Reports

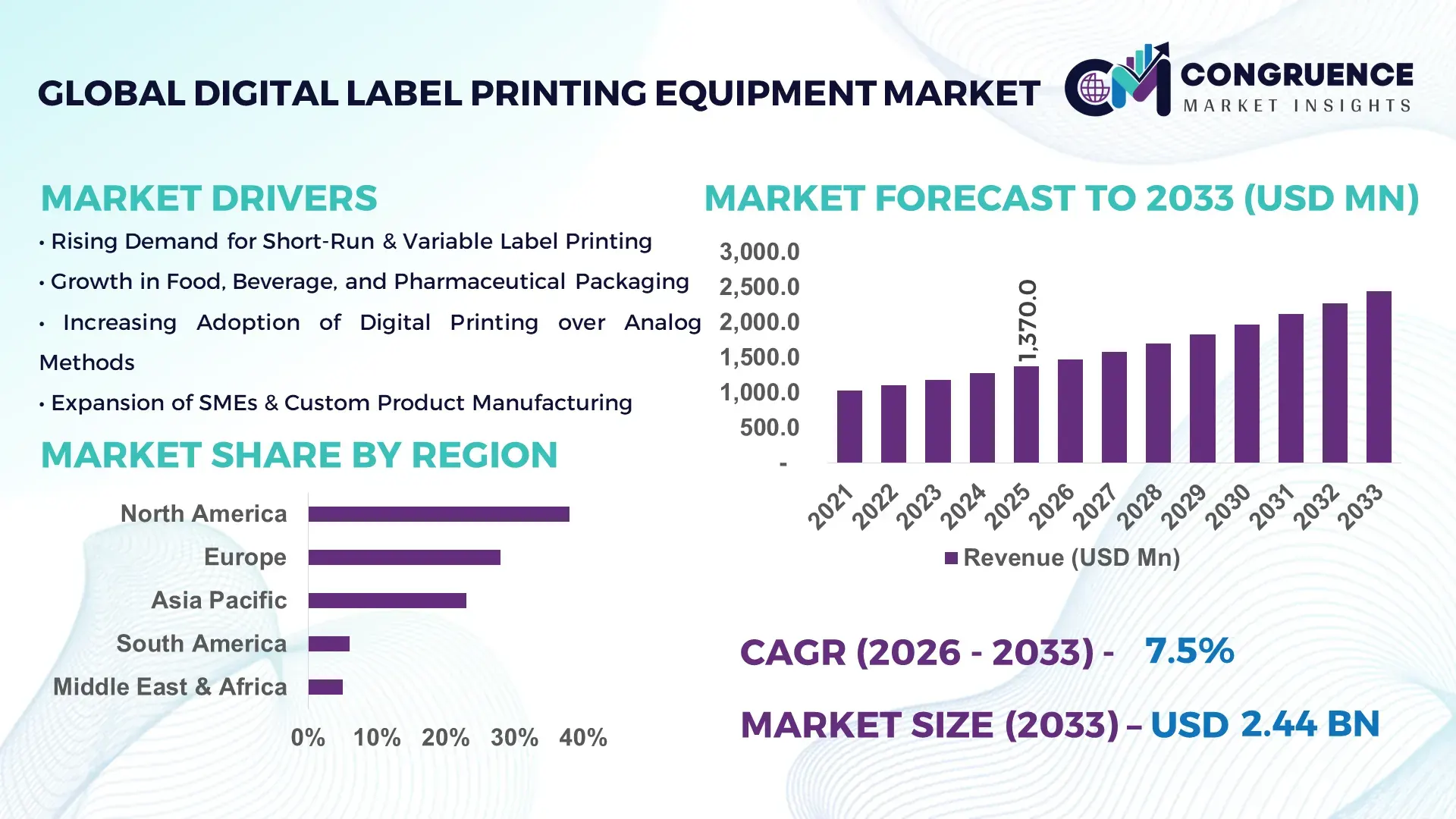

The Global Digital Label Printing Equipment Market was valued at USD 1,370.0 Million in 2025 and is anticipated to reach a value of USD 2,443.4 Million by 2033 expanding at a CAGR of 7.5% between 2026 and 2033, according to an analysis by Congruence Market Insights, driven by rising adoption of high-speed, precision printing in packaging and labeling operations.

The United States leads the Digital Label Printing Equipment Market, boasting production facilities capable of producing over 3,500 high-performance label presses annually. The country has invested more than USD 250 million in R&D over the past five years, focusing on hybrid inkjet technologies and UV-curable inks. Major applications span food and beverage, pharmaceuticals, and consumer goods, with technological advancements in automated quality control, inline finishing, and AI-driven print optimization. Consumer adoption is accelerating, with over 65% of packaging enterprises integrating digital label solutions into production lines to enhance efficiency and reduce lead times.

Market Size & Growth: USD 1,370.0 Million in 2025; projected USD 2,443.4 Million by 2033; growth driven by precision labeling needs.

Top Growth Drivers: Increased automation adoption 68%, demand for short-run customization 55%, digital integration in packaging 60%.

Short-Term Forecast: By 2028, print speed efficiency expected to improve by 20%, reducing operational bottlenecks.

Emerging Technologies: Hybrid inkjet-thermal presses, AI-based color management, inline finishing automation.

Regional Leaders: North America USD 820.0 Million, Europe USD 630.0 Million, Asia Pacific USD 510.0 Million by 2033; Europe showing fastest uptake of AI-driven printing solutions.

Consumer/End-User Trends: Key end-users include pharmaceuticals, FMCG, and specialty packaging; rising preference for on-demand, short-run labels.

Pilot or Case Example: In 2025, a U.S. beverage manufacturer achieved 35% reduction in changeover time through automated label press deployment.

Competitive Landscape: Leading player holds approximately 18% market share; major competitors include Avery Dennison, Domino Printing, Epson, and Konica Minolta.

Regulatory & ESG Impact: Incentives for sustainable inks, reduction in volatile organic compounds (VOCs), and compliance with global packaging regulations driving adoption.

Investment & Funding Patterns: Recent investments exceeding USD 250 million; growing trend toward venture-backed innovation in hybrid printing technologies.

Innovation & Future Outlook: Integration of AI, IoT, and cloud-based print management; expansion of automated finishing systems for reduced labor dependency.

The market is witnessing accelerated adoption in food and beverage, healthcare, and personal care sectors, where regulatory compliance and product traceability are critical. Recent product innovations include UV-curable inks and inline quality control sensors, while regional consumption patterns show Europe leading in premium label adoption and Asia Pacific in high-volume, cost-efficient solutions. Emerging trends focus on sustainability, digital workflow integration, and smart packaging solutions.

The Digital Label Printing Equipment Market is strategically crucial for industries aiming to combine operational efficiency with sustainable production. Hybrid inkjet presses deliver 25% faster production compared to conventional flexographic presses, enhancing flexibility for short-run and high-mix jobs. North America dominates in volume, while Europe leads in adoption with over 62% of packaging enterprises implementing digital label printing solutions. By 2028, AI-driven color management is expected to reduce waste and rework by 18%. Firms are committing to environmental sustainability improvements, including a 20% reduction in VOC emissions and increased recycling of label substrates by 2030. In 2025, a leading U.S. pharmaceutical company achieved a 30% reduction in label changeover downtime through automated inline finishing. Looking forward, the Digital Label Printing Equipment Market will serve as a cornerstone of operational resilience, regulatory compliance, and sustainable growth, positioning manufacturers to meet evolving industry demands with precision and efficiency.

The Digital Label Printing Equipment Market is shaped by growing demand for high-speed, short-run labeling solutions, technological innovations in printing and finishing, and increased regulatory scrutiny on packaging. Manufacturers are focusing on hybrid and fully digital presses that enable on-demand printing, inline quality control, and integration with packaging lines. Industry trends include AI-driven workflow automation, IoT-enabled predictive maintenance, and sustainable ink formulations. Demand is also influenced by sectors requiring traceability, regulatory compliance, and rapid product launches, with North America and Europe leading in adoption due to mature packaging infrastructure.

The growing need for personalized packaging and smaller production batches is a key driver of market expansion. Approximately 60% of FMCG and beverage companies have implemented short-run digital label production to reduce inventory costs and accelerate time-to-market. Automation and hybrid printing technologies have improved print speeds by 25–30%, enabling businesses to respond quickly to changing consumer preferences. The surge in e-commerce packaging and specialty product launches further emphasizes the importance of agile labeling solutions, fostering greater adoption of digital label printing equipment globally.

Despite operational advantages, high upfront costs for advanced digital label presses limit adoption among smaller manufacturers. Capital requirements often exceed USD 250,000 per unit, with additional costs for maintenance, specialized inks, and staff training. Operational complexity, including integration with ERP systems and workflow software, poses a challenge for enterprises lacking technical expertise. In addition, volatile ink prices and energy consumption contribute to higher operating expenses, slowing market penetration in developing regions with constrained budgets.

Sustainability-focused packaging initiatives provide a significant growth opportunity. Manufacturers adopting UV-curable inks and recyclable substrates can reduce environmental impact by up to 40%. Smart labels embedded with QR codes or RFID chips are gaining traction, offering traceability and enhanced consumer engagement. Emerging sectors such as pharmaceuticals and organic food are increasingly investing in automated digital labeling solutions, with adoption rates projected to rise by 50% over the next three years. This trend encourages equipment manufacturers to innovate in precision printing, finishing automation, and IoT-enabled solutions.

The Digital Label Printing Equipment Market faces challenges from regulatory pressures, including environmental standards for inks and packaging materials, and compliance with international labeling requirements. Rising energy costs and material prices add financial strain, while training personnel on sophisticated digital presses requires additional investment. Moreover, the transition from analog to digital workflows involves process redesign, software integration, and infrastructure upgrades, all of which can delay ROI and limit adoption, particularly for mid-sized manufacturers in emerging markets.

Expansion of Hybrid Digital Presses: Hybrid presses are now adopted in over 55% of high-volume packaging operations, enabling flexibility for short-run jobs and cost reduction. These systems combine inkjet and flexographic technologies to improve print speed by 20% while maintaining high resolution.

Integration of AI and IoT: Nearly 48% of digital label presses now feature AI-driven color calibration and IoT-enabled predictive maintenance, reducing downtime by up to 25% and minimizing material waste.

Growth of Sustainable Printing Practices: Adoption of UV-curable and water-based inks has increased by 35% in North America and Europe, lowering VOC emissions and enhancing compliance with environmental regulations.

Automated Inline Finishing: Over 40% of new installations include automated finishing modules that cut, laminate, and inspect labels inline, improving throughput by 30% and reducing manual labor dependency, particularly in pharmaceutical and beverage packaging sectors.

The Digital Label Printing Equipment Market is organized around three primary segmentation pillars: type, application, and end-user. By type, the market includes hybrid presses, single-pass inkjet, and thermal transfer systems, each serving specific operational needs and production scales. Applications span food and beverage, pharmaceuticals, personal care, and industrial goods, reflecting diverse labeling requirements from compliance to consumer engagement. End-users encompass large-scale manufacturers, contract packagers, and small-to-medium enterprises adopting digital solutions for flexibility and speed. Geographic adoption patterns indicate that North America and Europe favor high-precision hybrid presses, while Asia Pacific prioritizes cost-efficient single-pass systems. Overall, segmentation reflects an interplay between technological sophistication, industry-specific labeling needs, and operational scale, offering strategic guidance for equipment deployment and investment decisions.

Hybrid digital presses currently lead the market, accounting for approximately 45% of adoption due to their flexibility in handling short-run and high-mix jobs while maintaining high print quality. Single-pass inkjet systems are the fastest-growing type, driven by demand for high-speed production in food and beverage sectors, enabling faster label throughput and enhanced efficiency. Thermal transfer systems, though more niche, continue to serve industrial and regulatory-focused applications, representing the remaining 30% combined market share.

Food and beverage labeling dominates the market with a 50% share, supported by stringent compliance requirements and high customization demand for retail packaging. Pharmaceutical labeling is the fastest-growing application, propelled by regulatory traceability mandates and automated serialization solutions, currently showing significant adoption increases. Other applications such as personal care, industrial goods, and specialty packaging contribute a combined 30% of market utilization.

Consumer adoption statistics highlight that over 38% of enterprises globally are piloting digital label solutions for product differentiation, while 60% of Gen Z consumers demonstrate stronger trust in brands offering transparent, on-demand labeling.

Large-scale manufacturers represent the leading end-user segment, capturing roughly 52% of market adoption, due to their high-volume labeling requirements and investments in hybrid presses. Contract packaging firms are the fastest-growing end-users, driven by the increasing outsourcing of labeling tasks and demand for flexible short-run capabilities, reflecting rapid operational adoption. SMEs and specialty product producers constitute the remaining 28% combined, focusing on niche or customized labeling needs. Industry adoption rates show 42% of food and beverage enterprises, 35% of pharmaceutical companies, and 25% of personal care firms actively integrating digital labeling technologies.

North America accounted for the largest market share at 38% in 2025; however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 8.2% between 2026 and 2033.

In 2025, North America deployed over 1,200 hybrid digital presses and 950 single-pass inkjet systems, supporting food & beverage, pharmaceuticals, and personal care sectors. Europe followed with 28% market share, driven by regulatory compliance and sustainability initiatives. Asia Pacific consumed over 40% of total production units in 2025, with China contributing 18% of the regional demand and India 12%. South America and Middle East & Africa collectively accounted for 11%, primarily supported by emerging industrial and energy sectors. Across regions, enterprise adoption ranges from 45% to 68%, reflecting a strong shift toward digital transformation and smart labeling solutions.

North America holds a 38% market share of digital label printing equipment, with high-volume manufacturing and healthcare sectors driving adoption. Enterprises are increasingly integrating AI-assisted quality control and inline finishing to enhance operational speed. Regulatory incentives for sustainable inks and reduced VOC emissions have accelerated modernization. Key technological trends include hybrid presses with IoT-enabled predictive maintenance and automated color calibration. Avery Dennison, a leading player, recently expanded production lines for hybrid presses supporting short-run customization. North American consumer behavior shows higher adoption in healthcare, finance, and FMCG, with over 62% of enterprises implementing digital labeling systems for operational efficiency and compliance.

Europe accounts for approximately 28% of the digital label printing equipment market, with Germany, the UK, and France leading adoption. Regulatory pressure for sustainable packaging and traceable labeling has led to widespread integration of eco-friendly inks and automated serialization solutions. Emerging technologies, including AI-driven print optimization and hybrid digital presses, are increasingly adopted. Local players such as Domino Printing Technologies are investing in inline finishing automation to reduce operational downtime. European consumer behavior is influenced by regulatory standards and environmental awareness, with 58% of enterprises prioritizing sustainable and explainable labeling systems to meet market and compliance demands.

Asia Pacific accounted for 23% of the market volume in 2025, ranking second in total adoption and expected to grow fastest. Top consuming countries include China, India, and Japan, with China deploying over 650 digital presses in 2025 alone. Manufacturing and packaging infrastructure is expanding, supporting high-speed label printing for food & beverage and e-commerce sectors. Technological innovation hubs in Singapore and Japan focus on smart labeling and IoT-enabled presses. A local Chinese player implemented hybrid presses across FMCG lines, increasing production efficiency by 20%. Consumer behavior trends show a strong preference for on-demand and personalized packaging, particularly in online retail and mobile commerce.

South America captured 6% of the market share in 2025, with Brazil and Argentina being the primary contributors. Industrial and food processing sectors drive demand, supported by modernization of packaging infrastructure. Government incentives and trade policies promote local manufacturing and import of high-tech printing equipment. A Brazilian company recently deployed hybrid presses for beverage labeling, reducing lead time by 18%. Consumer behavior in South America emphasizes localized content, language-specific labeling, and compliance with regional standards, particularly in multilingual and diverse markets.

Middle East & Africa accounted for 5% of the market share in 2025. Key growth countries include UAE and South Africa, where demand is driven by oil & gas, construction, and FMCG sectors. Technological modernization includes adoption of hybrid and automated presses with digital workflow integration. Local regulations and trade partnerships encourage sustainable inks and high-precision labeling solutions. A UAE-based packaging firm implemented hybrid presses to enhance labeling efficiency for consumer goods, achieving a 22% reduction in downtime. Consumer behavior shows a preference for high-quality packaging that meets international standards while supporting regional customization needs.

United States – 38% Market Share: Dominates due to high production capacity, advanced hybrid press deployment, and strong end-user adoption in healthcare and FMCG.

Germany – 12% Market Share: Leads in adoption because of stringent regulatory compliance, industrial automation, and investment in sustainable labeling solutions.

The competitive environment of the Digital Label Printing Equipment Market is dynamic and moderately consolidated, with a diverse mix of global leaders and niche specialists driving innovation and adoption. Around 20+ major competitors are actively competing worldwide, offering varied technologies spanning hybrid presses, single-pass inkjet, UV inkjet systems, and digital finishing solutions. The top 5 companies collectively hold around 50% of the market influence, indicating a competitive balance between established brands and emerging innovators. Tier‑1 leaders such as HP Indigo, Xeikon, and Canon maintain strong positioning through high‑performance digital presses and expanded service networks, while Tier‑2 firms including Epson, Durst, and Domino Printing capture significant volume with cost‑effective, high‑speed solutions. Other competitors like Konica Minolta, Mark Andy, Screen, and Fujifilm contribute to regional penetration and niche applications. Strategic initiatives are shaping competition: in 2025, Domino Printing Sciences introduced a high‑speed productivity mode for its N730i Digital Label Press that boosted throughput by up to 28% while reducing ink usage, enhancing its operational value proposition. Additionally, Husky Labels adopted advanced UV digital presses with extended media compatibility, expanding versatility in label formats. Innovation trends focus on AI‑enabled workflow automation, predictive maintenance, eco‑friendly inks, cloud‑based job management, and enhanced color gamut capabilities. These strategic moves underscore a competitive landscape where efficiency, sustainability, and technological differentiation are critical for maintaining market relevance.

Epson

Durst Phototechnik

Domino Printing Sciences

Konica Minolta

Mark Andy

Screen Holdings

Kodak

Avery Dennison

Videojet Technologies

Brother Industries

Primera Technology

Colordyne Technologies

Technology continues to be a core competitive differentiator in the Digital Label Printing Equipment Market, with current and emerging technological advancements reshaping operational capabilities and enterprise adoption. Hybrid digital presses, which combine inkjet with conventional printing technologies, are widely adopted for their versatility in handling both short and medium runs, while maintaining high resolution and color fidelity. Single‑pass inkjet systems are expanding in high‑speed environments, enabling printing speeds that align with modern packaging demands. Innovations such as water‑based inkjet inks and eco‑compliant consumables are gaining traction, addressing sustainability goals and regulatory pressures on volatile organic compounds (VOCs) and recyclability. Automation and smart features are also significant: AI‑driven color calibration systems, IoT‑enabled predictive maintenance, and automated inline finishing solutions are enhancing uptime and reducing waste by optimizing workflows. Industry 4.0 integration, including cloud‑based job management and workflow orchestration platforms, allows enterprises to synchronize print tasks, monitor performance metrics in real time, and adjust job parameters dynamically, improving resource efficiency and responsiveness. Higher resolution print heads (e.g., 1600 x 1600 dpi) have become standard offerings for premium and high‑quality label outputs, catering to brand packaging needs that emphasize sharp graphics and precise color reproduction. Consumer demand for variable data printing (VDP) capabilities has also driven software‑hardware integration, enabling unique, serialized, and secure labeling across sectors such as pharmaceuticals and logistics. This technological evolution positions digital label printing solutions as essential infrastructure for modern packaging operations, supporting agility, customization, and digital transformation strategies for decision‑makers and industry professionals.

• In July 2025, HP introduced the new HP Indigo 6K+ Digital Press, featuring the SmartControlSystem with AI‑powered automation, enhanced diagnostics, and real‑time workflow tools designed to increase uptime, streamline setup, and support diverse label substrates by covering up to 97% of the color gamut. This press is slated for global availability by the end of July 2025. Source: www.hp.com

• In September 2025, Domino Printing Sciences announced that its N730i Digital UV Inkjet Label Press received certification from Color‑Logic for compatibility with their metallic and high‑impact color effect design technology, enabling printers to produce visually enhanced premium labels and expand creative offerings. Source: www.color‑logic.com

• In October 2025, Domino Printing Sciences secured a second N610i Digital Label Press installation for Italian manufacturer Gruppo Finlogic, reinforcing investment in digital workflows and boosting printing performance and label production capacity. Source: www.domino‑printing‑sciences.prowly.com

• In January 2024, Art Advertising added a Domino N610i 7‑color digital UV inkjet label press to its operations, enabling flexible high‑quality printing and supporting a broader range of label applications for its commercial clients. Source: www.labelandnarrowweb.com

The scope of the Digital Label Printing Equipment Market Report encompasses a comprehensive examination of the technologies, segments, and regions that define this rapidly evolving industry. It covers a broad array of equipment types, including hybrid digital presses, single‑pass inkjet systems, UV inkjet solutions, and digital finishing technologies tailored for pressure‑sensitive labels, shrink sleeves, wrap‑around formats, and linerless applications. Advanced system types such as high‑resolution inkjet and electrophotographic platforms are analyzed for their impact on quality and operational flexibility. End‑use sectors are examined in detail, including packaging enterprises, converting companies, and retail label producers, highlighting specific adoption patterns across food & beverage, pharmaceutical, personal care, and industrial segments. Geographic insights span North America, Europe, Asia Pacific, Latin America, and Middle East & Africa, offering granular views of regional demand drivers, infrastructure readiness, and technology preferences. The report also explores workflow and software integration, predictive maintenance, automation, and sustainability trends shaping investment and procurement decisions. Additionally, niche and emerging segments such as variable data printing, eco‑compliant consumables, and smart labeling solutions are included to provide forward‑looking perspectives on innovation and market expansion opportunities. Tailored for industry professionals and decision‑makers, the report synthesizes numerical insights on system deployments, adoption rates, technology penetration, and competitive differentiation to support strategic planning, product development, and investment evaluation across the global digital label printing ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,370.0 Million |

| Market Revenue (2033) | USD 2,443.4 Million |

| CAGR (2026–2033) | 7.5% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | HP Indigo; Xeikon; Canon; Epson; Durst Phototechnik; Domino Printing Sciences; Konica Minolta; Mark Andy; Screen Holdings; Kodak; Avery Dennison; Videojet Technologies; Brother Industries; Primera Technology; Colordyne Technologies |

| Customization & Pricing | Available on Request (10% Customization Free) |