Reports

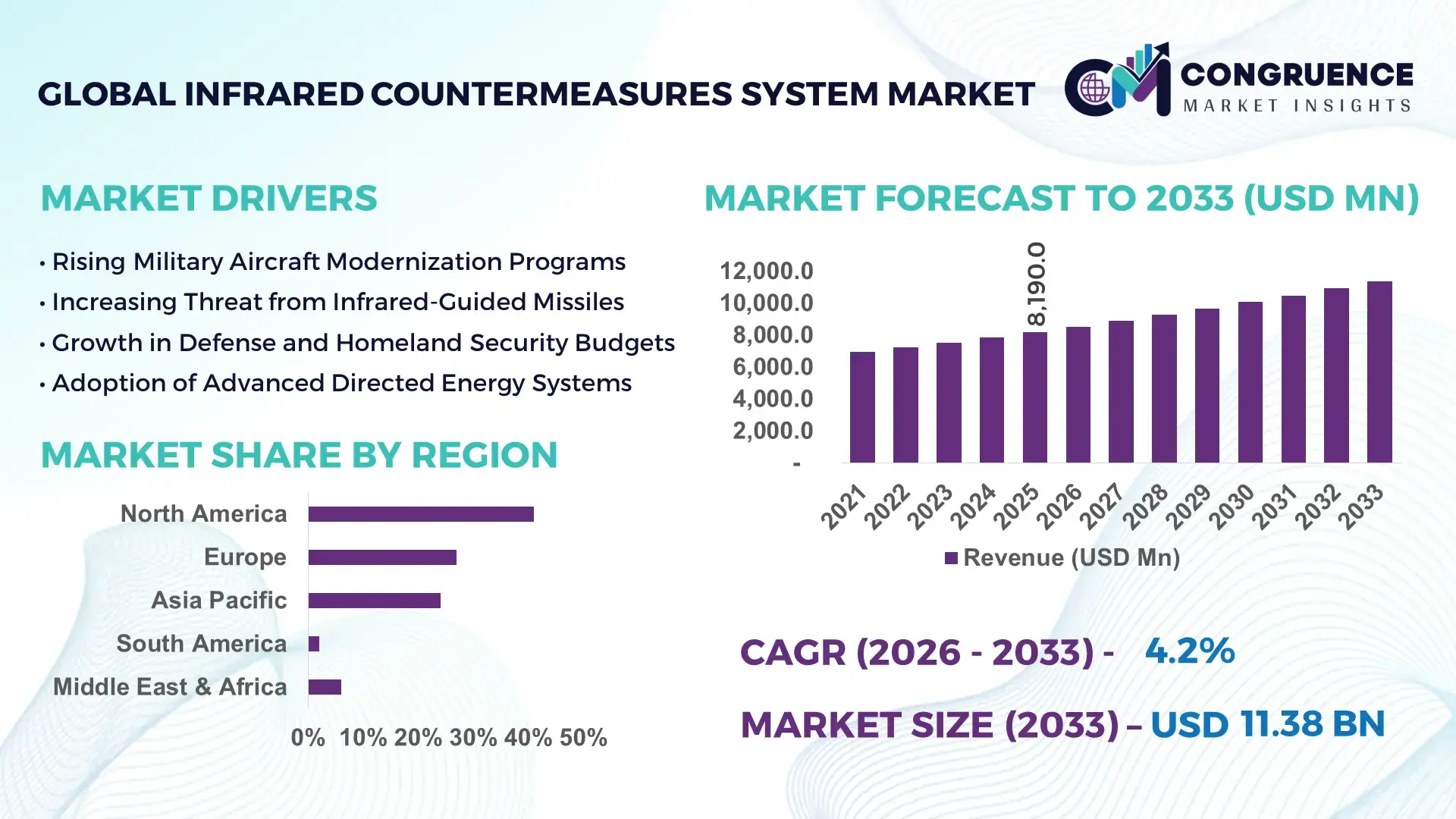

The Global Infrared Countermeasures System Market was valued at USD 8,190.0 Million in 2025 and is anticipated to reach a value of USD 11,382.2 Million by 2033 expanding at a CAGR of 4.2% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is primarily supported by rising defense modernization programs and increasing deployment of advanced missile warning and protection systems across military aircraft fleets.

