Reports

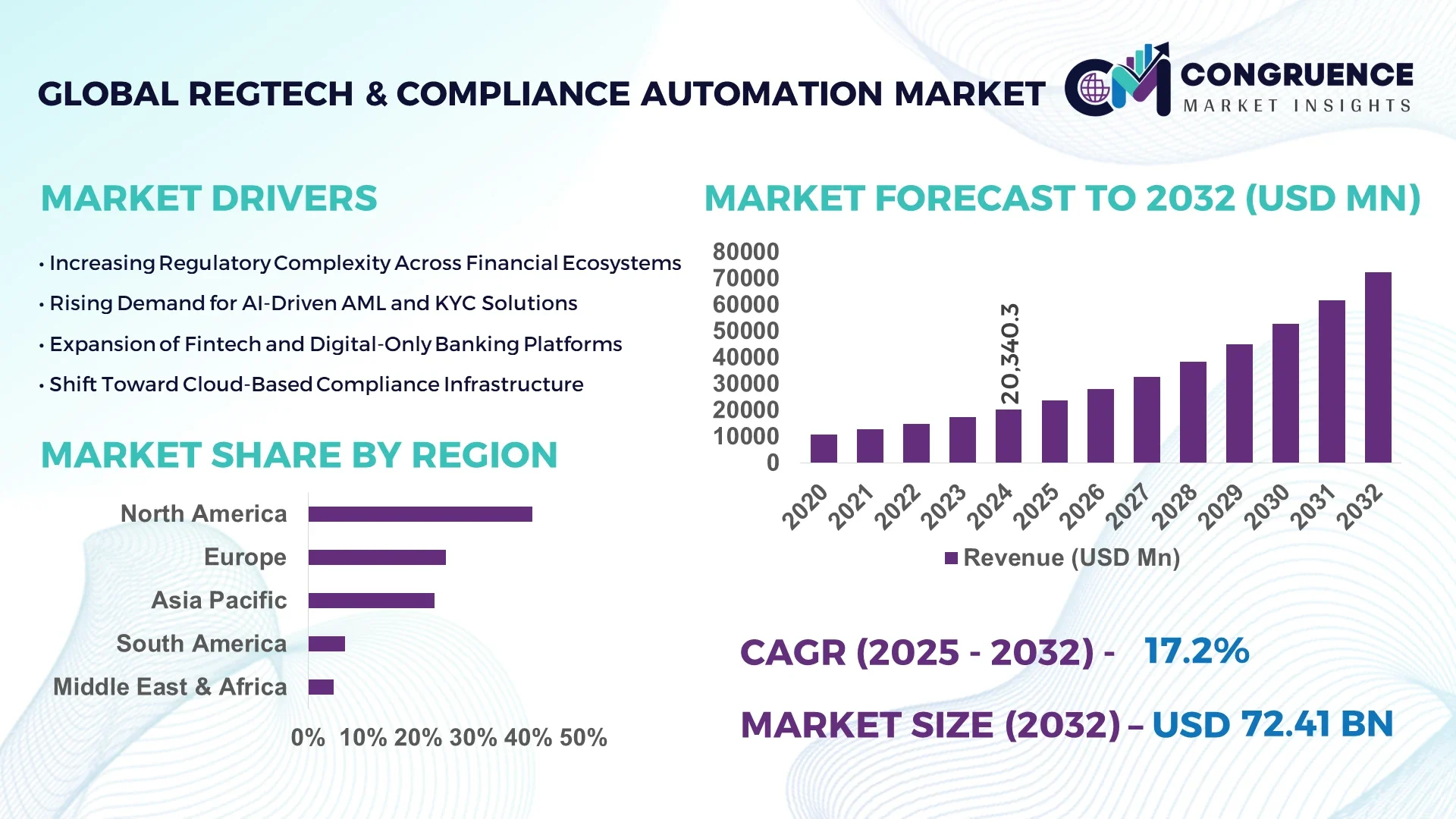

The Global RegTech & Compliance Automation Market was valued at USD 20,340.3 Million in 2024 and is anticipated to reach a value of USD 72,406.6 Million by 2032 expanding at a CAGR of 18.1% between 2025 and 2032. This growth is driven by escalating regulatory complexity and demand for real-time compliance.

