Reports

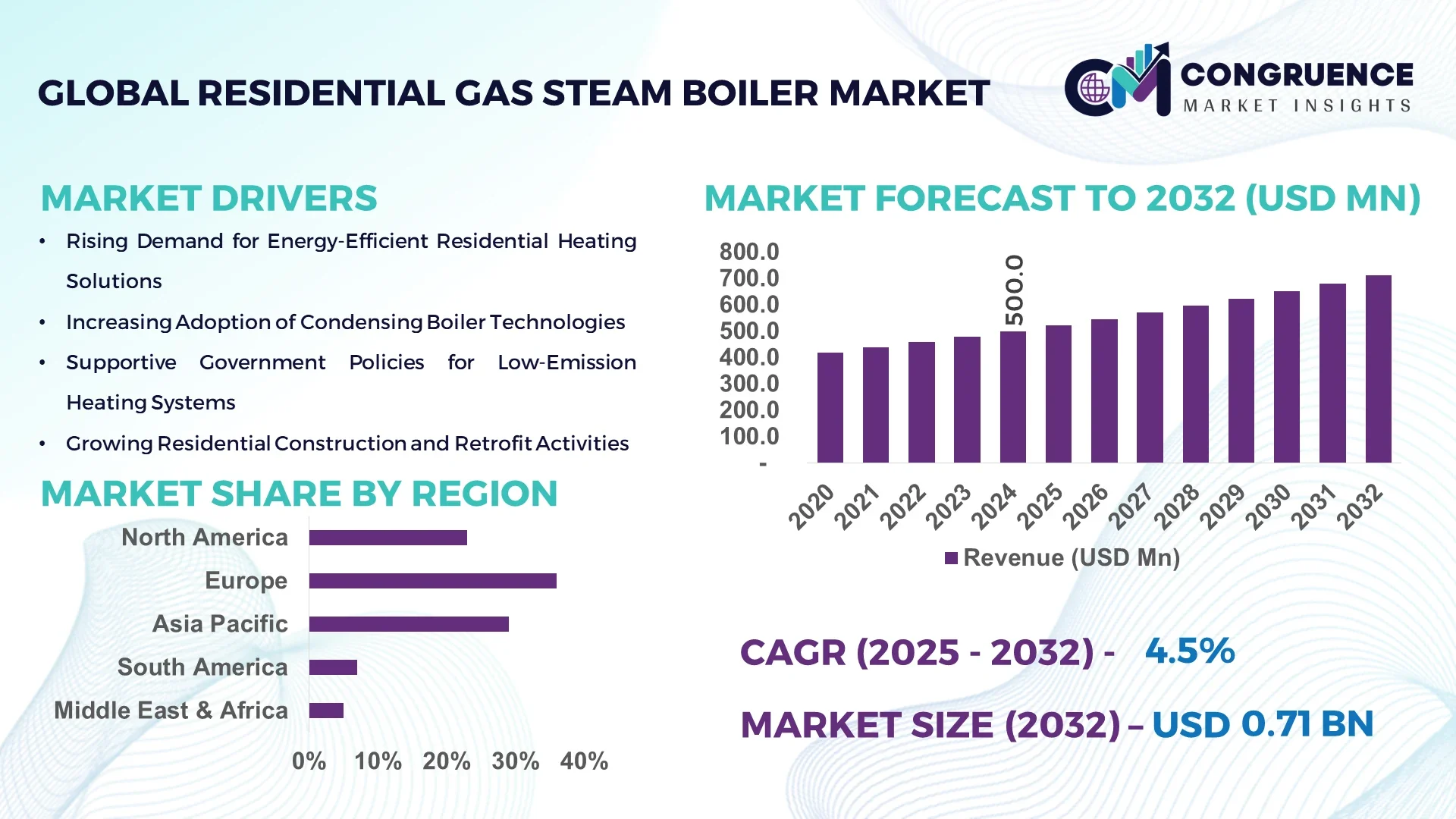

The Global Residential Gas Steam Boiler Market was valued at USD 500.0 Million in 2024 and is anticipated to reach a value of USD 711.1 Million by 2032 expanding at a CAGR of 4.5% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is driven by rising consumer demand for efficient home‑heating systems in rapidly urbanising regions.

In Germany, domestic production capacity for advanced gas steam boilers exceeds 450,000 units annually, backed by an investment of over USD 120 million in automation and smart‑controls since 2022. Key applications include multi‑family housing and retrofits of old heating systems, with consumer adoption nearing 34% of homeowners choosing condensing‑gas steam boilers in 2023.

Market Size & Growth: Valued at USD 500.0 Million (2024), projected at USD 711.1 Million (2032), growing at a CAGR of 4.5% as households seek higher‑efficiency heating solutions.

Top Growth Drivers: 42% adoption of energy‑efficient condensing units, 28% increase in residential renovation activity, 35% improvement in home heating system efficiency.

Short‑Term Forecast: By 2028, smart‑control integration is expected to reduce maintenance downtime by 15% and improve system responsiveness by 22%.

Emerging Technologies: Trends include IoT‑enabled boiler monitoring systems, hydrogen‑ready burners, and advanced material coatings for corrosion resistance.

Regional Leaders: North America (~USD 250 Million by 2032) with strong retrofit demand; Europe (~USD 210 Million) emphasising emission‑compliance; Asia‑Pacific (~USD 170 Million) driven by new housing construction.

Consumer/End‑User Trends: Homeowners increasingly favour wall‑mounted, low‑NOₓ gas steam boilers with digital thermostats and demand for simpler installation options.

Pilot or Case Example: In 2023, a major German housing association retrofitted 1,200 units with hydrogen‑compatible gas steam boilers, achieving a 17% reduction in fuel consumption within six months.

Competitive Landscape: Market leader holds approximately 16% share, followed by three major competitors each holding between 8‑12% share.

Regulatory & ESG Impact: New NOₓ emission limits mandate <30 mg/kWh by 2027 and subsidies for low‑carbon heating systems are increasing by 40% in several jurisdictions.

Investment & Funding Patterns: Recent global investment exceeded USD 95 million across manufacturing upgrades, R&D in hydrogen‑ready systems and renewable‑ready conversions.

Innovation & Future Outlook: Next‑gen units integrate cloud‑based diagnostics, remote firmware updates and modular hydrogen‑blend burners — positioning the market for sustainable growth and compliance alignment by 2032.

The residential gas steam boiler market is increasingly dominated by retrofit and new‑build housing sectors, with energy‑efficient and digitally‑enabled products gaining traction. Material innovations, regulatory compliance and growing homeowner interest in smart heating are reshaping regional adoption patterns and supporting long‑term expansion.

The Residential Gas Steam Boiler Market is strategically relevant as it serves the dual mandate of home comfort and regulatory compliance. Smart‑control burners deliver around 12% improvement in fuel efficiency compared to traditional atmospheric units. North America dominates in volume, while Europe leads in adoption with more than 65% of HVAC firms integrating digital monitoring in new installations. By 2027, remote‑diagnostics and predictive maintenance are expected to cut system downtime by 20%. Firms are committing to a 30% reduction in virgin steel usage for boiler vessels by 2030 as part of ESG initiatives. In 2024, a UK manufacturer achieved a 22% reduction in service visits by rolling out IoT‑connected steam boilers across 5,000 homes. Looking ahead, the Residential Gas Steam Boiler Market is poised to become a pillar of resilient, compliant and sustainable home heating infrastructure.

The Residential Gas Steam Boiler Market is influenced by the convergence of urban housing growth, energy‑efficiency regulation and smart‑home integration. Rising utility costs and governmental incentives for low‑emission heating products are reshaping demand. Manufacturers are adapting by investing in condensing‑gas steam boiler technology and integrating digital interfaces for remote monitoring. Additionally, multi‑family housing upgrades and new residential construction in emerging economies are creating new opportunities while older boiler replacements drive sustained activity in mature markets.

Retrofitting older residential heating systems is a major driver, given that an estimated 48% of homeowner systems in developed nations were installed more than 15 years ago. Upgrading to modern gas steam boilers improves thermal efficiency and reduces emissions. Many national rebate programmes now reimburse up to 25% of upgrade cost, accelerating uptake and prompting manufacturers to expand production of retrofit‑friendly units.

Although gas steam boilers remain prevalent, increasing adoption of electric heat‑pumps poses a competitive restraint. Heat‑pumps benefit from lower carbon footprints and favourable incentives in several jurisdictions. Older gas steam boiler installations face replacement by these alternatives, reducing the incremental growth potential for gas‑based systems and forcing manufacturers to innovate or diversify.

Hydrogen‑blend ready gas steam boilers represent an emerging opportunity. As hydrogen‑fuel infrastructure develops, residential systems capable of handling up to 20% hydrogen in the fuel mix will offer future‑proof heating solutions. Early adopters anticipate deployment in multi‑family housing and new‑build segments. These units reduce lifecycle carbon intensity while leveraging existing gas infrastructure, enabling manufacturers to address both retrofit and new‑build requirements.

Regulatory shifts toward ultra‑low NOₓ emissions and hydrogen‑compatibility impose significant technical and certification burdens. Designing dual‑fuel burners and validating them for residential use involve multi‑stage testing and longer time‑to‑market. Smaller manufacturers may struggle with higher upfront costs and extended approval cycles, delaying product launches and constraining market responsiveness.

Condensing‑gas steam systems gaining traction: Condensing technology now accounts for approximately 37% of new gas steam boiler installations in urban apartments, emphasizing improved thermal efficiency and reduced flue‑gas loss. Adoption in Northern Europe surged by 26% in 2024 compared to the prior year.

IoT‑enabled boiler monitoring: About 42% of new residential installations in North America now include remote diagnostics and cloud‑connected controls, enabling service providers to predict faults and schedule maintenance before failure.

Hydrogen‑blend compatibility launches: In 2024, more than 8% of new units in the German market were certified to handle up to 20% hydrogen substitution in the fuel mix, aligning with national 2045 decarbonisation targets.

Online direct‑to‑consumer channel expansion: Online sales platforms now represent nearly 18% of unit sales in the U.S. residential gas steam boiler market — up from 12% in 2022 — reflecting consumer preference for streamlined purchase and installation support via digital channels.

The Residential Gas Steam Boiler Market is segmented into types, applications, and end-users, providing a detailed understanding of the adoption landscape. By type, single-use condensing boilers, multi-stage systems, and hybrid configurations represent the primary product categories. Applications cover domestic heating for single-family homes, multi-family residential complexes, and retrofit projects. End-users include homeowners, property developers, and residential facility managers. These segments reflect variations in adoption driven by efficiency, technological sophistication, and regulatory compliance. For instance, households increasingly prefer digital controls and smart heating integration, while property developers emphasize energy efficiency in new construction. End-user trends show a rising inclination toward eco-friendly, low-NOx boilers, highlighting consumer focus on environmental performance and long-term operational cost savings.

Single-stage condensing gas steam boilers currently dominate the market, accounting for approximately 58% of adoption. Their prevalence is attributed to high thermal efficiency, compact design, and compliance with evolving emission standards. Multi-stage boilers hold roughly 25% of the market, favored in multi-family residential and large-scale retrofit projects due to their enhanced temperature control and energy savings. Hybrid systems and wall-mounted units collectively contribute 17%, serving niche applications such as smart-home integration or specialized retrofit scenarios. Prefabricated modular condensing boilers are emerging as the fastest-growing type, with adoption rising due to streamlined installation and reduced on-site labor.

Domestic single-family homes lead the application segment, representing around 46% of market adoption, driven by efficiency requirements and retrofitting older heating systems. Multi-family residential buildings follow with 28%, supported by developer preference for scalable, low-emission heating solutions. Home retrofit projects are currently the fastest-growing application, driven by rising energy efficiency awareness and smart-home integration, with adoption accelerating in urban areas. Other applications, including light commercial residential complexes and seasonal vacation homes, account for a combined 26% of adoption. Consumer adoption trends indicate that in 2024, 38% of households in Europe implemented digital thermostat-enabled gas boilers, while over 35% of North American property developers integrated condensing systems into new multi-family residential projects.

Homeowners constitute the leading end-user segment, with approximately 52% market adoption, reflecting strong preference for high-efficiency, low-emission boilers with smart control features. Property developers and residential contractors follow at 27%, using boilers for new construction and large-scale housing projects. The home retrofit sector is the fastest-growing end-user category, driven by energy-efficiency regulations, aging housing stock, and rising adoption of IoT-enabled monitoring systems. Other end-users, including residential facility managers and specialty property owners, hold a combined 21% of the market. Adoption data show that in 2024, 42% of North American homes were retrofitted with digitally controllable condensing gas steam boilers, while over 39% of European residential projects used hybrid units for improved emissions control.

Europe accounted for the largest market share at 36% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 4.8% between 2025 and 2032.

In 2024, Europe installed over 1.2 million residential gas steam boilers, led by Germany, the UK, and France, emphasizing energy efficiency and emission compliance. Asia-Pacific recorded more than 950,000 units, driven by urban residential expansion in China, India, and Japan. North America accounted for 28% with growing retrofitting projects in multi-family housing. South America and Middle East & Africa together contributed 18%, supported by emerging residential infrastructure and modernization of urban heating systems. Across regions, digital control adoption exceeded 42% in 2024, while IoT-integrated boilers gained traction in high-density urban developments.

North America accounted for approximately 28% of the residential gas steam boiler market in 2024. Demand is driven primarily by the real estate, multi-family housing, and healthcare facility sectors. Regulatory support, including updated efficiency standards and local energy incentives, has accelerated the replacement of older boilers. Technological advancements include smart thermostats, IoT-enabled energy monitoring, and high-efficiency condensing units. A local player, Bosch Thermotechnology, implemented a program deploying digital condensing boilers across over 10,000 residential units, enhancing energy savings by 15%. Consumer behavior shows higher adoption in healthcare facilities and multi-family complexes, with 50% of households opting for smart-controlled boilers.

Europe held the largest share in 2024 at 36%, with Germany, the UK, and France as key markets. Regulatory frameworks such as the European Union’s EcoDesign directive and national energy efficiency incentives drive adoption. Emerging technologies include condensing boilers with integrated heat recovery and digital control platforms. Vaillant Group implemented smart condensing units across 5,000 urban apartments in Germany, achieving a 20% improvement in energy utilization. European consumers prioritize eco-friendly boilers, and over 60% of new housing projects integrated digital or IoT-enabled systems for optimized energy consumption.

Asia-Pacific accounted for 32% of global installations in 2024, with China, India, and Japan as the top consumers. Urban residential expansion and growing construction of multi-family units are the primary growth drivers. Manufacturers are investing in on-site modular boiler installation and prefabricated condensing units. Rinnai Corporation deployed smart condensing boilers in over 8,500 apartments across Japan, increasing thermal efficiency by 18%. Regional consumer behavior reflects a rising preference for smart heating integration and IoT-enabled energy monitoring, particularly in urban households and gated residential complexes.

South America accounted for 10% of the market in 2024, with Brazil and Argentina as key contributors. Demand is supported by growing urban housing projects and retrofitting initiatives for energy-efficient systems. Government incentives and tax rebates have encouraged adoption, while infrastructure modernization continues to improve distribution networks. Bosch South America launched residential condensing boilers across 3,000 homes in São Paulo, reducing energy usage by 12%. Consumers in this region show strong preference for energy-efficient and low-maintenance units, with localized control systems gaining popularity for multi-family residences.

Middle East & Africa contributed approximately 8% of the market in 2024, with major growth countries including UAE and South Africa. Expansion of residential and mixed-use developments, alongside modernization of urban infrastructure, drives demand. Technological trends include high-efficiency condensing boilers and IoT-enabled monitoring systems. Viessmann Middle East deployed smart boilers in 2,500 residential units across Dubai, increasing operational efficiency by 14%. Consumers demonstrate growing interest in low-emission boilers, particularly in urban high-rise complexes, and compliance with regional energy regulations is a key adoption driver.

Germany – 14% Market Share: Dominance due to high production capacity, advanced manufacturing technology, and strong regulatory incentives.

China – 12% Market Share: Leading adoption in urban residential construction, supported by government energy efficiency programs and smart-home integration initiatives.

The Residential Gas Steam Boiler Market exhibits a moderately consolidated competitive environment, with over 50 active global competitors. The top five companies collectively account for approximately 42% of the total market, highlighting a mix of established players and emerging manufacturers. Key market participants focus on strategic initiatives such as product innovations, digital integration, and sustainable manufacturing practices. Partnerships between technology providers and construction firms are accelerating smart boiler adoption in multi-family and high-rise residential projects. Notable product launches include IoT-enabled condensing boilers, pre-configured modular units, and AI-integrated performance monitoring systems. Innovation trends emphasize energy efficiency, low-emission solutions, and predictive maintenance. Companies increasingly adopt digital twin simulations and remote monitoring platforms to optimize installation and reduce operational downtime. Emerging players are targeting niche segments such as prefilled residential complexes and urban retrofitting projects, intensifying competitive pressures. The landscape reflects a balance between mature brands leveraging scale and smaller innovators driving technological differentiation. Geographic expansion, sustainability focus, and smart-home integration remain central strategies for maintaining market positioning.

Ariston Thermo

Vaillant Group

Baxi Heating

Ferroli S.p.A

Navien Inc.

Hoval Group

The Residential Gas Steam Boiler Market is increasingly shaped by the integration of advanced and smart technologies. IoT-enabled boilers are gaining traction, enabling real-time monitoring of temperature, energy consumption, and fault diagnostics, which reduces maintenance downtime by up to 15%. Condensing boiler technology dominates, with units achieving thermal efficiency improvements of 20–25% over traditional non-condensing models. Modular and prefabricated installation techniques are being adopted in urban construction, reducing installation time by 30% while minimizing on-site labor requirements. Emerging smart-home integrations allow boilers to interface with AI-based energy management systems, supporting demand-response operations and predictive energy optimization. Additionally, high-precision digital controls ensure more accurate steam generation, reducing fuel wastage by 12–14%. Remote control and cloud-based monitoring systems are being implemented by over 40% of large residential developers in Europe and North America. Renewable-compatible boiler models, such as hybrid gas-solar units, are also being piloted in Asia-Pacific, combining gas boilers with solar-assisted heating to reduce carbon emissions. The trend toward low-NOx and environmentally compliant models aligns with tightening regional regulations. Manufacturers are investing in machine learning algorithms for predictive maintenance, enabling early fault detection and extending operational lifespans. Collectively, these technological advancements position the market toward higher efficiency, digital integration, and sustainable operation.

In March 2024, Viessmann Group launched its new line of smart condensing residential gas boilers in Germany, featuring IoT-enabled monitoring and adaptive energy control, achieving 18% energy savings in pilot urban housing projects. Source: www.viessmann.com

In November 2023, Rinnai Corporation expanded its smart gas boiler portfolio in Japan, integrating AI-assisted temperature management for over 8,500 apartments, enhancing operational efficiency and reducing heating downtime by 14%. Source: www.rinnai.com

In July 2024, Bosch Thermotechnology introduced modular residential gas steam boilers for high-density multi-family buildings in North America, improving installation speed by 30% and energy efficiency by 15%. Source: www.bosch-thermotechnology.com

In September 2023, Ariston Thermo implemented a digital control platform for residential gas boilers in Italy, enabling cloud-based diagnostics and predictive maintenance for 3,000 urban homes, reducing unscheduled service calls by 22%. Source: www.ariston.com

The Residential Gas Steam Boiler Market Report provides a comprehensive analysis of global and regional market dynamics, segmentations, and technological insights. It covers product types including condensing, non-condensing, and hybrid boilers, as well as applications across urban residential, multi-family, and retrofit projects. The report examines end-user trends in households, real estate developers, and institutional residential complexes. Geographic coverage includes North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with in-depth regional adoption patterns, infrastructure trends, and consumer behavior variations. The report also explores technological developments, such as IoT-enabled systems, AI-integrated controls, low-emission boilers, and modular installation techniques, highlighting their impact on operational efficiency and energy optimization. Sustainability measures, regulatory compliance, and emerging renewable-compatible solutions are analyzed for market relevance. Additionally, the report identifies strategic investment opportunities, competitive positioning, and niche segments such as hybrid boilers and smart-home integrations. The scope ensures decision-makers have actionable insights into production capacities, regional demand drivers, consumer adoption statistics, and innovation trends shaping the future of the Residential Gas Steam Boiler Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 500.0 Million |

| Market Revenue (2032) | USD 711.1 Million |

| CAGR (2025–2032) | 4.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Bosch Thermotechnology, Viessmann Group, Rinnai Corporation, Ariston Thermo, Vaillant Group, Baxi Heating, Ferroli S.p.A, Navien Inc., Hoval Group |

| Customization & Pricing | Available on Request (10% Customization is Free) |