Reports

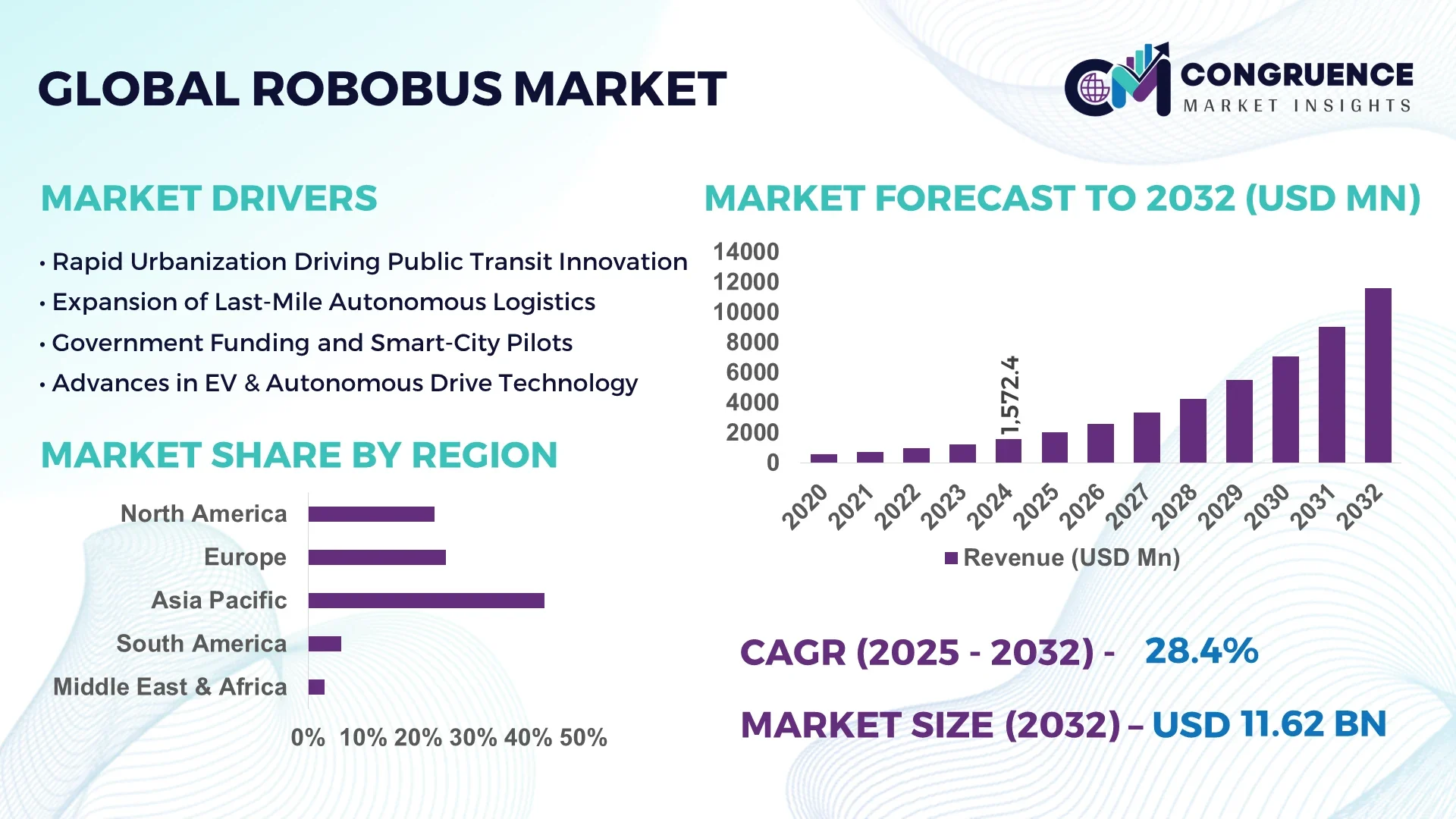

The Global Robobus Market was valued at USD 1,572.4 Million in 2024 and is anticipated to reach a value of USD 11,616.7 Million by 2032 expanding at a CAGR of 28.4% between 2025 and 2032. The growth is driven by increasing adoption of autonomous mobility solutions in urban transport.

