Reports

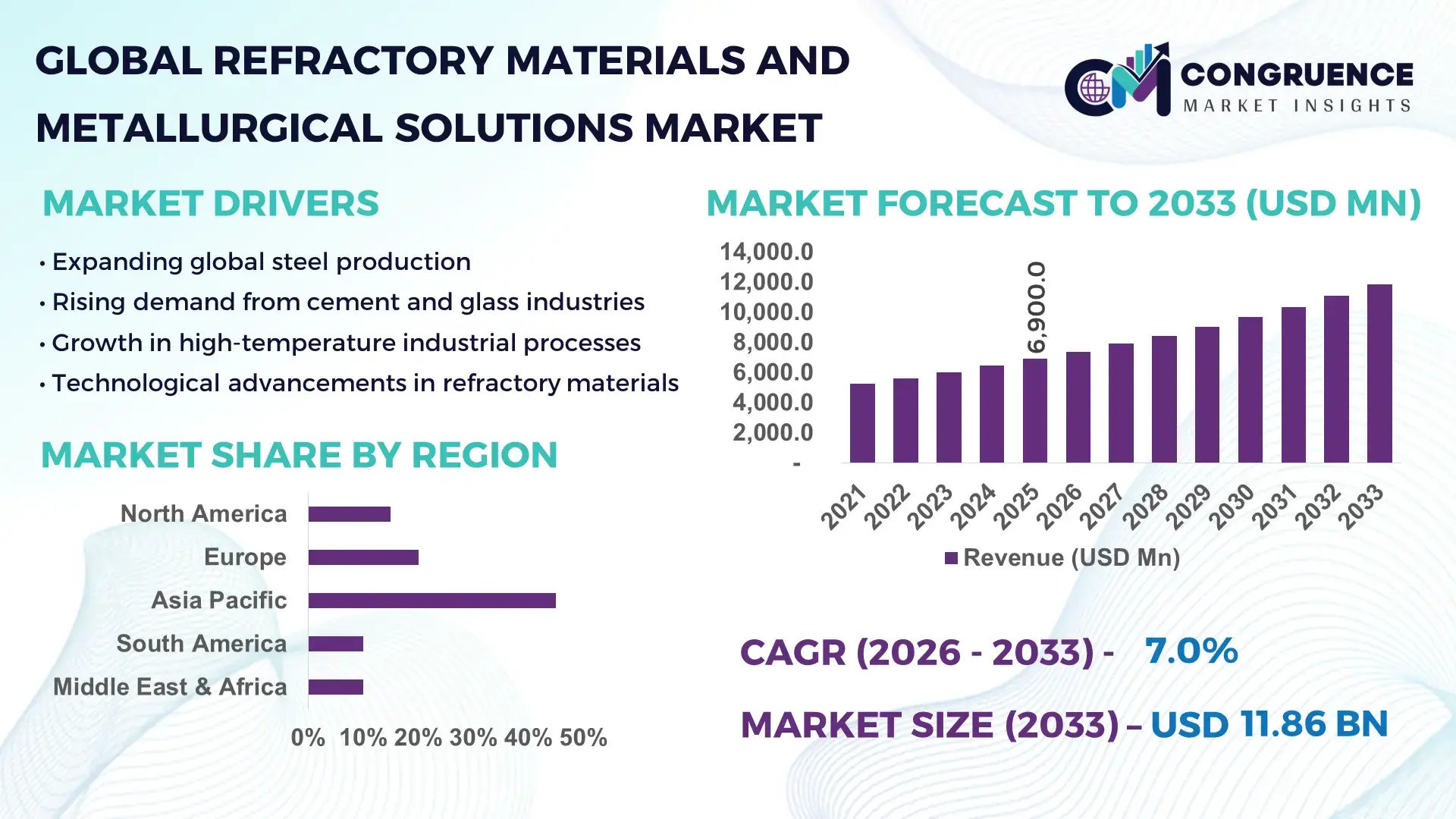

The Global Refractory Materials and Metallurgical Solutions Market was valued at USD 6,900 Million in 2025 and is anticipated to reach a value of USD 11,855.5 Million by 2033, expanding at a CAGR of 7% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth trajectory is supported by sustained capacity expansion in primary metals, higher-temperature industrial processing requirements, and accelerated adoption of advanced refractory formulations across energy-intensive industries.

China dominates the Refractory Materials and Metallurgical Solutions Market in terms of scale and industrial penetration. The country operates more than 60% of global crude steel production capacity, exceeding 1.02 billion metric tons annually, creating continuous demand for monolithic refractories, basic bricks, and metallurgical linings. China hosts over 2,000 refractory manufacturing units, with several facilities exceeding 200,000 tons/year in output. Annual investments in metallurgical infrastructure surpassed USD 150 billion in recent years, supporting blast furnaces, electric arc furnaces, and non-ferrous smelting. Advanced applications include alumina-carbon refractories, low-cement castables, and digitally monitored furnace linings. Automation adoption in large steel plants now exceeds 45%, improving refractory life cycles and thermal efficiency across industrial operations.

Market Size & Growth: Valued at USD 6.9 billion in 2025 and projected to reach USD 11.86 billion by 2033, driven by higher-temperature industrial processing and furnace modernization.

Top Growth Drivers: Steel production expansion (42%), energy-efficiency upgrades in furnaces (31%), increased non-ferrous metal processing (27%).

Short-Term Forecast: By 2028, furnace downtime is expected to decline by nearly 18% through adoption of advanced monolithic refractories.

Emerging Technologies: Low-carbon refractory formulations, AI-based lining wear monitoring, and nano-bonded ceramic composites.

Regional Leaders: Asia Pacific projected at USD 5.2 billion by 2033 with volume-driven demand; Europe at USD 3.1 billion driven by sustainability compliance; North America at USD 2.4 billion led by furnace retrofits.

Consumer/End-User Trends: Steel and cement plants account for nearly 68% of consumption, with rising uptake in glass and aluminum smelting.

Pilot or Case Example: In 2024, a Japanese steel plant reduced refractory replacement cycles by 22% using sensor-enabled linings.

Competitive Landscape: RHI Magnesita leads with ~18% presence, followed by Vesuvius, Krosaki Harima, Calderys, and Shinagawa.

Regulatory & ESG Impact: Emission reduction mandates are accelerating low-carbon refractory adoption, targeting 20% lifecycle emission cuts.

Investment & Funding Patterns: Over USD 4.5 billion invested globally in furnace upgrades and refractory innovation projects since 2022.

Innovation & Future Outlook: Integration of digital twins and recyclable refractory materials is shaping next-generation industrial furnaces.

The Refractory Materials and Metallurgical Solutions Market serves steel (≈52%), cement (≈16%), non-ferrous metals (≈14%), glass (≈9%), and other high-temperature industries. Innovations in ultra-low porosity bricks, longer-life castables, and recycling-ready refractories are reshaping operational efficiency. Environmental regulations, regional industrial output, and energy-cost optimization remain decisive factors, while Asia Pacific leads consumption and Europe drives sustainable product adoption.

The Refractory Materials and Metallurgical Solutions Market holds strategic importance as a foundational enabler of high-temperature industrial processes across steel, cement, glass, and non-ferrous metal production. These industries collectively support over 40% of global industrial energy consumption, making refractory efficiency a direct lever for cost optimization and emissions control. Advanced refractory systems now function as performance assets rather than consumables, with lifecycle optimization influencing furnace productivity and asset utilization.

New technologies such as AI-enabled refractory monitoring systems deliver nearly 25% improvement in lining life prediction compared to traditional manual inspection standards. Asia Pacific dominates in production volume due to large-scale steelmaking, while Europe leads in advanced refractory adoption, with nearly 48% of enterprises integrating low-carbon and recycled refractory materials. By 2028, digital furnace analytics and smart linings are expected to improve thermal efficiency by approximately 15%, directly reducing unplanned shutdowns.

From an ESG perspective, firms are committing to 30% refractory material recycling rates by 2030, supporting circular economy targets. In 2024, Germany achieved a 19% reduction in refractory waste through closed-loop reuse programs in cement kilns. Strategically, the Refractory Materials and Metallurgical Solutions Market is evolving into a pillar of industrial resilience, regulatory compliance, and sustainable growth, supporting future-ready manufacturing ecosystems worldwide.

The Refractory Materials and Metallurgical Solutions Market is shaped by industrial output cycles, energy transition policies, and continuous advancements in high-temperature material science. Demand remains closely linked to steelmaking, cement manufacturing, and metallurgical processing volumes, while innovation is driven by the need for longer service life and lower thermal losses. Increasing electrification of furnaces and stricter emission thresholds are influencing material selection and design. Regional dynamics vary, with Asia Pacific emphasizing capacity scale, Europe focusing on sustainability compliance, and North America prioritizing furnace modernization and operational efficiency.

Global steel output exceeds 1.9 billion metric tons annually, requiring continuous refractory replacement and maintenance. Electric arc furnace adoption has crossed 33% globally, increasing demand for high-purity, thermal-shock-resistant refractories. Aluminum and copper smelting volumes are also rising, with aluminum production surpassing 70 million tons, driving specialized refractory linings capable of handling corrosive molten metals and higher operational temperatures.

Key refractory inputs such as magnesite, bauxite, and graphite experience price fluctuations exceeding 20% annually, impacting production planning. Energy-intensive firing processes account for nearly 35% of manufacturing costs, while regional energy price instability limits profitability. Additionally, supply concentration of high-grade minerals creates procurement risks for refractory producers.

Decarbonization initiatives are accelerating adoption of lightweight, insulating refractories that can reduce furnace heat losses by 10–18%. Hydrogen-ready steelmaking and alternative fuel kilns require new refractory chemistries, opening innovation opportunities. Recycling-enabled refractory systems are gaining traction, with reuse rates approaching 25% in pilot programs.

Refractory installation requires specialized expertise, yet skilled labor availability has declined by nearly 12% in mature markets. Improper installation can reduce lining life by up to 30%, increasing maintenance frequency. Training gaps, safety regulations, and complex furnace geometries further elevate operational challenges for end-users.

Smart Refractory Monitoring Systems: More than 38% of large industrial furnaces now deploy embedded sensors for temperature and wear monitoring. These systems improve predictive maintenance accuracy by 24% and reduce unplanned shutdowns by 17%, particularly in steel and cement kilns.

Shift Toward Low-Carbon and Recyclable Refractories: Over 46% of new refractory product launches incorporate reduced-carbon binders or recycled aggregates. Industrial trials show waste reduction levels reaching 28%, aligning with tightening environmental compliance standards in Europe and East Asia.

Growth in Monolithic Refractories Adoption: Monolithic refractories now account for approximately 62% of total installations, up from 54% five years ago. Their use reduces installation time by 20–25% and improves furnace turnaround efficiency in continuous operations.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Refractory Materials and Metallurgical Solutions Market. Nearly 55% of new industrial projects report cost efficiencies through prefabricated refractory components. Pre-formed elements produced via automated systems lower on-site labor needs by 30% and accelerate commissioning timelines, especially in Europe and North America where productivity optimization is critical.

The Refractory Materials and Metallurgical Solutions Market is segmented primarily by type, application, and end-user, reflecting how materials are engineered, deployed, and consumed across high-temperature industries. By type, the market spans shaped and unshaped refractories with distinct performance profiles, installation methods, and durability characteristics. By application, demand aligns closely with furnace design, process temperature, and exposure to slag, molten metal, or chemical corrosion. End-user segmentation is anchored in energy-intensive industries—particularly steel, cement, and non-ferrous metals—where refractory performance directly influences productivity, downtime, and operational efficiency. Across all segments, material selection is increasingly guided by thermal efficiency, recyclability, ease of installation, and compatibility with low-carbon industrial processes.

Shaped refractories (pre-formed bricks and blocks) and unshaped refractories (monolithics, castables, and gunning mixes) constitute the core of the market, alongside specialty products such as insulating refractories and basic refractories. Unshaped (monolithic) refractories lead the market with roughly 62% share, as they enable faster installation, fewer joints, and superior resistance to thermal cycling—critical for electric arc furnaces, continuous casters, and rotary kilns. Their pumpable and sprayable nature reduces labor intensity and shortens furnace turnaround times in steel and cement plants.

The fastest-growing type is low-cement and ultra-low-cement castables, advancing at about 9–10% CAGR, driven by tighter emission norms, the need for longer lining life, and the shift toward energy-efficient furnaces that operate at higher temperatures with lower heat loss.

Shaped basic bricks (magnesia, magnesia-carbon, and alumina-magnesia) remain essential for slag-intensive zones such as steel ladles and converters, while insulating refractories serve as thermal barriers in furnace walls and roofs. High-purity alumina products cater to glass and petrochemical kilns, and silica refractories persist in coke ovens. Collectively, these remaining types account for roughly 38% of the market, serving performance-critical but more specialized applications.

• According to a 2025 publication by the U.S. Department of Energy, next-generation low-cement castables were successfully trialed in a commercial steel electric arc furnace, extending lining life by over 20% while reducing kiln heat loss.

Steel production is the dominant application, accounting for about 52% of total consumption, because every stage—blast furnaces, basic oxygen furnaces, electric arc furnaces, and ladles—requires tailored refractory linings to withstand extreme heat and chemical attack. Cement kilns represent the second-largest use case, where refractories protect long rotary kilns operating above 1,400°C and determine clinker quality and fuel efficiency.

The fastest-growing application is electric arc furnace (EAF) steelmaking, expanding at roughly 8–9% CAGR, propelled by scrap-based steel production, decarbonization policies, and the rapid build-out of mini-mills worldwide.

Glass manufacturing, non-ferrous metal smelting (aluminum, copper, zinc), petrochemicals, and power generation together make up around 33–36% of remaining demand, relying on high-purity and corrosion-resistant materials.

Consumer and adoption signals show clear momentum: in 2025, about 38% of large metals producers reported piloting sensor-enabled refractory monitoring systems, and over 60% of industrial engineers surveyed indicated preference for modular, pre-cast refractory components to reduce installation risk and downtime.

• In 2025, the International Energy Agency highlighted a program in Europe where smart refractory linings in cement kilns reduced unplanned shutdowns across more than 20 plants while cutting fuel consumption by nearly 8%.

The steel industry leads end-user demand with roughly 55% share, reflecting its reliance on continuous high-temperature operations, aggressive slag chemistry, and frequent relining cycles. Refractory longevity directly affects furnace availability, making material performance a strategic priority for steelmakers transitioning to low-carbon and scrap-based production routes.

The fastest-growing end-user segment is renewable-linked metals processing (including aluminum and battery-grade materials), rising at approximately 9% CAGR, fueled by electric vehicle manufacturing, grid infrastructure expansion, and demand for high-purity metals that require specialized refractory environments.

Cement producers account for about 16–18% of usage, prioritizing thermal insulation and abrasion resistance, while glass manufacturers and petrochemical refiners collectively represent another 12–14%. Power generation and other industrial processors contribute the remaining 12–15%, often favoring lightweight, energy-saving refractories.

Adoption trends show that 42% of U.S. heavy-industry plants were testing AI-assisted furnace monitoring in 2025, and nearly 35% of global cement operators reported shifting toward recyclable refractory systems to meet sustainability targets.

• A 2025 report by the International Aluminium Institute documented that more than 15 major smelters adopted low-carbon refractory linings, reducing waste generation by over 18% while improving furnace stability.

Asia-Pacific accounted for the largest market share at 45% in 2025, however, North America is expected to register the fastest growth, expanding at a CAGR of 7% between 2026 and 2033.

Asia-Pacific’s dominance stems from large-scale steel, cement, and non-ferrous metal production, with China contributing over 1.02 billion metric tons of steel annually and India surpassing 120 million metric tons. Europe holds 20%, North America 15%, South America 10%, and Middle East & Africa 10%. The region benefits from high industrial output, continuous modernization of furnaces, and strong adoption of energy-efficient and automated refractory solutions.

North America holds about 15% of the global market, led by steel, cement, and non-ferrous metal sectors. Key industries driving demand include electric arc furnace steelmaking, aluminum smelting, and glass production. Regulatory support from environmental agencies encourages low-carbon refractory adoption, while technological trends such as digital furnace monitoring and predictive maintenance are gaining traction. Companies like RHI Magnesita’s North American operations are upgrading kilns with sensor-enabled linings to optimize maintenance cycles and reduce energy consumption. Regional consumer behavior shows higher adoption of smart and automated solutions in heavy industry and high-value manufacturing sectors.

Europe accounts for 20% of the global market, with Germany, France, and the UK being major contributors. Sustainability regulations and emission reduction mandates are driving demand for low-carbon and recyclable refractories. Emerging technologies such as AI-based wear monitoring and modular monolithic installation are increasingly deployed. Companies like Vesuvius are integrating digital lining sensors to enhance steel and cement plant efficiency. Regional consumer behavior reflects strict compliance-driven adoption, particularly in energy-intensive industries where explainable, traceable refractory solutions are required for regulatory audits.

Asia-Pacific dominates with 45% of the global market, led by China, India, and Japan. Large-scale steel and cement production facilities, totaling over 1.1 billion metric tons of annual output, drive consistent demand. Rapid infrastructure growth and investment in high-temperature industrial processes are prevalent. Technological innovations include automated installation of monolithic refractories and smart furnace monitoring in major manufacturing hubs. Companies like Calderys China are expanding capacity and deploying sensor-enabled linings to extend furnace life. Consumer behavior favors large industrial operators adopting high-performance, energy-efficient refractory solutions to maximize uptime.

South America represents 10% of the global market, with Brazil and Argentina as the leading contributors. Growth is linked to steel, aluminum, and cement production, alongside energy infrastructure projects. Government incentives and trade policies support modernization of kilns and furnaces. Local players such as Magnesita South America are upgrading plants with advanced monolithic linings to reduce maintenance frequency. Regional consumer behavior shows selective adoption by heavy industry operators focused on cost reduction and operational efficiency.

Middle East & Africa accounts for 10% of the market, led by UAE, Saudi Arabia, and South Africa. Demand is fueled by oil & gas, steel, and cement sectors. Technological modernization, including automated monolithic installation and digital monitoring, is gradually increasing. Regional players such as RHI Magnesita Middle East are enhancing refractory solutions for high-temperature industrial processes. Consumer behavior indicates adoption focused on durability and energy efficiency to optimize furnace operations in energy-intensive industries.

China – 28% Market Share: High steel production capacity exceeding 1.02 billion metric tons annually and extensive industrial infrastructure drive demand.

United States – 15% Market Share: Strong adoption of advanced furnace technologies and regulatory incentives for low-carbon refractory solutions enhance market presence.

The Refractory Materials and Metallurgical Solutions Market exhibits a moderately consolidated competitive structure, with a substantial number of active companies vying for position worldwide. While there are dozens of producers and solution providers globally, the combined share of the top 5 companies—RHI Magnesita, Vesuvius, Krosaki Harima, Saint‑Gobain, and Morgan Advanced Materials—accounts for approximately 30% of global capacity, indicating significant presence but also ongoing fragmentation as smaller regional players maintain influence. Approximately 70+ companies operate in this space, with competition shaped by product performance, service integration, sustainability profiles, and digital innovation.

Strategic initiatives are shaping competitive dynamics: acquisitions like RHI Magnesita’s planned purchase of Resco Group are expanding geographical reach and alumina‑based refractory portfolios, while partnerships (for instance, co‑development agreements between major refractories firms) are accelerating development of low‑carbon and recycled‑content materials. Product launches in 2024 and 2025 have focused on smart linings with embedded sensors for wear monitoring, modular refractory systems for faster installation, and high‑strength composite bricks tailored to high‑temperature metallurgical applications.

Innovation trends exert pressure on competitors to adopt robotics, AI for real‑time quality control, and advanced material chemistries that improve thermal stability, corrosion resistance, and lifecycle performance. Companies are also investing in waste‑recycling hubs, digital production lines, and enhanced distribution networks to serve heavy industries such as steel, cement, glass, and non‑ferrous metals more effectively. Overall, competitive positioning increasingly reflects technological differentiation and service depth rather than solely scale of output.

Saint‑Gobain

Morgan Advanced Materials

HarbisonWalker International

Shinagawa Refractories Co., Ltd.

Imerys

Calderys

TATA Refractories

Almatis

Dalian Jinma Refractory

Qinghua Refractory

CUMI

Technology adoption is increasingly central to competitiveness in the Refractory Materials and Metallurgical Solutions Market, driven by demands for efficiency, performance, and environmental compliance. A major area of development is smart refractory monitoring systems that incorporate embedded temperature and wear sensors. These technologies enable real‑time analysis of the condition of refractory linings inside furnaces and kilns, improving predictive maintenance and reducing unplanned stoppages. Digital casting and installation systems are being implemented in nearly 30% of new refractory factories, providing real‑time quality verification and reducing waste.

Advanced material chemistries are also transforming product performance. High‑purity alumina, magnesia‑carbon composites, and zircon‑mullite refractories exhibit enhanced resistance to corrosion and thermal shock, extending service intervals and lowering operating costs. Innovations such as ultra‑low cement and recycled‑content castables are reducing environmental impact by lowering CO₂ emissions and supporting circular economy initiatives. Composite and fiber‑enhanced refractories with improved thermal insulation are gaining traction in glass and petrochemical applications, where stability at extreme temperatures is critical.

Automation and robotics in refractory mixing, forming, and packaging streamline production and maintain consistency, with AI‑driven quality inspection systems improving defect detection and consistency. Hybrid installation systems that combine robotic assistance with traditional lining methods are reducing installation time by significant percentages in pilot implementations. Industry collaboration with research institutes is also catalyzing exploration into nanotechnology‑based coatings and high‑entropy alloys capable of withstanding higher operating temperatures for next‑generation industrial processes. These technology trends underscore a shift toward smarter, more resilient refractory solutions that align with both operational efficiency and sustainability objectives, offering decision‑makers enhanced control over performance and lifecycle outcomes.

• In November 2025, Calderys and Binzagr announced a strategic partnership to serve the evolving refractory market in the Middle East, establishing a 16,300 m² production facility in Jubail, Saudi Arabia with monolithics and precast lines set to begin production in April 2026, aimed at reinforcing supply for iron & steel, aluminum, cement, and petrochemical sectors. Source: www.calderys.com

• In November 2025, Calderys commissioned the basic monolithics line at its new CAPES facility in Odisha, India, enhancing its capability to produce both acidic and basic monolithic refractories, strengthening its support for India’s steel, cement, aluminum, and petrochemical industries and expanding tailored refractory solutions for key industrial hubs. Source: www.calderys.com

• In April 2025, RHI Magnesita launched high-performance refractory solutions for foundries, showcasing its portfolio of customized refractory products for furnaces, converters, valves, and technical support services at the Metalurgia industrial fair, underscoring its technological and sustainability focus in high-temperature industrial processes. Source: www.metalurgia.com.br

• In August 2025, RHI Magnesita India deployed a full end‑to‑end robotic solution in continuous casting operations at a major Indian steel plant, as part of its 4PRO business model, demonstrating increased automation, enhanced safety, and productivity improvements in refractory management within continuous casting applications. Source: www.rhimagnesitaindia.com

The scope of the Refractory Materials and Metallurgical Solutions Market Report encompasses a broad and detailed analysis of product types, applications, end‑user uses, regional dynamics, technology trends, and competitive strategies in the high‑temperature materials sector. This market serves industries that operate furnaces, kilns, reactors, and high‑heat environments—including steel, cement, glass, petrochemical, and non‑ferrous metal processing—by providing refractory bricks, monolithic castables, fiber modules, slide gate systems, and composite linings. The report examines segmentation by material form (shaped, unshaped, fiber, composite) and by application zone (e.g., furnace hearth, roof, sidewalls, ladles) to highlight performance requirements and engineering considerations for different thermal exposures. It also analyzes end‑user behavior across primary industries, offering insight into adoption patterns, service life expectations, and purchasing criteria for refractory systems.

On the geographic front, the report evaluates demand patterns and infrastructure trends across key regions—North America, Europe, Asia‑Pacific, South America, and Middle East & Africa—examining factors such as manufacturing intensity, regulatory environments, and investment in digitalization. Technology focus areas include digital monitoring, robotics in installation, advanced material chemistries, and sustainability‑driven innovations like recyclable and low‑emission refractory systems. The report also profiles competitive strategies such as mergers, joint ventures, product launches, and regional expansions to illustrate how market participants are positioning themselves for future growth. Additionally, emerging niche segments—such as refractory solutions for hydrogen‑ready furnaces, advanced thermal barrier coatings, and high‑entropy alloys—are explored to offer a comprehensive view of present capabilities and future opportunities.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 6,900 Million |

| Market Revenue (2033) | USD 11,855.5 Million |

| CAGR (2026–2033) | 7% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | RHI Magnesita; Vesuvius; Krosaki Harima Corporation; Saint-Gobain; Morgan Advanced Materials; HarbisonWalker International; Shinagawa Refractories Co., Ltd.; Imerys; Calderys; TATA Refractories; Almatis; Dalian Jinma Refractory; Qinghua Refractory; CUMI |

| Customization & Pricing | Available on Request (10% Customization Free) |