Reports

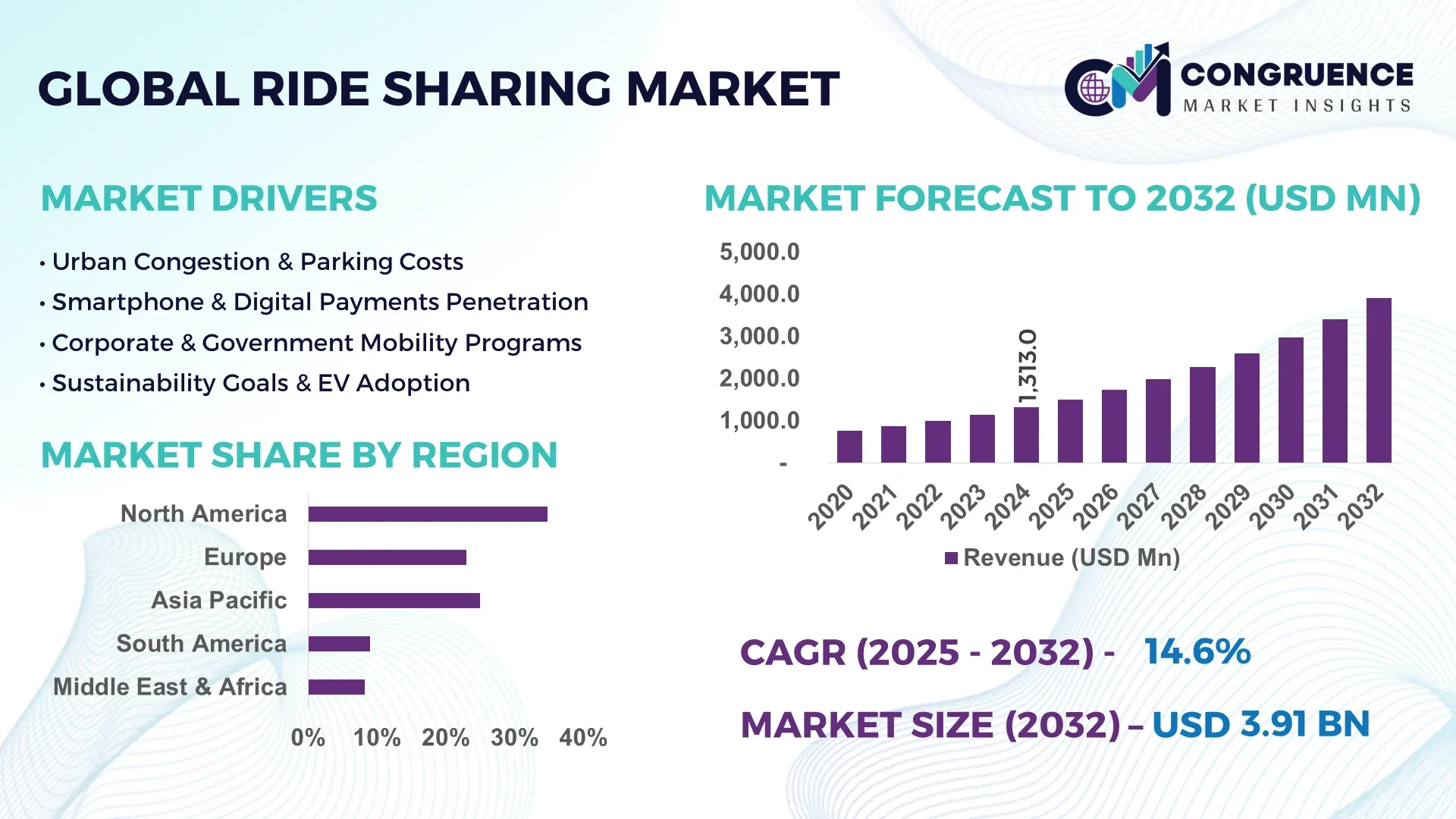

The Global Ride Sharing Market was valued at USD 1,313.0 Million in 2024 and is anticipated to reach a value of USD 3,911.5 Million by 2032 expanding at a CAGR of 14.62% between 2025 and 2032.

The United States remains the leading nation in the Ride Sharing Market, bolstered by high investment levels in autonomous mobility infrastructure, robust software development capacity, and expansive ride-hailing networks. The country is also home to some of the largest telematics and AI mobility platforms, enabling enhanced route optimization, fleet management, and ride allocation systems in major metropolitan areas. These technological advancements and sustained venture capital inflow continue to strengthen the country’s position within the global landscape.

The Ride Sharing Market continues to evolve rapidly due to technological convergence, urban mobility shifts, and rising environmental consciousness. Key industry sectors contributing to market activity include transportation-as-a-service (TaaS), micro-mobility, and corporate commuting solutions. Emerging innovations such as autonomous vehicle integration, electric vehicle (EV)-based fleet deployment, and multi-modal mobility platforms are reshaping user engagement and service delivery models. Regulatory drivers, particularly those favoring emissions reductions and congestion mitigation in urban environments, are supporting adoption in Asia-Pacific and European cities. Additionally, economic considerations, including cost-saving preferences among younger demographics and declining car ownership trends, have boosted market penetration. Regional variations also play a critical role, with North America prioritizing AI-based service optimization, while Asia-Pacific demonstrates strong growth in app-based carpooling and scooter-sharing services. Looking ahead, the market is set to benefit from connected vehicle ecosystems, dynamic pricing algorithms, and integration with public transit networks, enabling a more seamless urban mobility experience. The continued fusion of smart city initiatives and next-gen transport systems positions the Ride Sharing Market for transformative growth.

AI is playing a pivotal role in transforming the Ride Sharing Market by optimizing operations, enhancing rider and driver experiences, and supporting sustainable mobility strategies. AI algorithms enable real-time dynamic pricing, predictive demand forecasting, and hyper-efficient routing—significantly reducing idle time and fuel consumption for fleet operators. For instance, AI-based route planning systems have cut average wait times by up to 25% in major metropolitan areas, enabling quicker passenger pickups and lower operational overhead. Driver performance monitoring, powered by AI, leverages telematics data to improve safety by providing in-app coaching and identifying risky behavior, contributing to a reported 30% reduction in accident claims among AI-assisted fleets.

Additionally, customer service is being revolutionized through intelligent chatbots that address inquiries in multiple languages and resolve complaints faster, enhancing brand loyalty and engagement. AI also plays a central role in fleet asset management, analyzing usage patterns and recommending predictive maintenance schedules, thereby extending vehicle lifecycles. Furthermore, AI is being employed in fraud detection systems that monitor transaction anomalies and suspicious rider behavior, reducing financial risks. As ride-sharing platforms increasingly integrate autonomous vehicles, AI continues to serve as the underlying architecture enabling perception, navigation, and decision-making processes—fundamentally reshaping the future of urban mobility within the Ride Sharing Market.

“In April 2025, a leading ride-sharing company implemented an AI-powered driver assignment algorithm that reduced average passenger wait times by 18% across 50 major cities, while improving overall fleet efficiency by 21% through optimized vehicle dispatching and predictive traffic management.”

The Ride Sharing Market is being reshaped by a combination of technological innovations, evolving urban mobility preferences, and supportive regulatory frameworks. Rapid urbanization, coupled with increasing smartphone penetration, has made on-demand transportation more accessible and affordable for millions globally. Governments are progressively promoting shared mobility to curb traffic congestion and reduce carbon emissions, driving policy-level changes that favor ride-sharing operators. Market trends point toward the integration of electric vehicles and autonomous driving technologies, further enhancing service efficiency and environmental compliance. Meanwhile, rising data-driven insights allow providers to fine-tune services according to regional and consumer-specific demand. As the market matures, both traditional and new entrants are focusing on platform enhancements, fleet diversification, and strategic partnerships to strengthen their competitive positions in the Ride Sharing Market.

The increasing pace of urbanization has intensified the demand for efficient, cost-effective, and sustainable mobility solutions. Ride sharing has emerged as a viable response, particularly under the broader framework of Mobility-as-a-Service (MaaS). As urban centers grapple with congestion, limited parking, and environmental concerns, ride-sharing platforms are enabling citizens to forgo car ownership in favor of accessible, app-based transport. In cities like New Delhi, São Paulo, and London, the adoption of integrated ride sharing systems has risen by over 35% in the past three years, fueled by improved digital infrastructure and smart city initiatives. The convergence of multiple transit options—bike sharing, carpooling, on-demand taxis—within single platforms reflects a strategic industry push toward seamless, multimodal mobility. This trend not only diversifies revenue streams for providers but also enhances commuter flexibility and satisfaction.

