Reports

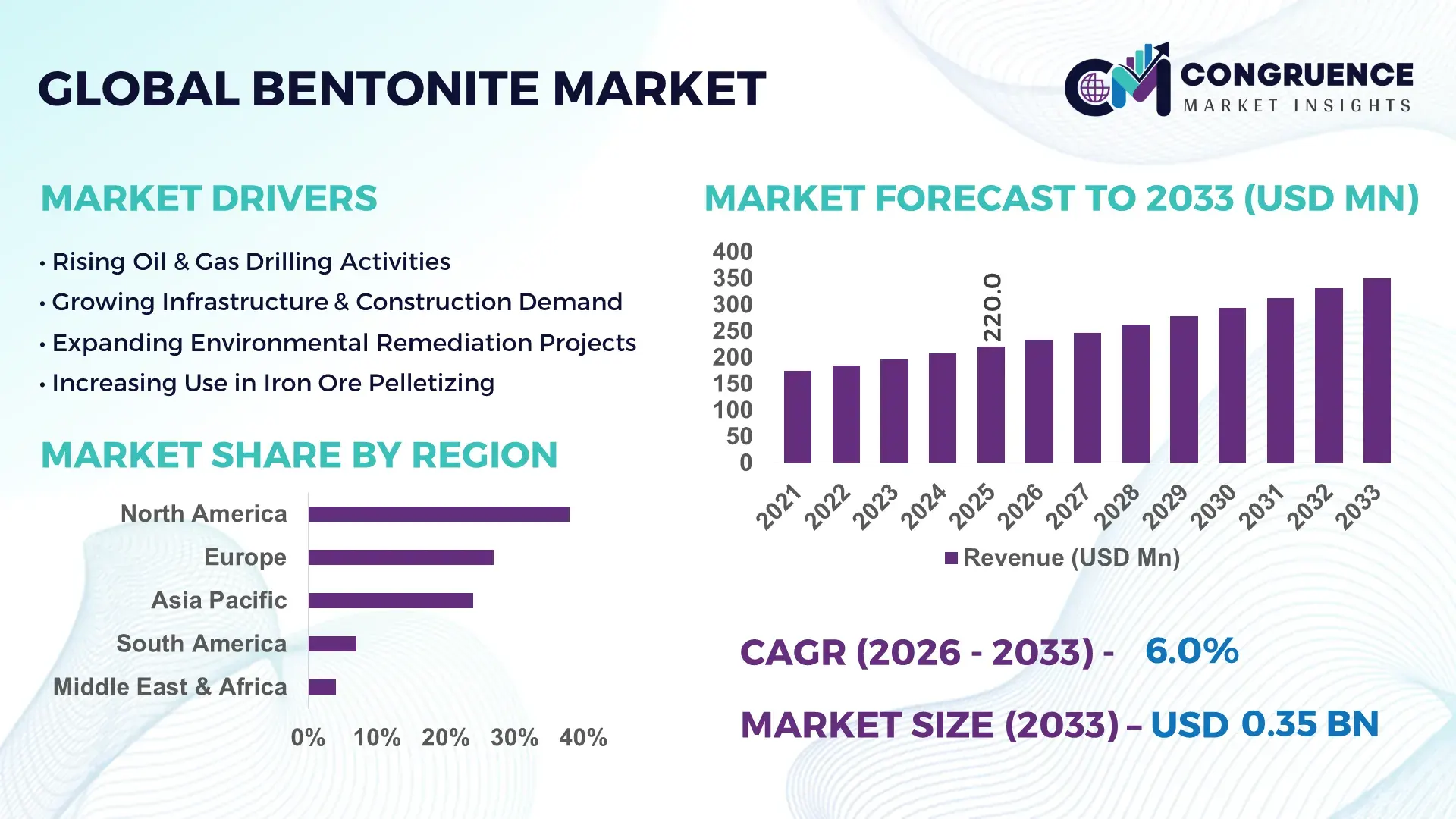

The Global Bentonite Market was valued at USD 220.0 Million in 2025 and is anticipated to reach a value of USD 350.6 Million by 2033 expanding at a CAGR of 6% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is primarily driven by expanding demand for drilling fluids, iron ore pelletizing, and environmental sealing applications across energy, mining, and infrastructure sectors.

The United States represents the dominant country in the global Bentonite Market, supported by extensive natural reserves and large-scale production infrastructure. Wyoming alone accounts for more than 70% of U.S. sodium bentonite output, with annual production exceeding 4.5 million metric tons. Capital investment in bentonite mining and processing facilities surpassed USD 480 million between 2020 and 2024, focusing on automation and beneficiation technologies. Over 35% of U.S. bentonite output is used in drilling fluids for oil and gas, while 22% is consumed in iron ore pelletizing and 15% in environmental liners and geosynthetic clay liners (GCLs). Adoption of high-purity activated bentonite in foundry sands increased by 18% over the last five years, supported by sensor-based quality control systems and closed-loop water recycling technologies in processing plants.

Market Size & Growth: Valued at USD 220.0 Million in 2025, projected to reach USD 350.6 Million by 2033, expanding at 6% CAGR, driven by rising infrastructure drilling and environmental sealing demand.

Top Growth Drivers: Oil & gas drilling adoption +28%, iron ore pelletizing efficiency +22%, landfill liner usage +19%.

Short-Term Forecast: By 2028, drilling fluid performance efficiency is expected to improve by 17% through advanced rheology modifiers.

Emerging Technologies: Plasma-activated bentonite, nano-modified clays, and AI-based slurry optimization systems.

Regional Leaders: North America USD 120.0 Million by 2033 with automation adoption; Asia Pacific USD 95.0 Million with mining expansion; Europe USD 72.0 Million with environmental liner penetration.

Consumer/End-User Trends: Mining accounts for 34% of demand, construction 27%, oil & gas 24%, environmental engineering 15%.

Pilot or Case Example: In 2024, a Wyoming pilot plant achieved 21% water reuse improvement through closed-loop activation systems.

Competitive Landscape: Market leader holds ~18% share, followed by four competitors each between 7–12%.

Regulatory & ESG Impact: Environmental liner mandates increased compliant bentonite usage by 26% in waste containment projects.

Investment & Funding Patterns: Over USD 1.2 Billion invested globally in beneficiation plants and automation upgrades since 2021.

Innovation & Future Outlook: Integration of sensor-based activation control and low-emission drying systems shaping next-generation processing.

Bentonite demand is concentrated across oil & gas drilling (34%), iron ore pelletizing (29%), construction sealing (21%), and foundry applications (16%). Recent innovations in polymer-enhanced bentonite improved swelling capacity by 14% and reduced slurry loss by 11%. Environmental regulations promoting landfill liners and groundwater protection are accelerating consumption in Europe and Asia, while mining-driven demand growth remains strongest in Australia and Brazil.

The Bentonite Market plays a strategic role in supporting critical infrastructure, energy security, environmental protection, and industrial materials supply chains. Its relevance is anchored in drilling fluids, iron ore pelletizing, geosynthetic clay liners, and specialty absorbents, where performance reliability directly influences operational efficiency and regulatory compliance.

Advanced activation technologies are reshaping processing economics. Microwave-assisted drying delivers 24% energy efficiency improvement compared to conventional rotary kiln drying. North America dominates in volume, while Asia Pacific leads in adoption with 41% of mining and construction enterprises integrating high-activation bentonite grades into operations. By 2028, AI-driven slurry optimization is expected to improve drilling fluid stability by 19% and cut additive consumption by 15%.

Compliance pressures are intensifying. Firms are committing to ESG metrics such as 30% reduction in water discharge and 25% increase in tailings recycling by 2030. In 2024, a U.S.-based processor achieved 22% energy reduction through electrified calcination systems. In parallel, environmental liner specifications in Europe now require permeability below 1×10⁻⁹ m/s in over 65% of new containment projects.

Looking forward, the Bentonite Market is positioned as a pillar of industrial resilience, regulatory compliance, and sustainable growth, supporting long-term infrastructure expansion, circular processing models, and low-impact material technologies.

The Bentonite Market is shaped by cyclical mining activity, infrastructure expansion, environmental regulation, and evolving drilling technologies. Demand remains closely linked to oil & gas well counts, iron ore pellet production volumes, and landfill liner installations. Technological progress in beneficiation, activation control, and water recycling is improving product consistency and lowering environmental footprints. Regional production remains concentrated in North America, China, India, and Turkey, while consumption growth is strongest in Asia Pacific and Latin America. Supply chains are increasingly influenced by logistics costs, moisture control requirements, and regulatory permitting timelines. Sustainability mandates are driving adoption of low-emission drying systems and closed-loop processing, while end-users are prioritizing higher swelling index and lower impurity grades for performance-critical applications.

Rising drilling activity and iron ore pellet production are major growth drivers for the Bentonite Market. Global onshore drilling programs increased by 23% between 2021 and 2024, raising consumption of sodium bentonite in drilling mud systems. In iron ore processing, pellet plants now use an average of 6–8 kg of bentonite per ton of pellets, with pellet output exceeding 2.3 billion tons annually. Environmental sealing projects also expanded, with geosynthetic clay liner installations rising 19% in landfill and hazardous waste containment. These trends are increasing demand for high-swelling, low-filtrate bentonite grades, directly strengthening volume stability and long-term supply contracts.

Bentonite’s high moisture sensitivity and bulk transport requirements create operational constraints. Moisture absorption above 12% reduces swelling efficiency by up to 18%, increasing rejection rates in foundry and drilling applications. Long-distance transport raises logistics costs by 20–35% per ton, particularly for exports from landlocked mines. Storage requires controlled humidity environments, raising warehousing expenses by 14% annually. In addition, permitting delays for new quarries average 24–36 months, limiting supply flexibility and slowing capacity expansion in high-growth regions.

Environmental containment offers significant opportunity for bentonite suppliers. Over 68% of new landfill cells now specify geosynthetic clay liners, each consuming 5–7 kg/m² of bentonite. Groundwater protection projects expanded by 26% between 2020 and 2024, increasing demand for low-permeability sealing materials. Polymer-modified bentonite adoption rose 21% in slurry wall construction, delivering 17% lower permeability and 13% longer service life. These applications create stable, regulation-driven demand with long project cycles and premium pricing potential.

Regulatory compliance and grade consistency remain major challenges. Over 32% of shipments fail initial quality checks due to variable montmorillonite content. Environmental regulations require trace metal levels below 50 ppm in liner-grade bentonite, increasing beneficiation complexity. Energy-intensive drying consumes 900–1,200 kWh per ton, exposing producers to power price volatility. Compliance audits now occur every 12–18 months in key regions, raising operational costs and slowing plant expansions.

Automation in Beneficiation Plants: Automated activation control systems improved yield by 16% and reduced off-grade output by 21% in 2024. Sensor-guided blending reduced impurity variability from 9% to 4%, improving product consistency across 62% of upgraded facilities.

Growth in Geosynthetic Clay Liners: GCL installations increased 27% between 2021 and 2024, with permeability performance improving by 18% through polymer-enhanced bentonite. Over 74% of new hazardous waste cells now specify reinforced bentonite liners.

Advanced Drilling Fluid Formulations: High-performance bentonite-based fluids improved wellbore stability by 22% and reduced fluid loss by 15% in deep onshore wells. Adoption reached 48% of new drilling programs in North America.

Sustainability-Driven Processing Upgrades: Electrified drying systems cut CO₂ emissions by 31% and water discharge by 28% in modern plants. Closed-loop water systems now operate in 44% of large-scale processing facilities, reducing freshwater intake by 35%.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Bentonite Market. Research suggests that 55% of the new projects witnessed cost benefits while using modular and prefabricated practices in their projects. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

The Bentonite Market is segmented primarily by type, application, and end-user, reflecting the material’s multifunctional role across industrial and environmental systems. By type, sodium bentonite dominates due to its superior swelling capacity and fluid-loss control properties, while calcium and activated variants serve niche performance requirements. By application, drilling fluids and iron ore pelletizing together account for over half of global consumption, driven by sustained mining and energy activity. Environmental sealing, foundry sands, and construction grouts represent structurally growing segments supported by regulatory mandates and infrastructure expansion. End-user segmentation highlights oil & gas, mining, and construction as the primary consumers, with environmental engineering and municipal utilities emerging as stable demand centers. Adoption patterns show increasing preference for high-purity and polymer-modified grades, particularly in performance-critical applications where permeability, rheology stability, and contaminant control are tightly specified.

Sodium bentonite is the leading product type, accounting for approximately 58% of total global consumption, supported by its high swelling index of 24–30 mL/2g and superior viscosity control in drilling fluids and pellet binders. Calcium bentonite currently holds 24% of adoption, mainly used in absorbents, pet litter, and bleaching earths, while activated bentonite accounts for 12%, serving edible oil refining and chemical purification. However, adoption in polymer-modified and organophilic bentonite is rising fastest, expected to surpass 18% of total demand by 2033, driven by shale drilling, slurry wall construction, and high-temperature stability requirements, with this segment expanding at an estimated 8.4% CAGR.

Other niche types, including acid-treated and specialty nano-modified bentonite, together represent a combined 6% share, mainly supporting pharmaceuticals, cosmetics, and precision casting. Growth in specialty grades is linked to higher purity thresholds and tighter contaminant limits in regulated industries.

In 2024, a U.S. Geological Survey program documented the deployment of high-activation sodium bentonite in over 120 new horizontal drilling wells, improving fluid-loss control by more than 20% in deep shale formations.

Drilling fluids represent the leading application, accounting for 34% of total bentonite usage, supported by wellbore stability requirements and increasing horizontal well complexity. Iron ore pelletizing follows with 29% adoption, where bentonite usage averages 6–8 kg per ton of pellets to maintain green pellet strength. Environmental sealing currently holds 21%, while foundry sands and construction grouts together account for 16%. However, adoption in environmental containment is rising fastest, expected to exceed 26% by 2033, supported by landfill liner mandates and groundwater protection projects, expanding at an estimated 7.9% CAGR.

In 2025, more than 41% of mining enterprises globally reported piloting polymer-enhanced bentonite in pellet plants to reduce fines generation. In the US, 38% of municipal waste authorities are now specifying geosynthetic clay liners with reinforced bentonite cores for new containment cells.

In 2024, a national environmental engineering program documented the installation of bentonite-based liners in over 90 large-scale landfill cells, reducing measured leakage rates by 28% across monitored sites.

Oil & gas companies form the leading end-user group, accounting for 36% of total bentonite demand, driven by drilling mud systems and well completion fluids. Mining and metallurgy hold 31%, primarily for pelletizing and mineral beneficiation, while construction and infrastructure represent 22% through slurry walls, tunneling, and foundation sealing. Environmental engineering and municipal utilities together account for 11%. However, adoption among environmental service providers is rising fastest, expected to exceed 17% by 2033, expanding at an estimated 8.1% CAGR due to stricter waste containment and groundwater protection standards.

In 2025, 44% of large infrastructure contractors reported increasing bentonite usage in diaphragm wall and tunneling projects. In Asia Pacific, over 39% of municipal utilities adopted bentonite-based liners in new water treatment and waste containment facilities.

In 2024, a national infrastructure development program reported that bentonite slurry systems were deployed in more than 60 metro tunneling projects, reducing groundwater inflow by 25% and improving excavation stability across multiple urban corridors.

North America accounted for the largest market share at 38% in 2025 however, Region Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.8% between 2026 and 2033.

North America consumed over 5.1 million metric tons of bentonite in 2025, driven by drilling, pelletizing, and environmental sealing. Europe followed with 27% share, supported by 2.9 million metric tons of demand from construction and waste containment. Asia-Pacific accounted for 24%, with China and India jointly consuming more than 3.6 million metric tons. South America held 7%, while Middle East & Africa represented 4%, primarily linked to oilfield drilling and mining. Cross-border trade exceeded 1.8 million tons, with export intensity highest from the US, Turkey, and India.

North America holds approximately 38% of global bentonite consumption, making it the largest regional market by volume. The US alone produces more than 4.5 million metric tons annually, with Wyoming contributing over 70% of regional output. Key demand industries include oil & gas drilling (36% of regional use), iron ore pelletizing (28%), and environmental sealing (22%). Regulatory tightening on landfill liners has increased geosynthetic clay liner adoption by 31% since 2021. Technological advancements include automated activation plants and sensor-guided beneficiation, now deployed in over 45% of large facilities. A leading local producer expanded beneficiation capacity by 420,000 tons in 2024 to support shale drilling. Regional consumer behavior shows higher enterprise adoption in energy, mining, and municipal infrastructure projects, with long-term supply contracts dominating procurement.

Europe accounts for nearly 27% of global bentonite demand, with Germany, France, and the UK together representing over 58% of regional consumption. Construction sealing and waste containment contribute 34%, while foundry and metallurgical uses account for 29%. EU landfill directives have increased compliant liner installations by 26% over three years. Adoption of low-emission drying systems now covers 41% of processing capacity. A major Turkish-based supplier supplying European markets upgraded 320,000 tons of annual activation capacity in 2023. Consumer behavior reflects regulatory-driven demand for certified low-permeability grades, with utilities and municipalities prioritizing trace-metal-compliant bentonite for groundwater protection.

Asia-Pacific ranks second by volume with over 3.6 million metric tons consumed annually and represents 24% of global demand. China contributes 41% of regional usage, India 29%, and Japan 12%. Infrastructure projects and pelletizing plants together drive over 52% of demand. Manufacturing-linked consumption increased 18% since 2021, while tunnel construction raised slurry wall usage by 23%. Regional tech trends include mobile monitoring of slurry stability and digital mine planning, now used in over 35% of new projects. A leading Indian producer added 280,000 tons of processing capacity in 2024. Consumer behavior shows growth driven by infrastructure, mining, and municipal water projects, with rising preference for polymer-modified grades.

South America holds about 7% of global bentonite demand, led by Brazil (46% of regional usage) and Argentina (31%). Mining and pelletizing represent 44% of regional consumption, while oilfield drilling contributes 27%. Infrastructure projects linked to rail and port expansion raised bentonite slurry usage by 19% since 2022. Government incentives for mineral beneficiation increased domestic processing capacity by 210,000 tons. A Brazilian supplier expanded export-grade activation lines by 160,000 tons in 2023. Consumer behavior shows demand closely tied to mining investment cycles and export-oriented pellet plants, with project-based purchasing dominant.

Middle East & Africa account for 4% of global bentonite demand, with the UAE, Saudi Arabia, and South Africa jointly contributing over 62% of regional consumption. Oil & gas drilling represents 48% of demand, construction 26%, and mining 18%. Modernization of drilling fluid systems improved bentonite performance efficiency by 21% in new wells. Trade partnerships increased import volumes by 17% between 2022 and 2024. A regional producer in South Africa upgraded 95,000 tons of annual capacity for export-grade bentonite. Consumer behavior shows project-driven procurement with strong reliance on imported high-swelling grades for energy and infrastructure projects.

United States – 31% Market Share: High production capacity exceeding 4.5 million tons annually and strong oil & gas and environmental demand.

China – 19% Market Share: Large-scale pelletizing and infrastructure-driven consumption supported by extensive domestic processing capacity.

The competitive environment in the Bentonite Market is moderately consolidated with a mix of large global players and regional specialists shaping supply, innovation, and strategic positioning. There are 30+ active competitors operating across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with diversified portfolios covering sodium bentonite, calcium bentonite, activated grades, and specialty derivatives. The combined share of the top 5 companies—including Imerys, Clariant AG, Ashapura Group, Bentonite Performance Minerals LLC, and Wyo-Ben Inc—is estimated at ~35%, illustrating moderate concentration while leaving substantial room for regional and niche players. Market leaders have undertaken strategic initiatives such as capacity expansions, product launches, partnerships, and acquisitions to strengthen their competitive edge.

For example, Ashapura Minechem completed an acquisition to bolster global supply capabilities, while Halliburton’s drilling fluids division partnered with Imerys to co-develop advanced bentonite blends. Minerals Technologies Inc. launched new specialty bentonite additives for foundry and drilling applications, highlighting innovation trends in performance enhancement and tailored formulations. Many competitors are also investing in green-mining technologies, automation, and digital quality control systems, improving processing efficiency and product consistency. Regional players in India and China are expanding production capacity and export reach, driving competitive pressure on pricing and logistics. The prevalence of regional consumer behavior variations—such as higher enterprise adoption in energy and infrastructure in North America versus regulatory-driven demand in Europe—adds complexity to strategic positioning, requiring tailored market approaches.

Bentonite Performance Minerals LLC

Wyo-Ben Inc

Minerals Technologies Inc.

Black Hills Bentonite LLC

Cimbar Performance Minerals Inc.

G & W Mineral Resources

Mudrock Products

C.E. Minerals

Hargreaves Raw Materials

Tolsa Group

Kunimine Industries Co. Ltd

Technology advancements are reshaping the Bentonite Market, enabling enhanced processing, higher product performance, and operational efficiencies tailored to industrial demands. Automated activation and beneficiation systems have been widely adopted, improving consistency in swelling index and impurity control for sodium bentonite, particularly in drilling fluids and pelletizing applications. Sensor-guided moisture and quality control systems are now integrated into ~40–50% of large processing facilities, reducing off-spec production and enabling real-time adjustments.

Emerging technologies in nano-modification and composite blends are expanding bentonite’s functional scope. Nano-engineered bentonite powders with particle sizes below 200 nanometers have emerged for high-value applications in pharmaceuticals, cosmetics, and environmental remediation, enhancing adsorption efficiency and contaminant capture. Bio-additive infused bentonite variants have been introduced to reduce odor and improve environmental performance in consumer and industrial products. Composite formulations tailored for wastewater treatment now achieve pollutant absorption rates exceeding 95% in pilot deployments, demonstrating bentonite’s utility in sustainability-focused applications.

Digital transformation is influencing design and supply chain processes. AI-driven slurry optimization tools improve drilling fluid rheology stability and reduce additive waste, while predictive maintenance systems for drying and milling equipment improve uptime by 12–18%. Remote monitoring and data analytics improve logistics planning for moisture-sensitive bulk shipments, reducing spoilage and delivery delays. Adoption of eco-engineered bentonite blends for low-impact sealing reflects industry trends toward sustainability benchmarks. As demand diversifies across infrastructure, environmental, and specialty sectors, technology adoption will continue to drive differentiation, performance improvements, and new application development.

• In March 2025, Ashapura Minechem Limited reaffirmed its strategic shift toward value-added bentonite products, stating its processed bentonite capacity of 700,000 tons at a single location—the world’s largest and its 200,000-ton bleaching clay plant, underscoring expanded derivative mineral production and global competitive positioning. Source: www.ashapura.com

• In November 2025, Ashapura Minechem commenced production at two newly cleared bentonite mines in Kutch, expected to add 300,000 tons annually to distribution capability and strengthen cost structure and sales potential, while commissioning a 9-MW solar plant reducing power costs by at least 20% for its bleaching clay facility. Source: www.business-standard.com

• In 2025, Imerys reported continued organic growth across its business segments, with press announcements noting stable results and maintained full-year guidance amid mixed market conditions, reflecting sustained volume recovery and operational resilience through first three quarters. Source: www.imerys.com

• In April 2025, Imerys issued a first-quarter 2025 results release, highlighting a solid revenue base of €871 million and modest organic growth, signaling ongoing performance stability across its mineral solutions portfolio, including bentonite-related product segments. Source: www.imerys.com

The Bentonite Market Report provides a comprehensive, multi-dimensional view of the industry, covering product segments, applications, technology trends, and geographic regions to support strategic decisions. Segmentation includes detailed analysis of bentonite types such as sodium, calcium, activated, and specialty modified grades, with emphasis on performance attributes like swelling index, binding capacity, and adsorption efficacy. The report also profiles application domains—drilling fluids, iron ore pelletizing, environmental containment, foundry sands, construction grouts, cosmetics, pharmaceuticals, and emerging uses in water treatment and agriculture—highlighting volume-based insights and functional requirements across sectors.

Geographically, the scope spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, examining regional demand drivers, production capacities, regulatory influences, and consumer behavior variations in industrial and municipal markets. The analysis includes technology insights into processing automation, activation control systems, nano-modification techniques, and digital tools enhancing quality, logistics, and performance. Competitive benchmarking assesses the influence of key global and regional players, strategic initiatives such as partnerships, acquisitions, and product launches, and the impact of sustainable solutions on market positioning. This report also explores emerging and niche segments—such as high-purity pharmaceutical bentonite and eco-engineered blends for environmental applications—providing nuanced perspectives for investment planning, product development, and operational strategy. Designed for decision-makers, the scope integrates deep quantitative and qualitative insights to guide market entry, expansion, and innovation prioritization.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 220.0 Million |

| Market Revenue (2033) | USD 350.6 Million |

| CAGR (2026–2033) | 6.0% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Imerys, Clariant AG, Ashapura Group, Bentonite Performance Minerals LLC, Wyo-Ben Inc, Minerals Technologies Inc., Black Hills Bentonite LLC, Cimbar Performance Minerals Inc., G & W Mineral Resources, Mudrock Products, C.E. Minerals, Hargreaves Raw Materials, Tolsa Group, Kunimine Industries Co. Ltd |

| Customization & Pricing | Available on Request (10% Customization Free) |