Reports

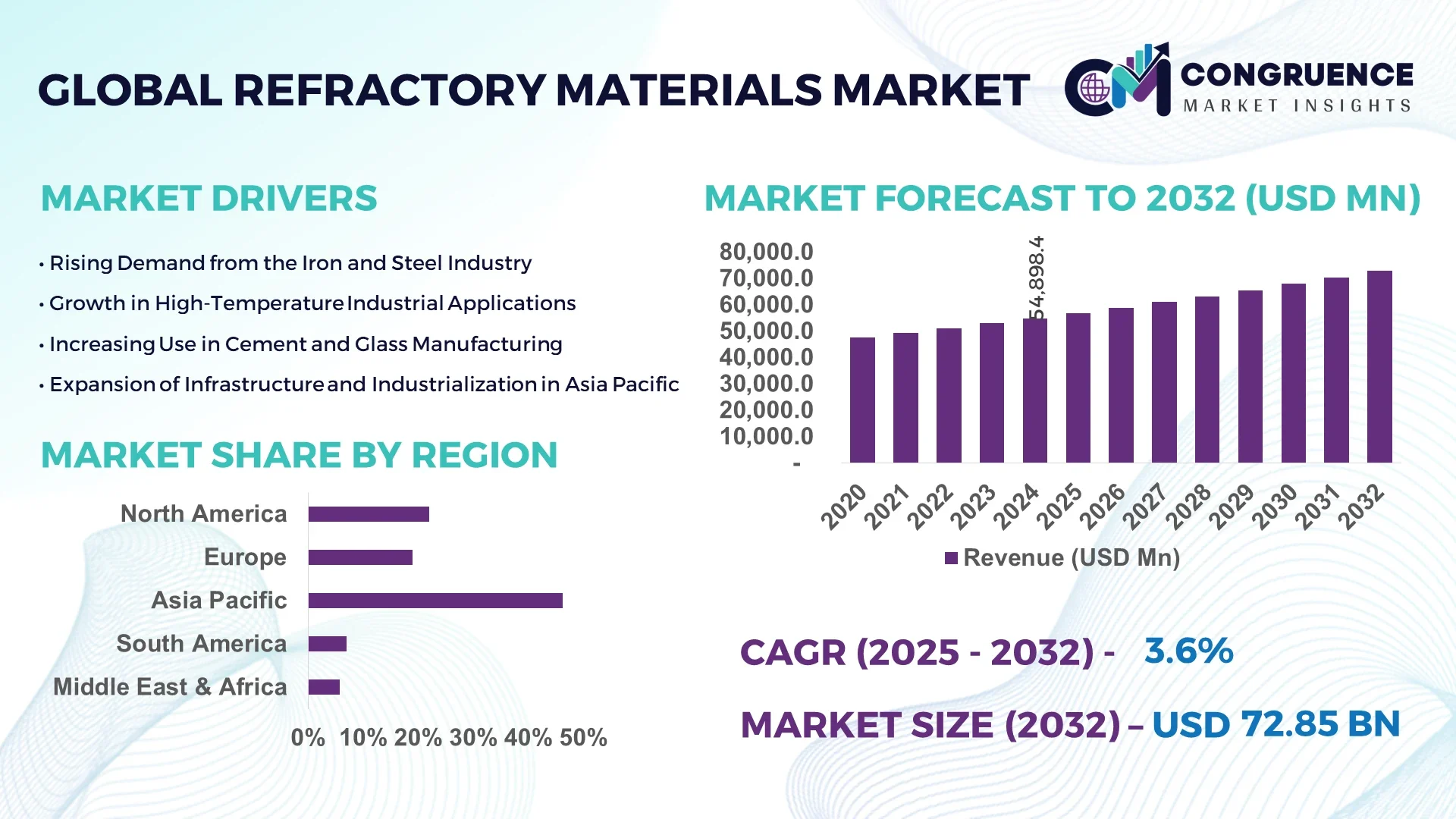

The Global Refractory Materials Market was valued at USD 54,898.4 Million in 2024 and is anticipated to reach a value of USD 72,851.4 Million by 2032, expanding at a CAGR of 3.6% between 2025 and 2032.

To Learn More About This Report, Request A Free Sample Copy

China remains a critical player in the refractory materials industry, supported by extensive production capacity across provinces like Henan and Shandong, massive state-backed investments in fire-resistant ceramics, and integration of refractory materials in large-scale steel and cement production lines. The country’s industry is also distinguished by high-temperature process innovations, including automated brick-lining systems and heat-efficient insulating materials.

The Refractory Materials Market continues to gain traction across major industries such as steel, non-ferrous metals, cement, and glass, with steel manufacturing alone accounting for over 60% of global consumption. Growing demand for energy-efficient and durable refractories in high-temperature industrial processes is driving innovation, particularly in unshaped and monolithic refractories. The market is further shaped by strict environmental compliance regulations, pushing manufacturers toward low-emission, recyclable formulations. Innovations in advanced ceramic coatings and nanomaterial-enhanced refractories are enabling extended service life and reduced downtime in industrial furnaces and kilns. Regional consumption patterns are evolving, with Southeast Asia and the Middle East emerging as growth hotspots due to expanding metallurgical infrastructure. The future outlook points toward increased customization, higher automation, and smart refractory monitoring technologies to support operational reliability and cost-efficiency in high-temperature operations.

Artificial intelligence is reshaping the operational dynamics of the Refractory Materials Market by introducing intelligent automation, predictive analytics, and process optimization tools across the manufacturing and application stages. AI-integrated systems are enabling real-time quality monitoring during the production of refractory bricks and castables, reducing human error and material wastage. Through advanced machine learning models, manufacturers are now able to forecast wear patterns in furnace linings, allowing for predictive maintenance and extending operational uptime in steel and glass production.

In refractory installation, AI-powered robotics and computer vision are improving precision in lining placements, ensuring tighter tolerances and better thermal performance. AI also contributes to customized refractory solutions by analyzing process-specific thermal loads and chemical environments, thereby recommending optimal formulations based on historical performance data. Smart sensors embedded in refractory linings, connected via AI-powered platforms, are enhancing performance tracking by continuously monitoring temperature gradients, erosion rates, and mechanical stress in real-time.

Furthermore, AI is helping manufacturers reduce energy consumption during sintering and calcination processes by fine-tuning kiln temperatures and residence times based on real-time feedback loops. This not only optimizes energy usage but also improves the final product's density and resistance. As a result, the Refractory Materials Market is transitioning toward an era of digitalized production, operational efficiency, and customized high-performance solutions.

"In 2024, a leading refractory producer in Europe implemented an AI-driven monitoring system across its magnesia-carbon brick production lines, achieving a 17% reduction in manufacturing defects and cutting quality inspection time by over 30%, significantly improving overall throughput efficiency."

Advancements in high-temperature technology are driving growth within the Refractory Materials Market, particularly through the development of next-generation materials that offer improved thermal shock resistance, chemical inertness, and lifecycle durability. These innovations are especially vital in industries such as steelmaking, where furnace linings are subjected to rapid heating and cooling cycles. The integration of nanomaterials and fiber-reinforced composites has extended the lifespan of refractory linings by 20–30% compared to traditional bricks. Additionally, the deployment of smart sensors embedded in refractory linings allows for real-time thermal data analysis and maintenance scheduling, optimizing operational uptime. Innovations in unshaped refractory products, such as low-cement castables and gel-bonded formulations, also contribute to faster installation times and enhanced performance. These developments are increasing the reliability and efficiency of critical industrial processes, reinforcing the demand for advanced refractory solutions globally.

The Refractory Materials Market faces considerable restraint due to the fluctuating availability and pricing of essential raw materials like bauxite, magnesite, and graphite. Global mining disruptions, geopolitical tensions, and environmental restrictions in major producing countries have resulted in unpredictable supply patterns. For instance, export regulations on fused magnesia from China and rising transportation costs have led to a surge in raw material expenses, impacting the profitability of refractory manufacturers. In addition, limited reserves of high-purity minerals in alternative regions restrict diversification opportunities. This cost volatility creates uncertainty for procurement planning and production scheduling, forcing companies to seek more sustainable and substitute materials, which may not always match the performance standards of traditional inputs. Such instability in raw material supply chains hampers production scalability and delays delivery schedules in downstream industries.

Emerging economies in Asia-Pacific, Africa, and Latin America are creating substantial opportunities for the Refractory Materials Market as they invest heavily in steel and cement infrastructure projects. Countries such as India, Vietnam, and Indonesia are expanding their integrated steel plants and ramping up urbanization-driven cement production, leading to a surge in refractory demand. India alone added over 30 million tonnes to its annual steel output capacity between 2022 and 2024, triggering a significant uptick in local refractory consumption. Furthermore, infrastructure initiatives under government programs such as “Make in India” and “Belt and Road Initiative” are accelerating industrialization, directly benefiting refractory usage. Market players that can localize production and adapt to region-specific requirements—including high-abrasion resistance for cement kilns or corrosion-resistant linings for iron smelting—stand to gain considerable competitive advantage in these high-growth territories.

Environmental compliance is an escalating challenge for the Refractory Materials Market, as global governments tighten regulations on carbon emissions, hazardous waste disposal, and industrial furnace operations. Traditional refractory manufacturing processes involve high energy consumption and release significant greenhouse gases during sintering and calcination. Additionally, disposal of used refractories—particularly those containing chromium or other hazardous substances—must now meet strict guidelines under environmental safety laws. The cost and complexity of compliance with these evolving standards have forced many manufacturers to overhaul production lines, invest in emission control technologies, and redesign products using environmentally benign alternatives. However, such transitions often require high capital expenditure and technical adaptation, posing operational burdens, particularly for small and medium-sized enterprises. Balancing ecological responsibility with production efficiency remains a key hurdle that will shape the future competitiveness of refractory suppliers globally.

• Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Refractory Materials Market. With off-site prefabrication gaining traction, especially in Europe and North America, manufacturers are investing in high-precision refractory cutting and forming machines. These technologies allow for quicker, more uniform installation of refractory linings in furnaces and reactors, reducing labor dependency by up to 40%. This trend is further driven by construction firms seeking faster turnaround on industrial projects and lower safety risks on-site.

• Shift Toward Monolithic and Unshaped Refractories: Monolithic refractories now represent a growing share of market demand due to their ease of application, reduced installation time, and superior thermal performance. In iron and steel plants, monolithic products have replaced traditional bricks in several linings due to their enhanced resistance to thermal shocks and abrasion. Adoption is particularly strong in Asia-Pacific, where infrastructure growth is driving industrial furnace deployment, creating heightened need for these versatile materials.

• Use of Recycled and Eco-Friendly Refractory Materials: Environmental mandates and cost pressures are pushing manufacturers toward recycling used refractory waste. Refractory materials made from recycled magnesia-carbon and alumina bricks are increasingly used in secondary steelmaking and cement kilns. Recycled content usage in refractory production increased by over 25% in 2024, significantly lowering the carbon footprint while maintaining material quality and performance for mid-to-high temperature applications.

• Integration of Smart Monitoring Systems in Industrial Furnaces: Smart refractory technologies are emerging as a competitive differentiator. Embedded temperature and erosion sensors now provide real-time performance data, enabling predictive maintenance and longer refractory life cycles. In steel plants, the adoption of such systems has improved furnace uptime by over 12% annually. These smart systems are increasingly being integrated with AI-driven control software, improving process efficiency, especially in high-output industrial settings.

The Refractory Materials Market is segmented across three core dimensions: type, application, and end-user. By type, products are classified into bricks and shapes, monolithic refractories, insulating materials, ceramic fiber, and others. Among these, monolithic and unshaped refractories are experiencing increased adoption due to operational efficiency benefits and customization capabilities. Application-wise, the market serves key industrial segments such as steel, cement, glass, non-ferrous metallurgy, and petrochemicals. Steelmaking leads the application category, supported by consistent infrastructure growth and high furnace demand. In terms of end-users, industries such as iron & steel, non-ferrous metals, cement, energy, and chemical processing are the dominant consumers, with the iron & steel sector accounting for the highest consumption share. Notably, demand from the energy sector—particularly in waste-to-energy and hydrogen-based applications—is rising. This segmentation helps manufacturers and suppliers target product innovation and geographic expansion strategies more effectively.

Bricks and shapes remain a widely used product in the Refractory Materials Market, especially in high-load zones of furnaces requiring structural stability. However, monolithic refractories have become the leading type, primarily due to their flexibility, ease of installation, and ability to conform to complex geometries. These unshaped materials reduce installation downtime and can be directly cast, gunned, or rammed, offering better adherence and durability in extreme conditions. The fastest-growing type is ceramic fiber, largely driven by increasing demand for lightweight insulation and energy-saving solutions in high-temperature processes. Ceramic fibers offer low thermal conductivity and high temperature resistance, making them ideal for linings in kilns, boilers, and furnaces in the glass and aluminum industries. Other product types such as insulating castables and precast shapes also play niche roles in specific sectors like petrochemical and glass, where thermal control and energy conservation are mission-critical. Each product category serves unique performance and installation requirements based on end-use industry standards.

The steel industry dominates application-based demand for refractory materials, utilizing them in blast furnaces, converters, tundishes, and ladles. Refractories in this segment must endure temperatures exceeding 1,600°C, aggressive slag chemistry, and mechanical abrasion. This makes high-performance bricks and monolithics essential for process continuity. The fastest-growing application is in the cement industry, propelled by rising global infrastructure investments and new capacity additions across Asia, Africa, and Latin America. Rotary kilns used in cement production demand refractories that resist alkaline and sulfate attacks, prompting increased use of high-alumina and low-porosity materials. Other important applications include non-ferrous metallurgy, particularly for copper and aluminum smelting, where thermal stability and resistance to metal penetration are vital. Additionally, petrochemical refining and glass production also contribute consistently to refractory consumption, especially as process intensities and thermal efficiencies are pushed higher by evolving industrial standards.

The iron and steel sector is the leading end-user in the Refractory Materials Market, accounting for the bulk of demand across primary and secondary metallurgy. This dominance is driven by the need for constant refractory lining replacements due to extreme wear from molten metal and slag, especially in high-throughput plants. The fastest-growing end-user segment is the energy sector, particularly waste-to-energy, hydrogen production, and renewable fuels. These plants operate at variable high temperatures and require tailored refractory linings to ensure thermal containment and emission control. As governments expand clean energy targets, demand from this segment is expected to continue rising. Other end-users such as cement producers, glass manufacturers, and non-ferrous metal industries also contribute significantly, each with distinct thermal and chemical requirements. In chemical processing, for instance, refractories must resist acid corrosion, while in glass melting tanks, transparency and surface quality demand precise thermal control, placing high requirements on refractory purity and stability.

Asia-Pacific accounted for the largest market share at 46.3% in 2024; however, South America is expected to register the fastest growth, expanding at a CAGR of 4.1% between 2025 and 2032.

To Learn More About This Report, Request A Free Sample Copy

The Asia-Pacific region, led by China and India, remains the manufacturing hub of global refractory materials production, thanks to extensive investments in steel, cement, and glass manufacturing. The region also houses a dense network of small and large refractory producers, bolstered by government-backed infrastructure initiatives.

In contrast, South America, though smaller in scale, is witnessing accelerating demand due to growing steelmaking and industrial energy developments, particularly in Brazil and Argentina. Across all regions, global dynamics in raw material accessibility and rising demand from non-ferrous metallurgy and waste-to-energy sectors are shaping consumption patterns. The refractory materials market is also being influenced by tightening environmental regulations and increased focus on recycling, which is prompting a transition toward sustainable refractory product innovations. The adoption of smart refractory systems and AI-enhanced monitoring tools is further driving efficiency across developed regions. Emerging economies, meanwhile, are capitalizing on capacity expansion, creating lucrative opportunities for new entrants and specialized product developers in the refractories domain.

Adoption of Automation Technologies Reshaping Furnace Maintenance

North America held an estimated 17.5% share of the global refractory materials market in 2024. The market is largely driven by robust demand from the steel, non-ferrous metals, and oil refining sectors, especially in the U.S. and Canada. The shale gas boom and increase in hydrogen production facilities are supporting refractory consumption in energy applications. Government-backed decarbonization programs are incentivizing facilities to adopt energy-efficient and environmentally compliant refractory linings. Additionally, automation in furnace repair and digital tracking of refractory wear are becoming standard in high-volume steel plants. The adoption of smart sensors for temperature and erosion monitoring is improving operational efficiency and reducing unplanned downtimes, which is crucial for maintaining North American industrial competitiveness.

Green Transition Driving High-Performance Refractory Solutions

Europe accounted for approximately 22.1% of the global refractory materials market in 2024. Major economies such as Germany, France, and Italy lead the region’s consumption, primarily fueled by steel, cement, and advanced ceramics industries. Stringent European Union sustainability mandates and carbon neutrality goals are pushing refractory producers to develop low-emission, recyclable materials. Institutions like REACH and the European Green Deal are driving compliance-focused innovation. Advanced manufacturing technologies, including additive manufacturing for complex-shaped refractories and digital twin integration in kilns, are being increasingly adopted. These trends support a strong regional demand for high-performance refractories with superior environmental performance, durability, and digital integration capabilities.

Industrial Expansion Accelerates Refractory Demand in Key Manufacturing Zones

The Asia-Pacific region holds the dominant position in terms of market volume, representing over 46% of global consumption. China remains the largest single-country market, followed by India and Japan. Industrial expansion, fueled by domestic infrastructure investments and global outsourcing, continues to increase refractory requirements across the region. Major industries like cement, glass, and ferrous metallurgy are witnessing significant upgrades and capacity additions. Rapid urbanization and mega-infrastructure projects are also contributing to demand. Meanwhile, digital innovation hubs in countries like Japan and South Korea are supporting advancements in refractory processing automation, smart kiln monitoring, and nanomaterials integration, enhancing material performance and lifecycle management.

Growing Steel Output and Energy Sector Investments Stimulate Refractory Needs

In 2024, South America contributed around 6.7% of global refractory materials demand, with Brazil and Argentina as key markets. Brazil’s revitalized steel industry and its role in renewable energy projects are spurring demand for durable and high-efficiency refractory materials. Government-backed infrastructure schemes and tax incentives for industrial modernization are creating favorable conditions for refractory suppliers. Growth in cement and glass manufacturing, particularly for domestic consumption, is also driving demand. Furthermore, increased interest in lithium extraction and processing in the Andean regions is expanding opportunities for specialized refractories that can handle high thermal and chemical stresses.

Energy Sector Expansion and Construction Boom Supporting Steady Refractory Growth

The Middle East & Africa region accounted for nearly 7.4% of global refractory materials market volume in 2024. Demand is driven by large-scale oil & gas processing facilities, petrochemical complexes, and booming construction projects, especially in the UAE, Saudi Arabia, and South Africa. Major government initiatives such as Vision 2030 and Africa’s infrastructure development programs are boosting industrial furnace installation, enhancing the need for refractories. At the same time, digital transformation initiatives are introducing automation in maintenance operations and smart materials integration. Free trade agreements and policy harmonization across regions are facilitating smoother access to refractory products and technologies, particularly those aligned with international energy efficiency standards.

China – 34.5% market share

Dominates due to high production capacity and integrated supply chain for steel, cement, and refractory raw materials.

Germany – 11.8% market share

Leads with advanced technologies and strong demand from energy-efficient manufacturing and regulated high-temperature industries.

The Refractory Materials market is highly competitive, characterized by the presence of over 120 active manufacturers operating at global, regional, and niche levels. Major players are concentrated in Asia-Pacific and Europe, where raw material accessibility and established manufacturing hubs offer a strategic advantage. Companies are increasingly focusing on backward integration of supply chains, particularly in magnesia and alumina sourcing, to maintain quality control and reduce procurement costs.

Competitive dynamics in the market are evolving through aggressive product innovation, with several players introducing monolithic refractories and environment-friendly compositions for lower emissions. Technological advancements such as robotics in refractory lining, AI-driven wear monitoring systems, and 3D-printed refractory bricks are setting new industry benchmarks. Mergers and acquisitions are a frequent strategy, particularly among mid-tier players aiming to diversify their product portfolio and expand into high-demand geographies like the Middle East and South America. Strategic partnerships with steelmakers, glass manufacturers, and cement producers are also becoming common, enabling tailored refractory solutions aligned with specific thermal and mechanical stress requirements. The market is further witnessing increased investments in R&D focused on enhancing material lifespan, thermal resistance, and energy-saving potential, creating a robust competitive environment where innovation, sustainability, and regional adaptability are key success factors.

RHI Magnesita GmbH

Vesuvius plc

Krosaki Harima Corporation

Imerys Group

Shinagawa Refractories Co., Ltd.

HarbisonWalker International

Chosun Refractories Co., Ltd.

Refratechnik Holding GmbH

Morgan Advanced Materials

Resco Products, Inc.

Technological advancements in the refractory materials market are increasingly transforming production, application, and monitoring processes. One of the most significant innovations is the integration of robotics and automation in refractory installation, particularly in steel and cement plants. Automated gunning machines and robotic arms are now widely used for applying monolithic refractories, reducing installation time by up to 35% while enhancing worker safety in high-temperature environments. Smart refractory systems equipped with IoT sensors are gaining traction for real-time temperature and wear monitoring, helping plants schedule predictive maintenance and reduce unplanned downtimes. These systems improve refractory service life and minimize material waste, leading to cost optimization in high-energy industries. AI-powered software is being developed to model thermal behavior in kilns and reactors, enabling precise material selection based on usage conditions.

Another growing trend is the application of 3D printing to manufacture complex refractory shapes, allowing for reduced lead times and customized geometries. This technique is particularly valuable in aerospace and non-ferrous metallurgy sectors. Additionally, nanotechnology is being employed to enhance refractory resistance against corrosion and thermal shock. Materials like nano-zirconia and nano-alumina are being used to improve structural stability under extreme conditions. Sustainable innovation is also emerging, with an increase in refractory recycling technologies that allow recovery of high-value minerals from spent linings. This aligns with global environmental goals and supports the circular economy by reducing dependence on virgin raw materials.

• In February 2024, Vesuvius launched a new range of low-carbon alumina refractories for steel tundishes. The products are manufactured using recycled aggregates and offer improved thermal insulation, reducing overall energy consumption in continuous casting by 8%.

• In September 2023, RHI Magnesita opened its first digitalized refractory recycling plant in Germany. The facility has a processing capacity of 150,000 tons annually and aims to reduce primary raw material consumption by 10% across European operations.

• In November 2023, Imerys developed a new spinel-based castable refractory designed for use in cement rotary kilns. The new formulation shows enhanced resistance to chemical attack and extends maintenance intervals by up to 20% compared to previous products.

• In March 2024, Shinagawa Refractories introduced a line of AI-optimized monolithic refractories for glass melting furnaces. The AI model improves formulation based on thermal modeling and lifecycle data, increasing material durability by 15% in trial deployments.

The Refractory Materials Market Report provides a comprehensive analysis of the global landscape, encompassing key market segments, regional performance, industrial applications, technological advancements, and emerging trends. The scope of the report extends across critical refractory types, including monolithic, bricks, castables, and ceramic fibers, with insights into their utilization across diverse industries such as steel, glass, cement, non-ferrous metals, power generation, and petrochemicals. The report investigates product performance in both shaped and unshaped formats, examining thermal resistance, mechanical strength, and resistance to chemical corrosion under extreme environments.

Geographically, the report covers major regions including North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, offering comparative insights into demand drivers, production hubs, and consumption trends in each territory. In-depth regional evaluations highlight strategic manufacturing zones such as China, India, the U.S., and Germany, where infrastructure expansion and industrial output significantly influence market dynamics.

The report also explores the growing adoption of sustainable and energy-efficient refractory technologies, including recyclable and low-carbon emission materials. The scope further addresses the integration of digital monitoring systems for real-time wear tracking in refractory linings, signaling a shift toward predictive maintenance practices. Additionally, the market report identifies opportunities in specialized applications such as aerospace, defense, and high-temperature battery systems, broadening the market’s strategic relevance.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 54,898.4 Million |

|

Market Revenue in 2032 |

USD 72,851.4 Million |

|

CAGR (2025 - 2032) |

3.6% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Lenzing AG, Rayonier Advanced Materials Inc., Sappi Limited, Bracell Limited, Domtar Corporation, Aoyang Technology Co., Ltd., Grasim Industries Limited, Sun Paper Group, Sichuan Vanov New Material Co., Ltd., Fortress Global Enterprises Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |