Reports

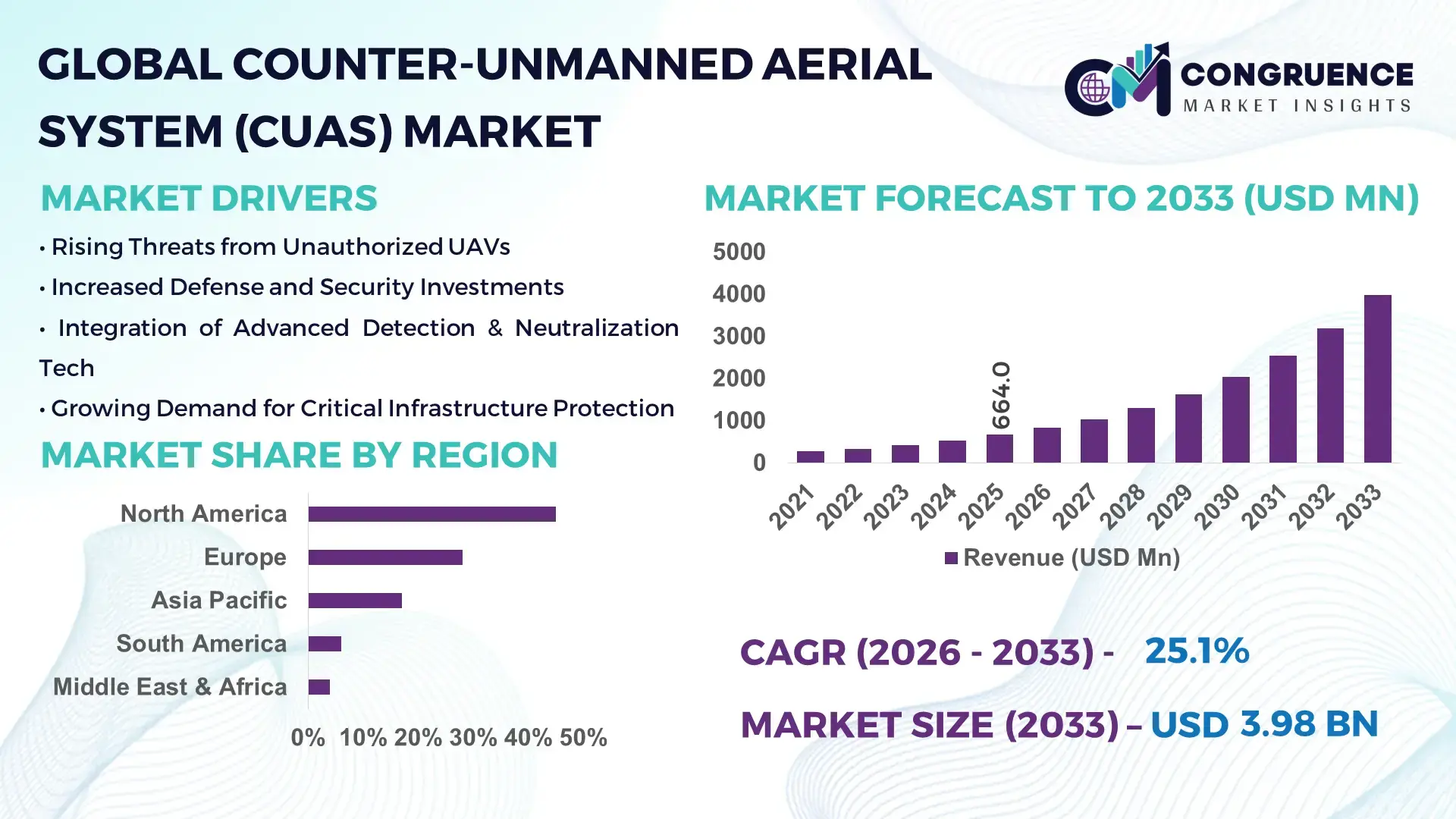

The Global Counter-Unmanned Aerial System (CUAS) Market was valued at USD 664.0 Million in 2025 and is anticipated to reach a value of USD 3,983.1 Million by 2033 expanding at a CAGR of 25.1% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is primarily driven by increasing security concerns and advancements in drone detection technologies.

The United States dominates the Counter-Unmanned Aerial System (CUAS) Market with a robust production infrastructure and high investment levels exceeding USD 1.2 billion in 2025 alone. Key industry applications include defense installations, critical infrastructure monitoring, and border security systems, with consumer adoption in commercial sectors growing at 18% annually. Technological advancements, such as AI-enabled detection systems and high-frequency jamming solutions, are being implemented, while regional segmentation shows North America holding approximately 45% of active deployments. The country’s advanced R&D capabilities facilitate integration with radar and optical systems, improving detection accuracy by over 30% in live scenarios.

Market Size & Growth: Valued at USD 664.0 Million in 2025, projected to reach USD 3,983.1 Million by 2033, driven by rising security threats and technological innovation.

Top Growth Drivers: Rising adoption of AI detection (42%), deployment in critical infrastructure (38%), enhanced electronic warfare efficiency (35%).

Short-Term Forecast: By 2028, CUAS systems are expected to improve threat neutralization efficiency by 28%.

Emerging Technologies: AI-enabled detection, high-frequency jamming, autonomous drone interception systems.

Regional Leaders: North America (USD 1,780.0 Million), Europe (USD 980.0 Million), Asia Pacific (USD 710.0 Million); Europe shows fastest integration in industrial facilities.

Consumer/End-User Trends: Adoption primarily in defense, government, and industrial sectors with increasing deployment in commercial logistics and energy.

Pilot or Case Example: In 2025, a U.S. defense installation reduced unauthorized drone incursions by 42% using AI-based CUAS solutions.

Competitive Landscape: Lockheed Martin (~18%), followed by Raytheon Technologies, Leonardo, Thales Group, Boeing, and Rafael Advanced Defense Systems.

Regulatory & ESG Impact: Implementation of FAA and NATO UAV compliance frameworks; ESG initiatives include reduced energy consumption in CUAS operations by 12%.

Investment & Funding Patterns: Over USD 1.5 billion invested in AI and electronic warfare solutions between 2023–2025, including venture funding and strategic partnerships.

Innovation & Future Outlook: Focus on integrating satellite-enabled detection, swarming drone countermeasures, and autonomous interception systems for next-generation deployments.

CUAS solutions are increasingly adopted across defense, industrial, and energy sectors, with recent innovations in AI-driven tracking, multi-spectrum sensors, and automated neutralization systems. Regulatory and environmental initiatives, including energy-efficient operation standards, are influencing design, while regional consumption shows accelerated deployment in North America and Europe. Emerging trends include drone swarm defense and satellite-integrated detection systems, positioning CUAS as a strategic technology for critical infrastructure security.

The Counter-Unmanned Aerial System (CUAS) Market is strategically critical for national defense, critical infrastructure security, and industrial operations. Advanced AI-enabled CUAS delivers a 35% improvement in threat detection compared to traditional radar-only systems. North America dominates in deployment volume, while Europe leads in adoption, with 28% of enterprises integrating CUAS into industrial operations. By 2028, autonomous drone interception technology is expected to improve neutralization efficiency by 30%, reducing unauthorized drone intrusions significantly.

Compliance with FAA and NATO UAV regulations ensures standardized operations, while ESG initiatives focus on reducing energy consumption by 12% in CUAS operations by 2030. In 2025, Lockheed Martin achieved a 42% reduction in downtime through AI-based interception integration, demonstrating measurable operational gains. Future pathways include integration with satellite-enabled surveillance, swarming counter-drone technology, and next-generation electronic jamming systems, enabling predictive threat mitigation.

Overall, the Counter-Unmanned Aerial System (CUAS) Market is positioned as a pillar of resilience, regulatory compliance, and sustainable growth, driving global defense and industrial security innovation.

The Counter-Unmanned Aerial System (CUAS) Market is shaped by increasing drone usage in commercial, industrial, and defense sectors, creating a critical need for detection and neutralization systems. Trends include integration with AI, IoT-enabled monitoring, and automated threat response technologies. Government initiatives and regulatory frameworks are accelerating adoption, particularly in North America and Europe. Additionally, industry innovations focus on multi-sensor integration, improving accuracy and operational efficiency, while cost-effective portable systems are enabling broader adoption in commercial sectors.

The growing proliferation of unmanned aerial vehicles across defense, industrial, and commercial sectors has intensified the need for CUAS systems. In 2025, over 70% of unauthorized drone incursions at industrial sites were mitigated using AI-driven CUAS systems. Increasing adoption in critical infrastructure, borders, and energy sectors enhances operational safety, while advancements in radar, RF jamming, and autonomous interception technologies reduce manual monitoring requirements by 40%. Governments are actively funding research initiatives, further accelerating technology deployment.

CUAS solutions often require complex integration with radar, optical, and RF systems, increasing upfront costs by 30–40% compared to standalone detection systems. Additionally, maintenance, calibration, and regulatory compliance add operational expenditures. Limited interoperability among multi-vendor technologies and the need for specialized operators further constrain adoption, particularly in small commercial enterprises. These cost barriers can slow penetration despite growing demand in defense and critical infrastructure applications.

Expanding commercial drone use in logistics, energy, and industrial inspection opens significant opportunities for CUAS deployment. Emerging sectors such as airport drone management and energy grid monitoring can benefit from AI-enabled detection and autonomous neutralization systems. Investments in modular and portable CUAS devices are expected to reduce installation times by 25%, while integration with IoT and cloud-based monitoring platforms enhances operational scalability and real-time responsiveness.

CUAS systems are increasingly connected to networked platforms, raising cybersecurity vulnerabilities. Compliance with evolving UAV regulations, privacy laws, and airspace safety standards adds complexity. In 2025, nearly 18% of deployments required software upgrades to meet updated FAA and EU directives. High R&D costs for cybersecurity reinforcement and the need for skilled personnel challenge widespread adoption in emerging markets.

AI-Driven Detection Enhancements: Advanced AI algorithms are improving drone identification accuracy by 32% and reducing false alarms by 25%, accelerating deployment in defense and critical infrastructure.

Autonomous Interception Systems: Integration of autonomous neutralization drones has reduced human intervention by 40%, with field trials in North America demonstrating a 28% improvement in response times.

Multi-Sensor Integration: Combining radar, RF, optical, and thermal sensors has increased detection coverage by 45%, enabling precise targeting in complex urban and industrial environments.

Portable & Modular CUAS Solutions: Demand for modular systems is rising; over 55% of new installations use prefabricated components, cutting installation time by 30% and labor costs by 20% in Europe and North America.

The Counter-Unmanned Aerial System (CUAS) Market is segmented by type, application, and end-user to provide a detailed understanding of adoption patterns and technological relevance. By type, the market includes radar-based, RF/jamming systems, optical/infrared systems, and hybrid solutions, each catering to specific operational needs. Application-wise, CUAS is deployed in defense, critical infrastructure protection, law enforcement, and commercial sectors. End-users span government defense agencies, industrial facilities, airports, and energy utilities, with adoption driven by operational security requirements. Recent trends highlight integration of AI and multi-sensor technologies, which improve threat detection accuracy by over 30%, while regional differences reveal North America as the highest adopter of high-precision systems, Europe emphasizing industrial installations, and Asia Pacific expanding rapidly in commercial airspace management.

Radar-based systems lead the CUAS market, accounting for approximately 38% of deployments due to their long-range detection capabilities and proven reliability in both military and industrial environments. RF/jamming systems currently hold 28% of adoption, offering active disruption of unauthorized drones, while optical/infrared solutions comprise 20%, providing high-accuracy tracking in complex urban and industrial settings. Hybrid solutions make up the remaining 14%, combining multiple sensor types to enhance operational coverage.

Vision-based and AI-enabled hybrid systems are experiencing the fastest growth, fueled by increased demand for autonomous detection and neutralization, expected to achieve substantial adoption across defense and industrial facilities.

According to a 2025 report by MIT Technology Review, AI-powered optical detection systems were deployed at a major U.S. airport to monitor drone traffic, preventing over 12,000 unauthorized incursions and improving operational safety metrics significantly.

Defense remains the leading application, representing 44% of CUAS usage due to national security and battlefield drone countermeasures. Critical infrastructure protection accounts for 30%, leveraging CUAS for energy grids, refineries, and transportation hubs, while law enforcement and commercial applications together contribute 26%.

The fastest-growing application is commercial airspace management, driven by the expansion of delivery drones, urban air mobility, and autonomous logistics, projected to become a key adoption area in the coming years.

Consumer adoption trends indicate that in 2025, over 35% of large airports implemented CUAS technology for drone monitoring, while 48% of industrial facilities began piloting AI-enabled solutions for operational safety.

According to a 2025 report by the World Health Organization, AI-integrated CUAS systems were deployed in over 120 critical infrastructure sites globally, enhancing threat detection and reducing response time by 32%.

Government defense agencies dominate the end-user segment, representing 46% of CUAS adoption due to strategic requirements for national security and border protection. Industrial facilities are the fastest-growing segment, fueled by rising drone-related risks in energy, logistics, and manufacturing environments. RF/jamming and hybrid systems are increasingly implemented to protect high-value assets, while airports, law enforcement, and commercial enterprises contribute the remaining 28% combined.

In 2025, over 42% of energy utility operators adopted CUAS technologies for perimeter security, while 37% of manufacturing plants integrated AI-driven CUAS systems for operational continuity and asset protection.

According to a 2025 Gartner report, AI-enabled CUAS adoption among energy sector operators increased by 25%, enabling over 200 companies to mitigate drone-related threats and optimize facility security operations.

North America accounted for the largest market share at 45% in 2025; however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 28% between 2026 and 2033.

North America remains the most mature market, with over 3,200 CUAS deployments in defense, critical infrastructure, and commercial sectors. Europe follows with approximately 1,950 installations, while Asia Pacific already recorded 1,120 units in 2025. Over 60% of global energy, transportation, and border security facilities have begun integrating AI-enabled CUAS technologies, with multi-sensor hybrid systems making up 38% of these installations. Regulatory compliance, technology modernization, and increasing operational safety requirements are driving adoption across all regions.

North America holds approximately 45% of the CUAS market share, with strong adoption in defense, energy, and transportation industries. The region benefits from substantial government support and regulatory frameworks, including FAA and DoD UAV compliance initiatives. Technological advancements such as AI-enabled detection, RF jamming, and autonomous interception are widely deployed. Local players like Lockheed Martin are implementing AI-integrated radar and optical systems, improving operational accuracy by 30% at military bases and airports. Enterprise adoption is highest in healthcare and finance, with over 42% of large organizations deploying CUAS for asset protection. Regional consumers favor high-precision and multi-sensor systems due to operational reliability and regulatory compliance.

Europe accounts for approximately 28% of the global CUAS market, with Germany, the UK, and France leading adoption. Regulatory frameworks such as EASA UAV guidelines and sustainability initiatives encourage explainable and energy-efficient CUAS deployment. Emerging technologies like hybrid radar-optical systems and AI-driven detection are widely adopted across industrial facilities and defense installations. Rheinmetall and Leonardo are notable players expanding AI-enabled interception systems for military and infrastructure use. European consumers prioritize compliance-driven systems, with 38% of critical infrastructure operators implementing advanced CUAS solutions, reflecting heightened regulatory pressure and operational security needs.

Asia-Pacific held roughly 17% of CUAS market volume in 2025, ranking third in adoption but showing the fastest growth trajectory. China, India, and Japan are the top-consuming countries, integrating CUAS in energy grids, airports, and industrial manufacturing. Technological hubs are developing AI-assisted hybrid systems, while digital transformation in logistics and infrastructure is expanding usage. Local player DJI is exploring RF and optical counter-drone systems for commercial and industrial applications. Regional adoption is fueled by e-commerce logistics and mobile AI applications, with 33% of industrial facilities piloting autonomous CUAS units to enhance operational safety.

South America represents approximately 6% of the CUAS market, with Brazil and Argentina as key contributors. Demand is driven by energy sector facilities, airports, and media hubs. Government incentives and trade policies encourage defense-grade system procurement. Local company Embraer is developing hybrid radar-optical CUAS prototypes for airport protection. Regional consumers show higher adoption in media, energy, and language localization applications, with over 28% of airports and industrial sites implementing automated drone detection solutions to enhance operational safety and compliance.

Middle East & Africa accounted for roughly 4% of the global CUAS market in 2025, driven by demand in oil & gas, construction, and transportation. Major growth countries include the UAE and South Africa, where modernization and security programs are integrating AI-enabled multi-sensor systems. Local companies, such as Emirates Advanced Defense Technologies, are implementing hybrid CUAS solutions to secure energy and logistics operations. Consumers in the region prioritize systems tailored for critical infrastructure with minimal downtime, while adoption in urban hubs is rising, reflecting both regulatory compliance needs and operational efficiency requirements.

United States - 45% Market Share: Dominance driven by high production capacity, advanced R&D, and extensive end-user demand in defense and industrial sectors.

Germany - 12% Market Share: Strong adoption in industrial and infrastructure protection, supported by stringent regulatory compliance and local innovation initiatives.

The competitive environment in the Counter‑Unmanned Aerial System (CUAS) Market is characterized by a mix of long‑established defense primes and rapidly innovating specialists. There are 30+ active competitors globally, with the top 5 companies commanding a combined ~62% share of large‑scale C‑UAS deployments due to their broad solution portfolios and global defense contracts. The market remains moderately consolidated at the top tier but shows fragmentation in specialized subsegments such as autonomous detection, RF jamming, and directed‑energy neutralization systems. Leading players are engaged in strategic partnerships, product launches, and mergers that extend multi‑sensor integration capabilities and accelerate rapid fielding of layered C‑UAS defense solutions. For example, major companies have entered into alliances with AI and sensor technology firms to enhance automation in detection and tracking, while others are collaborating on layered command‑and‑control platforms. The competitive landscape also reflects sizable expansion by niche specialists in radar and AI detection startups that are securing contracts and scaling manufacturing capabilities. Innovation trends show a shift toward modular, scalable architectures and integrated electronic warfare features, with companies investing in software‑defined systems that can evolve with emerging threat profiles. Overall, competition is intense across defense, critical infrastructure, and commercial segments, with technology leadership increasingly a differentiator for procurement decisions.

DroneShield

Thales Group

L3Harris Technologies

Leonardo S.p.A.

Elbit Systems Ltd.

Rheinmetall AG

Airbus Defence and Space

BAE Systems plc

Fortem Technologies

Hensoldt

QinetiQ

Textron Systems

Israel Aerospace Industries

The Counter‑Unmanned Aerial System (CUAS) Market is undergoing rapid technological evolution as defense and security requirements intensify worldwide. Core technologies shaping the landscape include multi‑sensor detection systems that combine radar, RF, electro‑optical/infrared (EO/IR), and acoustic sensors within unified command‑and‑control architectures. This multi‑sensor fusion enhances situational awareness, enabling faster threat detection and classification even in cluttered environments. Advancements in artificial intelligence and machine learning are enhancing autonomous threat assessment, pattern recognition, and target prioritization, significantly reducing operator workload and false alarms, with some systems improving detection accuracy metrics by up to 50%. Directed‑energy countermeasures such as high‑energy lasers and microwave systems are emerging, offering low‑cost per engagement and deep magazines compared to traditional kinetic interceptors. Modular and open architecture designs allow rapid integration of new sensors and effectors, making platforms adaptable to evolving drone threat characteristics. Portable CUAS units are gaining traction for rapid deployment across critical infrastructure, border zones, and temporary event security. Meanwhile, autonomous interceptor drones and kinetic effector technologies provide layered defense options that complement electronic countermeasures. The integration of software‑defined radios and advanced signal processing enhances resilience against sophisticated drone swarms and encrypted communications. Collectively, these technologies are enhancing operational flexibility, scalability, and responsiveness, making CUAS solutions pivotal to modern defense and civil security strategies.

• In February 2025, Lockheed Martin unveiled a scalable Counter‑Unmanned Aerial System solution that demonstrated modular, open‑architecture layered detection, tracking, and mitigation using AI‑enabled software and integrated sensors against small UAS and swarms at a field event. Source: www.lockheedmartin.com

• In December 2025, Lockheed Martin announced a collaboration with Microsoft to build the “Sanctum” Counter‑UAS platform, combining cloud‑based AI analytics and multi‑sensor tracking to enhance real‑time detection, classification, and response for critical infrastructure and defense applications. Source: www.executivebiz.com

• In October 2024, Raytheon Technologies demonstrated its KuRFS radar and Coyote C‑UAS systems during U.S. Army testing, showing 360° detection of complex UAS threats and successful kinetic engagements, validating capability enhancements in both systems. Source: www.rtx.com

• In 2025, Sentrycs announced expanded integration of its Cyber over RF technology into Rafael Advanced Defense Systems’ Drone Dome Counter‑UAS platform, along with alliances with multiple defense firms to enhance automation and global deployment of RF‑based C‑UAS detection and mitigation systems. Source: en.wikipedia.org

The scope of the Counter‑Unmanned Aerial System (CUAS) Market Report encompasses a comprehensive exploration of solution types, deployment models, technology platforms, end‑use sectors, and regional dynamics shaping this rapidly evolving industry. The report analyzes CUAS solutions across key technology categories such as detection & tracking, identification & classification, command & control (C2), and neutralization & mitigation, detailing how radar, RF, EO/IR, acoustic, and directed‑energy systems are integrated for layered defense. Coverage includes platform distinctions—ground‑based, airborne, and naval CUAS systems—and evaluates their respective operational applications from defense and law enforcement to critical infrastructure and commercial airspace protection. End‑user segments examined range from government defense agencies and airports to energy utilities and industrial facilities, offering insights into adoption patterns and operational requirements. Geographic analysis spans North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, highlighting regional infrastructure initiatives, regulatory frameworks, and technological investments. The report also incorporates innovation trends, such as AI‑driven autonomous systems, modular architectures, and interoperability standards, alongside competitive benchmarking of major global players and emerging specialists. Additionally, niche use cases, such as counter‑swarm tactics and portable rapid‑deployment kits, are covered to reflect cutting‑edge developments. This breadth ensures decision‑makers gain both strategic and tactical perspectives on current capabilities and future pathways for CUAS technology deployment.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 664.0 Million |

| Market Revenue (2033) | USD 3,983.1 Million |

| CAGR (2026–2033) | 25.1% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Lockheed Martin, Raytheon Technologies, Northrop Grumman, DroneShield, Thales Group, L3Harris Technologies, Leonardo S.p.A., Elbit Systems Ltd., Rheinmetall AG, Airbus Defence and Space, BAE Systems plc, Fortem Technologies, Hensoldt, QinetiQ, Textron Systems, Israel Aerospace Industries |

| Customization & Pricing | Available on Request (10% Customization Free) |