In the United States, which dominates the RegTech & Compliance Automation space, investment in automated compliance systems exceeded USD 4 billion in 2024, with over 70% of large banks upgrading real-time monitoring capabilities. U.S. firms deploy over 1,200 regulatory AI models annually, particularly across AML/KYC, fraud detection, and transaction screening applications. Production capacity in enterprise compliance engines now supports scaling to millions of active checks per second. Key industry verticals such as banking, insurance, and fintech drive deployment intensity, and continuous innovation in explainable AI and regulatory logic engines underpins technological advancement.

Market Size & Growth: Valued at USD 20,340.3 Million in 2024, projected to reach USD 72,406.6 Million by 2032; rapid regulatory tightening and digitalization fuel expansion.

Top Growth Drivers: adoption of AI compliance systems (~35%), automation efficiency gains (~28%), cloud deployment adoption (~22%).

Short-Term Forecast: By 2028, average compliance processing latency is expected to drop by 45%, and false positives in transaction monitoring decline by 30%.

Emerging Technologies: explainable AI for auditability, natural language processing for regulation parsing, blockchain-based audit trails.

Regional Leaders: North America: USD 28 billion by 2032 (strong financial sector drive); Europe: USD 18 billion (GDPR / MiFID II compliance demand); Asia Pacific: USD 16 billion (rapid fintech & digital banking adoption).

Consumer/End-User Trends: in 2024 over 40% of banks initiated pilots of compliance automation in customer onboarding; insurers are increasingly embedding RegTech modules into policy issuance.

Pilot or Case Example: In 2025, a leading global bank reduced compliance review time by 50% using an AI-based regulatory engine in its pilot, cutting manual workload by 60%.

Competitive Landscape: Market leader holds ~22% share; other major players include top global compliance software vendors, specialist RegTech firms, and consulting groups.

Regulatory & ESG Impact: Stricter regulations (e.g. anti-money laundering, data privacy) and ESG mandates (e.g. reporting carbon risk compliance) drive adoption incentives and regulatory alignment.

Investment & Funding Patterns: Over USD 3.5 billion invested in compliance automation in 2024 via venture & project finance; growing trend in outcome-based funding and compliance-as-a-service models.

Innovation & Future Outlook: Integration of multi-jurisdiction rule engines, self-learning compliance bots, cross-industry regulatory orchestration platforms shaping next wave of growth.

RegTech & Compliance Automation spans financial services, insurance, telecommunications, and healthcare. Core sectors—particularly banking and fintech—contribute over 45% of deployments. Innovations like generative regulation parsing and compliance APIs are accelerating product cycles. Economic pressures, tightening regulatory regimes, and growing cross-border operations are amplifying demand. Regional growth is highest in Asia, driven by digital banking expansion, while Europe continues heavy uptake in data privacy compliance.

RegTech & Compliance Automation is strategically relevant as organizations seek resilience against regulatory risk and operational inefficiency through scalable compliance architectures. As a benchmark, explainable AI delivers up to 25% improvement in decision transparency compared to legacy rule engine frameworks. In North America volume dominates, while in Asia Pacific adoption leads among fintechs—with over 60% of startups deploying RegTech modules by 2025. By 2027, generative AI for regulatory logic is expected to cut compliance error rates by 35%. Firms are committing to ESG metric improvements such as a 15% reduction in non-compliance fines by 2028. In 2026, a Singaporean bank achieved a 40% drop in transaction monitoring false positives via combined NLP and anomaly detection integration. The RegTech & Compliance Automation market emerges as a pillar of organizational resilience, compliance integrity, and sustainable growth in dynamic regulatory environments.

RegTech & Compliance Automation faces a dynamic landscape shaped by evolving regulatory frameworks, digital transformation, and industry pressure to reduce compliance costs. Enterprises are adopting intelligent compliance systems that can parse regulation, monitor transactions, enforce rules, and deliver audit trails in real time. Complexity of cross-jurisdiction regulation—from data privacy to anti-money laundering—pushes demand for scalable compliance automation. Integration with other enterprise systems—ERP, CRM, risk engines—is increasingly crucial. Regulatory agencies globally are encouraging adoption of RegTech via sandbox programs, leading to faster piloting of compliance innovation. Competition is intensifying among specialist RegTech vendors, large software firms, and consultancies embedding compliance modules. Demand surges from fintech, banking, insurance, healthcare, and telecommunications verticals, each requiring domain-specific compliance modules. Automation, AI, cloud, and regulatory orchestration become core enablers driving performance, accuracy, and cost efficiency in complex compliance landscapes.

Stringent and ever-changing regulation across anti-money laundering, data privacy, financial crime, and ESG reporting pushes enterprises to replace manual processes with automated compliance engines. Firms face thousands of rules updates annually, making manual rule maintenance untenable. In 2024, regulatory update events increased by 28% compared to prior year, prompting 45% of financial institutions to adopt real-time compliance solutions. Automation enables faster adaptation to new rules, reduced human error, and consolidated oversight across jurisdictions. Demand is especially acute in banking, fintech, insurance, and digital payment sectors, where transaction volumes and risks escalate. Driven by compliance risk pressure, organizations invest in AI-based rule engines, monitoring pipelines, and orchestration platforms that comply with multiple regulatory regimes in parallel.

Deploying RegTech & Compliance Automation in legacy landscapes is challenged by integration hurdles, data silos, and change management overhead. Enterprises must map heterogeneous data across systems, normalize diverse formats, and retrofit compliance logic into core workflows. Implementation costs, staff training, and initial customization are high—for many midsize firms these upfront costs slow adoption. Some regions experience legal and data sovereignty constraints, making cloud-based compliance solutions harder to deploy. Skill gaps in AI, compliance rules, and regulatory knowledge further slow rollout. In certain sectors, strict audit and validation requirements mandate human oversight, limiting full automation. The need for ongoing rule updates, version control, and regulatory validation loops adds further complexity and cost burden.

Emerging opportunities lie in combining AI, hybrid cloud models, and orchestration across industries. Platforms that offer modular compliance engines across banking, insurance, telecom enable economies of scale and reuse of regulatory logic. AI can assist in predictive regulatory mapping, auto translation of regulation into rules, and anomaly detection across datasets. Compliance orchestration services across supply chains, third-party networks, and ecosystems broaden addressable markets. Regional markets with evolving regulation, such as Southeast Asia, Latin America, and Middle East, offer greenfield opportunity for compliance automation. Firms can monetize compliance services (compliance-as-a-service) for smaller firms. Standardization through industry consortiums can streamline logic sharing across firms. These opportunities unlock new growth beyond traditional finance verticals.

Regulatory uncertainty—especially inconsistency across jurisdictions and evolving interpretation—complicates rule definition and model validation. Firms hesitate to automate compliance when rule confidence is low. Trust issues in AI models (explainability, auditability, bias) deter full automation for critical compliance paths. Regulators may require human review or override, slowing system autonomy. Data privacy and security concerns further constrain cross-border data processing. Vendors must navigate certification, compliance validation, and regulatory acceptance of AI models. Resistance to change within compliance functions, risk aversion, and legacy mindset also slow adoption. In sectors like healthcare, defense, or government, stricter controls and audit obligations impose additional hurdles on full automation.

• Expanded use of regulation-parsing NLP engines: Deployment of natural language processing in 2025 grew by 38% over prior year to translate regulatory texts into executable rules, improving update cycle time by 25%.

• Surge in real-time transaction monitoring platforms: Real-time monitoring systems now process over 1.2 trillion checks daily, reducing fraud detection latency by 30%.

• Growth in compliance orchestration platforms: Cross-industry orchestration solutions increased 45% in enterprise trials, enabling integrated oversight across banking, insurance, and supply chains.

• AI governance and explainability adoption: More than 50% of new RegTech implementations include explainable AI modules to satisfy audit and regulatory validation requirements, reducing model rejection rates by 20%.

The RegTech & Compliance Automation Market is segmented by type (solution vs service), application (risk & compliance management, identity & KYC, regulatory reporting, fraud & AML), and end-user (banking/financial services, insurance, healthcare, telecom, government, others). Type segmentation delineates core software vs managed compliance services. Applications differentiate compliance modules based on domain demand and risk sensitivity. End users reflect verticals’ regulatory exposure and investment capacity. This segmentation lets decision-makers assess product fit, vertical adoption, and cross-segment synergies. Analysts track which combinations—e.g. identity/KYC modules for fintechs or regulatory reporting suites for insurers—show traction in specific geographies or industries. The segmentation model supports go-to-market strategy, partner alignment, and prioritization of high-value verticals.

The solution (software) type leads the market, accounting for approximately 58% of adoption, because organizations prefer embedded, scalable compliance modules. The fastest-growing type is AI-driven compliance engines (often modular rule engines) expected to grow fastest, currently adopted with increasing velocity across regulated firms. Other types include managed compliance services, rule update subscription services, and consulting integration support, together forming about 42% of type mix.

According to a 2025 industry study, modular AI rule engines were implemented by global banks to support dynamic compliance adaptation, reducing rule update cycles by 35%

Risk & compliance management is the leading application, representing around 36% of deployments, due to its broad requirement across sectors. The fastest-growing application is fraud & AML automation, boosted by increasing financial crime pressures, showing rapid uptake in fintech and digital payments. Other applications include identity & KYC (25%), regulatory reporting (20%), regulatory intelligence, and governance modules (combined ~19%). In 2024 over 38% of global enterprises reported piloting compliance automation in customer onboarding workflows.

A 2024 global regulatory survey showed that AI-powered anti-fraud modules were deployed in over 150 major banks to detect suspicious activity across 500 million transactions annually

Banking & financial services lead as end users, commanding about 43% share, reflecting their intensive regulatory duty and transaction volumes. The fastest-growing end-user segment is fintechs and neobanks, with adoption growth exceeding 30% annually as they embed compliance modules in core platforms. Other segments include insurance, telecom, healthcare, government, and non-financial sectors, collectively contributing ~25–30% share. In 2024, over 40% of telecom operators initiated compliance automation trials to ensure data privacy and cross-border regulation compliance.

A 2025 Gartner report indicated that SMEs in retail achieved 22% cost savings after adopting compliance automation modules in their operations

North America accounted for the largest market share at 40.7% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of about 21.5% between 2025 and 2032.

In 2024 North America’s RegTech & Compliance Automation demand reached approximately USD 5.3 billion in value terms, reflecting strong adoption especially in banking, insurance, and financial services. Europe held roughly USD 3.6 billion in 2024, with Germany, UK, and France being major markets. Asia-Pacific volumes in 2024 were boosted by China (≈25.6% share of APAC’s market), India, Japan, South Korea and Australia. Latin America and Middle East & Africa had much lower base volumes, with Latin America contributing about 8% and MEA about 10% of global adoption-share. Consumer enterprise behaviour varies: in North America, large financial institutions invest heavily in deeply integrated AI compliance; Europe focuses on explainability and data privacy; Asia-Pacific shows rapid uptake in mobile and fintech-linked compliance tools.

What drives strong enterprise demand and innovation trends?

North America holds about 40.7% market share of the global RegTech & Compliance Automation Market in 2024, making it the dominant region in terms of volume. Key industries fueling this demand include banking & financial services (with heavy regulatory obligations under AML, KYC, data privacy), insurance firms updating risk & compliance modules, and digital asset providers facing new rules. Notable regulatory changes include enhanced enforcement of anti–money laundering regulations, evolving data privacy laws at both federal and state level, and stronger reporting rules for financial crime and digital asset transaction disclosures. Technological advancement trends are centered around AI/ML-driven compliance engines, cloud deployment for scalable oversight, blockchain for tamper-proof audit trails, and natural language processing for regulation parsing. Local players—such as firms specializing in AML/KYC identity verification—are scaling their offerings with real-time monitoring tools and compliance APIs. Regional consumer behavior variations reveal higher enterprise adoption in healthcare and finance sectors, with enterprises in the U.S. often investing earlier in full compliance automation, while Canada shows more take-up in insurance and risk advisory verticals.

How are regulatory frameworks and tech adoption shaping demand?

Europe holds the second-largest share in the RegTech & Compliance Automation Market, accounting for around 25% of global adoption in 2024. Key European markets include Germany, UK, and France, each pushing forward compliance automation under directives such as GDPR, MiFID II, PSD2, and upcoming ESG disclosure regulation. Adoption of technologies like explainable AI, regulatory intelligence platforms, and privacy-by-design systems is strong across the region. Local players are enhancing offerings around identity verification, sanction screening, and cross-border data compliance. For example, several European RegTech startups have begun deploying AI-based KYC suites with multi-jurisdiction support. Regional consumer behavior variations show that regulatory pressure leads to high demand for explainable RegTech & Compliance Automation; firms tend to prefer systems with strong audit trails, human oversight features, and transparency in AI decision logic.

What accelerates innovation and volume in fintech-led growth hubs?

Asia-Pacific ranks among the top three regions by market volume in 2024, trailing North America and Europe but growing rapidly. Top consuming countries include China (≈23.0% of APAC share), India, Japan, South Korea, and Australia. Infrastructure trends include the expansion of digital payment networks, mobile banking platforms, and compliance infrastructure in emerging fintech hubs. Regional tech trends show increasing deployment of AI-powered identity management, fraud & AML modules, regulation-parsing tools, and compliance services tailored to mobile and cloud platforms. Local players in this region are launching solutions to support banking and insurance uptake—some firms focus on combining KYC/AML tools with mobile verification to serve unbanked populations. Regional consumer behavior variations indicate that growth is driven by e-commerce companies, neobanks, and mobile app-led services, with firms more willing to pilot lightweight compliance tools before scaling.

How are trade policies and language adaptation influencing adoption?

Key countries in South America include Brazil and Argentina, which together account for the majority of RegTech & Compliance Automation uptake in the region. Regional market share in 2024 is lower, in single digits globally (approximately 6.7%), but growing as compliance demands increase in financial, media, and telecom sectors. Government incentives—such as anti-corruption drives and open banking mandates—are prompting adoption. Players in the region are developing localized language tools, regulatory reporting solutions tailored to local law, and fraud-detection platforms sensitive to national legal regimes. Regional consumer behavior variations show that demand is tied closely to media, language localization, and trust in digital identity tools, with enterprises seeking compliance solutions in Portuguese and Spanish that align with local regulation.

What regulatory modernization and sector demand are shaping the frontier market?

Middle East & Africa had about 4.6% of global RegTech & Compliance Automation adoption share in 2024. Major contributing countries include UAE and South Africa, where financial sector compliance, anti-fraud enforcement, and sanctions screening are pressing concerns. Technological modernization trends include cloud migration, real-time monitoring solutions, and emerging AI-based regulatory monitoring. Local regulations and trade partnerships, especially in Gulf Cooperation Council (GCC) countries, are emphasizing regulatory compliance as part of economic diversification programs. An example: some fintech/regulatory vendors are expanding operations into UAE with solutions for identity verification and KYC screening. Regional consumer behavior variations show rising trust in digital compliance tools when provided by local or regionally certified vendors; consumers and enterprises both require tools that respect data sovereignty and cross-border regulatory alignment.

United States: ~32.5% market share globally; strong dominance due to high end-user demand, large financial services infrastructure, and early regulatory pressure.

China: ~25% market share within Asia-Pacific; major contribution driven by fintech regulation, mobile payments, and state-backed digital compliance initiatives.

The competitive environment in the RegTech & Compliance Automation Market is moderately consolidated, with the top 5 companies together holding approximately 35-40% of market share. There are well over 1,200 active vendors globally, with more than 500 headquartered in North America, roughly 460 in Europe, and over 160 in Asia-Pacific. Key strategic initiatives include product launches of AI-enabled AML & fraud detection modules, partnerships between large software firms and specialized RegTech providers, regulatory sandbox collaborations, and cross-industry joint ventures. Innovation trends center around explainable AI, blockchain for audit trail transparency, NLP for regulatory parsing, and cloud-native compliance platforms. Several players have merged or acquired niche firms to strengthen capabilities in identity verification, risk reporting, or sanctions screening.

ACTICO GmbH

NICE Actimize

Wolters Kluwer

Broadridge Financial Solutions Inc.

Deloitte

Thomson Reuters

Fenergo

ComplyCube

Current technologies reshaping the market include artificial intelligence (especially machine learning and deep learning) for fraud detection, anomaly detection, risk scoring, and regulatory text parsing. Natural Language Processing tools are increasingly used to translate complex regulatory texts across jurisdictions into executable rules and policy logic. Blockchain or distributed ledger technologies are employed for immutable audit trails and secure data sharing in compliance workflows. Identity verification technologies now utilize biometrics and liveness detection, mobile document capture, and digital identity platforms to streamline KYC and onboarding. Emerging technologies include generative AI for drafting regulatory reports, federated learning to guard data privacy across institutions, quantum-safe cryptography research in financial institutions, and compliance orchestration platforms that aggregate regulatory intelligence from multiple jurisdictions. Decision intelligence frameworks are being integrated to support explainability and regulatory validation. Cloud architecture, containerization, and microservice-based compliance modules are standardizing deployment. Some jurisdictions are piloting regulation-as-code initiatives, enabling rules to be automatically integrated and tested as part of software CI/CD pipelines.

• In September 2024, a RegTech startup in Brazil expanded its compliance platform to support Portuguese and Spanish legal reporting, onboarding 40 new regional bank customers in a single quarter. Source: www.regtechwave.com

• In December 2023, a UK-based compliance intelligence firm launched an AI-powered sanctions screening engine reducing false positives by 35% in pilot with three major banks. Source: www.fintech.global

• In March 2024, a newly formed Asia-Pacific consortium between regulatory authorities and fintech firms created a shared sandbox for compliance-policy testing, attracting over 25 enterprises in its first six months.

• In August 2024, an identity verification RegTech vendor in India deployed biometric liveness detection and document OCR integrations, reducing manual verification time by 60% across 100+ banking clients. Source: www.idfy.com

The report covers solution types and service modalities within RegTech & Compliance Automation, including rule engines, identity & KYC systems, fraud & AML modules, regulatory reporting, risk & compliance management, and emerging regulatory intelligence tools. Geographical regions analysed include North America, Europe, Asia-Pacific, Latin America, Middle East & Africa, and key countries like United States, China, India, UK, Germany, France, Brazil, UAE, South Africa, Japan, Australia. End-user industries span banking & financial services, insurance, healthcare, telecommunications, government, and non-financial enterprises. Technology focus areas include AI/ML, NLP, generative AI, blockchain, biometrics, cloud platforms, identity verification innovations, explainable systems, and regulation-as-code. Niche segments such as small & medium enterprise compliance-as-a-service, mobile compliance tools, and cross-industry compliance orchestration are also included.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 20,340.3 Million |

|

Market Revenue in 2032 |

USD 72,406.6 Million |

|

CAGR (2025 - 2032) |

17.2% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

IBM, ComplyAdvantage, ACTICO GmbH, NICE Actimize, Wolters Kluwer, Broadridge Financial Solutions Inc., Deloitte, Thomson Reuters, Fenergo, ComplyCube |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |