Reports

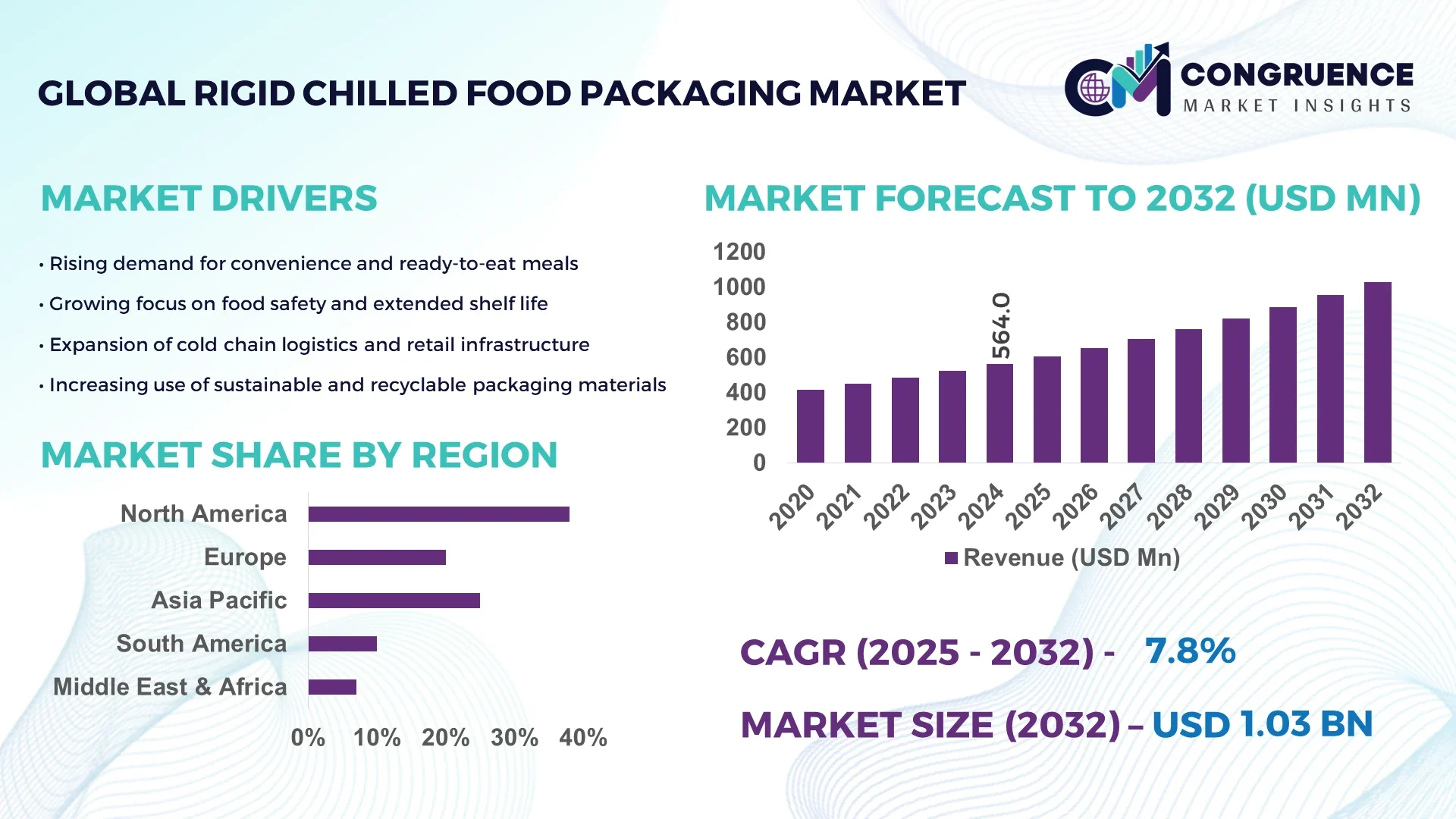

The Global Rigid Chilled Food Packaging Market was valued at USD 564 Million in 2024 and is anticipated to reach a value of USD 1,028.55 Million by 2032 expanding at a CAGR of 7.8% between 2025 and 2032. The market growth is primarily driven by the rising demand for extended shelf-life products and sustainable packaging formats in the chilled food sector.

In 2024, the United States dominated the global Rigid Chilled Food Packaging market owing to its extensive cold chain infrastructure and advanced packaging technologies. The country hosts more than 1,200 large-scale chilled food processing units and has witnessed over USD 1.4 billion invested in packaging automation and material innovation between 2022 and 2024. With approximately 72% consumer adoption of ready-to-eat chilled foods, U.S. manufacturers are increasingly leveraging recyclable PET and PP containers integrated with oxygen barrier technologies to enhance food preservation and reduce material waste.

Market Size & Growth: Valued at USD 564 Million in 2024, projected to reach USD 1,028.55 Million by 2032, expanding at a CAGR of 7.8% driven by increasing demand for sustainable and high-barrier chilled packaging solutions across food distribution networks.

Top Growth Drivers: 68% surge in recyclable material adoption, 42% efficiency improvement in cold chain logistics, and 39% rise in demand for extended-shelf-life packaging formats.

Short-Term Forecast: By 2028, operational packaging costs are expected to decline by 18% through adoption of lightweight rigid plastics and thermoforming automation.

Emerging Technologies: Smart temperature indicators, antimicrobial coatings, and vacuum-sealed rigid polymer containers are gaining traction for improved food safety and shelf management.

Regional Leaders: North America (USD 415 Million by 2032) leading with smart packaging integration; Europe (USD 326 Million) emphasizing circular packaging; Asia-Pacific (USD 287 Million) witnessing rapid growth in processed chilled meals.

Consumer/End-User Trends: Strong adoption among supermarket chains, meal kit providers, and online grocery platforms, with increasing preference for eco-friendly rigid containers.

Pilot or Case Example: In 2024, Amcor implemented a recyclable PET rigid tray solution reducing product spoilage by 27% and downtime by 15% in chilled dairy logistics.

Competitive Landscape: Amcor plc leads with an estimated 17% market share, followed by Sealed Air Corporation, Sonoco Products Company, Berry Global Inc., and Faerch Group.

Regulatory & ESG Impact: Strict compliance with FDA and EU food-contact regulations, coupled with government incentives promoting low-carbon packaging solutions.

Investment & Funding Patterns: Over USD 650 million invested globally in chilled packaging automation and material R&D from 2022 to 2024, highlighting venture capital interest in sustainable packaging start-ups.

Innovation & Future Outlook: The industry is shifting toward mono-material rigid packaging, recyclable PP solutions, and integration of IoT-enabled freshness tracking for enhanced transparency and traceability.

The Rigid Chilled Food Packaging market is witnessing strong momentum across sectors such as ready-to-eat meals, dairy, meat, and seafood packaging, accounting for more than 70% of demand in 2024. Ongoing innovation in recyclable plastics, barrier coatings, and active packaging systems is transforming the market landscape. Regulatory emphasis on circular economy practices and environmental compliance is accelerating the use of low-carbon materials. Rising consumption of chilled convenience foods in urban areas, coupled with advancements in packaging automation and supply chain monitoring, positions the industry for sustained growth through 2032.

The strategic relevance of the Rigid Chilled Food Packaging Market lies in its critical role within the global cold chain ecosystem, supporting food safety, shelf-life extension, and sustainability mandates. As chilled food demand continues to rise—up by 31% globally between 2020 and 2024—manufacturers are prioritizing packaging innovations that deliver both environmental compliance and operational efficiency. Advanced thermoformed PET solutions deliver 28% improvement in barrier performance compared to conventional polystyrene containers, reducing spoilage and maintaining product freshness during extended distribution cycles.

Regionally, North America dominates in production volume, while Europe leads in adoption with 64% of enterprises integrating recyclable rigid packaging materials into their chilled food lines. By 2027, automation and AI-enabled packaging quality control are expected to cut operational inspection time by 35%, boosting throughput and traceability. Firms are committing to ESG improvements such as 45% packaging material recycling by 2030 in alignment with global sustainability frameworks.

In 2024, Amcor implemented AI-based thermoforming optimization in the U.K., achieving a 19% energy reduction through real-time production control. As digitization, data-driven sustainability tracking, and low-carbon polymers reshape the supply chain, the Rigid Chilled Food Packaging Market stands as a pillar of resilience, compliance, and sustainable industrial growth across food manufacturing and logistics ecosystems.

The accelerating transition toward sustainable packaging materials is a key driver in the Rigid Chilled Food Packaging Market. Consumers are increasingly preferring eco-friendly chilled food packaging, with 67% of European buyers favoring recyclable rigid plastics over traditional multi-layer composites. Manufacturers are responding with high-performance mono-material designs that cut plastic use by up to 22% while maintaining durability. Additionally, the implementation of food-grade recycled PET and polypropylene is driving product development, aligning with regulatory targets for circular economy compliance. Continuous improvements in material transparency and shelf-life preservation are enhancing brand value and consumer trust, positioning sustainability as a major competitive differentiator across global markets.

Volatile raw material prices, particularly for PET, HDPE, and PP resins, remain a significant restraint for the Rigid Chilled Food Packaging Market. Between 2022 and 2024, polymer price fluctuations exceeded 30% in key markets, leading to unpredictable production costs and delayed procurement cycles. These fluctuations disrupt long-term supply contracts and margin stability, especially for small and mid-sized converters. Furthermore, the energy-intensive nature of rigid packaging production amplifies cost pressures amid increasing global electricity rates. Companies are investing in local sourcing strategies and advanced recycling systems to mitigate price instability; however, dependence on imported resin and limited regional refining capacity continue to constrain consistent cost optimization.

Rapid advancements in digital manufacturing and material engineering present significant opportunities for the Rigid Chilled Food Packaging Market. The integration of automated thermoforming, IoT-enabled quality sensors, and bio-based polymers is projected to increase production efficiency by 26% within the next five years. Smart packaging technologies that monitor temperature and freshness in real time are gaining adoption among premium chilled food producers, enhancing consumer confidence and reducing wastage. Emerging opportunities also stem from partnerships between packaging manufacturers and food logistics companies to deploy recyclable rigid trays designed for returnable systems. As major brands commit to carbon-neutral packaging by 2035, innovation in lightweight rigid materials and energy-efficient molding solutions will unlock new growth pathways across regions.

The Rigid Chilled Food Packaging Market faces growing challenges due to stringent environmental regulations and limited recycling infrastructure. The enforcement of Extended Producer Responsibility (EPR) frameworks across Europe and Asia requires producers to recover or recycle up to 50% of their packaging waste by 2030, placing pressure on existing operations. Inadequate sorting facilities and inconsistent recycling standards reduce the recovery rate of rigid plastics, which currently averages only 29% globally. Furthermore, compliance costs related to traceability labeling and material certification increase operational burdens. These constraints compel manufacturers to accelerate R&D in mono-materials and closed-loop systems while balancing regulatory compliance, cost efficiency, and market competitiveness.

• Integration of Smart and Connected Packaging Solutions: The market is experiencing accelerated adoption of intelligent packaging technologies that enhance food quality monitoring and traceability. Approximately 48% of chilled food producers have implemented smart sensors or freshness indicators in rigid containers to track temperature variations and spoilage rates. By 2026, the use of connected packaging is expected to increase efficiency in cold chain monitoring by 32%, improving transparency for consumers and retailers alike. This trend reflects the growing intersection of IoT and food safety within the packaging ecosystem.

• Adoption of High-Barrier and Recyclable Polymer Materials: Manufacturers are increasingly shifting toward recyclable PET, PP, and bio-based polymers to address sustainability targets. Over 62% of new rigid chilled packaging designs in 2024 utilized mono-material or recyclable compositions compared to 44% in 2022. These materials offer a 29% improvement in gas barrier efficiency and a 21% reduction in food spoilage incidents. As environmental compliance intensifies, companies are investing in R&D to enhance the performance and recyclability of rigid polymers for chilled applications.

• Automation and Digital Manufacturing Expansion: Automation has become a core focus for production scalability and cost optimization in the Rigid Chilled Food Packaging Market. In 2024, nearly 58% of global rigid packaging lines integrated robotic handling or AI-based inspection systems, reducing production downtime by 17% and defect rates by 23%. Digital manufacturing technologies are driving greater customization flexibility while lowering waste output. The trend underscores the industry’s commitment to precision-driven, energy-efficient packaging systems that support large-scale chilled food logistics.

• Shift Toward Lightweight Rigid Packaging Formats: Lightweight rigid formats are gaining traction as manufacturers aim to minimize transportation costs and material use. Between 2021 and 2024, the average material thickness of rigid chilled food containers declined by 18%, translating to a 14% reduction in overall logistics weight. These formats maintain durability while enhancing recyclability and reducing carbon emissions per shipment. The adoption of lightweight packaging is particularly strong in Asia-Pacific, where demand for cost-effective and eco-conscious chilled packaging has risen by 41% over the last three years.

The Rigid Chilled Food Packaging Market is segmented based on type, application, and end-user, each reflecting distinct growth dynamics shaped by material innovation, consumption behavior, and packaging design advancements. Among these, rigid plastics and paper-based composites dominate in type segmentation due to their superior performance in temperature retention and durability. In applications, dairy and ready-to-eat meal packaging remain the most prominent, driven by a sharp rise in chilled food consumption across urban markets. End-user segmentation highlights food manufacturers and retail distributors as primary adopters, collectively accounting for over 70% of the global demand. The increasing shift toward sustainable packaging, automated production processes, and compliance with food safety regulations continues to redefine product differentiation and strategic positioning across these segments.

Rigid plastics, including PET and polypropylene-based containers, currently account for 46% of total adoption in the Rigid Chilled Food Packaging Market, supported by their balance of recyclability and high-barrier protection. This segment leads the market due to its broad compatibility with chilled dairy, meat, and ready-meal products. Paperboard-based rigid packaging holds around 27% share, appealing to sustainability-focused brands seeking fiber-based alternatives with lower carbon footprints. Meanwhile, metal and glass containers represent 17% combined, primarily used in premium chilled food segments requiring extended preservation. Biopolymer rigid packaging is emerging as the fastest-growing type, expanding at an estimated CAGR of 9.1% due to regulatory incentives favoring biodegradable solutions. These materials provide up to 35% improvement in compostability compared to conventional plastics, enhancing circular economy compliance.

Dairy product packaging represents the leading application in the Rigid Chilled Food Packaging Market, accounting for approximately 39% of total usage in 2024. This dominance is attributed to the high perishability of dairy goods and the need for temperature-stable packaging that maintains integrity throughout transport and storage. Ready-to-eat (RTE) meal packaging follows with a 33% share, driven by rising urbanization and demand for convenience-oriented chilled food options. Meat, poultry, and seafood packaging collectively hold a 21% share, while fruits and vegetable packaging accounts for the remaining 7%. Ready-meal packaging is the fastest-growing application, projected to expand at a CAGR of 8.4% through 2032, supported by e-commerce-driven grocery distribution and sustainable tray innovation.

Food and beverage manufacturers are the leading end-users in the Rigid Chilled Food Packaging Market, accounting for roughly 44% of demand in 2024. Their dominance stems from widespread adoption of recyclable rigid containers across dairy, ready meals, and frozen segments to meet both efficiency and sustainability mandates. Retail distributors and supermarkets hold 31% of market participation, emphasizing standardized packaging for inventory management and product display efficiency. Meanwhile, food service providers and meal kit companies contribute a combined 25%, with adoption accelerating as these players integrate lightweight and customized rigid packaging for delivery operations. The fastest-growing end-user category is the online food delivery sector, expanding at a CAGR of 10.2% owing to rapid growth in chilled meal logistics and temperature-controlled e-commerce solutions.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.9% between 2025 and 2032.

Europe followed closely with a 31% share, driven by sustainability legislation and rigid plastic recycling mandates. South America represented 12% of the market, while the Middle East & Africa together contributed approximately 9%. The regional distribution highlights strong demand for recyclable rigid packaging materials and temperature-stable containers across developed economies. Rising cold chain infrastructure investments, exceeding USD 3.2 billion globally in 2024, along with technological automation in packaging production, continue to accelerate market expansion. Increasing regional diversification, government-driven sustainability goals, and localized packaging innovation clusters are reinforcing the global competitiveness of the Rigid Chilled Food Packaging Market.

North America held a 38% share of the Rigid Chilled Food Packaging Market in 2024, driven by robust cold chain infrastructure and a mature food manufacturing base across the United States and Canada. Key industries fueling demand include dairy, ready-to-eat meals, and frozen foods, with over 67% of regional producers adopting recyclable PET containers. The U.S. government’s emphasis on circular packaging and low-carbon production is accelerating the shift toward lightweight rigid plastics and digitalized production lines. Technological adoption—particularly automation and AI-enabled inspection—has increased production efficiency by 25% across major packaging facilities. Amcor’s North American unit launched AI-integrated sealing systems in 2024 to reduce material waste by 15%. Consumers in this region display a strong preference for eco-labeled, durable chilled packaging, with 72% favoring recyclable rigid containers for meal kits and fresh food purchases.

Europe accounted for a 31% share of the Rigid Chilled Food Packaging Market in 2024, with leading markets including Germany, the UK, and France. The region remains at the forefront of sustainability initiatives such as the EU Packaging and Packaging Waste Regulation (PPWR), which targets 55% recyclability by 2030. Over 60% of chilled food producers in Europe now use mono-material rigid packaging formats designed for easier recovery. Germany leads in advanced thermoforming lines, while the UK has emerged as a pioneer in fiber-based rigid tray development. Danish packaging manufacturer Faerch introduced a 100% post-consumer recycled PET solution in 2024, setting a new sustainability benchmark. European consumers demonstrate strong eco-conscious behavior, with 68% indicating they would switch brands for recyclable chilled packaging.

Asia-Pacific ranked second globally with a 26% market volume in 2024 and is expected to witness the fastest expansion through 2032. China, India, and Japan collectively accounted for 78% of the region’s chilled packaging consumption, supported by rapid industrialization and e-commerce growth. Manufacturing modernization has increased automation penetration by 36% since 2021, with localized R&D hubs in Japan and South Korea focusing on lightweight, recyclable rigid containers. In 2024, a major Indian packaging producer invested in bio-based rigid plastics for dairy products, reducing energy consumption by 19%. Consumer behavior in Asia-Pacific is shaped by convenience and affordability—65% of urban consumers prefer pre-packaged chilled meals. Digital traceability platforms and sustainability certification programs are also gaining traction, enabling transparency across regional supply chains.

South America contributed approximately 12% to the Rigid Chilled Food Packaging Market in 2024, with Brazil and Argentina emerging as primary contributors. The region’s growing processed food export sector, valued at over USD 28 billion in 2024, continues to boost chilled packaging requirements. Government programs promoting local material production and trade liberalization have supported market expansion, while regional recycling infrastructure investment increased by 31% between 2021 and 2024. Brazilian packaging firms are focusing on rigid PET tray innovation to improve shelf stability and reduce waste. Regional consumers prioritize affordability, but sustainability awareness is climbing, with 47% now opting for recyclable chilled packaging formats in retail. Increasing collaborations between local producers and multinational packaging firms are driving modernization in material sourcing and design optimization.

The Middle East & Africa accounted for 9% of the Rigid Chilled Food Packaging Market in 2024, led by the UAE, Saudi Arabia, and South Africa. Rapid urbanization and diversification in food processing industries are propelling demand for temperature-controlled packaging solutions. The UAE’s Smart Industry Strategy 2031 and Saudi Arabia’s Vision 2030 initiatives are fostering local production of recyclable rigid packaging materials. South Africa’s adoption of biodegradable rigid polymers grew by 24% in 2024, reflecting strong ESG-driven innovation. A UAE-based packaging company recently launched solar-powered thermoforming plants, reducing carbon emissions by 18%. Regional consumers are showing a growing inclination toward premium chilled foods, with 53% preferring rigid packaging formats that ensure longer shelf stability and tamper resistance.

United States – 27% Market Share: Driven by advanced automation in packaging plants, strong cold chain infrastructure, and high consumer demand for recyclable chilled food packaging.

Germany – 18% Market Share: Supported by stringent EU sustainability mandates, mature packaging R&D facilities, and large-scale adoption of post-consumer recycled PET rigid containers across food manufacturing sectors.

The global Rigid Chilled Food Packaging market is characterized by a moderately consolidated competitive landscape, with the top five companies collectively accounting for approximately 46% of total market share in 2024. Around 120 active participants operate globally, including large multinational packaging manufacturers and regional players specializing in polymer, metal, and bioplastic-based packaging solutions. Competitive intensity remains high due to the growing focus on sustainability, recyclable materials, and automation in packaging production. Strategic collaborations and product innovations are shaping market dynamics, with over 35 new product launches recorded between 2023 and 2024 emphasizing lightweight rigid trays and temperature-stable polymers. Mergers and acquisitions increased by nearly 18% year-over-year, with several leading firms expanding their cold-chain packaging capabilities to enhance freshness retention and shelf-life performance.

Technological advancement remains a defining factor, as approximately 42% of market players have adopted digital manufacturing systems, including IoT-enabled molding and AI-driven inspection technologies, to reduce waste and improve operational efficiency. Players in North America and Europe maintain strong dominance, while Asia-Pacific firms continue to gain share through cost-efficient production and scalable export capacities.

Overall, competition is driven by innovation, recyclability mandates, and regional customization strategies aimed at addressing shifting consumer demand for sustainable and durable chilled food packaging materials.

DS Smith Plc

Faerch A/S

Huhtamäki Oyj

Sabert Corporation

Sonoco Products Company

Winpak Ltd.

Anchor Packaging LLC

Linpac Packaging Limited

Pactiv Evergreen Inc.

Greiner Packaging International GmbH

Coveris Holdings S.A.

Plastipak Holdings, Inc.

Technological advancement is reshaping the Rigid Chilled Food Packaging market, with automation, digitalization, and material innovation emerging as core drivers of operational efficiency and sustainability. As of 2024, nearly 48% of manufacturers have implemented automated thermoforming and molding systems to achieve uniform product quality and minimize wastage. These systems enhance productivity by approximately 22%, allowing faster turnaround times and better process consistency across global manufacturing plants. The integration of smart packaging technologies, including embedded temperature indicators and RFID-enabled tracking, is growing rapidly, especially in frozen and chilled food logistics. Around 31% of newly developed rigid packaging formats now include real-time freshness sensors or QR-based traceability features that provide product lifecycle transparency to retailers and consumers. Such innovation supports food safety compliance and reduces spoilage rates by an estimated 15–18% across cold-chain networks.

Sustainability continues to guide R&D investments, with bio-based polymers and recyclable PET structures replacing traditional rigid plastics in more than 40% of new packaging lines launched in 2024. Advanced material processing technologies such as vacuum sealing and co-extrusion have improved insulation properties while maintaining structural rigidity. Additionally, digital twins and predictive maintenance tools are being integrated into packaging production systems, allowing manufacturers to optimize machine performance, forecast equipment failures, and reduce downtime by nearly 25%. Collectively, these technologies are enabling the global Rigid Chilled Food Packaging market to evolve toward high-efficiency, traceable, and environmentally resilient operations.

The Rigid Chilled Food Packaging Market Report offers a comprehensive evaluation of the industry landscape, encompassing structural materials, manufacturing processes, and application-based demand dynamics across global and regional markets. It provides coverage of key packaging formats such as trays, containers, cups, and tubs used predominantly in ready meals, dairy, and frozen food applications, which together account for over 68% of market usage.

Geographically, the report spans five major regions—North America, Europe, Asia-Pacific, South America, and the Middle East & Africa—analyzing region-specific trends such as technological adoption, sustainability mandates, and consumer-driven packaging transformations. North America currently holds approximately 34% of the global share due to its advanced cold chain infrastructure, while Asia-Pacific is witnessing a notable rise in consumption volumes exceeding 22 million tons annually, driven by urbanization and expanding retail networks.

The scope also includes in-depth segmentation by end-user industries such as food processing, retail, and catering, collectively contributing over 80% of total demand. Furthermore, the report explores emerging technologies like intelligent packaging, biodegradable rigid polymers, and digital labeling systems reshaping the industry’s operational and sustainability paradigms. This comprehensive coverage positions the report as an essential analytical tool for strategic planning, investment assessment, and competitive benchmarking across all key dimensions of the global rigid chilled food packaging ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 564 Million |

Market Revenue in 2032 | USD 1028.55 Million |

CAGR (2025 - 2032) | 7.8% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Amcor plc, Berry Global Group, Inc., Sealed Air Corporation, DS Smith Plc, Faerch A/S, Huhtamäki Oyj, Sabert Corporation, Sonoco Products Company, Winpak Ltd., Anchor Packaging LLC, Linpac Packaging Limited, Pactiv Evergreen Inc., Greiner Packaging International GmbH, Coveris Holdings S.A., Plastipak Holdings, Inc. |

Customization & Pricing | Available on Request (10% Customization is Free) |