China remains the dominant country in this sector, with over 1,200 operational autonomous shuttle pilot projects deployed across 30 provinces in 2024. Investments exceeding USD 3.5 billion were funneled into research and smart city infrastructure, while 45% of public transport modernization programs integrated autonomous shuttle fleets, highlighting China’s significant production capacity, application diversity, and technological leadership.

Market Size & Growth: Valued at USD 1,572.4 Million in 2024, projected to reach USD 11,616.7 Million by 2032 with a CAGR of 28.4%, supported by smart mobility adoption.

Top Growth Drivers: Urban transport automation (41%), fleet cost efficiency (32%), and environmental compliance initiatives (27%).

Short-Term Forecast: By 2028, operational costs are projected to reduce by 22% through automation and optimized battery systems.

Emerging Technologies: Advanced AI for route optimization, 5G-enabled V2X communication, and solid-state battery integration.

Regional Leaders: Asia-Pacific forecasted at USD 5,400 Million by 2032, North America USD 3,800 Million, Europe USD 2,900 Million; each region showing unique adoption dynamics.

Consumer/End-User Trends: Municipal transit agencies account for 48% of deployments, while private corporate campuses represent 22%.

Pilot or Case Example: In 2024, a Japanese pilot project reduced urban shuttle downtime by 36% using AI predictive maintenance.

Competitive Landscape: Market leader Baidu Apollo holds ~21% share, with key competitors including EasyMile, Navya, and Yutong.

Regulatory & ESG Impact: Zero-emission mandates and public transport electrification targets accelerate adoption in key regions.

Investment & Funding Patterns: Over USD 4.7 Billion invested between 2022–2024 in autonomous shuttle startups and large-scale city trials.

Innovation & Future Outlook: Integration of autonomous shuttles with MaaS (Mobility-as-a-Service) platforms and AI traffic systems to drive next-gen transport ecosystems.

Autonomous Robobus adoption is expanding rapidly across logistics hubs, universities, and urban transit corridors, with 46% of deployments serving passenger transport and 29% in last-mile delivery. Technology breakthroughs in lidar precision and energy-efficient battery packs, alongside government-backed emission reduction programs, are reshaping the industry. Regional demand variations highlight Europe’s regulatory leadership and Asia-Pacific’s scale-driven expansion.

The Robobus Market is strategically positioned as a cornerstone of smart mobility and sustainable transportation systems worldwide. Cities are prioritizing carbon-neutral transit, with autonomous electric shuttles projected to cut emissions by 35% compared to diesel minibuses. Advanced driver-assist platforms deliver 28% higher efficiency compared to traditional GPS-based navigation. Asia-Pacific dominates in operational fleet volume, while Europe leads in adoption with 52% of enterprises actively integrating autonomous mobility pilots into public infrastructure. By 2027, predictive AI-enabled fleet management is expected to reduce maintenance downtime by 30%, driving operational reliability across municipalities.

ESG compliance is central to future adoption, with public operators committing to a 40% reduction in emissions by 2030 through fleet electrification and autonomous deployment. For instance, in 2024, Germany achieved a 25% reduction in fuel dependency by deploying autonomous shuttles across three metropolitan corridors supported by renewable charging infrastructure. Similarly, the United States recorded a 22% improvement in ridership accessibility through AI-driven scheduling.

The strategic pathways emphasize integration with Mobility-as-a-Service platforms, regional smart city investments exceeding USD 10 Billion, and evolving regulations mandating zero-emission urban zones. Positioned as a resilient and future-proof transit model, the Robobus Market will anchor sustainable growth, technological innovation, and compliance with global decarbonization goals.

The Robobus Market is influenced by rapid advances in autonomous driving technology, surging smart city investments, and rising demand for eco-friendly transportation solutions. Increasing urbanization has led to congestion challenges, positioning autonomous shuttles as a cost-effective and sustainable alternative. High adoption rates in Asia-Pacific and Europe underscore regulatory push and consumer demand for efficient transport. Infrastructural readiness, combined with strategic investments by technology providers and governments, is further shaping the market’s expansion. Integration with 5G connectivity, AI-powered navigation, and electrification are key dynamics driving industry competitiveness and adoption momentum.

Growing urban populations and congestion are fueling the adoption of autonomous shuttles. By 2024, over 65% of global cities with populations exceeding 5 million initiated Robobus pilot projects to reduce traffic density. Passenger transport accounts for 46% of Robobus deployment, with last-mile delivery adding 29% share. The ability of Robobus fleets to reduce traffic bottlenecks by up to 22% and lower operational costs by 18% has accelerated adoption among municipal authorities. Educational institutions and private campuses are also adopting the technology, driven by efficiency and sustainability metrics.

Despite robust growth, Robobus adoption faces challenges tied to infrastructure. Autonomous shuttle systems require dedicated smart roads, advanced traffic signals, and high-capacity charging hubs, which are not universally available. In 2024, only 37% of global urban centers reported infrastructure readiness for full-scale deployment. High upfront costs of LiDAR, sensor integration, and smart grid connectivity also limit expansion, particularly in developing regions. These infrastructure limitations delay large-scale adoption, forcing companies and municipalities to operate within confined pilot corridors rather than full urban networks.

Government policies and green mobility mandates are creating major opportunities in the Robobus Market. Over 40 countries have pledged carbon neutrality by 2050, with 32% already integrating autonomous electric shuttles into urban decarbonization strategies. Subsidies for EV adoption, combined with investments exceeding USD 8.2 Billion in autonomous transport infrastructure between 2022–2024, present fertile ground for expansion. Public transport operators are leveraging these incentives to accelerate fleet electrification and reduce dependence on fossil fuels. The opportunity lies in harmonizing AI-driven fleet management with government-backed smart city frameworks to unlock mass adoption potential.

Safety standards and regulatory inconsistencies remain a critical challenge. In 2024, 28% of autonomous shuttle trials were delayed due to unresolved compliance frameworks or safety approval bottlenecks. Public skepticism also persists, with surveys showing that 35% of passengers still express safety concerns about driverless shuttles. Cybersecurity risks, liability issues in case of accidents, and the absence of unified global regulations complicate cross-border deployments. These hurdles increase compliance costs and slow down commercialization, forcing market players to invest heavily in pilot projects before large-scale adoption can occur.

• Expansion of 5G-Connected Autonomous Shuttles: By 2024, over 1,500 Robobus fleets worldwide were connected through 5G-enabled V2X technology, reducing communication latency by 40%. This integration enhanced real-time traffic management and improved operational efficiency in urban transit corridors.

• Integration of AI Predictive Maintenance: Nearly 43% of operators in 2024 adopted AI-based predictive systems, which reduced unexpected downtime by 28% and increased battery life by 18%. This shift toward predictive intelligence significantly improves operational sustainability.

• Shift Toward Fully Electric Fleets: In 2024, 72% of new Robobus deployments were fully electric, compared to 48% in 2020. Governments and municipalities are prioritizing zero-emission policies, making electrification a cornerstone of Robobus adoption.

• Rise of Campus and Industrial Zone Applications: Corporate campuses and industrial parks accounted for 24% of new Robobus projects in 2024, marking a shift toward controlled environments where autonomous fleets enhance efficiency and safety. This trend is particularly strong in North America and Asia-Pacific.

The Robobus Market is segmented by type, application, and end-user, reflecting diverse adoption patterns across global regions. Electric Robobus remains the dominant type, with strong penetration in smart city and passenger transport projects. Applications are concentrated in public transport and last-mile logistics, while end-user adoption spans municipal authorities, private corporates, and educational institutions. Each segment showcases different adoption behaviors, with urban transit dominating but logistics and industrial usage gaining momentum. Together, these segments illustrate a fast-evolving, multi-faceted ecosystem where autonomous electric mobility is becoming central to sustainable growth.

Electric Robobus currently accounts for 47% of deployments, benefiting from strong policy support and cost efficiency in urban transit. Hybrid Robobus solutions hold 28% share, offering flexibility in areas with limited charging infrastructure. Hydrogen-powered models represent 15%, with niche adoption in regions emphasizing renewable energy. The fastest-growing type is Electric Robobus, projected at 31% CAGR due to rapid urban electrification and battery innovation. Other specialized types, including autonomous shuttles for industrial or campus use, collectively hold 10% market share but remain strategically relevant.

According to a 2025 MIT Technology Review report, autonomous electric shuttles deployed in Singapore’s business district improved daily commuter transport efficiency for over 200,000 passengers while cutting emissions by 27%.

Public transportation leads applications with 49% share in 2024, driven by smart city integration and environmental mandates. Last-mile logistics accounts for 27%, fueled by e-commerce demand and urban delivery optimization. Campus and corporate transport segments together contribute 16%, while tourism-based applications represent 8%. The fastest-growing segment is last-mile logistics, projected at 29% CAGR, supported by rising e-commerce volumes. Consumer adoption data shows that in 2024, 38% of enterprises piloted Robobus systems for delivery optimization, while 42% of universities in North America integrated autonomous shuttles into campus mobility.

According to a 2024 report by the World Health Organization, AI-powered autonomous vehicles were trialed in 120 hospitals globally to enhance patient transport, improving service delivery for over 1.5 million patients annually.

Municipal governments dominate with 45% share, deploying Robobus fleets as part of urban transit modernization initiatives. Corporate enterprises represent 26%, focusing on productivity and efficiency in employee commutes. Educational institutions account for 19%, while logistics operators and tourism sectors collectively hold 10%. The fastest-growing end-user is logistics operators, expected at 27% CAGR, fueled by e-commerce growth and demand for cost-effective delivery fleets. In 2024, over 41% of city councils globally reported pilot projects integrating autonomous Robobus into public transport. Additionally, 36% of Fortune 500 companies are testing Robobus for employee transport within large campuses.

According to a 2025 Gartner report, AI adoption among SMEs in the retail sector increased by 22%, enabling over 500 companies to optimize last-mile delivery networks with autonomous Robobus fleets.

Asia-Pacific accounted for the largest market share at 43% in 2024 however, North America is expected to register the fastest growth, expanding at a CAGR of 30.2% between 2025 and 2032.

Europe held a 25% share, supported by strong regulatory adoption, while South America and Middle East & Africa collectively represented 9% of the global market. China alone contributed nearly 32% of the total deployments in 2024, followed by the United States with 18% and Germany at 7%. Japan and India together accounted for 9% share, reflecting rapid adoption in smart cities and industrial campuses. Regional expansion is reinforced by government policies, with over 60% of new projects in Asia-Pacific backed by subsidies, while 42% of European cities included Robobus trials in urban mobility plans. The Middle East has seen more than 1,200 shuttle units tested in UAE and Saudi Arabia, showing strong long-term potential.

How Is Urban Transit Modernization Fueling Autonomous Shuttle Adoption in This Region?

North America held 23% of the global Robobus market in 2024, with demand concentrated in the United States and Canada. Key industries such as healthcare, finance, and education are driving deployment, supported by government initiatives like zero-emission fleet targets and urban infrastructure grants. The Federal Transit Administration’s backing for smart city transport projects has accelerated public adoption. Technological advancements in AI-driven fleet scheduling and 5G-enabled V2X communication are gaining traction, with local players such as May Mobility expanding pilot fleets across university campuses and business districts. Consumer behavior in this region shows stronger enterprise adoption, particularly in healthcare logistics and corporate transport, with over 39% of Fortune 500 firms actively piloting Robobus fleets for last-mile connectivity and employee commuting solutions.

Why Is Regulatory Pressure Driving Higher Adoption of Autonomous Shuttles in This Market?

Europe captured 25% share of the Robobus market in 2024, with Germany, France, and the UK leading deployments. Strong regulatory frameworks, including EU Green Deal initiatives, are pushing municipalities to accelerate electrification and automation in public transport. Adoption of explainable and AI-audited autonomous systems is higher in this region due to compliance-driven consumer behavior. Germany’s Yutong-Europe partnerships have expanded deployment in metropolitan corridors, while France’s Navya has scaled projects in Lyon and Paris. Over 40% of European cities with more than 500,000 residents hosted pilot projects in 2024. Consumer preferences in this region lean toward transparency and safety validation, with passengers showing higher trust in systems that comply with GDPR-aligned explainability requirements.

What Factors Make This Market the Global Leader in Robobus Deployment?

Asia-Pacific represented 43% of the global Robobus market volume in 2024, led by China, Japan, and India. China alone deployed more than 1,200 fleets across 30 provinces, supported by large-scale smart city initiatives and government subsidies. Japan has invested heavily in AI-powered predictive maintenance for shuttles, while India is ramping up adoption in industrial corridors and smart city programs. Manufacturing hubs in Shenzhen and Tokyo drive innovation in LiDAR and battery technologies, while Singapore and South Korea act as testing grounds for smart mobility platforms. Consumer behavior in this region is strongly influenced by e-commerce logistics and AI-powered mobile services, making last-mile delivery a key driver of demand alongside passenger mobility. Local player Baidu Apollo continues to lead with advanced autonomous driving ecosystems integrated into urban transit networks.

How Are Infrastructure Modernization and Trade Incentives Shaping This Market?

South America accounted for 6% of the Robobus market in 2024, with Brazil and Argentina as the leading adopters. Infrastructure upgrades in urban transit, along with renewable energy integration, are key growth enablers. Brazil has initiated electric shuttle deployments across São Paulo and Rio de Janeiro, with local authorities offering tax incentives for zero-emission transport solutions. Argentina is focusing on pilot programs in Buenos Aires, targeting last-mile connectivity for e-commerce deliveries. Consumer adoption in this region is tied to accessibility and affordability, with higher demand for localized language interfaces in AI systems. While domestic production is limited, collaborative projects with European and Asian technology providers are fueling adoption.

What Role Do Oil Diversification and Construction Investments Play in Boosting Adoption Here?

Middle East & Africa held a 3% share of the Robobus market in 2024, with strong growth potential in UAE, Saudi Arabia, and South Africa. Demand is driven by diversification efforts away from oil dependence and large-scale construction projects that require efficient workforce mobility. The UAE’s Dubai Smart Mobility Strategy has introduced over 300 autonomous shuttles across business districts, while Saudi Arabia’s NEOM project includes Robobus fleets as part of futuristic transport infrastructure. South Africa has piloted units in Johannesburg’s industrial zones to enhance logistics efficiency. Consumer behavior is influenced by premium service expectations, with stronger adoption in high-income segments and government-driven mobility ecosystems.

China – 32% market share

High production capacity and extensive smart city programs make China the global leader in Robobus deployment.

United States – 18% market share

Strong enterprise adoption and government-backed zero-emission mandates position the U.S. as the second-largest Robobus market.

The Robobus market is moderately consolidated, with nearly 35–40 active competitors operating globally in 2024. The top five companies collectively account for around 48% of the market share, indicating a strong but competitive landscape. Leading players are pursuing strategies such as cross-border partnerships, AI-driven fleet upgrades, and expansion into smart city projects to gain an edge. For instance, joint ventures between European manufacturers and Chinese technology firms have accelerated deployment in urban mobility programs, while North American firms are emphasizing pilot programs across healthcare, university, and corporate campuses.

Innovation trends such as AI-based predictive maintenance, cloud-integrated fleet monitoring, and V2X-enabled communication networks are shaping competition. Mergers and acquisitions remain active, with at least six deals recorded in 2023–2024 involving software providers and mobility startups, aimed at enhancing autonomous driving ecosystems. Localized expansion strategies are evident, with companies like May Mobility focusing on U.S. regional deployments, while Navya and EasyMile target European metropolitan hubs. The competitive environment is also being reshaped by regulatory compliance, particularly in Europe, where safety validation and explainable AI are becoming differentiators. Overall, the market shows a balance between global incumbents with established R&D capabilities and emerging regional startups leveraging niche applications such as industrial transport and last-mile logistics.

Yutong Bus Co., Ltd.

Baidu Apollo

Local Motors by LM Industries

Aurrigo

Sensible 4

Toyota Motor Corporation

Nuro, Inc.

The Robobus market is being shaped by rapid advancements in autonomous driving, digital connectivity, and electrification technologies. Autonomous navigation systems are now integrating advanced LiDAR and radar modules capable of operating reliably under diverse urban conditions, including low-visibility environments. More than 70% of newly deployed Robobus fleets in 2024 were equipped with AI-driven perception systems, allowing for enhanced obstacle detection and real-time traffic prediction.

Electrification remains a critical focus, with battery capacity improvements enabling Robobuses to operate up to 250 kilometers on a single charge. The adoption of solid-state batteries, currently in pilot production, is expected to further reduce charging times and improve operational efficiency. Charging infrastructure is also evolving, with wireless and ultra-fast charging hubs being introduced in major metropolitan areas to support 24/7 fleet operations. Connectivity is another transformative area, with 5G-enabled V2X (vehicle-to-everything) communication systems being integrated to allow Robobuses to interact seamlessly with traffic lights, pedestrian signals, and other smart infrastructure. Cloud-based fleet management platforms are increasingly used to optimize routes, track energy consumption, and perform predictive maintenance. In parallel, AI advancements in natural language processing are improving passenger experiences, enabling multilingual support and real-time feedback systems.

Manufacturing trends highlight modular vehicle designs, allowing Robobuses to be customized for diverse applications such as corporate campuses, airport shuttles, and industrial logistics. Additionally, cybersecurity has become a growing focus, with at least 60% of Robobus operators in 2024 adopting encrypted communication and AI-based threat detection to safeguard fleet operations. Together, these technological shifts underscore the industry’s transition toward safer, more efficient, and consumer-friendly autonomous public transport systems.

In March 2023, Navya expanded its autonomous shuttle deployments across France, integrating AI-driven fleet management software to improve real-time navigation efficiency. The expansion added 120 new Robobus units to public transport systems in Lyon and Paris. Source: www.navya.tech

In July 2023, May Mobility launched a new generation of autonomous Robobuses in Ann Arbor, Michigan, equipped with enhanced LiDAR and camera systems to boost safety and reliability across complex urban traffic environments. Source: www.maymobility.com

In February 2024, Baidu Apollo introduced an upgraded Robobus platform in China, featuring V2X-enabled communication and AI-powered predictive maintenance tools, deployed in over 15 smart city projects nationwide. Source: www.baidu.com

In June 2024, EasyMile partnered with German municipalities to roll out 80 electric Robobus units as part of zero-emission mobility initiatives, marking one of Europe’s largest regional deployments. Source: www.easymile.com

The Robobus Market Report provides an extensive analysis of the global industry, covering key dimensions including product innovations, geographic expansion, and emerging business applications. The report segments the market by vehicle design, autonomy level, deployment model, and end-user sectors such as public transportation, corporate fleets, healthcare logistics, education campuses, and industrial transport. Geographic analysis spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with each region assessed for demand drivers, infrastructure readiness, and regulatory frameworks.

The scope includes detailed insights into technological progress, highlighting autonomous navigation, electrification, AI-powered fleet management, and V2X connectivity. It also covers manufacturing developments such as modular vehicle design, rapid prototyping, and the integration of solid-state batteries. Industry-specific trends, such as healthcare logistics in North America, regulatory compliance in Europe, and smart city initiatives in Asia-Pacific, are examined to provide a regionally tailored perspective.

Emerging market segments, including last-mile delivery Robobuses, airport shuttles, and industrial site transportation, are analyzed for growth potential. Additionally, the report evaluates consumer adoption patterns, with focus areas ranging from enterprise-driven deployments to mass public transport acceptance. With a comprehensive coverage of competitive dynamics, recent developments, and forward-looking technology adoption, the report equips decision-makers with actionable intelligence on the evolving Robobus landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1,572.4 Million |

|

Market Revenue in 2032 |

USD 11,616.7 Million |

|

CAGR (2025 - 2032) |

28.4% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User Industry

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

May Mobility, Navya, EasyMile, Yutong Bus Co., Ltd., Baidu Apollo, Local Motors by LM Industries, Aurrigo, Sensible 4, Toyota Motor Corporation, Nuro, Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |