Reports

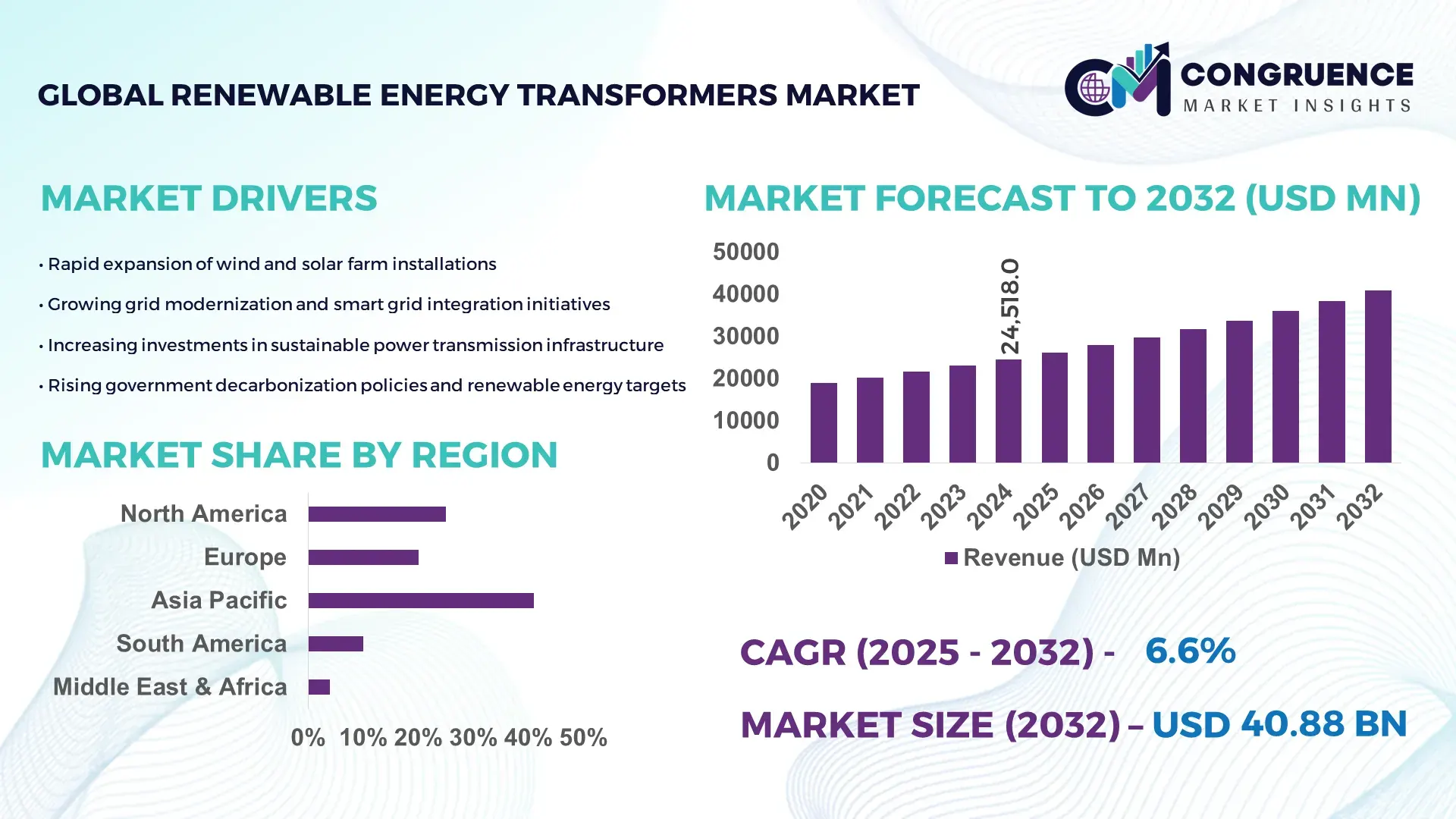

The Global Renewable Energy Transformers Market was valued at USD 24518 Million in 2024 and is anticipated to reach a value of USD 40882.99 Million by 2032 expanding at a CAGR of 6.6% between 2025 and 2032. This growth is driven by the accelerating integration of renewables into grid infrastructures worldwide.