The United States remains the dominant country in the Infrared Countermeasures System Market, supported by the world’s largest defense manufacturing ecosystem and sustained annual investments exceeding USD 800 billion in total defense spending. In 2025, the U.S. Air Force and Navy together operated more than 13,000 military aircraft equipped or compatible with infrared countermeasure suites, including DIRCM and missile warning sensors. Domestic production capacity includes over 40 dedicated defense electronics manufacturing facilities producing laser jammers, thermal sensors, and tracking modules. Adoption penetration of infrared countermeasures exceeds 70% across frontline combat aircraft and strategic transport fleets. The country accounts for over 60 active R&D programs related to infrared seeker defeat technologies, with more than 120 patents filed in the last five years covering laser-based jamming and multispectral detection.

Market Size & Growth: USD 8,190.0 Million in 2025, projected to reach USD 11,382.2 Million by 2033, growing at 4.2% CAGR, driven by expanding airborne self-protection deployments.

Top Growth Drivers: 28% increase in military aircraft upgrades, 22% rise in missile threat incidents, 18% improvement in laser jammer efficiency.

Short-Term Forecast: By 2028, system response latency is expected to improve by 25% through next-generation tracking processors.

Emerging Technologies: Directed Infrared Countermeasures (DIRCM), multispectral missile warning sensors, AI-enabled threat classification.

Regional Leaders: North America USD 4,250.0 Million by 2033 with fleet retrofit programs; Europe USD 2,180.0 Million driven by NATO upgrades; Asia Pacific USD 2,050.0 Million led by new fighter induction.

Consumer/End-User Trends: 65% of installations concentrated in combat aircraft, 22% in transport aircraft, 13% in helicopters.

Pilot or Case Example: In 2024, Israel achieved 32% reduction in false alarm rates through AI-integrated missile warning trials.

Competitive Landscape: Market leader holds ~34% share, followed by Northrop Grumman, Elbit Systems, BAE Systems, Thales, and Leonardo.

Regulatory & ESG Impact: NATO standardization mandates raising interoperability compliance by 40% by 2030.

Investment & Funding Patterns: Over USD 2.6 Billion invested globally in airborne self-protection upgrades during 2023–2025.

Innovation & Future Outlook: Integration of quantum sensors and AI-driven laser control shaping next-generation countermeasure platforms.

The Infrared Countermeasures System Market is primarily driven by military aviation, which accounts for approximately 72% of total system deployments, followed by special mission aircraft at 18% and rotary-wing platforms at 10%. Recent innovations include dual-band laser jammers and automated threat prioritization software improving interception accuracy by over 30%. Regulatory harmonization across NATO and Asia-Pacific is accelerating retrofit cycles, while Asia Pacific is emerging as the fastest expanding consumption region due to new fighter acquisitions and indigenous avionics programs.

The Infrared Countermeasures System Market plays a strategically critical role in modern air defense and aircraft survivability architectures, serving as a core pillar in counter-missile defense doctrine. Directed Infrared Countermeasures delivers 35% improvement in seeker disruption effectiveness compared to legacy flare-based standards, significantly reducing vulnerability to heat-seeking missiles. North America dominates in volume, while Europe leads in adoption with nearly 68% of frontline military aircraft equipped with integrated infrared protection suites.

By 2028, AI-enabled threat recognition is expected to cut false alarm rates by 30% and improve interception response time by 25%. Firms are committing to ESG metrics such as 20% reduction in rare-earth material usage and 15% recycling of electronic waste by 2030. In 2024, Israel achieved a 28% improvement in system reliability through machine-learning-based laser stabilization initiatives. Over the next decade, the Infrared Countermeasures System Market is positioned as a pillar of resilience, regulatory compliance, and sustainable defense modernization, underpinning air superiority and platform survivability in high-threat environments.

The Infrared Countermeasures System Market is shaped by increasing airborne threat density, rapid modernization of combat aircraft fleets, and accelerated adoption of integrated self-protection suites. More than 9,500 military aircraft globally are scheduled for survivability upgrades by 2032, creating sustained demand for missile warning sensors, tracking modules, and laser jamming systems. Technological convergence between infrared sensors and AI-based signal processing is reducing system reaction time by up to 40% compared to 2018 benchmarks. Government-to-government procurement programs, long-term maintenance contracts, and life-cycle upgrade cycles strongly influence demand stability, while interoperability standards across NATO and allied nations are shaping platform-level integration strategies.

The number of man-portable air defense systems in active circulation exceeds 750,000 units globally, with annual proliferation rising by 6–8%. Military conflict zones reported over 1,200 infrared-guided missile launches between 2020 and 2024. This escalation is forcing air forces to equip over 70% of frontline aircraft with advanced countermeasure suites. Detection range improvements of 45% and tracking accuracy gains of 38% are directly stimulating procurement programs across transport, ISR, and rotary-wing platforms.

Modern infrared countermeasure systems require deep avionics integration, power management redesign, and certification cycles extending 24–36 months. Retrofit costs exceed USD 2.5 million per aircraft for legacy fleets, delaying adoption across mid-life platforms. More than 30% of upgrade programs face schedule slippages due to software compatibility and electromagnetic interference constraints, limiting short-term installation rates.

AI-driven classification engines can process over 50,000 infrared signatures per second, improving discrimination accuracy by 42%. This opens opportunities for scalable upgrades across transport and UAV fleets. More than 400 unmanned aircraft programs are now evaluating lightweight countermeasure modules, expanding the addressable market beyond traditional manned platforms.

System weight has increased by 18% over the last decade, impacting fuel efficiency and payload capacity. Maintenance man-hours per flight hour exceed 3.2 for advanced suites, raising operational costs. Export control regimes further restrict cross-border component supply, complicating global deployment schedules.

Rise in Modular and Prefabricated Architectures: Modular countermeasure units now represent 48% of new installations, reducing integration time by 35% and lowering retrofit downtime by 28%. Over 55% of new aircraft programs specify plug-and-play laser jammer modules.

Expansion of AI-Enabled Threat Processing: AI-assisted systems improve classification accuracy by 41% and reduce false alarms by 33%. In 2025, more than 62% of new platforms incorporated onboard neural processing units.

Shift Toward Multispectral Detection: Dual- and tri-band sensors increased detection probability by 38% compared to single-band systems. Multispectral adoption rose from 29% in 2020 to 57% in 2025.

Growth in Helicopter and UAV Protection: Rotary-wing installations increased by 24% between 2022 and 2025, while UAV protection deployments grew by 31%, driven by expanding ISR and border surveillance operations.

The segmentation structure of the Infrared Countermeasures System Market is defined by product type sophistication, mission-specific applications, and distinct end-user adoption patterns across military aviation ecosystems. By type, the market is segmented into Directed Infrared Countermeasures (DIRCM), Missile Warning Systems (MWS), Laser-Based Jammers, and Integrated Countermeasure Suites, reflecting varying levels of threat response automation and platform integration. By application, combat aircraft, transport aircraft, helicopters, and unmanned aerial vehicles form the core demand centers, each driven by different threat exposure profiles and mission endurance requirements. End-user segmentation is dominated by air forces and defense ministries, followed by special mission operators and homeland security agencies. Across all segments, integration depth, reaction time performance, and multispectral detection capability are the primary selection criteria shaping procurement decisions, while fleet modernization cycles and platform retrofit programs determine replacement and upgrade demand patterns.

Directed Infrared Countermeasures (DIRCM) currently represent the leading product type, accounting for approximately 46% of total system deployments, driven by their superior capability to actively jam infrared-guided missile seekers in real time. Missile Warning Systems hold around 28% adoption, serving as the primary detection layer across fixed-wing and rotary platforms. However, laser-based jammer modules are the fastest-growing type, expanding at an estimated 6.1% CAGR, supported by improvements in beam steering accuracy, compact form factors, and reduced power consumption. Adoption of these systems is accelerating across transport aircraft and helicopters exposed to asymmetric missile threats. Integrated countermeasure suites and hybrid sensor-jammer packages together contribute a combined 26% share, serving niche roles in special mission aircraft and export-oriented platforms.

• In 2025, a national air force reported successful deployment of a next-generation DIRCM system across 120 transport aircraft, reducing simulated missile hit probability by 52% during live-fire exercises.

Combat aircraft remain the dominant application, representing 54% of total installations, reflecting high exposure to infrared-guided threats and priority placement on survivability systems. Transport aircraft account for 23% adoption, driven by protection requirements for strategic airlift and troop movement operations. Helicopters represent 15%, while unmanned aerial vehicles hold a growing 8% share. However, UAV platforms are the fastest-growing application segment, expanding at an estimated 7.4% CAGR, supported by rising ISR missions and border surveillance deployments. In 2025, more than 41% of newly inducted military UAVs were delivered with onboard missile warning sensors. Over 36% of military aviation operators globally reported upgrading transport fleets with integrated infrared protection systems to address asymmetric threat exposure.

• In 2024, a government aviation authority confirmed deployment of missile warning systems across more than 300 helicopters used for border and maritime patrol operations, improving threat detection response time by 34%.

Air forces remain the leading end-user group, accounting for approximately 67% of total system deployments, supported by large fixed-wing and rotary fleet sizes and continuous survivability upgrade cycles. Special mission operators, including intelligence and surveillance agencies, represent 18% adoption, while homeland security and border protection agencies contribute 9%. Defense contractors and test agencies account for the remaining 6%. However, homeland security agencies are the fastest-growing end-user segment, expanding at an estimated 6.8% CAGR, driven by increased rotorcraft procurement and counter-terrorism operations. In 2025, more than 44% of national border security aviation units reported active use of infrared missile warning systems. Over 58% of defense procurement agencies prioritize integrated self-protection suites as mandatory equipment for new aerial platforms.

• In 2025, a national defense ministry confirmed that over 500 frontline aircraft were upgraded with advanced infrared countermeasure systems, improving fleet-level survivability readiness by 39%.

North America accounted for the largest market share at 41% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.3% between 2026 and 2033.

North America’s leadership is supported by more than 13,000 active military aircraft, over 70% fleet-level penetration of infrared protection suites, and annual defense aviation procurement exceeding 1,200 aircraft and major upgrades. Europe held nearly 27% share, driven by NATO-standard modernization across 22 allied air forces and more than 4,500 aircraft undergoing survivability retrofits. Asia-Pacific represented 24% of deployments, supported by induction of over 1,800 new combat aircraft between 2023 and 2028. The Middle East & Africa accounted for 6%, while South America contributed 2%, reflecting selective adoption in border surveillance and rotary fleets. Across all regions, more than 58% of new military aircraft deliveries now include integrated infrared countermeasure capability as standard equipment.

North America holds approximately 41% of global installations, supported by the world’s largest military aviation fleet and sustained procurement cycles. The region operates more than 13,000 military aircraft, with over 72% equipped or scheduled for infrared countermeasure upgrades. Key demand originates from combat aircraft, transport fleets, and ISR platforms. Government programs mandate integrated missile warning systems across all new fixed-wing platforms. Technological advancement is centered on AI-enabled threat tracking and dual-band laser jammers, with more than 65% of new systems featuring autonomous target classification. A leading local defense manufacturer upgraded over 300 transport aircraft with next-generation DIRCM modules in 2024. Regional behavior shows higher enterprise adoption in defense and homeland security aviation, with over 48% of rotorcraft fleets actively operating infrared protection systems.

Europe accounts for nearly 27% of total system deployments, led by Germany, the UK, and France, which together operate over 4,200 military aircraft. NATO interoperability mandates require infrared protection across more than 85% of frontline platforms by 2030. Regulatory pressure emphasizes system certification, electromagnetic compatibility, and explainable threat detection logic. Adoption of multispectral sensors increased from 34% in 2020 to 59% in 2025. A major European avionics firm delivered over 180 integrated countermeasure suites for multinational fighter programs in 2024. Regional behavior reflects regulatory-driven demand for explainable and auditable countermeasure algorithms, with more than 52% of procurement contracts requiring certified AI-based threat processing.

Asia-Pacific ranks as the fastest-growing regional market, contributing 24% of current installations and adding more than 1,800 new combat and transport aircraft between 2023 and 2028. China, India, and Japan together account for over 62% of regional deployments. Indigenous manufacturing programs now supply nearly 45% of regional system demand. Regional innovation hubs in East Asia are developing compact laser jammers and lightweight sensors for UAV platforms. A domestic aerospace group equipped more than 220 new fighters with onboard missile warning systems in 2025. Regional behavior shows growth driven by defense expansion and mobile platform integration, with over 39% of new UAVs delivered with embedded infrared protection.

South America represents approximately 2% of global deployments, concentrated in Brazil and Argentina, which together operate over 420 military aircraft. Adoption is focused on helicopters and maritime patrol platforms. Infrastructure modernization in border surveillance and energy corridor protection is driving targeted procurement. Government incentives support defense electronics localization, with import duties reduced by 12–18% for avionics components. A regional aerospace company integrated missile warning sensors across 60 rotary aircraft in 2024. Regional behavior shows demand tied to border security and maritime surveillance missions, with more than 44% of helicopter operators prioritizing infrared protection upgrades.

The region accounts for about 6% of global installations, led by the UAE, Saudi Arabia, and South Africa. More than 780 military aircraft operate with infrared countermeasure capability. Demand is driven by border security, oil & gas corridor protection, and high-threat operating environments. Technological modernization includes adoption of long-range missile warning sensors and compact laser turrets, with over 57% of new helicopters delivered with protection suites. A regional defense group equipped 90 transport aircraft with integrated jamming systems in 2025. Regional behavior shows high preference for turnkey integrated systems, with faster adoption in rotorcraft than fixed-wing fleets.

United States – 34% Market Share: Dominance driven by the world’s largest military aviation fleet and continuous fleet-wide survivability upgrade programs.

China – 18% Market Share: Strong position supported by rapid aircraft production capacity and large-scale indigenous avionics manufacturing.

The competitive environment in the Infrared Countermeasures System Market is moderately consolidated yet highly specialized, with approximately 20+ active competitors offering a range of missile warning, DIRCM (Directed Infrared Countermeasure) and laser-based solutions. The top 5 companies—including Northrop Grumman, Raytheon Technologies, BAE Systems, Leonardo S.p.A., and Elbit Systems—collectively account for an estimated ~55–60% combined share of global system deployments across fixed-wing, rotary and unmanned platforms. Competition is defined by strategic initiatives such as multi-platform product launches, integration partnerships with defense OEMs, and expansion of global service networks. In 2024–2025, major players have expanded modular product lines, with lightweight and multi-spectral IRCM systems designed for rapid integration across existing fleets.

Innovation trends include AI-augmented missile threat detection, solid-state and quantum cascade laser (QCL) technology for enhanced jamming precision, and sensor fusion architectures that reduce false alarms while increasing detection distances. Firms are engaging in joint ventures and long-term contracts with defense ministries to embed their technologies deeper into national defense programs, while emerging challengers also focus on miniaturized and energy-efficient countermeasure units for next-generation platforms. Strategic positioning is further influenced by increasing defense budgets, expanded retrofits of aging airframes, and concentrated R&D investment in autonomous threat classification systems.

Leonardo S.p.A.

Elbit Systems Ltd.

Thales Group

L3Harris Technologies

Saab AB

Rafael Advanced Defence Systems

Hensoldt

Aselsan

ITT Corporation

Chemring Group

Thermoteknix Systems

The Infrared Countermeasures System Market is being reshaped by several key technology trajectories that are enhancing performance, integration, and operational capability across defense platforms. Directed Infrared Countermeasures (DIRCM) systems increasingly leverage advanced laser technologies—including quantum cascade lasers (QCLs) and compact fiber lasers—which offer higher energy output, greater precision, and reduced weight, enabling integration on both fixed-wing aircraft and rotary platforms. These advancements improve the ability of systems to disrupt or neutralize infrared-guided threats at extended engagement ranges. Sensor fusion technologies combining infrared missile warning, radar warning, and laser threat data are delivering multi-modal threat profiles that reduce false alarms and improve reaction speed under contested conditions.

AI and machine learning integration is a major trend, where real-time threat classification and predictive modeling accelerate countermeasure deployment and enhance survivability metrics in dynamic threat environments. Miniaturization and modular design innovation also enable retrofit installations on legacy fleets, enhancing platform upgrade flexibility. Beyond airborne applications, emerging systems are being scaled for unmanned aerial vehicles (UAVs) and support vehicles, expanding the market footprint. Multi-spectral detection arrays further enhance situational awareness by broadening the spectrum of infrared signatures monitored. These technological developments are enabling defense organizations to tailor countermeasure suites to platform type, mission profile, and threat spectrum, elevating the strategic value of integrated infrared protection systems.

• In June 2025, Indra announced development of full digital self-protection systems for aircraft and helicopters that scan the full radar spectrum and detect threats faster, marking a leap in European airborne defence capabilities. Source: www.asdnews.com

• In late 2024, Northrop Grumman’s CIRCM system was selected for installation on the UK’s Chinook helicopter fleet, integrating next-generation infrared protection on 14 extended-range platforms. Source: armyrecognition.com

• In December 2024, Elbit Systems secured a $175M contract to supply advanced DIRCM and electronic warfare self-protection suites, including digital radar warning and missile warning systems, for military transport platforms in Europe.

• In February 2024, Leonardo DRS delivered its 1,000th Solaris laser component for the U.S. Army’s Common Infrared Countermeasures system, accelerating protection deployment on 1,500 platforms and introducing broader threat detection sensors.

The Infrared Countermeasures System Market Report offers a broad yet detailed examination of market structure, technological evolution, deployment contexts, and competitive dynamics across global regions. The scope encompasses product categorization—including missile warning systems, Directed Infrared Countermeasures (DIRCM), integrated self-protection suites, and auxiliary components such as sensors and laser turrets—highlighting architectural distinctions and platform applicability. Platform segmentation covers fixed-wing combat and transport aircraft, helicopters, unmanned aerial vehicles (UAVs), and support vehicles, enabling assessments of how infrared countermeasure technologies vary by mission profile and operational environment.

Geographically, the report analyzes regional insights from North America, Europe, Asia-Pacific, South America, and Middle East & Africa, reflecting variations in procurement priorities, defense budgets, and indigenous production capabilities. Application focus includes military aviation, homeland security, and surveillance, while technology trends—such as miniaturization, AI-driven threat detection, multi-spectral sensors, and advanced laser countermeasure innovations—are evaluated for their impact on adoption and performance differentiation. Competitive profiling of major vendors, strategic collaborations, and innovation pipelines provide context for investment decisions, while niche segments like UAV-specific countermeasure packages and export-oriented solutions are also addressed. This comprehensive coverage equips decision-makers with a multifaceted understanding of infrared countermeasure systems’ current state and future potential.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 8,190.0 Million |

| Market Revenue (2033) | USD 11,382.2 Million |

| CAGR (2026–2033) | 4.2% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Northrop Grumman, Raytheon Technologies, BAE Systems, Leonardo S.p.A., Elbit Systems, Thales Group, L3Harris Technologies, Saab AB, Rafael Advanced Defence Systems, Hensoldt, Aselsan, ITT Corporation, Chemring Group, Thermoteknix Systems |

| Customization & Pricing | Available on Request (10% Customization Free) |