Despite its growth trajectory, the Ride Sharing Market faces regulatory hurdles across multiple jurisdictions. Varying legal frameworks for licensing, insurance, and labor classification continue to present operational complexity and increased compliance costs. For example, recent mandates in parts of the EU require platform workers to be classified as employees, significantly affecting cost structures and prompting business model realignments. Additionally, local government interventions such as ride quotas, operational zone restrictions, and dynamic tolling policies pose barriers to scale. Navigating this fragmented regulatory landscape demands ongoing legal counsel, adaptive technology systems, and significant administrative overhead—factors that disproportionately impact smaller or emerging players in the market. These restrictions can delay market entry, limit innovation, and increase the financial burden on operators.

Electrification and automation represent substantial opportunities for the Ride Sharing Market. Major industry stakeholders are investing in electric vehicle (EV) infrastructure and pilot autonomous ride-hailing services. This shift is driven by environmental regulations and lower total cost of ownership for EVs. Cities like Oslo and San Francisco are piloting zero-emission ride sharing zones, backed by public-private partnerships and clean energy incentives. Simultaneously, autonomous fleet deployments in test environments have shown promising safety and operational outcomes. Investment in AI and LiDAR technologies has enabled vehicles to perform complex navigation tasks, laying the groundwork for scalable autonomous mobility. These advancements, combined with evolving consumer acceptance, offer long-term potential to reduce labor costs, optimize fleet utilization, and meet global sustainability targets.

As ride-sharing platforms collect and process vast volumes of user data—from geolocation and payment credentials to behavioral analytics—ensuring data security and user privacy has become a critical challenge. The market has witnessed several instances of data breaches leading to reputational and financial damages. With the increasing integration of AI, IoT, and vehicle telematics, the attack surface for cyber threats continues to expand. In 2024, cybersecurity expenditures in the transportation tech sector rose by 22%, reflecting heightened risk mitigation efforts. Complying with GDPR, CCPA, and emerging regional data laws necessitates robust encryption, access control systems, and regular audits. Failure to maintain data integrity not only undermines consumer trust but also attracts legal penalties and deters platform adoption, especially in heavily regulated markets.

Rise of Autonomous Vehicle Integration: Autonomous technology integration is reshaping the Ride Sharing Market, with major players conducting large-scale pilot programs across urban centers in the U.S., Europe, and Asia. In 2025, more than 3,000 self-driving ride-sharing vehicles were operational in controlled city environments, reducing human dependency and increasing operational consistency. These vehicles are equipped with advanced AI and sensor fusion systems, enabling real-time decision-making, lane management, and collision avoidance. This trend is anticipated to reduce long-term labor costs and create scalable 24/7 service models.

Surge in Subscription-Based Ride Sharing Models: Subscription-based ride sharing is gaining traction, offering users fixed-rate packages for daily or weekly commuting. In 2024–25, over 15% of urban users in key North American and European cities opted for subscription rides over pay-per-use models, reflecting a shift toward convenience and predictable budgeting. These services often bundle perks like premium vehicle access, priority pickups, and carbon-offset credits—enhancing customer retention and loyalty in competitive urban markets.

Expansion into Rural and Tier-2 Markets: The Ride Sharing Market is expanding beyond dense urban areas into rural and Tier-2 markets, especially across Asia-Pacific and Latin America. Companies are launching lightweight, low-cost ride sharing apps compatible with basic smartphones and integrating local languages and payment methods. These efforts have led to a 28% rise in ride volumes across non-metropolitan regions within one year, demonstrating the viability and profitability of market diversification strategies.

Integration with Public Transit Ecosystems: Ride sharing platforms are increasingly partnering with public transportation systems to offer first-mile/last-mile connectivity. Real-time integration with bus and train schedules, combined with unified fare payment systems, is improving commuter convenience and expanding user bases. In 2025, several cities implemented municipal co-branded apps allowing users to plan and pay for mixed-mode journeys, fostering a collaborative mobility ecosystem that benefits both public and private transport providers.

The Ride Sharing Market is segmented across multiple parameters, including type, application, and end-user categories, offering critical insights into industry operations and demand dynamics. The segmentation by type includes models such as car sharing, e-hailing, car rental, and station-based mobility, each serving different service delivery frameworks. Application-wise, ride sharing is used extensively across intra-city travel, intercity commuting, airport transportation, and corporate travel. End-user segmentation spans individuals, enterprises, government bodies, and educational institutions. These divisions reflect the market's adaptability to evolving mobility needs, urban transportation infrastructures, and user preferences. Key trends shaping segmentation patterns include the proliferation of electric vehicles, digitized fleet management, and shifting urban policies favoring shared transit modes. As platform-based mobility becomes the norm, understanding segmentation nuances becomes essential for stakeholders aiming to align offerings with precise user needs, service zones, and operational strategies.

The Ride Sharing Market consists of various types, including e-hailing, car sharing, station-based mobility, and car rental. Among these, e-hailing holds the leading position, driven by widespread smartphone penetration, urban congestion challenges, and growing user preference for on-demand mobility. Its dominance is further reinforced by seamless app-based booking, integrated payment systems, and real-time vehicle tracking, making it a staple in metropolitan areas across North America, Europe, and Asia-Pacific.

The fastest-growing type is car sharing, fueled by increasing environmental awareness, cost-efficiency preferences, and rising urban initiatives promoting reduced vehicle ownership. Users are drawn to the flexibility of accessing vehicles without long-term commitments, especially in environmentally conscious cities and student-dense areas.

Station-based mobility continues to serve as a niche solution, particularly in smart city pilot zones where integration with public transit infrastructure is a priority. Car rentals, while declining in some traditional settings, still maintain relevance in tourism-heavy regions where ride-hailing services may not be fully operational. Overall, the variety of types reflects the growing diversity in consumer needs and operator strategies in the Ride Sharing Market.

The application of ride sharing spans several key use cases, including intra-city transportation, intercity travel, airport transfers, and corporate mobility services. Intra-city transportation remains the leading application segment, as daily commuters and city dwellers increasingly rely on ride sharing to navigate congested streets without the hassle of parking or car maintenance. This dominance is reinforced by smart urban planning and rising fuel costs that make traditional commuting less viable.

The fastest-growing application is corporate travel, driven by businesses seeking to streamline employee transport, cut costs, and adopt greener fleet options. Many organizations are integrating ride sharing platforms into their mobility budgets, especially in regions where fleet leasing is less practical. Growth is further supported by the emergence of enterprise-focused ride sharing services offering features like centralized billing, scheduling, and analytics.

Airport transfers continue to see steady demand, particularly with the return of business and leisure travel post-pandemic. Meanwhile, intercity ride sharing is gaining slow but consistent traction in areas where traditional bus or rail options are limited, offering a cost-effective alternative for longer journeys. Together, these applications showcase the market's adaptability across mobility needs and geographic scales.

End-users in the Ride Sharing Market include individual consumers, enterprises, government organizations, and educational institutions, each contributing uniquely to market expansion. Individual consumers constitute the leading end-user group, reflecting a broad shift away from personal vehicle ownership toward shared, tech-enabled transport solutions. Convenience, affordability, and urban mobility constraints continue to drive adoption at the individual level, especially among younger populations and urban professionals.

The fastest-growing end-user segment is enterprises, with businesses increasingly leveraging ride sharing to manage employee transportation, reduce fleet management overheads, and meet sustainability targets. Corporate subscription models, customized dashboards, and bulk booking capabilities have further strengthened enterprise adoption across global markets.

Government and municipal agencies are also emerging as active end-users, using ride sharing to support mobility programs for public employees or underserved populations. Similarly, educational institutions are embracing ride sharing for campus transit solutions and student transport in collaboration with platform providers. The widening end-user base reflects the Ride Sharing Market’s deepening integration into daily life and institutional frameworks.

North America accounted for the largest market share at 34.8% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 17.2% between 2025 and 2032.

The North American market benefits from widespread digital infrastructure, tech-savvy consumers, and deep-rooted investment in AI-enabled transportation services. Meanwhile, Asia-Pacific’s accelerated growth is driven by high urban population density, increasing smartphone adoption, and robust government support for shared mobility and electric vehicle adoption. Each region demonstrates varying maturity levels in ride sharing implementation, but all reflect a shift toward digitized, cost-efficient, and sustainable transport alternatives. From EU-led carbon neutrality goals to Brazil's urban planning reforms and the UAE’s smart mobility initiatives, regional nuances shape both competitive strategies and operational scalability across the Ride Sharing Market.

North America captured 34.8% of the global Ride Sharing Market in 2024, led by countries like the United States and Canada. High smartphone penetration, advanced telematics systems, and consumer preference for convenience-based travel have propelled demand in this region. Key industries such as corporate travel, logistics, and urban commuting have integrated ride sharing services to streamline operations and reduce emissions. Regulatory updates, including California’s Clean Miles Standard and NYC’s fleet electrification mandates, are promoting greener mobility. Additionally, partnerships between ride sharing companies and EV manufacturers are accelerating electric fleet conversions. AI-driven routing and digital payment integration continue to improve customer experience and operational efficiency, reinforcing North America’s leadership in smart urban mobility adoption.

Europe accounted for 26.1% of the global Ride Sharing Market in 2024, with Germany, the UK, and France representing the dominant national markets. Strong regulatory frameworks promoting carbon neutrality and low-emission zones are driving the transition from private vehicles to shared, app-based transportation. The EU’s Green Deal and mobility-as-a-service (MaaS) programs are key enablers of this shift. Countries like Germany have launched incentives for EV ride sharing fleets, while the UK supports ride pooling through congestion charge exemptions. The region is also embracing innovations in vehicle-to-grid systems and ride sharing integration with public transport apps, making Europe a hub for regulatory-led sustainability and digital innovation within the Ride Sharing Market.

Asia-Pacific is the fastest-growing Ride Sharing Market globally, with countries like China, India, and Japan leading demand. Rapid urbanization, heavy traffic congestion, and digital infrastructure expansion have created a strong base for ride sharing adoption. China dominates in volume, with hundreds of millions of active users leveraging app-based transport daily. India’s growing middle class, combined with smartphone and UPI adoption, has led to significant uptake in both metro and Tier-2 cities. Innovation hubs like Singapore and Seoul are pioneering autonomous ride sharing trials, while Japan invests in senior mobility platforms. Public-private partnerships and smart city projects across the region are reinforcing Asia-Pacific’s position as a global growth hotspot for ride sharing services.

The South America Ride Sharing Market is anchored by Brazil and Argentina, with Brazil accounting for the majority share regionally. In 2024, South America represented approximately 6.8% of global ride sharing volume. Rapid urban migration, growing digital payment ecosystems, and unmet public transit needs are accelerating the adoption of ride sharing in major cities like São Paulo, Rio de Janeiro, and Buenos Aires. The construction and energy sectors also utilize ride sharing services to manage labor mobility. Governments in the region are slowly integrating ride sharing into formal transit frameworks through licensing and safety regulations. While infrastructure gaps persist, initiatives around fuel subsidies, app localization, and regional partnerships are enhancing service penetration across Latin America.

The Middle East & Africa Ride Sharing Market is witnessing consistent demand growth, particularly in UAE and South Africa. In 2024, the region contributed around 4.2% of global ride sharing activity. The UAE’s National Smart Mobility strategy and Saudi Arabia’s Vision 2030 have created fertile ground for innovation in shared transport. Oil & gas, construction, and tourism remain key demand generators. South Africa leads sub-Saharan deployment, supported by fintech growth and youth-oriented mobility apps. Digital transformation, including AI-based fare optimization and multilingual app development, is enabling mass adoption. Regional trade partnerships and relaxed licensing norms are also fostering new market entrants and investor confidence in this growing Ride Sharing Market.

United States – 29.5% Market Share

High digital penetration, advanced AI mobility platforms, and a vast urban commuter base make the U.S. the global leader in the Ride Sharing Market.

China – 22.7% Market Share

Massive population density, smartphone usage, and state-supported smart city integration contribute to China's dominance in volume-based ride sharing demand.

The Ride Sharing Market is characterized by intense competition, with over 50 active players operating across global, regional, and niche levels. Leading companies dominate in key regions through well-established platforms, robust user bases, and multi-modal service offerings, while emerging players are targeting underserved areas with tailored models. Competitive dynamics are largely shaped by technological innovation, partnerships, and service diversification. Companies are increasingly investing in AI-powered route optimization, autonomous vehicle integration, and in-app safety features to enhance customer experience and operational efficiency.

Strategic collaborations between ride sharing providers and automotive manufacturers are also redefining the value chain. For instance, partnerships for electric vehicle deployment and charging infrastructure expansion are becoming common. Additionally, several companies have introduced subscription-based ride services, corporate mobility packages, and integration with public transit to retain users and diversify revenue streams. The growing emphasis on sustainability, user safety, and data-driven mobility is pushing companies to continuously evolve, resulting in a highly agile and innovation-driven market landscape.

Gojek

Curb Mobility

Gett

Ola (ANI Technologies Pvt. Ltd.)

BlaBlaCar

Bolt Technology OÜ

Grab Holdings Limited

DiDi Global Inc.

Lyft Inc.

Uber Technologies Inc.

inDrive

Cabify

Yandex Go

The Ride Sharing Market is undergoing a transformative shift driven by cutting-edge technologies focused on efficiency, safety, and environmental sustainability. Artificial Intelligence (AI) is central to route optimization, real-time traffic prediction, dynamic pricing, and fraud detection. Companies are implementing machine learning algorithms that analyze vast amounts of user behavior data to personalize experiences and optimize dispatch systems.

Autonomous vehicles (AVs) are gaining momentum, with pilot programs in urban centers testing self-driving fleets for ride sharing. Integration of Level 4 automation into ride hailing services is expected to reduce labor costs and increase vehicle availability in the long term. Electric Vehicle (EV) adoption is also surging, with ride sharing operators investing in EV fleets and battery-swapping infrastructure to meet sustainability goals and lower operational costs.

Mobile app enhancements such as biometric logins, voice-based commands, and multi-language support are improving accessibility and user retention. Moreover, Internet of Things (IoT) sensors and onboard diagnostics are enabling predictive vehicle maintenance, improving safety and reducing downtime. Digital payment innovations including contactless wallets and blockchain-based ride settlements are reshaping transaction security. These technological advancements are not only elevating user satisfaction but are also enhancing operational scalability and regulatory compliance in the global Ride Sharing Market.

In March 2024, Uber launched its first all-electric ride-sharing fleet in London, comprising over 10,000 EVs, as part of its zero-emissions goal and to meet expanding urban sustainability mandates.

In October 2023, DiDi Chuxing partnered with a Chinese EV manufacturer to deploy autonomous taxis in Shanghai, expanding its pilot program to include over 300 self-driving vehicles across designated zones.

In May 2024, Ola introduced its new AI-powered safety platform, Guardian 2.0, which leverages real-time anomaly detection to monitor rides and alert emergency services automatically if needed.

In December 2023, Bolt expanded its shared micromobility service into five Eastern European cities, adding over 15,000 electric scooters and integrating them into its main ride-sharing app to offer seamless last-mile connectivity.

The Ride Sharing Market Report offers a comprehensive analysis across a wide array of segments, including vehicle types, ride modes, payment platforms, and operational models. It covers key types such as car sharing, e-hailing, carpooling, and station-based mobility. The report provides deep insights into application areas spanning corporate travel, daily commuting, airport transfers, and tourism. Geographic coverage includes all major regions—North America, Europe, Asia-Pacific, South America, and the Middle East & Africa—with a focus on both developed and emerging markets.

Technological integration is a major focal point, with detailed analysis on the role of AI, EVs, autonomous vehicles, and IoT-enabled platforms. The report also explores customer experience innovations, digital transformation in ride hailing, and green mobility initiatives influencing adoption trends.

Furthermore, the study identifies and profiles key market players, emerging startups, and regional disruptors, offering strategic insights into their growth models and competitive strengths. It evaluates regulatory developments, urban planning integration, and the role of government incentives in shaping market evolution. The report is tailored for stakeholders including mobility solution providers, automotive OEMs, tech investors, urban policymakers, and sustainability strategists seeking a clear and actionable market understanding.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 1,313.0 Million |

| Market Revenue (2032) | USD 3,911.5 Million |

| CAGR (2025–2032) | 14.62% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End‑User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Trends, Market Dynamics, AI & Technology Insights, Segment Analysis, Regional & Country‑Wise Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia‑Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Via Transportation Inc. , Gojek, Curb Mobility, Careem (a subsidiary of Uber), Gett, Ola (ANI Technologies Pvt. Ltd.), BlaBlaCar, Bolt Technology OÜ, Grab Holdings Limited, DiDi Global Inc., Lyft Inc., Uber Technologies Inc., Wingz Inc. , Zimride, inDrive, Cabify, Yandex Go, Carma Technology Corporation |

| Customization & Pricing | Available on request (10 % Customization is Free) |