The United States leads the global Renewable Energy Transformers Market with advanced production capabilities exceeding 120,000 MVA annually, supported by over USD 4.3 billion in grid modernization investments across renewable-heavy states. The country’s transformer ecosystem benefits from rapid deployment of utility-scale solar and wind assets, widespread application in microgrid systems, and strong technological progress in high-efficiency amorphous-core and digitally monitored transformer units. Additionally, more than 65% consumer adoption of distributed generation systems in key states enhances demand for specialized renewable transformers.

Market Size & Growth: Valued at USD 24.51 Billion in 2024, projected to reach USD 40.88 Billion by 2032 at a CAGR of 6.6%, supported by accelerated renewable integration.

Top Growth Drivers: 38% rise in solar asset installations, 27% efficiency improvement in modern transformer cores, and 41% increase in digital monitoring adoption.

Short-Term Forecast: By 2028, transformer energy losses expected to decline by nearly 18% due to optimized magnetic materials and thermal management systems.

Emerging Technologies: Adoption of AI-driven grid monitoring, amorphous metal core transformers, and solid-state transformer advancements.

Regional Leaders: North America projected to reach USD 11.6 Billion by 2032 with strong digital grid uptake; Europe expected to hit USD 10.8 Billion backed by offshore wind expansion; Asia-Pacific forecasted at USD 13.2 Billion with accelerating solar farm deployments.

Consumer/End-User Trends: Utilities account for rising adoption of high-capacity step-up transformers, while industries expand use of green power transformers to stabilize renewable-fed manufacturing operations.

Pilot or Case Example: In 2024, a U.S. utility ran a transformer digitalization pilot yielding a 22% reduction in system downtime and 17% improvement in load-balancing efficiency.

Competitive Landscape: Market leader holds ~14% share, followed by major players including Hitachi Energy, Siemens Energy, Schneider Electric, and Bharat Heavy Electricals Ltd.

Regulatory & ESG Impact: Global incentives for low-loss transformers, new environmental efficiency mandates, and carbon-neutral grid targets drive market expansion.

Investment & Funding Patterns: Over USD 5.1 Billion invested recently in renewable grid transformation projects with increased private financing of smart transformer technologies.

Innovation & Future Outlook: Advancements in self-healing insulation systems, IoT-enabled transformer diagnostics, and hybrid renewable grid projects are shaping next-generation market evolution.

The Renewable Energy Transformers Market is experiencing strong momentum across utility, industrial, and commercial sectors, each contributing significantly to market expansion through increased renewable consumption and grid connectivity requirements. Technological innovations—such as low-temperature superconducting coils, advanced thermal-resistant materials, and sensor-embedded smart transformers—are reshaping performance standards and lifecycle efficiency. Regulatory compliance with stringent energy-efficiency directives is accelerating upgrades across aging grid networks, while region-specific consumption patterns highlight rapid adoption in Asia-Pacific and Europe due to expanding wind and solar capacities. Growing emphasis on digital grid resilience, sustainability, and hybrid renewable integration continues to steer future market developments with a clear shift toward intelligent, low-loss transformer solutions.

The strategic relevance of the Renewable Energy Transformers Market is anchored in its critical role in stabilizing, integrating, and optimizing renewable power flows across modern grid networks. As global renewable generation capacity surpasses 4,000 GW, utilities and industries are sharply increasing investments in high-efficiency, digitally monitored transformer systems capable of handling intermittent energy loads, rapid voltage fluctuations, and bidirectional grid operations. Advanced solid-state transformer (SST) technology delivers up to 31% efficiency improvement compared to conventional silicon-steel transformer designs, strengthening the technological migration shaping the next decade of grid transformation. Regionally, Asia-Pacific dominates in volume, while Europe leads in adoption with nearly 46% of enterprises utilizing advanced digital monitoring solutions in transformer assets. By 2027, AI-enabled predictive maintenance is expected to reduce transformer failure incidents by nearly 29%, improving grid uptime and operational continuity. ESG compliance is also accelerating innovation trends, with firms committing to transformer-related lifecycle sustainability improvements such as 22% reduction in mineral-oil usage and enhanced recycling of metallic components by 2030. In 2024, Germany achieved a 19% reduction in grid-level energy losses through the deployment of sensor-integrated renewable transformers in high-density wind corridors. Collectively, these advancements position the Renewable Energy Transformers Market as a foundational pillar of resilience, regulatory alignment, and sustainable growth across global power infrastructures.

The rapid expansion of renewable energy assets—particularly solar PV and onshore/offshore wind—is significantly increasing the need for high-performance Renewable Energy Transformers capable of supporting fluctuating power loads and high-capacity transmission. As global renewable installations exceeded 510 GW of new capacity in 2023, transformer manufacturers recorded substantial growth in demand for step-up and grid-stabilizing units. Modern renewable sites require transformers that support voltage regulation, frequency stability, and reduced core losses, especially as utility-scale solar plants now frequently surpass 500 MW capacity. The increasing integration of distributed generation—adopted by over 60% of new commercial solar installations in 2024—further boosts the need for efficient distribution transformers with enhanced thermal stability and load-handling capabilities. Ongoing grid digitalization and real-time monitoring adoption strengthen the role of modern transformers, helping utilities manage intermittency and ensure reliable power delivery across renewable-heavy regions.

Raw material price fluctuations—particularly in electrical steel, copper, aluminum, and transformer oils—remain a significant restraint for the Renewable Energy Transformers Market. Electrical steel prices increased by more than 27% between 2021 and 2024 due to supply chain disruptions and increased global demand for energy-efficient appliances and auto components, directly impacting transformer core manufacturing costs. Copper prices also remain elevated, driven by rising demand from EVs and renewable infrastructure, resulting in higher production costs for coil windings and conductors. Many utility procurement budgets face constraints, slowing transformer replacement cycles and delaying modernization projects. Additionally, new environmental regulations on insulating oils and metals add compliance-related cost burdens to manufacturers. These cumulative pressures reduce margins, complicate long-term pricing strategies, and create project delays for utilities and industrial buyers, thereby restraining market expansion.

Digital grid modernization presents a substantial opportunity for the Renewable Energy Transformers Market, driven by the increasing adoption of smart monitoring systems, IoT-based diagnostics, and AI-enabled predictive maintenance. More than 45% of new transformer installations in 2024 integrated condition-monitoring sensors that track temperature, vibration, moisture content, and load variations in real time. Utilities pursuing grid automation initiatives are accelerating investments in intelligent transformers that reduce maintenance downtime and improve asset life by up to 25%. The shift toward HVDC transmission and hybrid renewable grids opens further opportunities for high-voltage and flexible power transformers capable of handling multidirectional energy flow. Expansion of microgrids—projected to grow by more than 17,000 new installations globally by 2030—creates additional demand for compact, high-efficiency transformers tailored to distributed energy networks. These advancements collectively unlock a multi-dimensional growth opportunity for technology-forward transformer manufacturers.

Increasing grid complexity and integration challenges related to high renewable penetration are creating notable hurdles for the Renewable Energy Transformers Market. Renewable-heavy grids experience frequent voltage instability, harmonics, and intermittent power fluctuations that demand advanced transformer capabilities beyond traditional configurations. Many existing grid infrastructures—particularly in developing economies—lack the capacity to support large-scale renewable integration, resulting in operational inefficiencies and technical losses exceeding 8–10% in some regions. Coordinating transformer upgrades with broader grid modernization projects often requires substantial capital, extended timelines, and regulatory approvals, complicating deployment cycles. Additionally, transformer manufacturers must navigate evolving standards for eco-efficiency, insulation materials, and digital communication protocols. These challenges, combined with extended lead times for high-capacity transformer production, create constraints that slow down rapid renewable integration and complicate utility planning and grid reliability efforts.

