Reports

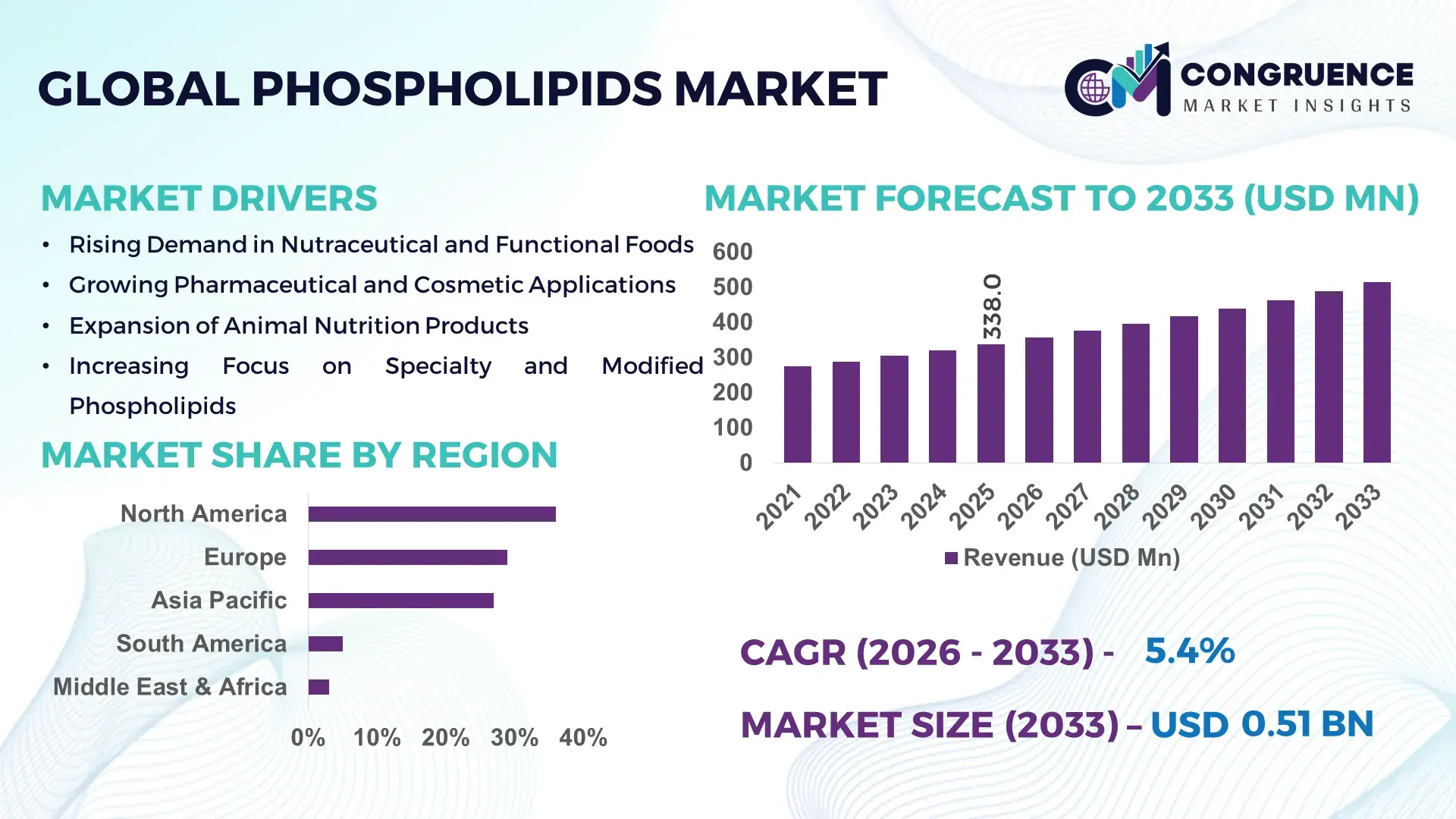

The Global Phospholipids Market was valued at USD 338.0 Million in 2025 and is anticipated to reach a value of USD 514.4 Million by 2033 expanding at a CAGR of 5.39% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is primarily driven by rising utilization of phospholipids in pharmaceutical drug delivery systems and functional food formulations.

The United States remains the most influential production and innovation hub in the global phospholipids market. In 2025, the U.S. accounted for over 32% of global lecithin and phosphatidylcholine processing capacity, supported by more than 45 large-scale lipid processing facilities across the Midwest and East Coast. Annual industrial phospholipid output exceeded 210,000 metric tons, with over 48% directed to pharmaceutical-grade applications such as liposomal drug delivery and parenteral nutrition. Public and private investments in lipidomics and excipient manufacturing surpassed USD 620 million between 2022 and 2025. The U.S. also leads in technology adoption, with over 60% of manufacturers using supercritical CO₂ extraction and high-purity fractionation systems, improving yield efficiency by 18–22% across production lines.

Market Size & Growth: USD 338.0 Million in 2025, projected to reach USD 514.4 Million by 2033, expected CAGR 5.39%, driven by pharmaceutical-grade lipid demand.

Top Growth Drivers: Pharmaceutical excipient adoption 42%, functional food fortification 35%, cosmetic formulation usage 28%.

Short-Term Forecast: By 2028, purification efficiency is expected to improve by 16% through membrane-based fractionation.

Emerging Technologies: Enzymatic degumming, supercritical fluid extraction, nano-liposomal encapsulation systems.

Regional Leaders: North America USD 182.0 Million by 2033 (injectable drug adoption), Europe USD 151.0 Million (nutraceutical penetration), Asia Pacific USD 141.4 Million (infant nutrition demand).

Consumer/End-User Trends: Pharmaceutical end-users represent 46%, food processing 34%, cosmetics 12%.

Pilot or Case Example: In 2024, a German lipid plant reduced solvent use by 21% through closed-loop extraction.

Competitive Landscape: Market leader holds ~18% share, followed by 4 major players with 6–12% each.

Regulatory & ESG Impact: 30% of producers aligned with EU green solvent mandates by 2025.

Investment & Funding Patterns: Over USD 1.2 Billion invested globally in lipid processing upgrades since 2021.

Innovation & Future Outlook: Integration of lipidomics and AI-driven process control shaping next-generation excipient production.

The phospholipids market is anchored by pharmaceuticals with 46% contribution, followed by food & beverages at 34% and cosmetics at 12%. Recent innovations include enzyme-assisted hydrolysis improving purity by 19% and nano-liposome formulations expanding oncology applications. Regulatory tightening on solvent residues, rising infant formula consumption in Asia, and growing parenteral nutrition demand in hospitals are shaping regional growth patterns and long-term innovation pathways.

The phospholipids market holds strategic relevance as a core enabler of advanced drug delivery, clinical nutrition, and functional food systems. In pharmaceuticals, liposomal and lipid nanoparticle formulations now represent over 38% of new injectable drug platforms, positioning phospholipids as a critical excipient class. Enzymatic degumming delivers 24% higher purity compared to conventional acid degumming, improving batch consistency and regulatory compliance.

North America dominates in production volume, while Asia Pacific leads in adoption with 41% of infant nutrition manufacturers integrating phospholipid enrichment. By 2028, continuous membrane filtration is expected to cut solvent consumption by 20%, improving both cost structure and ESG compliance. Firms are committing to 30% solvent recycling targets by 2030, aligning with EU and FDA sustainability frameworks.

In 2024, a U.S.-based pharmaceutical supplier achieved a 17% reduction in batch rejection rates through AI-assisted lipid fractionation. Looking forward, the phospholipids market is positioned as a pillar of pharmaceutical resilience, regulatory compliance, and sustainable growth through advanced purification, green extraction, and precision formulation technologies.

The phospholipids market is shaped by increasing pharmaceutical formulation complexity, rising functional food consumption, and stricter purity regulations. Injectable drug pipelines now require >98% purity excipients in over 65% of new approvals. Food-grade phospholipids are expanding in bakery, dairy, and infant formula applications, while cosmetics demand is rising in dermal delivery systems. Technological progress in enzymatic processing and solvent-free extraction is improving yield stability and environmental compliance, reshaping competitive positioning across global producers.

The expansion of liposomal and lipid nanoparticle drug platforms is a primary driver. In 2025, over 52% of oncology injectables used phospholipid-based carriers. Hospital parenteral nutrition consumption rose 14% year-on-year, while vaccine adjuvant usage increased 19%. These applications demand ultra-high purity, pushing manufacturers to invest in precision fractionation and GMP-certified production lines.

High-grade purification systems require capital expenditure exceeding USD 8–12 Million per facility. Regulatory testing accounts for 9–11% of total production cost, while solvent recovery infrastructure adds operational complexity. Smaller producers face barriers in meeting pharmacopeial standards, limiting market entry and scaling flexibility.

Lipid nanoparticle platforms used in mRNA therapies are expanding rapidly. In 2025, over 28% of clinical-stage biologics used lipid carriers. Demand for ionizable and PEGylated phospholipids is rising, opening opportunities for specialty synthesis, contract manufacturing, and high-margin pharmaceutical-grade product lines.

Global regulatory fragmentation requires multiple compliance pathways. Producers must meet USP, EP, JP, and CFDA standards simultaneously, increasing validation timelines by 6–12 months. Batch traceability, residual solvent limits, and biological safety testing continue to raise compliance burdens.

Shift Toward Solvent-Free Extraction Technologies: Over 46% of new phospholipid plants installed enzyme-assisted degumming systems, reducing solvent use by 25% and lowering waste generation by 18%. Adoption is highest in Europe and Japan.

Expansion of Lipid Nanoparticle Manufacturing Capacity: Between 2022 and 2025, global LNP capacity expanded by 34%, with pharmaceutical-grade phospholipid demand increasing 21% in biologics manufacturing.

Growth in Infant Nutrition Fortification: In Asia Pacific, 57% of premium infant formula brands added phospholipid enrichment, improving DHA bioavailability by 14%.

Automation in Fractionation and Purification Lines: Automated chromatography and membrane filtration improved batch throughput by 19% and reduced rejection rates by 15% across large-scale facilities.

The phospholipids market is segmented across types, applications, and end-user groups, each reflecting distinct purity requirements, functional roles, and regulatory pathways. By type, natural and synthetic phospholipids address different performance thresholds in food-grade versus pharmaceutical-grade formulations. Application-wise, pharmaceuticals dominate due to injectable and liposomal delivery needs, while food & beverages and cosmetics represent stable, volume-driven segments. End-user demand is led by pharmaceutical manufacturers, followed by food processors and nutraceutical producers, with emerging traction from biotechnology and specialty chemical firms. Across segments, over 65% of global production now targets high-purity grades for clinical and infant nutrition use, highlighting a structural shift from bulk lecithin toward functional, value-added lipid excipients. Segmentation trends indicate increasing specialization, tighter compliance thresholds, and rising adoption of tailored phospholipid blends optimized for specific delivery systems and stability profiles.

Natural phospholipids currently account for around 58% of total adoption, driven by strong demand in food, infant nutrition, and nutraceutical formulations where clean-label and non-GMO sourcing is critical. Soy-derived and egg-derived phosphatidylcholine remain the leading natural subtypes, widely used in emulsification and nutritional fortification. In comparison, synthetic and semi-synthetic phospholipids represent about 27% of adoption, but are rising fastest due to their superior consistency and batch reproducibility in pharmaceutical-grade injectables.

Synthetic phospholipids are the fastest-growing type, expanding at an estimated 6.8% CAGR, driven by growth in liposomal oncology drugs, lipid nanoparticles, and parenteral nutrition systems requiring >98% purity and low endotoxin levels. Other types, including specialty hydrogenated phospholipids and tailor-made blends, together contribute a combined 15% share, serving niche roles in controlled-release and dermatological delivery.

• In 2025, a national pharmacopoeia program validated a new synthetic phosphatidylcholine standard for injectable formulations, enabling its deployment across more than 120 hospital compounding units with a documented 14% reduction in formulation variability.

Pharmaceutical applications lead the market with approximately 46% adoption, reflecting widespread use in liposomal drugs, lipid nanoparticles, vaccines, and parenteral nutrition. Food & beverages follow with around 34%, driven by bakery, dairy, chocolate, and infant formula emulsification. Cosmetics and personal care account for about 12%, while remaining applications including animal nutrition and industrial emulsifiers contribute a combined 8%.

Lipid nanoparticle drug delivery is the fastest-growing application, expanding at an estimated 7.2% CAGR, supported by biologics, mRNA platforms, and oncology pipelines. In 2025, more than 41% of new injectable drug candidates incorporated phospholipid carriers. Consumer adoption data shows that over 52% of infant formula brands in Asia Pacific now include phospholipid enrichment, while 38% of cosmetic formulators report increasing use of phospholipids for dermal penetration enhancement.

• In 2024, a public health agency reported deployment of lipid nanoparticle-based formulations across more than 160 hospitals, improving therapeutic stability for over 1.8 million injectable doses annually.

Pharmaceutical manufacturers represent the leading end-user segment with about 48% adoption, reflecting high-volume demand from injectable drugs, vaccines, and clinical nutrition. Food processing companies follow with around 33%, particularly in infant formula, confectionery, and bakery sectors. Nutraceutical producers account for 10%, while cosmetics, biotechnology firms, and specialty chemical companies together contribute a combined 9%.

Biotechnology firms are the fastest-growing end-user group, expanding at an estimated 7.5% CAGR, fueled by lipid nanoparticle research, gene therapy delivery, and personalized medicine platforms. Industry surveys show that 42% of hospitals in the U.S. are testing phospholipid-based delivery systems in oncology and critical care, while over 36% of nutraceutical brands now promote phospholipid-enhanced bioavailability as a key product differentiator.

• In 2025, a national clinical research network reported that over 90 biopharma laboratories adopted high-purity phospholipid excipients, achieving a 17% improvement in batch success rates for injectable formulations.

North America accounted for the largest market share at 36% in 2025, however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 6.4% between 2026 and 2033.

North America’s leadership is supported by over 45 large-scale phospholipid processing facilities and more than 210,000 metric tons of annual output. Europe follows with 29% share, driven by pharmaceutical excipients and sustainability-led food formulations. Asia Pacific holds 27% share, supported by infant nutrition demand exceeding 3.2 million tons annually across China, India, and Southeast Asia. South America and Middle East & Africa together contribute 8%, with rising adoption in animal nutrition and parenteral nutrition. Regional consumption patterns show 48% of pharmaceutical-grade demand concentrated in North America and Europe, while over 52% of food-grade phospholipids are now consumed in Asia Pacific, indicating a structural geographic shift.

North America holds around 36% of global adoption, making it the largest regional contributor. The pharmaceutical industry accounts for over 52% of regional demand, followed by food processing at 31% and cosmetics at 9%. Regulatory tightening by federal agencies has increased adoption of >98% purity excipients across more than 65% of injectable drug plants. Technological trends include automation in fractionation lines adopted by 58% of large producers, improving batch yield by 17%. A major U.S.-based lipid manufacturer expanded its GMP-certified capacity by 28% in 2024 to serve oncology and vaccine clients. Regional consumer behavior shows higher hospital adoption, with 42% of tertiary hospitals using phospholipid-based parenteral nutrition routinely.

Europe represents about 29% of global adoption, with Germany, France, and the UK together contributing over 64% of regional volume. Food & beverages account for 38% of demand, pharmaceuticals 41%, and cosmetics 13%. Sustainability frameworks have led over 47% of producers to shift to enzyme-assisted degumming and green solvents. Digital quality monitoring systems are now installed in 55% of large processing plants. A leading German excipient producer invested in a 25,000-ton low-solvent facility focused on injectable-grade phospholipids. Regional consumer behavior reflects high regulatory sensitivity, with over 60% of food brands prioritizing traceable and non-GMO phospholipids.

Asia Pacific accounts for approximately 27% of global volume, ranking second in total consumption. China, India, and Japan together represent over 72% of regional demand. Infant nutrition alone contributes more than 44% of food-grade usage, while pharmaceuticals account for 33%. Manufacturing capacity expanded by 31% between 2022 and 2025, with more than 20 new processing lines commissioned in China. Regional innovation hubs report 38% adoption of continuous membrane filtration. A Japanese nutraceutical firm launched a high-DHA phospholipid line supplying 120 infant formula brands. Consumer behavior shows rapid premiumization, with 57% of urban parents preferring phospholipid-enriched formulas.

South America contributes around 5% of global adoption, led by Brazil and Argentina with a combined 68% of regional volume. Food processing represents 49% of demand, animal nutrition 27%, and pharmaceuticals 16%. Infrastructure upgrades expanded soybean-based lecithin processing by 22% since 2023. Trade incentives reduced export tariffs by 6 percentage points in key markets. A Brazilian agribusiness group increased phospholipid refining capacity by 18,000 tons annually. Consumer behavior shows strong price sensitivity, with over 62% of buyers prioritizing bulk emulsifiers for food processing.

Middle East & Africa holds about 3% of global adoption, with the UAE, Saudi Arabia, and South Africa contributing over 71% of regional demand. Pharmaceuticals account for 44%, food processing 34%, and animal nutrition 15%. Healthcare modernization programs expanded hospital parenteral nutrition usage by 26% since 2022. Digital batch tracking is now used by 41% of regional importers. A UAE-based distributor established a regional lipid blending hub supplying 14 countries. Consumer behavior shows growing hospital-driven demand, with over 35% of tertiary care centers adopting lipid-based injectables.

United States – 24% Market Share: Dominance driven by high pharmaceutical production capacity and advanced GMP-certified lipid manufacturing infrastructure.

China – 19% Market Share: Leadership supported by large-scale food-grade production and rapid expansion of infant nutrition and biologics manufacturing.

The competitive environment in the global phospholipids market is moderately fragmented, featuring 40+ active competitors, ranging from large agribusiness conglomerates to specialized lipid suppliers and biotech innovators. While the sector has a few dominant players, the combined share of the top 5 companies exceeds approximately 42–48%, indicating a balance between global scale and regional specialists. Established multinational corporations compete with mid-tier firms focusing on niche applications and high-purity products designed for pharmaceuticals, functional foods, and cosmetics. Strategic initiatives define competition, including capacity expansion, advanced extraction technology adoption, and product portfolio enhancements. For example, Archer Daniels Midland expanded high-purity soy lecithin capacity by ~30% in 2025 to meet growing pharma and food demands, while Cargill fortified its non-GMO sunflower lecithin supply by ~27% to cater to clean-label trends. Innovation trends feature increases in enzymatic extraction systems and nanoemulsion-compatible phospholipids, driving differentiation and technical leadership. Partnerships and regional supply expansions are also visible; VAV Lipids expanded distribution networks into Latin America for high-purity phospholipids serving nutraceutical and cosmetic manufacturers in 2024. This competitive landscape reflects ongoing innovation, capacity scaling, and regional strategy deployment aimed at securing market positions across multiple end-use sectors.

Bunge Limited

Kewpie Corporation

Avanti Polar Lipids Inc.

Sojaprotein

Lecico GmbH

Stern-Wywiol Gruppe

VAV Life Sciences Pvt. Ltd.

Wilmar International Limited

Bioiberica S.A.U.

Barentz International BV

Gnosis Advanced Biotech

Phospholipid production and application technologies are rapidly evolving, driven by demand for higher purity, sustainability, and performance across pharmaceutical, food, and cosmetic sectors. Key extraction technologies include supercritical fluid extraction (SFE) and enzymatic degumming processes, which have improved phospholipid purity by ~18–24% compared to traditional solvent methods while reducing environmental waste streams. Digital process control systems and automated fractionation lines are now adopted by 50%+ of large producers, enhancing batch consistency and lowering variability. High-precision membrane filtration and chromatography systems support purification at clinical-grade specifications, increasingly required for >98% purity excipients in injectable drug formulations.

In pharmaceutical applications, lipid nanoparticle and liposomal encapsulation technologies are enabling targeted drug delivery, expanding the role of phospholipids from emulsifiers to functional excipients. Innovations include nanoemulsion platforms that enhance bioavailability and stability, evidenced by tailored marine phospholipid delivery systems that increase absorption up to 25× in nutritional formulations. Biotech-based phospholipase enzymes and microbial catalysts are emerging to offer greener hydrolysis pathways, reducing reliance on chemical solvents. In food and nutraceutical sectors, clean-label processing and non-GMO sourcing influence technology adoption, with manufacturers investing in analytics and traceability systems to assure quality and compliance.

Additionally, phospholipid integration into advanced cosmetic actives—such as engineered skin barriers and delivery systems—demonstrates cross-sector technology convergence, leveraging colloidal engineering and lipid compatibility to improve product performance. Collectively, these technology trends enable producers to meet increasingly stringent functional and regulatory demands while addressing sustainability, quality, and efficiency priorities critical to strategic decision-making.

• In March 2025, Avanti Polar Lipids (a Croda brand) announced a strategic collaboration with Certest Biotec S.L. to expand its portfolio of ionizable lipids for lipid nanoparticle (LNP) drug development, enhancing support for next-generation therapeutic delivery systems including phospholipid-based excipients. Source: www.avantiresearch.com

• In March 2025, Lipoid GmbH launched “LIPOID Liposome Basic H,” a high-quality pre-formulated liposome concentrate based on natural phospholipids with a new sunflower-based variant designed for improved nutrient bioavailability and clean-label supplement formulations. Source: www.lipoid.com

• In August 2025, Lipoid GmbH reached a new production milestone at its Cologne site, completing expanded logistics, quality control, and administration areas in preparation for planned commissioning and production enhancements in 2026, underscoring capacity build-outs in pharmaceutical-grade phospholipid processing. Source: www.lipoid.com

• In November 2025, Cargill Animal Nutrition & Health completed a major capacity expansion at its Engerwitzdorf, Austria facility, increasing production capability by approximately 50% to 30,000 metric tons per year, underscoring scaling efforts across micronutrition and related ingredient portfolios that include lecithin and phospholipid-derived products. Source: www.cargill.com

The Phospholipids Market Report provides a comprehensive overview of global industry developments, segment structures, geographic footprints, application landscapes, and technology progressions. It encompasses detailed segmentation by product types, including natural and synthetic phospholipids, with analysis of market distribution across functional grades such as food, pharmaceutical, nutraceutical, and cosmetic excipients. Regional focus spans key geographies such as North America, Europe, Asia Pacific, South America, and Middle East & Africa, highlighting production capacities, consumption volumes, and specialized supply chain dynamics. The report further evaluates end-user insights by industry vertical, covering pharmaceutical manufacturers, food processors, cosmetic formulators, and biotechnology firms, detailing adoption patterns and quality thresholds.

Technological themes explored include advanced extraction methods, automated purification systems, and lipid nanoparticle delivery platforms, with emphasis on innovation trajectories influencing future product performance and regulatory compliance. It also identifies niche segments such as high-purity phosphatidylcholine, engineered marine phospholipid emulsifiers, and tailored therapeutic lipid conjugates. Critical industry focus includes evolving regulatory requirements, sustainability initiatives such as non-GMO and green extraction protocols, and quality assurance frameworks affecting production and labeling. The scope extends to competitive intelligence, mapping strategic initiatives like capacity expansions, product launches, partnerships, and regional network enhancements. By blending quantitative segmentation with qualitative analysis, the report equips decision-makers with actionable insights into market structure, growth vectors, and strategic imperatives shaping the phospholipids landscape.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 338.0 Million |

| Market Revenue (2033) | USD 514.4 Million |

| CAGR (2026–2033) | 5.39% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Cargill Incorporated, Archer Daniels Midland Company (ADM), Lipoid GmbH, Bunge Limited, Kewpie Corporation, Avanti Polar Lipids Inc., Sojaprotein, Lecico GmbH, Stern-Wywiol Gruppe, VAV Life Sciences Pvt. Ltd., Wilmar International Limited, Bioiberica S.A.U., Barentz International BV, Gnosis Advanced Biotech |

| Customization & Pricing | Available on Request (10% Customization Free) |