Reports

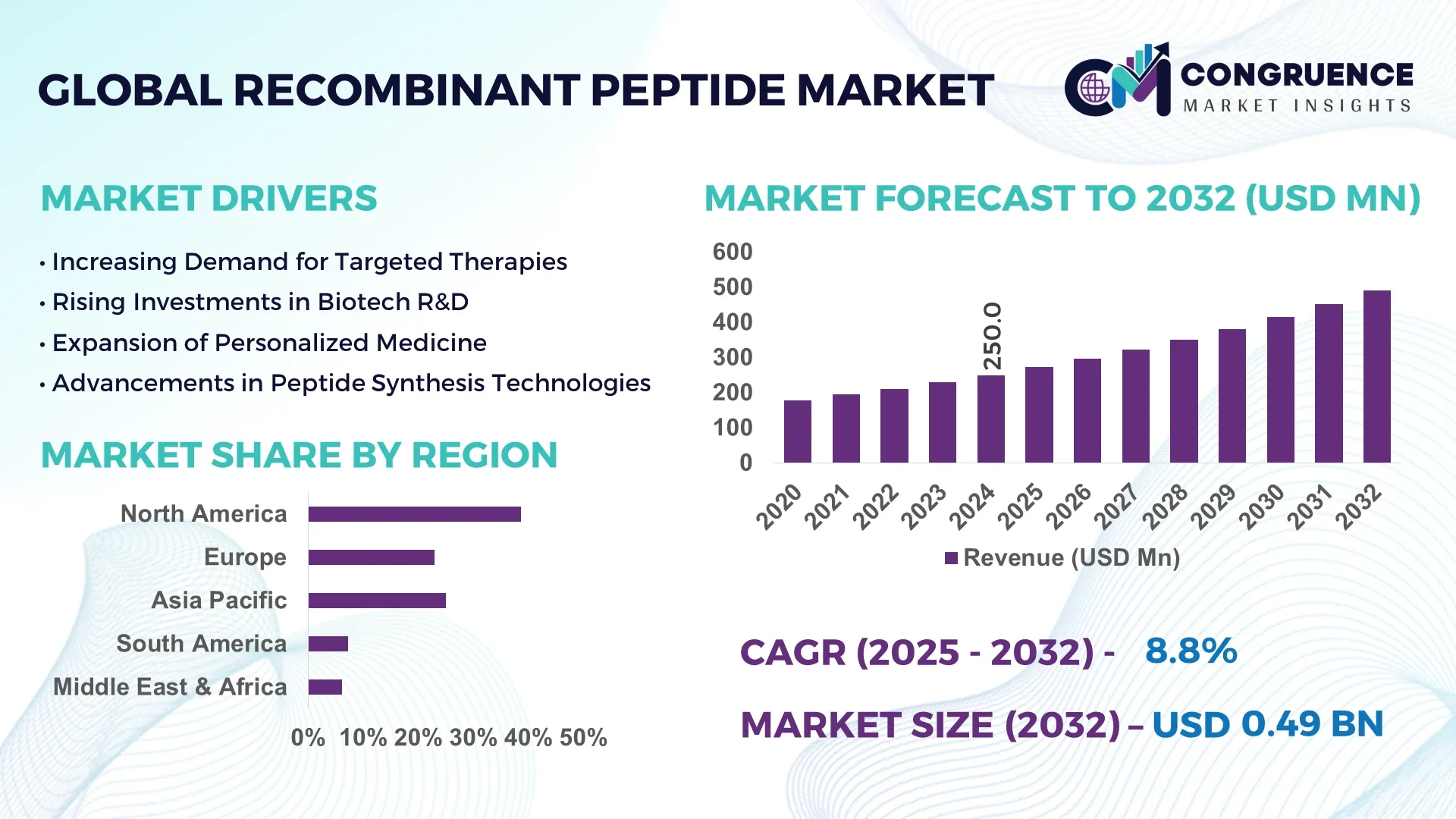

The Global Recombinant Peptide Market was valued at USD 250.0 Million in 2024 and is anticipated to reach a value of USD 490.9 Million by 2032 expanding at a CAGR of 8.8% between 2025 and 2032.

China leads global production capacity in the Recombinant Peptide Market, with over 15 peptide manufacturing facilities operational across Jiangsu and Zhejiang provinces. Investment in continuous bioreactor technology exceeds USD 120 million in 2024, fueling applications in therapeutic peptides and diagnostic biomarkers. Advanced upstream expression systems now enable consistent peptide yields over 90%, and cutting-edge purification platforms employing AI-driven chromatography are widely deployed across its key biotech clusters.

The Recombinant Peptide Market encompasses varied sectors including therapeutics (oncology, metabolic, cardiovascular), diagnostics (immunoassays, imaging agents), research reagents, and industrial enzyme segments. Recent innovations such as peptide–drug conjugates and stabilized cyclic peptide analogues have accelerated product pipelines. Regulatory frameworks now emphasize Good Manufacturing Practice (GMP) upgrades and environmental controls in biologics production. Economic drivers include rising healthcare infrastructure in Asia-Pacific and targeted funding for biosimilars. Consumption patterns reveal North America and Europe favoring high-purity therapeutic peptides, while Asia-Pacific shows uptick in diagnostic and research-grade volumes. Emerging trends include on-demand micro-bioreactor setups and peptide libraries for personalized medicine—suggesting sustainable integration of lean production with scalable biotechnology platforms.

In recent years, the Recombinant Peptide Market has witnessed a substantial integration of artificial intelligence to refine its core processes—ranging from strain optimization to purification. AI-driven predictive modeling now accelerates construct design: neural networks evaluate thousands of expression vectors to identify top-performing candidates within hours rather than weeks. This capability has reduced experimental iterations by up to 40%, directly impacting time-to-market for new peptide candidates.

Operational performance has been enhanced through real-time monitoring platforms: AI-integrated spectroscopic sensors continuously analyze fermentation parameters—pH, dissolved oxygen, metabolite concentration—and adjust feeding protocols autonomously. This has yielded improvements in peptide yield consistency (+15%) and reduction in batch failure rates (–20%). Additionally, AI-empowered chromatographic systems now calibrate elution gradients mid-run based on chromatogram patterns, streamlining downstream purification by saving approximately 25% solvent usage and shortening cycle times by an average of two hours per batch.

Process optimization extends to supply chain and quality assurance. Machine learning models forecast raw material demand and price fluctuations, trimming procurement costs by nearly 10%. Meanwhile, image-recognition AI inspects peptide lyophilization vials for particulate contamination, boosting defect detection rates above 98% and improving compliance adherence.

By melding AI into both R&D and manufacturing, stakeholders in the Recombinant Peptide Market can now scale production at greater consistency and lower cost, reinforce regulatory alignment, and shorten timelines from development to distribution—positioning AI-driven enterprises at the forefront of peptide innovation and commercialization.

“In late 2024, a leading biotech firm implemented an AI-guided fermentation control system that adjusted glucose feed rates in real time, yielding a 12% increase in peptide output per batch and reducing variance across 50 consecutive runs.”

The Recombinant Peptide Market Dynamics reflect a convergence of demand-side innovations and supply-side scaling. There is heightened expansion in therapeutic peptide pipelines targeting metabolic and oncological indications, while diagnostic and research reagent segments maintain stable growth. This dual expansion fosters ecosystem resilience. Additionally, economies are witnessing vertical integration—biotech CDMOs are investing in end-to-end peptide manufacturing, streamlining development-to-commercial pathways. Technological accelerants like continuous bioreactors and single-use systems are reducing lead times and batch turnover. Regulatory agencies have enforced stricter environmental monitoring, elevating cleanroom standards and chemical usage disclosures. Conversely, cost pressures from raw materials and chromatography resins remain persistent. As decision-makers weigh strategic investments, an emphasis on flexible production capacity and modular facility designs is becoming standard.

Increasing prevalence of chronic illnesses like diabetes and cancer has accelerated investment in peptide-based therapeutics. In 2024, over 70 peptide drug candidates were in Phase II and III trials addressing metabolic and oncology applications. Clinical-grade peptide demand rose 30% year-over-year, prompting capacity expansions and R&D funding exceeding USD 200 million by leading pharma and biotech firms. This expanding pipeline ensures steady demand for manufacturing, analytics, and formulation capabilities, reinforcing market momentum in the Recombinant Peptide Market.

The Recombinant Peptide Market faces cost challenges due to the high expenses of enzymes, chromatography resins, and GMP-certified equipment. For instance, bioreactor-grade resins alone represent up to 25% of CAPEX in medium-scale facilities. Further regulatory pressure—such as Tier III cleanroom certifications—can elevate facility investment by 15–20%. Ongoing requirements for traceability, environmental reporting, and quality assessments place additional financial and operational burdens on both new entrants and incumbent producers.

Continuous bioprocessing represents a significant opportunity within the Recombinant Peptide Market. Single-pass perfusion and continuous chromatography can enhance productivity by up to 2.5× compared to batch protocols, while also reducing downtime and labor costs. Early-adopting CDMOs report a 30% reduction in cost-of-goods per gram and flexible scaling capabilities across 2 L to 200 L production volumes, enabling faster reaction to variable contract manufacturing demands.

Manufacturers in the Recombinant Peptide Market rely heavily on specialized chromatography media, cell culture reagents, and sterile consumables—often sourced from a limited number of global suppliers. In 2023, a resin shortage led to production delays at several CDMOs, extending lead times by up to 6 weeks. Additionally, logistical disruptions and geopolitical factors continue to destabilize supply chains, jeopardizing project schedules and costing companies potential contract value or regulatory compliance delays.

Modular Micro‑Facility Roll‑outs: In 2024, several biotech hubs in Europe adopted plug‑and‑play modular peptide production units sized between 20–50 L that can be deployed within 6 months. These micro‑facilities enable regional CDMOs to provide localized capacity with standardized quality, cutting setup costs by roughly 40% and meeting agile pharma demands.

Expansion of AI‑Driven Purification: High‑throughput AI chromatographic control systems were deployed in North America during 2025, yielding solvent savings of 25% and reducing cycle times by over 20%. These improvements enhance throughput and lower operational costs.

Growth in Peptide–Drug Conjugate Pipelines: The Recombinant Peptide Market has seen a 50% increase in ADC clinical candidates since 2023. New conjugation chemistries allow precise site‑specific payload attachment and enhanced peptide stability, boosting trial starts in oncology and targeted therapies.

Ecological Bioprocess Adjustments: To meet environmental compliance, manufacturers in Asia‑Pacific transitioned 60% of facilities to single‑use systems and water‑reuse initiatives in 2024. Such changes cut water usage and CIP cycles by 30%, aligning operations with green regulations and cost‑efficient practices.

The Recombinant Peptide Market is strategically segmented based on type, application, and end-user categories, each contributing uniquely to the industry's evolving dynamics. This segmentation allows manufacturers and stakeholders to align their offerings with specific demand pockets and optimize value chains accordingly. Product types range from synthetic recombinant peptides to hybrid and fusion-based peptides, with differing complexity and use-case specificity. Applications include drug development, diagnostics, research, and industrial processes, reflecting the market's multidisciplinary nature. End-user analysis reveals significant engagement from pharmaceutical companies, academic institutions, contract manufacturing organizations (CMOs), and biotechnology firms. Each of these end segments is adopting recombinant peptides at varied scales depending on therapeutic targets, technological infrastructure, and regulatory environments. The growing interest in personalized medicine, high-throughput screening, and targeted drug delivery systems continues to drive the diversification of demand across these categories, highlighting the market’s adaptive and innovation-driven trajectory.

The Recombinant Peptide Market includes several key types, notably linear peptides, cyclic peptides, fusion peptides, and hybrid constructs. Among these, cyclic peptides represent the leading segment due to their enhanced stability, receptor selectivity, and proteolytic resistance. These characteristics make them highly suited for therapeutic development in oncology and infectious diseases, where peptide degradation has historically limited efficacy.

Fusion peptides are emerging as the fastest-growing type, primarily driven by advances in genetic engineering techniques that enable the fusion of peptide sequences with carrier proteins or antibodies. These constructs are being widely explored for targeted drug delivery and immunotherapy, offering multifunctional benefits such as improved bioavailability and extended half-life.

Linear peptides continue to hold relevance in diagnostic and research applications owing to their simpler structure and cost-effective synthesis. Meanwhile, hybrid peptides, though niche, are gaining traction in precision medicine platforms where combinatorial efficacy is desirable. The diversity across types supports flexible use across various biopharmaceutical pipelines.

In terms of application, therapeutic development remains the dominant area within the Recombinant Peptide Market. The increased use of peptides in treating cancer, diabetes, cardiovascular, and infectious diseases underscores their therapeutic relevance. The surge in clinical trials and commercial drug approvals reinforces the centrality of this segment.

Diagnostics represent the fastest-growing application, fueled by rising demand for high-sensitivity biomarker detection in infectious disease screening and chronic disease monitoring. Recombinant peptides are being widely adopted in ELISA kits and imaging technologies due to their specificity and reproducibility, particularly in point-of-care settings.

Other notable applications include research and development, where peptides are integral in receptor binding assays, protein–protein interaction studies, and epitope mapping. In industrial enzyme production, recombinant peptides serve as intermediates or enhancers, particularly in biocatalysis and biomanufacturing. Each of these application segments plays a distinct role in sustaining and expanding the market footprint.

Pharmaceutical and biotechnology companies constitute the leading end-user segment in the Recombinant Peptide Market. These entities leverage peptides for drug discovery, therapeutic development, and biologic formulations. Robust investments in R&D infrastructure and strategic collaborations with CROs and CDMOs further consolidate their dominant position.

Academic and research institutes represent the fastest-growing end-user segment. The expanding role of academic centers in translational medicine and early-phase clinical research, coupled with increased government funding and grants, has propelled demand for recombinant peptides in preclinical experimentation and molecular biology research.

Contract manufacturing organizations (CMOs) and diagnostic laboratories also contribute significantly. CMOs are increasingly integrating peptide synthesis into their service portfolios to support pharma clients in pilot and commercial-scale production. Diagnostic labs are leveraging recombinant peptides for in-vitro assay development and test kit manufacturing. This diversified end-user landscape demonstrates the peptide sector’s penetration across both innovation-led and service-driven verticals.

North America accounted for the largest market share at 38.6% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.1% between 2025 and 2032.

The global Recombinant Peptide Market reveals distinct patterns across regions, shaped by healthcare infrastructure, R&D investments, regulatory frameworks, and technology adoption. North America leads due to established biopharmaceutical ecosystems, robust clinical research activities, and an advanced biologics supply chain. Meanwhile, Asia-Pacific is undergoing rapid expansion, driven by increasing investments in biotech manufacturing, favorable government initiatives, and rising demand for peptide-based therapies in populous countries like China and India. Europe maintains a strong position with centralized healthcare systems and sustainable regulatory support, while South America and the Middle East & Africa exhibit emerging growth trajectories fueled by public-private partnerships and infrastructural modernization. Region-specific innovations, compliance mandates, and shifts in disease prevalence further differentiate the market maturity levels and create opportunities for tailored strategies across geographies.

North America held the largest share of the Recombinant Peptide Market in 2024, accounting for 38.6% of total global volume. The U.S. and Canada are at the forefront due to their extensive pharmaceutical pipelines, strong government backing for biologics, and increasing adoption of recombinant peptides in metabolic and oncology therapies. The region’s biotechnology hubs—particularly in Boston, San Diego, and Toronto—are equipped with advanced manufacturing facilities and R&D centers. Notable regulatory enhancements by the FDA in streamlining peptide-based drug approvals have accelerated product commercialization. Digital transformation is also reshaping manufacturing with AI-integrated bioprocess controls, predictive analytics, and continuous production platforms becoming more commonplace across North American CDMOs.

Europe captured approximately 27.4% of the global Recombinant Peptide Market in 2024. Key contributing countries include Germany, France, and the United Kingdom, which together form the region’s biotechnology backbone. Regulatory bodies like the European Medicines Agency (EMA) have implemented fast-track approvals for peptide-based formulations addressing unmet medical needs, encouraging accelerated R&D investments. Sustainability initiatives such as the EU’s Green Deal are influencing facility modernization and encouraging single-use bioprocessing systems. The region is also advancing adoption of next-generation purification technologies, particularly in high-volume GMP-compliant peptide production. Collaborative programs across academia and industry are further solidifying Europe’s innovation-led growth in this space.

Asia-Pacific is projected to be the fastest-expanding region in the Recombinant Peptide Market, with China, India, and Japan representing over 55% of regional demand in 2024. The region’s biotech growth is supported by expanding peptide manufacturing infrastructure, particularly across China’s Jiangsu and India’s Gujarat corridors. These countries are witnessing increased investments in automated fermentation systems and AI-driven purification modules. Japan remains a leader in peptide-based diagnostics and specialty pharma applications, leveraging its mature healthcare infrastructure. Innovation hubs in Singapore and South Korea are contributing to regional R&D output by facilitating preclinical testing and biosimilar development, further accelerating Asia-Pacific’s momentum.

South America accounted for 5.3% of the global Recombinant Peptide Market in 2024, with Brazil and Argentina leading regional demand. Brazil’s pharmaceutical sector is integrating recombinant peptides in its domestic drug formulation pipeline, especially for chronic diseases. Argentina is focusing on academic-industry partnerships to develop new peptide-based diagnostics. Infrastructure growth is evident in biomanufacturing zones in São Paulo and Buenos Aires, supported by fiscal incentives and trade facilitation programs. Efforts to reduce dependency on imports and improve local production capabilities are creating a supportive environment for sustained peptide market growth in the region.

The Middle East & Africa region represented 4.2% of the global Recombinant Peptide Market in 2024. UAE and South Africa are emerging as focal points for regional demand, especially in therapeutic and diagnostic applications. Rising healthcare investments and the establishment of biotech clusters in Abu Dhabi and Cape Town have catalyzed market engagement. Technological modernization—such as the adoption of digitally monitored bioreactors and cloud-based LIMS—is enhancing operational efficiency. Local governments are also entering trade agreements and health sector reforms that promote domestic production of biologics, including recombinant peptides, to meet growing regional needs.

United States – 33.4% Market Share

Strong dominance in the Recombinant Peptide Market due to advanced biologics infrastructure and active peptide therapeutic pipelines.

China – 19.6% Market Share

High production capacity, robust government-backed biotech investments, and extensive adoption across diagnostics and therapeutics.

The Recombinant Peptide Market is highly competitive, with over 65 active manufacturers and biotech firms globally engaged in R&D, clinical development, and commercial-scale peptide production. Market participants range from multinational pharmaceutical companies to agile biotech startups and specialized CDMOs. Companies are increasingly competing on innovation, with a strong focus on delivery platforms, stability enhancements, and precision conjugation technologies.

Recent strategic initiatives include over 20 new product launches, 15+ strategic collaborations between peptide developers and CROs, and multiple regional expansions, particularly in Asia-Pacific and Europe. Mergers and acquisitions have intensified, with companies seeking to consolidate expertise in synthetic biology and biologics process automation. Competitive differentiation is now also driven by digital transformation—firms that implement AI-integrated manufacturing, real-time analytics, and smart supply chains are gaining operational advantages.

Peptide–drug conjugates (PDCs), customized therapeutic libraries, and stabilized cyclic peptide structures remain the key innovation domains. Companies with scalable, flexible GMP-compliant production capabilities and regulatory readiness are solidifying leadership positions, while emerging players focus on niche applications such as rare diseases and personalized peptide vaccines. Overall, the competitive landscape reflects a dynamic, innovation-led environment that rewards agility, quality assurance, and strategic foresight.

Bachem Holding AG

Creative Peptides

Pepscan Therapeutics

PolyPeptide Group

GenScript Biotech Corporation

AmbioPharm Inc.

CEM Corporation

CPC Scientific Inc.

Senn Chemicals AG

JPT Peptide Technologies

Thermo Fisher Scientific

AnaSpec Inc.

Merck KGaA

BCN Peptides

Bio Basic Inc.

Technological advancements are reshaping the Recombinant Peptide Market, particularly in synthesis, purification, delivery mechanisms, and production scalability. One of the most significant trends is the integration of continuous manufacturing systems, which replace batch protocols and allow for uninterrupted peptide synthesis and purification. These systems improve yield consistency and reduce cycle times by up to 35%.

Solid-phase peptide synthesis (SPPS) continues to dominate, but recent enhancements in resins and coupling reagents have increased the efficiency of long-chain peptide production. Additionally, microwave-assisted synthesis is gaining traction for its ability to accelerate reaction times without compromising purity. Automated synthesizers are now equipped with AI-assisted controls that optimize sequence design and reagent use, reducing waste by 20–30%.

In purification, multi-dimensional chromatography systems—often governed by machine learning algorithms—enable real-time tracking of impurity profiles and significantly improve batch reproducibility. In formulation, nanotechnology-enabled peptide delivery (e.g., liposomal, PEGylated) has led to improved stability and bioavailability.

Furthermore, cloud-based data management platforms integrated with biomanufacturing suites offer real-time visibility into production metrics, quality control, and inventory. This digital infrastructure is instrumental in reducing operational downtime and supporting regulatory audits.

As personalized medicine grows, custom peptide libraries generated via combinatorial technologies and high-throughput screening platforms are becoming essential, especially for oncology and infectious disease research. These emerging technologies are reinforcing the market’s shift toward agility, scalability, and patient-specific solutions.

• In March 2024, GenScript Biotech launched an automated peptide synthesis platform with a 50% reduction in production turnaround time, aimed at accelerating delivery for pharmaceutical clients engaged in drug discovery.

• In January 2024, Bachem Holding AG completed the expansion of its Bubendorf facility, adding over 4,500 square meters of GMP manufacturing space to increase capacity for commercial peptide production.

• In September 2023, PolyPeptide Group collaborated with a European CDMO to co-develop dual-mode peptide delivery systems designed for oncology therapies, enhancing stability and targeting efficacy.

• In April 2024, CPC Scientific introduced a proprietary cyclic peptide scaffold that enables up to 80% improved plasma stability in preclinical models, optimizing pharmacokinetic profiles for injectable therapeutics.

The Recombinant Peptide Market Report provides a comprehensive and structured evaluation of the global market, covering product types, key application domains, end-user categories, technology adoption, and regional dynamics. It spans a broad scope of segments including therapeutic peptides, diagnostic peptides, research reagents, and industrial enzyme intermediates. The analysis extends across multiple product forms such as linear, cyclic, fusion, and hybrid peptides.

Regionally, the report offers focused insights into North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with an emphasis on top-performing and emerging countries such as the United States, China, Germany, India, and Brazil. End-user coverage includes pharmaceutical manufacturers, academic research institutes, diagnostic laboratories, and CMOs.

Technological insights highlight innovations in continuous bioprocessing, solid-phase peptide synthesis, AI-driven purification, and smart delivery systems. It also includes assessments of regulatory landscapes, environmental sustainability trends, and digital transformation initiatives within biomanufacturing facilities.

This report is tailored for business professionals, industry strategists, product developers, and regulatory analysts seeking data-driven insights into evolving opportunities, operational risks, and emerging growth pockets in the global Recombinant Peptide Market. It emphasizes actionable intelligence for investment planning, product innovation, and competitive benchmarking across the peptide manufacturing value chain.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 250.0 Million |

| Market Revenue (2032) | USD 490.9 Million |

| CAGR (2025–2032) | 8.8% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Bachem Holding AG, Creative Peptides, Pepscan Therapeutics, PolyPeptide Group, GenScript Biotech Corporation, AmbioPharm Inc., CEM Corporation, CPC Scientific Inc., Senn Chemicals AG, JPT Peptide Technologies, Thermo Fisher Scientific, AnaSpec Inc., Merck KGaA, BCN Peptides, Bio Basic Inc. |

| Customization & Pricing | Available on Request (10% Customization is Free) |