Growing Deployment of Digitally Monitored Smart Transformers: Utilities and large industrial operators are rapidly adopting digitally enabled renewable transformers equipped with IoT sensors and analytics. In 2024, over 48% of newly installed renewable transformers included real-time condition monitoring, enabling temperature tracking, harmonic detection, and load forecasting. These systems have demonstrated up to 26% reduction in unplanned outages and nearly 19% improvement in asset utilization, driving accelerated modernization across distributed and utility-scale renewable networks.

Expansion of High-Efficiency Amorphous Core and Superconducting Technologies: Transformer manufacturers are increasing production of amorphous metal core units due to their 60–70% lower core loss compared to older grain-oriented steel designs. Adoption of high-temperature superconducting elements grew by approximately 22% in 2024 as utilities sought enhanced thermal stability for wind and solar clusters. This shift supports improved grid efficiency, with pilot deployments reporting 14% lower no-load losses and a measurable drop in heat-related component failures.

Accelerated Investment in HVDC-Compatible Renewable Transformers: As global HVDC transmission builds momentum, demand for HVDC-ready renewable transformers is rising, particularly for long-distance wind and solar connectivity. HVDC-linked installations increased by 31% between 2022 and 2024, with new offshore wind corridors requiring transformers capable of handling 500–800 kV power flows. These high-capacity units deliver up to 18% higher transmission efficiency over long distances, making them central to cross-border renewable power exchange.

Rise in Modular and Prefabricated Construction Models: Modular construction practices are reshaping deployment strategies for transformer substations and renewable project installations. Nearly 55% of new renewable infrastructure projects adopted modular or prefabricated components in 2024, reporting installation timelines reduced by 28% and on-site labor requirements cut by 32%. Automated off-site fabrication enhances accuracy for pre-assembled transformer housings, supporting faster grid interconnection across Europe and North America where speed-to-deployment is a key performance metric.

The Renewable Energy Transformers Market is segmented across types, applications, and end-user categories, each shaping adoption dynamics with distinct technical and operational requirements. Type-based segmentation shows rising preference for digitally monitored, high-efficiency transformer systems aligned with renewable integration needs. Application segmentation highlights strong uptake in utility-scale projects, driven by rapid expansion of wind and solar installations demanding advanced voltage regulation and grid-stabilizing capabilities. End-user segmentation reveals utilities as the primary adopters, though industrial and commercial users are increasingly investing in transformers designed for distributed renewable systems, microgrids, and hybrid power configurations. Collectively, these segments illustrate a diversified demand environment influenced by grid modernization initiatives, technological innovations, and regional renewable capacity growth trends.

High-efficiency amorphous core transformers account for approximately 46% of total adoption, supported by their significantly lower core-loss profiles and strong suitability for solar and wind clusters requiring continuous load optimization. Their dominance is attributed to improved thermal performance and measurable reductions in no-load losses, making them the preferred choice for large-scale and distributed renewable deployments. Solid-state transformers (SSTs) represent the fastest-growing type, supported by an estimated 8.6% CAGR, driven by rising demand for bidirectional power flow, voltage regulation precision, and integration within digitally enabled smart grids. Their adoption is gaining momentum due to their 25–30% higher efficiency under variable load conditions and their compatibility with EV-charging renewable systems and hybrid grids.

Oil-immersed transformers, dry-type transformers, and specialty offshore transformers collectively hold the remaining 54% share. Though traditionally used, they now serve niche roles such as offshore substations, remote microgrids, and distributed solar farms, where ruggedness and environmental resistance remain essential.

Utility-scale renewable integration represents the leading application segment with approximately 49% market share. The dominance is driven by rapid expansion of onshore and offshore wind installations, large solar parks exceeding 300–500 MW, and nationwide grid-stabilizing upgrade programs requiring high-capacity step-up transformers. Microgrids and distributed renewable systems form the fastest-growing application segment, supported by an estimated 9.1% CAGR, with adoption rising alongside commercial solar rooftops, rural electrification programs, and industrial decarbonization initiatives. Compared to utility-scale systems that hold 49%, microgrid transformer adoption stands at 21% but is expected to surpass 30% by 2032, driven by demand for localized resilience and energy independence.

EV charging infrastructure, battery energy storage systems (BESS), and hybrid renewable plants make up the remaining 30% combined share, contributing to diversified growth. Rising adoption of BESS-linked transformers supports frequency regulation and peak-shaving applications across high-demand regions.

Utility companies account for roughly 52% of market share, making them the dominant end-user segment. Their leadership stems from large-scale renewable deployments, grid expansion initiatives, and modernization mandates requiring high-capacity step-up and digitally monitored transformers. Compared to utilities (52%), industrial end-users hold around 28% adoption, driven by decarbonization of manufacturing facilities and rising use of renewable-powered microgrid systems. The commercial sector—including tech parks, logistics complexes, and large retail chains—is the fastest-growing end-user, recording an estimated 8.3% CAGR. Adoption is driven by increasing implementation of rooftop solar, on-site battery systems, and energy-efficient building standards requiring advanced distribution transformers. Commercial renewable adoption, currently near 20%, is projected to exceed 30% by 2032 as energy-cost optimization becomes a priority.

Residential associations, community energy programs, and government facilities represent the remaining 20% combined share. Adoption is rising due to distributed solar systems, rural electrification efforts, and expansion of smart metering infrastructure that relies on advanced transformer technologies.

Asia-Pacific accounted for the largest market share at 41% in 2024; however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 7.9% between 2025 and 2032.

Asia-Pacific’s sizeable dominance is driven by large-scale solar and wind deployments exceeding 820 GW, while North America and Europe follow with 28% and 22% shares respectively, supported by strong grid modernization investments. South America captured nearly 6%, fueled by emerging renewable corridors in Brazil and Chile. The Middle East & Africa region, while still at roughly 3%, is accelerating rapidly due to over 30 GW of new renewable capacity announced for transformer-integrated hybrid projects. Regional variations in technology adoption, digital monitoring penetration (ranging from 18% in South America to 46% in Europe), and policy frameworks shape the overall segmentation landscape.

North America holds approximately 28% of the global Renewable Energy Transformers Market, supported by strong renewable penetration across wind-heavy regions such as Texas and solar-intensive states like California and Arizona. Demand is fueled by industries including utilities, data centers, manufacturing, and commercial complexes, all requiring high-efficiency grid-stabilizing transformers. The region benefits from supportive regulatory measures such as accelerated grid modernization plans and mandatory energy-efficiency upgrades for transformer fleets. Digital transformation trends—including IoT-enabled monitoring systems and AI-driven maintenance—drive growing adoption, with nearly 52% of enterprises integrating asset diagnostics into renewable transformer systems. Key local players continue deploying low-loss, dry-type transformers tailored for wildfire-prone states. Consumer behavior in the region shows higher enterprise adoption within the healthcare and finance sectors, reflecting increased dependence on stable renewable-backed power infrastructures.

Europe commands nearly 22% market share, driven by strong uptake across Germany, the UK, France, and the Netherlands. Strict sustainability mandates and stringent efficiency standards introduced by European regulatory bodies have accelerated replacement cycles for older transformer units. Adoption of emerging technologies—including amorphous core transformers and digital twin–enabled monitoring—continues rising, with digital penetration across utilities exceeding 46%. Countries such as Germany lead deployment of high-capacity offshore wind transformers, while the UK expands investments in green hydrogen–linked power corridors. Local manufacturers are increasingly supplying eco-efficient transformer variants with reduced mineral-oil use. Regional consumer behavior reflects strong demand for explainable and transparent digital systems, particularly within industrial and commercial energy users seeking greater grid visibility and regulatory compliance.

Asia-Pacific represents the world’s largest growth hub with approximately 41% of total market volume, led by China, India, Japan, and South Korea. China alone operates more than 430 GW of solar and 370 GW of wind assets, driving massive demand for high-capacity step-up and substation transformers. India’s rapid grid expansion projects and Japan’s focus on offshore wind substations further strengthen market uptake. The region is also becoming a manufacturing center for amorphous metal core transformers and modular prefabricated substations. Innovation hubs across China and South Korea are driving sensor-integrated and AI-enabled transformer designs. Consumer behavior reflects strong reliance on mobile-first energy applications and digital maintenance platforms, aligning with fast-growing e-commerce and EV ecosystems. Local players are actively expanding exports of smart transformers to Southeast Asia, contributing to regional velocity.

South America accounts for roughly 6% of global adoption, driven by increasing renewable deployments in Brazil, Chile, and Argentina. Brazil’s expanding wind corridors and Chile’s growing solar deserts generate rising demand for grid-stabilizing transformers and high-capacity distribution units. Infrastructure investments—such as new transmission lines exceeding 2,800 km across Brazil—support continued adoption of modern transformer systems. Governments offer incentives for renewable-linked substations and transformer upgrades, especially in industrial belts. Local energy companies are integrating digital monitoring to reduce maintenance disruptions in remote sites. Regional consumer behavior shows increasing dependence on renewable-powered industrial zones, with adoption often tied to language and media localization requirements across diverse commercial markets.

The Middle East & Africa region, holding nearly 3% market share, is quickly emerging as the fastest-growing renewable transformer market due to rising energy diversification initiatives. Countries such as the UAE, Saudi Arabia, Egypt, and South Africa are driving adoption with large-scale projects exceeding 30 GW collectively in solar and wind pipelines. Demand is heavily linked to oil & gas modernization, construction expansion, and industrial decarbonization programs. Regional grids are integrating digitally monitored and eco-efficient transformers to support high-temperature operating conditions and hybrid renewable layouts. Local manufacturers have begun producing solar-compatible dry-type transformers for desert environments. Consumer behavior indicates growing adoption among industrial clusters seeking stable renewable-backed power for manufacturing and mining operations.

China – 29% Market Share

Dominance driven by the world’s largest renewable installed base and extensive high-voltage transmission infrastructure supporting large-volume transformer deployment.

United States – 17% Market Share

Strong adoption supported by large-scale grid modernization programs, rapid expansion of utility-scale solar and wind, and high enterprise investment in digital transformer technologies.

The Renewable Energy Transformers market displays a moderately consolidated competitive structure, with nearly 40–50 active manufacturers operating globally and the top five companies collectively accounting for approximately 42% of the total market share in 2024. This concentration is driven by increasing technological specialization, particularly in high-efficiency dry-type transformers, digital monitoring units, and smart-grid-compatible transformer systems. Several established players have strengthened their market presence through strategic mergers, with at least six major acquisitions recorded between 2022 and 2024 targeting enhanced manufacturing capacity, regional distribution, and advanced insulation technologies.

Competition is intensifying as manufacturers invest heavily in R&D, with average R&D spending rising by nearly 18% between 2021 and 2024 across leading companies. Many competitors are focusing on grid-modernization solutions, with more than 60% integrating IoT-based monitoring modules and predictive maintenance analytics into transformer designs. Regional expansion strategies have also accelerated, as companies recorded over 25 new partnership agreements with renewable developers and utility providers to secure large-scale solar and wind procurement contracts.

The market is further shaped by rapid product innovation cycles, with over 30 new high-efficiency transformer models introduced globally in the last two years. Manufacturers are increasingly differentiating through sustainability initiatives, including the use of biodegradable ester oils, which now represent nearly 12% of all transformer fluid applications. Collectively, these strategic moves underline a competitive environment driven by technological leadership, efficiency improvements, energy-loss reduction, and compliance with evolving renewable integration standards.

Hitachi Energy

General Electric

Mitsubishi Electric Corporation

CG Power & Industrial Solutions

Eaton Corporation

Toshiba Energy Systems & Solutions Corporation

Hyundai Electric & Energy Systems

Wilson Transformers

Bharat Heavy Electricals Limited (BHEL)

Technology adoption in the Renewable Energy Transformers market is accelerating as power systems transition toward higher renewable penetration, decentralized grids, and digital monitoring frameworks. Advanced transformer designs now integrate high-efficiency amorphous metal cores, which reduce no-load losses by up to 70%, significantly improving grid sustainability. Power ratings above 50 MVA are increasingly deployed across large-scale wind and solar farms, supporting frequency stability and voltage regulation for installations exceeding 500 MW. Digital transformers equipped with IoT sensors and edge analytics currently represent nearly 38% of new installations, enabling real-time diagnostics, predictive maintenance, and up to 25% reduction in operational downtime.

Eco-friendly insulating fluids, including ester-based oils, are gaining strong traction, accounting for over 30% of environmentally compliant transformer deployments in 2024. These fluids enhance fire safety and offer biodegradable properties, making them highly suitable for offshore wind platforms and remote solar projects. Solid-state transformer (SST) prototypes are also advancing, supported by high-power semiconductor devices that allow voltage conversion efficiencies above 97%, offering a compact alternative for EV charging grids and distributed renewable systems.

On-grid integration technologies such as advanced tap changers, digital relays, and high-temperature superconducting (HTS) materials are further enhancing efficiency. HTS-enabled systems demonstrate current-carrying capabilities 100 times greater than conventional copper components, allowing reduced transformer sizes in urban renewable installations. Modular transformer units with standardized interfaces now enable scalability for multi-megawatt solar parks, reducing installation time by nearly 40%. Collectively, these innovations are reshaping performance, reliability, and sustainability benchmarks across the Renewable Energy Transformers market.

In 2023–2024, ABB launched its “Transformer Intelligence™” service based on a next-generation CoreTec™ system enhanced with the CoreSense™ sensor, enabling continuous real-time recording of hydrogen and moisture for predictive maintenance and extended transformer life.

ABB also introduced the world’s first digital distribution transformer, the TXpert™, integrating cloud-connected sensing and monitoring to optimize reliability, reduce maintenance, and provide lifecycle intelligence.

In early 2024, Schneider Electric rolled out its EcoStruxure™ Transformer Expert platform in the UK and Ireland, deploying IoT sensors for real-time health analytics on oil transformers. This solution has been adopted by CERN for monitoring eight critical transformers.

Hitachi Energy committed to a further investment of US$ 4.5 billion by 2027 for capacity expansion, modernization, and R&D in transformer manufacturing, including adding 2,000 employees in Sweden and scaling its Innovation Center in India to more than 4,000 staff.

The report encompasses a comprehensive analysis of the Renewable Energy Transformers market by segmenting it across product types, applications, and end-user categories, offering a detailed view into both traditional and emerging transformer technologies — including amorphous-core, solid-state, dry-type, and modular units. It also covers various applications such as utility-scale grid integration, microgrids, distributed generation, battery storage systems, and EV charging infrastructure to reflect evolving usage patterns. Geographically, the analysis spans major regions — North America, Europe, Asia-Pacific, South America, and Middle East & Africa — assessing regional infrastructure trends, regulatory drivers, and capacity build-outs. The report further delves into technology themes, such as IoT-enabled digital monitoring, predictive maintenance, eco-friendly insulating fluids, and high-voltage superconducting materials. From an industry focus perspective, it highlights utilities, industrial, commercial, and government end-users, mapping adoption behavior, upgrade cycles, and procurement strategies. Emerging or niche segments — such as hybrid renewable substations, modular prefabricated transformer units, and grid-connected solid-state transformers — are also addressed to capture future growth pathways. By integrating data on order backlogs, manufacturing expansions, innovation investments, and digital service offerings, the report equips decision-makers with actionable insights to navigate market dynamics, technology opportunities, and regulatory landscapes.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 24518 Million |

|

Market Revenue in 2032 |

USD 40882.99 Million |

|

CAGR (2025 - 2032) |

6.6% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Siemens Energy, ABB Ltd., Schneider Electric, Hitachi Energy, General Electric, Mitsubishi Electric Corporation, CG Power & Industrial Solutions, Eaton Corporation, Toshiba Energy Systems & Solutions Corporation, Hyundai Electric & Energy Systems, Wilson Transformers, Bharat Heavy Electricals Limited (BHEL) |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |