multilingual branding requirements.

The Middle East & Africa represents around 3% of global installations, but unit deployments grew by 22% in 2025 due to construction, hospitality, and infrastructure projects. The UAE, Saudi Arabia, and South Africa account for over 64% of regional demand. Architectural glass and building décor drive more than 38% of system utilization, supported by smart city programs. Technological modernization includes adoption of UV-LED systems in 51% of new deployments. A Gulf-based print integrator installed 12 industrial flatbed lines for infrastructure signage in 2024. Consumer behavior shows strong demand for premium graphics in hospitality, retail malls, and mega-event branding.

China – 29% Market Share: Dominates through the highest production capacity and large-scale textile and packaging printing installations.

United States – 24% Market Share: Leads through strong enterprise demand, advanced industrial décor printing, and high automation penetration.

The competitive environment of the Large-Format Inkjet Printers Market is moderately consolidated yet dynamic, with at least 30+ active competitors globally ranging from multinational printer manufacturers to specialized industrial inkjet solution providers. The top five companies — HP Development Company, L.P., Canon Inc., Seiko Epson Corporation, Ricoh Company Ltd., and Konica Minolta, Inc. — collectively command an estimated 40–45% share of the market, illustrating a competitive landscape where leading players balance technological leadership with broad geographic coverage and extensive channel networks.

Major firms position themselves through strategic initiatives such as new product launches, enhanced digital workflows, and expanded service ecosystems. For example, HP maintains a strong presence with its latex and thermal inkjet portfolios and integrated cloud print management solutions, while Canon leverages its multi-series imagePROGRAF platforms offering high color accuracy and media versatility. Epson’s investment in PrecisionCore printheads and eco-solvent solutions supports demand in textile and signage segments. Ricoh and Konica Minolta differentiate with production-grade systems tailored for industrial décor and long-run applications.

Innovation trends driving competition include the integration of AI-enabled predictive maintenance, inline media handling automation, and sustainable ink technologies such as UV-LED and water-based systems. Partnerships — such as collaboration agreements between OEMs and workflow software providers — and product portfolio expansions continue to shape the competitive chart as vendors seek to capture both enterprise and industrial print budgets. Overall, the market’s competitive nature reflects ongoing shifts toward automation, quality enhancement, and end-to-end print production solutions.

Ricoh Company Ltd.

Konica Minolta, Inc.

Roland DG Corporation

Mimaki Engineering Co. Ltd.

Agfa-Gevaert N.V.

Xerox Holdings Corporation

Mutoh Holdings Co. Ltd.

Fujifilm Holdings Corporation

Kyocera Corporation

Lexmark International Inc.

Brother Industries Ltd.

The Large-Format Inkjet Printers Market is experiencing rapid technological evolution as enterprises and industrial users increasingly demand higher throughput, quality, and automation. Core technologies shaping the landscape include advanced printhead architectures, ink chemistry innovations, and digital workflow integrations. Modern printheads, such as Epson’s PrecisionCore and Canon’s multi-jet configurations, deliver enhanced droplet control supporting resolutions beyond 2,400 dpi and enabling consistent media handling across signage, textile, and décor applications.

Ink chemistry advancements are transforming operational performance and environmental impact. UV-LED and water-based latex formulations provide durable outputs with low emissions, broad substrate compatibility, and reduced post-print processing, addressing health and compliance priorities in commercial and industrial settings. These ink systems also drive faster curing and minimize waste through precise droplet placement and dry-on-impact strategies.

Automation and digital transformation are central to technology adoption. Cloud-based fleet management, AI-driven predictive maintenance, and inline quality inspection modules improve uptime and reduce manual intervention, allowing enterprises to maintain production continuity and meet tight delivery windows. Integration with enterprise resource planning (ERP) and manufacturing execution systems (MES) enables real-time monitoring of print runs, capacity planning, and job scheduling, optimizing factory footprints.

Emerging technologies include single-pass industrial inkjet systems, offering continuous high-speed output capabilities suitable for décor, packaging, and textile markets; and hybrid UV/aqueous platforms that support versatile production environments. Decision-makers are also exploring automation robotics in media handling and finishing to enhance throughput. Overall, technology investments in print quality, sustainability, and digital connectivity are reshaping competitive advantage and unlocking new operational efficiencies across the large-format ecosystem.

• In May 2025, HP Inc. officially introduced the HP Latex 730 and HP Latex 830 Printer Series — the latest generation of water-based large-format printing solutions designed to enhance productivity, colour consistency, and sustainability for print service providers. These printers deliver up to 30% faster white-ink performance and support automated workflows with HP PrintOS Production Hub for enhanced job management. Source: www.hp.com

• In April 2025, Konica Minolta, Inc. unveiled the AccurioJet 30000 B2 HS-UV Inkjet Press, a next-generation digital UV inkjet solution that maximizes productivity with features such as improved RIP processing, high-definition modes, and automatic duplex printing, handling diverse media up to 0.6 mm thickness. Source: www.konicaminolta.com

• In June 2025, Konica Minolta Business Solutions U.S.A., Inc. announced the first commercial installation of its AccurioJet 30000 HS-UV Inkjet B2+ 29″ Press at Neyenesch Printers in California, delivering faster make-ready times and broader media handling for commercial printing applications. Source: www.print3.in

• In September 2025, HP Inc. scheduled a webinar to showcase how the HP Latex 730 and 830 series can transform print businesses by expanding service offerings into high-margin areas such as vehicle wrapping and custom wallpaper applications, underscoring HP’s commitment to innovation and partner support. Source: www.texintel.com

The Large-Format Inkjet Printers Market Report delivers a comprehensive view of the industry’s breadth and depth, covering segmentation across product types, applications, and end-users to inform strategic decision-making. It systematically analyzes core product categories including roll-to-roll, flatbed, hybrid, and single-pass inkjet systems, with detailed insights into their operational capabilities, media compatibility, and application-specific use cases tailored to signage, textile printing, décor, packaging prototyping, and architectural graphics. The report also dissects end-user landscapes — from commercial print service providers to industrial manufacturers — providing adoption patterns, utilization benchmarks, and technology integration trends that highlight how organizations deploy large-format inkjet solutions in real-world environments. Unique sections address regional market dynamics across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, offering unit shipment volumes, infrastructure influences, and technology penetration variations.

Technology analyses focus on printhead innovations, ink chemistry developments (including UV-LED, water-based, and eco-solvent platforms), digital automation capabilities such as cloud print management and AI-based predictive maintenance, and workflow integration with enterprise systems. Operational priorities like quality standards, media handling efficiency, and environmental compliance measures are examined to support competitive benchmarking. Additionally, the report highlights emerging and niche segments including high-speed industrial inkjet production, hybrid digital print workflows, and automated finishing solutions, presenting a holistic view of current capabilities and future potential. Designed for executives, strategists, and industry analysts, the report synthesizes quantitative indicators with qualitative insights to guide investments, product planning, and go-to-market strategies in the evolving large-format inkjet ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,103.0 Million |

| Market Revenue (2033) | USD 1,445.7 Million |

| CAGR (2026–2033) | 3.44% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia Pacific, South America, Middle East & Africa |

| Key Players Analyzed | HP Development Company, L.P., Canon Inc., Seiko Epson Corporation, Ricoh Company Ltd., Konica Minolta, Inc., Roland DG Corporation, Mimaki Engineering Co. Ltd., Agfa-Gevaert N.V., Xerox Holdings Corporation, Mutoh Holdings Co. Ltd., Fujifilm Holdings Corporation, Kyocera Corporation, Lexmark International Inc., Brother Industries Ltd. |

| Customization & Pricing | Available on Request (10% Customization Free) |