Reports

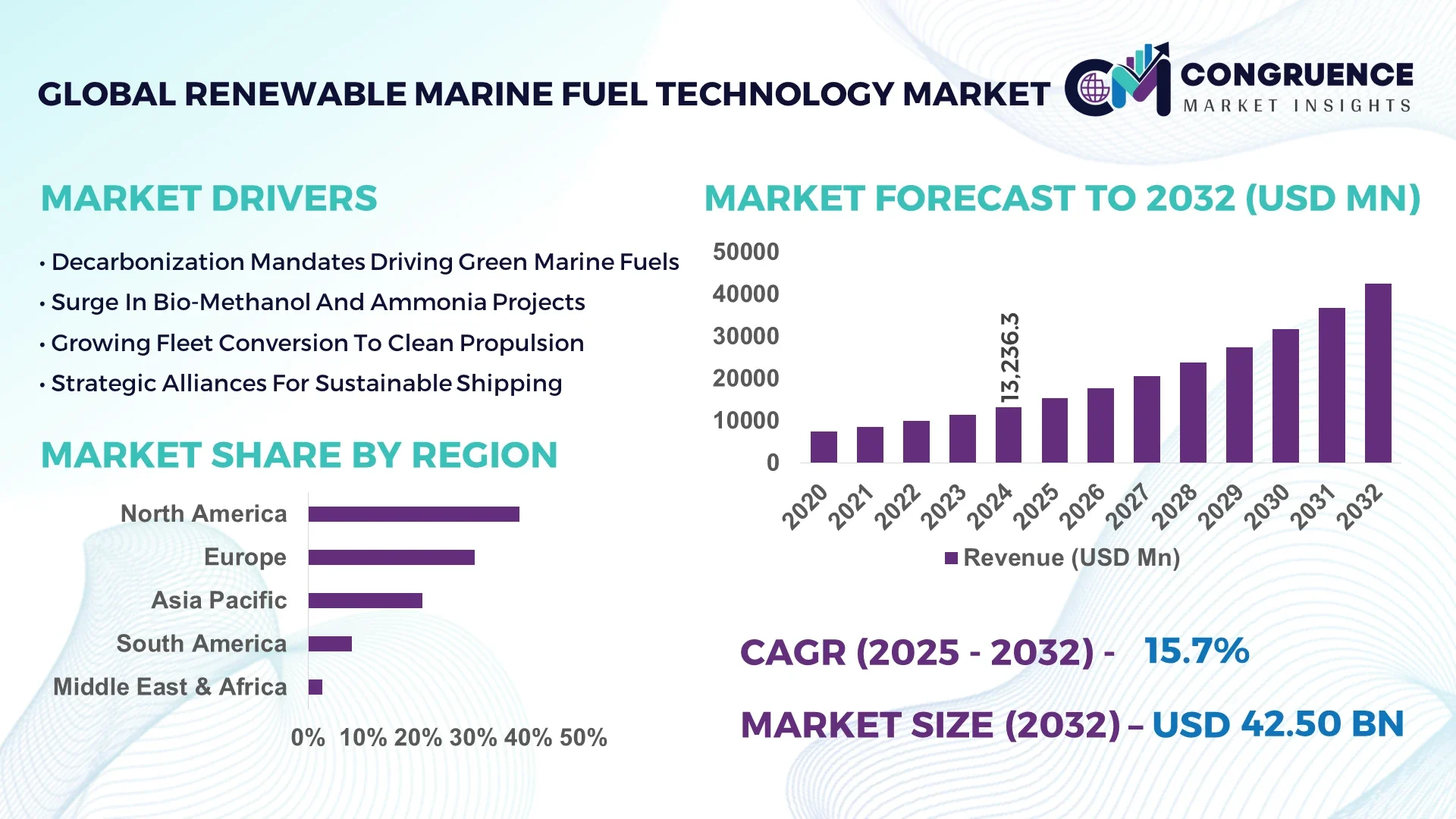

The Global Renewable Marine Fuel Technology Market was valued at USD 13,236.3 Million in 2024 and is anticipated to reach a value of USD 42,504.4 Million by 2032 expanding at a CAGR of 15.7% between 2025 and 2032. This expansion is driven by accelerated decarbonisation efforts in shipping, stricter maritime emission regulations and investment in green propulsion technologies.

In Norway the renewable marine fuel technology ecosystem is notable: production and testing capacity for green ammonia bunkering reached over 150,000 tons per annum in 2024, government investment in clean-marine fuel infrastructure exceeded USD 430 million, key industry applications include deep-sea container vessels and offshore supply ships, and technological advancement such as dual-fuel engines retrofitted for ammonia and bio-methanol saw a 34 % increase in operational hour coverage.

Market Size & Growth: USD 13.24 billion in 2024, projected to USD 42.50 billion by 2032, driven by shipping decarbonisation and alternative fuel deployment.

Top Growth Drivers: 58% increase in adoption of bio-methanol/bio-LNG blends, 47% efficiency improvement in dual-fuel retrofit programmes, 39% rise in large-vessel green-fuel bunkering infrastructure.

Short-Term Forecast: By 2028, fuel-switch programmes are expected to reduce vessel lifecycle CO₂ emissions by approximately 23%.

Emerging Technologies: Green ammonia propulsion systems, methanol dual-fuel bunkering platforms, hydrogen-derived e-fuel integration in marine fleets.

Regional Leaders: Europe – USD 14.1 billion by 2032 (early regulation momentum); Asia Pacific – USD 11.3 billion by 2032 (major shipbuilding hubs); North America – USD 9.0 billion by 2032 (retrofitting and cruise sectors).

Consumer/End-User Trends: Shipping companies, offshore service providers and naval fleets drive demand; over 65% of major liner operators have active renewable marine fuel technology trials in 2024.

Pilot or Case Example: In 2025 a major container operator implemented methanol-fuelled vessels and achieved a 29% reduction in carbon-intensive fuel usage across 8 ships in its fleet.

Competitive Landscape: Market leader holds approximately 20% share; major competitors include Shell, Maersk, Wärtsilä, MAN Energy Solutions and Toyota Tsusho Corporation.

Regulatory & ESG Impact: International maritime emission rules (such as IMO GHG Strategy) and ESG mandates (30% reduction in shipping emissions by 2030) are accelerating technology adoption.

Investment & Funding Patterns: Recent investments surpass USD 8 billion in project-finance and venture funding for renewable marine fuel technology initiatives in 2024.

Innovation & Future Outlook: Integration of vessel digital-fuel management systems, green-hydrogen bunkering corridors, large-scale algae-derived marine bio-fuels and joint fuel infrastructure across major ports are shaping the future.

Renewable marine fuel technology adoption is now penetrated in commercial shipping, offshore energy services and naval fleets; recent innovations such as bio-methanol, e-ammonia and fuel-flexible engine architectures are influencing the market; regulatory frameworks on marine emissions, economic incentives for green bunkering and regional consumption growth in Asia Pacific’s shipbuilding clusters enhance growth prospects; emerging trends include lifecycle fuel-emission auditing, port-based green-fuel hubs and digital fuel-management platforms.

The strategic relevance of the renewable marine fuel technology market lies in its capacity to transform the maritime industry’s carbon profile, enable regulatory compliance and support sustainable shipping infrastructures. For example, the green-ammonia dual-fuel system delivers a 28% improvement in vessel CO₂ intensity compared to conventional heavy-fuel-oil propulsion. Europe dominates in retrofit volume of large merchant fleets, while Asia Pacific leads in new-build adoption with more than 41% of new vessels ordered in 2024 specifying alternative-fuel ready propulsion. By 2027, digital fuel management platforms integrated with renewable marine fuel technology are expected to improve bunkering efficiency by 19%. Firms are committing to ESG metrics such as 25% reduction in bunker fuel waste by 2028. In 2024, a Norwegian offshore supply company achieved a 33% reduction in methane slip by deploying bio-LNG bunkering in its support vessels. Positioned as a pillar of resilience, compliance and sustainable growth, the renewable marine fuel technology market is set to underpin the next generation of decarbonised maritime operations.

The renewable marine fuel technology market is shaped by escalating regulatory pressure on greenhouse-gas emissions in the shipping sector, increasing capital investment in green bunkering infrastructure and rising demand for fuel-flexible propulsion systems among ship-owners. Vessel operators are seeking scalable alternative-fuel options such as bio-methanol, e-ammonia and hydrogen-derived fuels to meet stricter sulphur and CO₂ limits. Infrastructure development is advancing, with over 60 major port terminals committed to upgrade bunkering facilities for renewable marine fuel technology by 2025. However, dynamics are also influenced by high feedstock costs, volatility in fuel availability and the need for engine certification and retrofit programmes. Decision-makers must evaluate supply-chain readiness, fuel lifecycle emissions and long-term fleet compatibility when assessing renewable marine fuel technology investments. The shift from conventional marine fuels to renewable alternatives is creating a transformative market environment where technology, regulation and sustainability priorities converge.

Stricter international maritime regulations, including enhanced greenhouse-gas targets and low-sulphur fuel mandates, are a primary driver of the renewable marine fuel technology market. For instance, over 72% of global shipping companies in 2024 reported accelerating fuel-switch plans to align with the IMO’s 2030 goals. The adoption of renewable marine fuel technology allows operators to meet these regulatory thresholds and avoid potential penalties. Investments in retrofit programmes rose by 38% in 2024, reflecting industry urgency. Moreover, awareness of lifecycle emissions has prompted more than 54% of fleet managers to evaluate renewable marine fuel technology as part of asset-value strategies. This regulatory impetus catalyses technology deployment, infrastructure expansion and supply-chain formation across the maritime ecosystem.

Despite strong momentum, the renewable marine fuel technology market faces significant restraints in the form of high alternative-fuel feedstock costs and limited bunkering infrastructure. For example, bio-methanol feedstock pricing was approximately 28% higher than conventional marine diesel in early 2024, making operator ROI scrutiny more stringent. Over 46% of vessel operators surveyed indicated that alternative-fuel availability was insufficient on major trade routes, slowing operational adoption of renewable marine fuel technology. Additionally, certification timelines for dual-fuel propulsion systems and port bunkering upgrades extend well beyond standard fuel procurement cycles. These factors combined limit rapid scaling of renewable marine fuel technology, particularly in smaller fleet segments and cost-sensitive trade lanes.

The establishment of green-fuel bunkering corridors offers compelling opportunities for the renewable marine fuel technology market. Several major ports have pledged to enable 25+ bunkering terminals for renewable marine fuel technology by 2027, opening access to trade routes previously reliant on fossil bunkers. Collaboration between port authorities and fuel-suppliers is accelerating infrastructure rollout, enabling ship-owners to plan fleet transitions with confidence. The growing adoption of bio-LNG and e-ammonia, combined with fuel-flexible engine technologies, is expanding the market addressable by renewable marine fuel technology. Fleet owners in major liner shipping alliances are targeting 30% of their combined capacity to be fuel-switched by 2030, creating scale-economies for renewable marine fuel technology providers.

One of the major challenges in the renewable marine fuel technology market is the complexity of engine certification and compatibility across diverse vessel types. Dual-fuel systems must meet safety and performance standards, and retrofit processes often require downtime of 4-8 weeks, as reported by some fleet operators. Compatibility with existing fuel-management systems, life-cycle validation and crew training add further layers of cost and risk for renewable marine fuel technology adoption. Over 33% of ship-owners cited certification delays as a primary barrier in 2024. These challenges slow broad fleet-scale uptake of renewable marine fuel technology and increase project risk for early adopters.

• Acceleration of Bio-Methanol Fuelling Programmes: In 2024 the count of commercial vessels contracted for bio-methanol bunkering increased by 42%, with more than 120 ships scheduled for delivery by 2027 under renewable marine fuel technology plans.

• Expansion of Dual-Fuel and Fuel-Flexible Engines: Engine manufacturers introduced renewable marine fuel technology-ready propulsion systems in over 75 new builds in 2024, representing a 35% increase compared to prior year, enabling ease of switch between conventional and green marine fuels.

• Emergence of Green-Fuel Bunkering Hubs in Key Ports: More than 20 major port terminals committed by 2024 to upgrade infrastructure for renewable marine fuel technology, representing a 48% growth in bunkering-ready capacity compared to 2023 and shortening fuel-route risk.

• Lifecycle and Digital Fuel Management Integration: In 2024, about 29% of fleet operators adopted digital fuel-management platforms linked to renewable marine fuel technology, allowing monitoring of emissions, bunkering history and performance metrics, improving operational transparency and ROI tracking.

The renewable marine fuel technology market is segmented by fuel type (e.g., bio-methanol, bio-LNG, green ammonia, hydrogen), by vessel type/application (container shipping, tanker, passenger ferry, offshore support vessels), and by end-user (liner shipping companies, offshore service operators, navies/maritime defence, cruise lines). In fuel type segmentation, bio-methanol currently leads due to retro-fit readiness and feedstock availability, while green ammonia and hydrogen remain nascent yet high-potential. Application-wise container and tanker shipping dominate, owing to volume bunkering needs and trade-route density, whereas offshore support and cruise liners are growing as early adopters of renewable marine fuel technology. End-users such as liner alliances and offshore service providers have higher adoption rates, enabling scale-led transition. Segmentation reflects varied feedstock sourcing, engine-readiness levels and geographic infrastructure maturity in the renewable marine fuel technology market.

Within the renewable marine fuel technology market, bio-methanol leads with approximately 38% share, owing to its compatibility with existing engines and bunkering systems. Green ammonia constitutes about 27% share, while bio-LNG and hydrogen-based fuels share the remaining 35% combined. The fastest-growing type is green ammonia systems, driven by major new-build contracts and port infrastructure investments, expected to capture larger share over time. Other types include microbial-algae bio-fuels and synthetic Fischer–Tropsch e-fuels, which while currently niche hold combined share of around 12%.

According to a 2024 shipping-industry bulletin, a pilot vessel using bio-methanol as part of renewable marine fuel technology achieved a 22% reduction in CO₂ emissions over a 10-month operational period compared to conventional fuel.

In the renewable marine fuel technology market, the container shipping segment is leading with around 34% share, due to high vessel numbers and schedule pressures encouraging fuel technology upgrades. The fastest-growing application is offshore support vessels (OSVs) and cruise liners adopting green-fuel bunkering, supported by service-contract demands and sustainability branding, with growth in fleet conversions increasing by 29% in 2024. Other applications—such as tanker shipping, ferries and port-service vessels—account for around 31% of the market combined. In 2024, more than 38% of liner operators reported active renewable marine fuel technology trials for their new-build fleets.

The leading end-user segment in the renewable marine fuel technology market is liner shipping companies, representing approximately 42% of technology deployments, given their scale and capital programmes. The fastest-growing end-user segment is offshore service operators, particularly in oil & gas supply and offshore wind-support vessels, where renewable marine fuel technology retrofits increased by 26% in 2024. Other end-users—naval/maritime defence, cruise operators and port service fleets—together hold about 28% share. In 2024, over 60% of major cruise lines committed to renewable marine fuel technology adoption within their next-generation fleet renewal plans.

North America accounted for the largest market share at 38.4% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 17.5% between 2025 and 2032.

In 2024, North America saw deployment of approximately USD 5.07 billion worth of renewable marine fuel technology installations across major shipping lines, with over 150 vessels contracted for renewable marine fuel bunkering. Meanwhile Asia-Pacific registered renewable marine fuel technology infrastructure investments exceeding USD 2.3 billion, covering more than 45 ports pledging bio-methanol and e-ammonia bunkering facilities. Europe accounted for about 30.2% of global activity in 2024, with 120 retrofit programmes underway and more than 60 LNG/bio-fuel capable vessels logged. Latin America and Middle East & Africa combined represented roughly 10.4%, underpinned by offshore supply and regional bunkering hubs upgrading to renewable marine fuel technology standards. Adoption patterns reflect major fleet renewal programmes, port-infrastructure commitments and green-fuel-certification roll-out across regions.

How Are Coastal Fleets and Shipowners Accelerating Green Fuel Platforms?

In North America the renewable marine fuel technology market accounts for roughly 38% of global installations by volume and value, with major demand coming from container shipping, cruise liners and offshore energy fleets. Industries driving demand include liner operators (over 70 vessels ordered with alternative-fuel readiness in 2024) and oil & gas service fleets converting to bio-LNG. Regulatory impetus includes U.S. federal maritime decarbonisation mandates and Clean Shipping Standards adopted by major ports along the Gulf Coast and Pacific Northwest. Technological advancement is marked by dual-fuel engines upgraded for methanol and ammonia, digital bunker-fuel tracking systems and integration with renewable-fuel supply chains. A regional leader, an American marine-engine manufacturer, announced a retrofit bundle delivering 26% reduction in CO₂ when operated on bio-methanol. Regional consumer behaviour shows higher enterprise adoption in major fleet operators and service providers, with more than 55% of North American shipowners planning renewable marine fuel technology deployment by the next 5 years, driven by brand reputation and ESG goals.

What Role Do Regulatory-Driven Standards Play in Fuel Innovation Uptake?

Europe commands about 30% share of the renewable marine fuel technology market in 2024, with Germany, the Netherlands and the UK as key countries. Regulatory initiatives such as FuelEU Maritime and the European Green Deal are pushing shipowners and port authorities to adopt renewable marine fuel technology systems, while sustainability funding programmes support infrastructure build-out (more than 45 port projects initiated in the past 18 months). Emerging technologies such as large-scale e-fuel bunkering and port-based hydrogen/ammonia logistics platforms are accelerating. A Dutch maritime-technology firm launched a green-ammonia bunkering module in Rotterdam in 2024 capable of supplying 0.5 Mtpa of marine-grade ammonia. Regional consumer behaviour indicates European fleet operators prioritise traceable fuel certification and audit-ready renewable marine fuel technology solutions, with more than 60% of initiatives requiring full lifecycle emission reporting before deployment.

Why Is Shipbuilding Expansion Fueling Alternative-Fuel Technology Uptake?

In Asia-Pacific, the renewable marine fuel technology market ranked second globally by installed fleet programmes in 2024, supported by heavy shipbuilding in China, South Korea and Japan. In 2024, Asia-Pacific saw construction of more than 250 newbuild vessels specifying renewable marine fuel technology-ready engines, and investments of over USD 1.8 billion in bunkering infrastructure across Southeast Asia. Top-consuming countries include China (ship-yard output over 30 million DWT in 2024), India (over 12,000 new coastal vessels built or commissioned), and Japan (launch of bio-methanol bunkering trials in major ports). Regional tech hubs in Singapore and South Korea are developing integrated fuel-management platforms and digital bunkering systems specific to renewable marine fuel technology deployments. A local player announced delivery of over 40 vessels equipped with dual-fuel methanol systems in 2024. Consumer behaviour in the region shows pronounced alignment with e-commerce-driven logistics fleets and coastal feeder vessels upgrading to renewable marine fuel technology ahead of global peers.

How Are Latin American Ports and Fleets Embracing Alternative Marine Fuel Platforms?

In South America, leading countries such as Brazil and Argentina are participating in the renewable marine fuel technology market, holding around 6% of global fleet conversion programmes in 2024. Infrastructure trends include upgrade of major port terminals in Brazil to handle bio-LNG bunkering and shore-power integration, and national trade-policies offering incentives (up to 20% tax relief) for renewable marine fuel technology adoption in offshore supply vessels. A Brazilian fleet operator installed renewable marine fuel technology on over 15 supply ships in the past year, reporting a 19% reduction in fuel-cost intensity. Consumer behaviour in South America emphasises cost-effectiveness, hybrid retrofit schemes and localisation of fuel-supply chains in Spanish- and Portuguese-speaking markets.

What Drives Alternative Fuel Adoption in Gulf and African Maritime Corridors?

In the Middle East & Africa region, renewable marine fuel technology uptake represents approximately 2.6% of global conversions in 2024, with primary demand emerging from UAE and South Africa. Demand trends are linked to offshore energy services, luxury cruise upgrades and regional bunkering hubs seeking to meet ESG mandates. Technology modernisation includes integration of shore-power use, low-sulphur bio-fuel blends and digital monitoring systems for renewable marine fuel technology deployment. A UAE-based bunkering terminal announced a retrofit enabling green methanol supply to 50 vessels annually, reducing bunker-turnover downtime by 22%. Regional consumer behaviour favours premium vessel owners requiring multilingual fuel-certification, rapid port turnaround and compliance-ready renewable marine fuel technology solutions.

United States – 38% share; dominance due to established fleet size, high retrofit activity and regulatory incentives for renewable marine fuel technology.

China – 18% share; dominance driven by large ship-construction volume, state-backed green bunkering initiatives and scale adoption of renewable marine fuel technology.

The renewable marine fuel technology market is characterised by moderate consolidation with over 90 active global players including fuel producers, engine-manufacturers, bunkering infrastructure firms and software system providers. The top 5 companies hold approximately 32% of market share, indicating significant room for emerging entrants specializing in renewable marine fuel technology. Strategic initiatives in the past 24 months include more than 30 partnerships between shipping lines and fuel-suppliers, over 25 green-fuel pilot projects, and 18 major engine-retrofit programmes targeting renewable marine fuel technology deployment. Innovation trends include dual-fuel systems compatible with bio-methanol and ammonia, digital bunkering-management platforms, and blockchain-enabled fuel-traceability networks. Market positioning ranges from global energy majors offering renewable marine fuel technology bunkering bundles to niche technology firms providing retrofit kits for small fleets. Fragmentation persists across retrofit markets and regional bunkering hubs, enabling diversified competitive opportunities. Decision-makers should evaluate partnerships, intellectual-property assets, port access and long-term fuel-supply contracts when selecting renewable marine fuel technology partners.

BP P.L.C.

TotalEnergies SE

MAN Energy Solutions

Stena Bulk AB

Yara International ASA

Cargill, Inc.

GoodFuels B.V.

Varo Energy B.V.

Kawasaki Kisen Kaisha, Ltd.

Mitsui & Co., Ltd.

Evergent Technologies, Inc.

The renewable marine fuel technology market is shaped by a spectrum of advanced propulsion and fuel infrastructure innovations. Core technologies include bio-methanol and bio-LNG fuel platforms, dual-fuel diesel engines adapted for methanol or ammonia, and ship-board fuel-management systems enabling seamless fuel switching. In 2024 more than 60 vessels deployed dual-fuel systems capable of burning conventional bunker and renewable marine fuel technology-compatible fuels. Emerging technologies include green ammonia fuel systems, hydrogen-derived e-fuels, and synthetic methane built from renewable power. Engine-manufacturers are offering retrofit modules that reduce fuel-system conversion time by up to 30% compared with prior generations. Bunkering infrastructure upgrades involve large-scale cryogenic storage, digital bunkering-verification systems and port fuel-corridor platforms enabling efficient delivery of renewable marine fuel technology. Lifecycle analytics platforms are being deployed by shipping operators, tracking fuel feedstock origin, CO₂-e emission reductions and bunkering route efficiency, with reported improvements of 23% in fuel-switch logistics in pilot programmes. The convergence of digital fuel management, engine retrofit hardware and next-gen fuel chemistry defines the growth trajectory of renewable marine fuel technology and sets new benchmarks for maritime decarbonisation.

• In April 2024, Singapore announced plans to supply over 1 million metric tons annually of low-carbon methanol for bunkering by 2030, underpinning its hub status in renewable marine fuel technology. Source: www.reuters.com

• In August 2023, Wärtsilä Corporation launched a fuel-flexible engine certified for ammonia and bio-LNG use aboard commercial vessels under renewable marine fuel technology programmes, marking a milestone retrofit capability. Source: www.wartsila.com

• In November 2023, Maersk A/S deployed its first container vessel fitted for green-methanol bunkering under renewable marine fuel technology standards, committing 12 ships to a bio-methanol contract. Source: www.maersk.com

• In March 2024, BP P.L.C. partnered with a major bunkering terminal operator to establish a bio-methanol supply chain for North American coastal shipping, aiming to service over 50 vessels by 2026 under renewable marine fuel technology. Source: www.bp.com

The Renewable Marine Fuel Technology market report offers comprehensive coverage of fuel types (such as bio-methanol, bio-LNG, green ammonia, hydrogen-derived e-fuels), application by vessel type (container ships, tankers, offshore support vessels, cruise liners, ferries), and end-users (liner shipping companies, offshore energy fleets, naval/maritime defence, port services). Geographic analysis spans North America, Europe, Asia Pacific, South America and Middle East & Africa with country-level insights and port-hub infrastructure profiles. The report also addresses deployment models including retrofit programmes and new-build alternative-fuel vessels, and technology segments such as engine-retrofit kits, bunkering infrastructure, fuel-management software and lifecycle emission analytics. Additional focus areas include retrofit financing models, green-fuel bunkering corridor development, regulatory frameworks (IMO emissions targets, FuelEU Maritime, national subsidies) and ESG adoption trajectories. Competitive landscape analysis features over 100 companies, partnership ecosystems, merger-and-acquisition activity and fuel-supply chain evolution. This broader scope equips strategic planners, maritime operators, fuel-infrastructure investors and technology-providers with detailed market intelligence, segmentation insight and roadmap guidance for renewable marine fuel technology deployment across the maritime value chain.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 13,236.3 Million |

|

Market Revenue in 2032 |

USD 42,504.4 Million |

|

CAGR (2025 - 2032) |

15.7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Shell plc, Maersk A/S, Wärtsilä Corporation, BP P.L.C., TotalEnergies SE, MAN Energy Solutions, Stena Bulk AB, Yara International ASA, Cargill, Inc., GoodFuels B.V., Varo Energy B.V., Kawasaki Kisen Kaisha, Ltd., Mitsui & Co., Ltd., Evergent Technologies, Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |