Reports

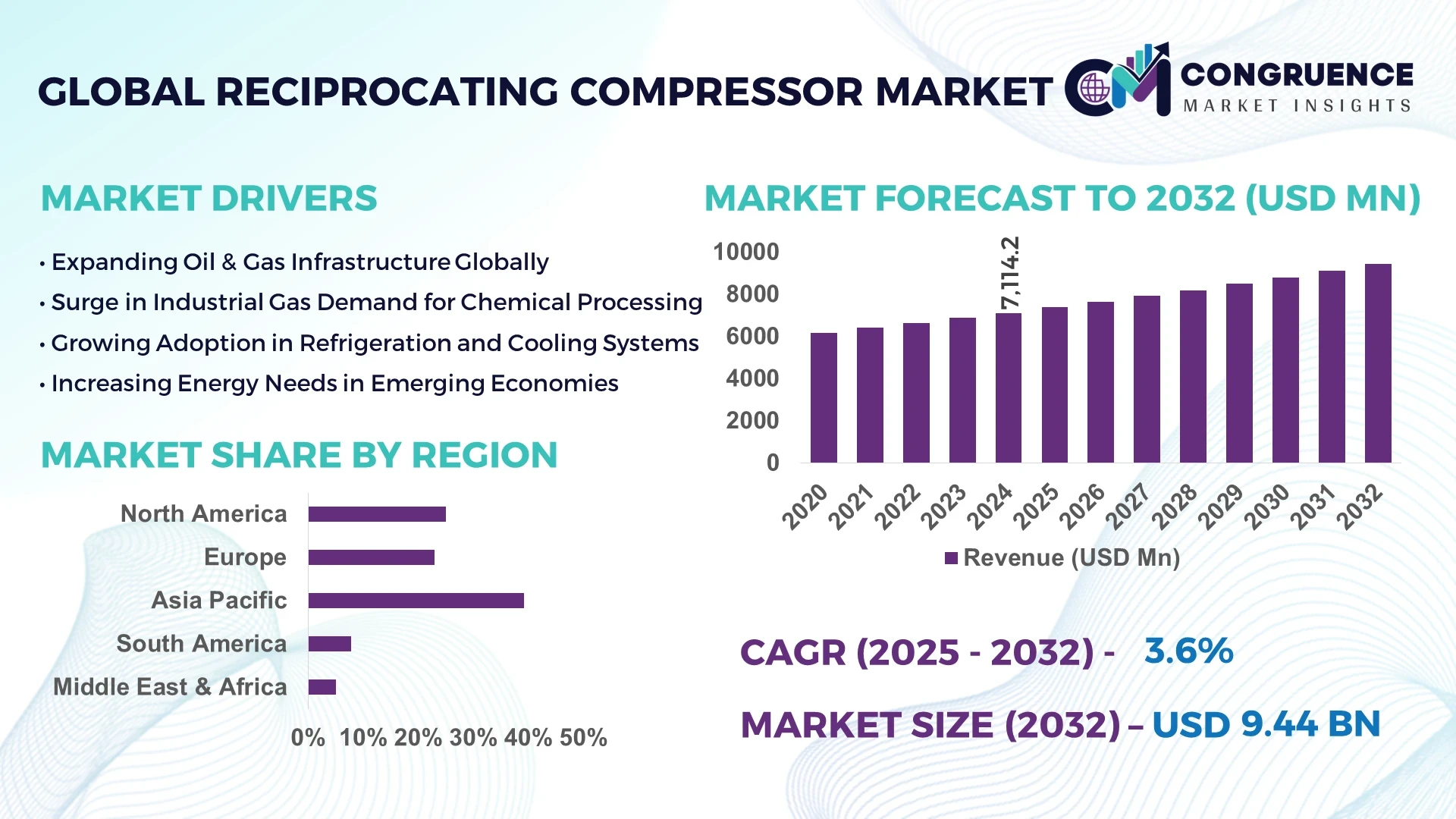

The Global Reciprocating Compressor Market was valued at USD 7,114.21 Million in 2024 and is anticipated to reach a value of USD 9,440.71 Million by 2032 expanding at a CAGR of 3.6% between 2025 and 2032.

The United States maintains a leading position in the Reciprocating Compressor Market, with its high production capacity driven by sustained investments in energy, oil and gas, and advanced petrochemical processing facilities using reciprocating compressors for critical applications. The country also showcases consistent technological advancements through digital monitoring solutions and low-emission compressor models tailored for industrial reliability.

The Reciprocating Compressor Market is witnessing consistent demand across industries including oil and gas, power generation, and manufacturing, where these compressors serve in high-pressure gas delivery, enhanced oil recovery, and pipeline transportation. The market’s structure benefits from a rising preference for modular, energy-efficient reciprocating compressor systems that lower operational costs and improve performance across onshore and offshore installations. Environmental regulations encouraging low-emission and leak-free compressors are pushing manufacturers to adopt upgraded sealing technologies and condition monitoring tools, enhancing predictive maintenance in heavy-duty compressor operations. The market is also supported by regional growth in Asia-Pacific, where expanding energy consumption and refining capacity drive demand for reciprocating compressors in industrial and utility sectors. Emerging trends, including the integration of AI diagnostics and IoT-enabled real-time analytics within reciprocating compressors, are strengthening predictive maintenance capabilities while improving system reliability, reducing downtime, and enabling data-driven operational control for end-users.

Artificial Intelligence is transforming the Reciprocating Compressor Market by enabling smart operational controls and real-time condition monitoring that increase efficiency while reducing unscheduled downtimes in critical industrial applications. AI-powered predictive maintenance systems are now embedded within reciprocating compressors to track vibration patterns, valve conditions, and cylinder performance parameters with precise sensor data analytics, allowing operators to detect abnormalities before failures occur. This proactive maintenance reduces operational disruptions while extending the lifecycle of reciprocating compressors used in sectors such as oil and gas, petrochemicals, and industrial manufacturing. Additionally, AI is enhancing process optimization within the Reciprocating Compressor Market by automatically adjusting compression ratios and energy usage based on workload demands, thereby minimizing energy consumption in high-capacity operations. AI-integrated reciprocating compressors now enable seamless remote monitoring capabilities, providing plant managers with actionable insights and enabling them to plan maintenance schedules without impacting production cycles. In the Reciprocating Compressor Market, AI-based adaptive control algorithms have significantly improved gas handling processes, ensuring optimal compression under variable operational conditions in refineries and natural gas facilities. This technological shift supports sustainability efforts in the market, as AI tools contribute to lower emissions and compliance with environmental standards by monitoring and controlling seal leakages and pressure variations in real time. As industries prioritize efficiency, safety, and sustainability, the adoption of AI across the Reciprocating Compressor Market is expected to accelerate, aligning with the growing demand for advanced, low-maintenance, and energy-efficient compressors for both onshore and offshore industrial operations globally.

“In March 2025, a leading industrial compressor manufacturer integrated an AI-powered predictive analytics system within its reciprocating compressor fleet for a major Middle Eastern gas processing facility, resulting in a 15% reduction in maintenance-related downtime and a 10% improvement in operational efficiency across high-capacity gas compression operations.”

The Reciprocating Compressor Market is shaped by the rising industrial focus on reliability, operational efficiency, and environmental compliance across global applications, including oil and gas, petrochemicals, and industrial gases. Industrial expansions in Asia-Pacific and the Middle East are fueling equipment upgrades and new installations, while advanced compressor control systems and digitized monitoring are enhancing performance across critical infrastructure. Increasing demand for natural gas processing and the development of gas pipeline infrastructure continue to drive the use of reciprocating compressors for high-pressure delivery and storage. Industry players are investing in energy-efficient, low-emission compressors equipped with condition monitoring systems to comply with tightening emission regulations and enhance lifecycle performance. Furthermore, industrial decarbonization goals are aligning with technological innovations in reciprocating compressors that enable low-leakage operations, lower energy consumption, and predictive maintenance, supporting long-term operational cost reductions in the Reciprocating Compressor Market.

The expansion of natural gas pipeline and processing infrastructure is a major driver for the Reciprocating Compressor Market, with countries in Asia-Pacific and the Middle East investing in high-capacity gas handling systems to meet growing domestic energy needs. Reciprocating compressors are essential for ensuring consistent gas flow in pipeline transmission and underground gas storage systems under variable demand conditions. Industrial users prefer reciprocating compressors for their ability to handle high-pressure, variable load applications in natural gas treatment and liquefaction processes. For example, ongoing pipeline construction projects in India and China are increasing the demand for reliable and efficient reciprocating compressors to manage high-pressure gas transportation and storage requirements. This driver supports market growth by reinforcing the need for advanced reciprocating compressors designed to deliver stable performance while reducing operational risks in large-scale natural gas infrastructure operations.

High maintenance requirements and the potential for unplanned downtimes act as restraints within the Reciprocating Compressor Market, particularly in continuous operations such as oil and gas processing and chemical manufacturing. Reciprocating compressors involve numerous moving parts, including pistons, valves, and seals, which require regular inspection and replacement due to wear and tear, increasing maintenance costs and operational planning complexity. Industries operating in harsh environments face additional challenges with the frequent replacement of critical components, which may result in unscheduled shutdowns, disrupting production cycles. For instance, operators managing reciprocating compressors in offshore oil platforms must consider the costs and logistics associated with maintenance scheduling while minimizing productivity loss. These factors encourage some end-users to consider alternative compressor technologies with lower maintenance profiles, impacting the consistent adoption of reciprocating compressors in certain industrial segments.

The integration of digital monitoring and predictive maintenance technologies presents a strong opportunity within the Reciprocating Compressor Market. As industries prioritize operational efficiency, the adoption of IoT-enabled sensors, vibration analysis, and AI-based predictive analytics in reciprocating compressors enables real-time condition monitoring and early detection of anomalies. This technology reduces downtime by allowing operators to schedule maintenance proactively while optimizing equipment utilization and extending compressor lifecycles. For instance, industrial gas producers are leveraging digital monitoring systems to track critical parameters such as cylinder pressures, temperatures, and valve performance, improving operational reliability. This shift toward intelligent reciprocating compressors aligns with industry goals for data-driven maintenance strategies and cost control, making digitally enabled reciprocating compressors an attractive investment for industrial facilities globally.

Meeting stringent environmental regulations is a significant challenge for the Reciprocating Compressor Market, particularly in regions with rigorous emission control standards for industrial operations. Compressors can be a source of methane and volatile organic compound emissions due to seal leaks and blowdowns, requiring manufacturers to adopt advanced sealing and emission control technologies. Compliance with environmental regulations such as the U.S. EPA’s air quality standards and the European Union’s emission directives requires investments in low-leakage designs, vapor recovery systems, and continuous monitoring, which can increase upfront and operational costs for end-users. Industrial facilities using reciprocating compressors in refineries, chemical plants, and natural gas processing facilities must adapt to evolving environmental frameworks while ensuring high operational reliability, which adds complexity to equipment selection and maintenance strategies in the Reciprocating Compressor Market.

• Expansion of Hydrogen Infrastructure: The Reciprocating Compressor market is witnessing growing demand for hydrogen compression systems driven by increased investments in hydrogen refueling stations and green hydrogen projects. Compressors with high-pressure handling capabilities are being deployed in hydrogen production, transportation, and storage applications, supporting initiatives across Europe and Asia-Pacific. For example, new hydrogen plants in Germany and South Korea have integrated advanced reciprocating compressors to manage compression at pressures exceeding 350 bar, meeting safety and operational efficiency requirements in emerging hydrogen value chains.

• Adoption of Digital Twin and Predictive Monitoring: The integration of digital twin technology and predictive maintenance tools is transforming the operational landscape of the Reciprocating Compressor market. Industrial facilities are utilizing real-time sensor data combined with digital twins to simulate compressor performance and anticipate maintenance needs, reducing unplanned downtime. Facilities in the Middle East oil and gas sector have reported efficiency gains of up to 12% through digital twin-based compressor monitoring, improving reliability while reducing operational costs and maintenance intervals.

• Shift Toward Low-Emission and Leak-Free Systems: Environmental regulations are pushing the Reciprocating Compressor market toward the adoption of low-emission, leak-free systems. Oil and gas operators are increasingly replacing older compressors with new models featuring enhanced sealing technologies to reduce methane emissions. Reciprocating compressors with zero-emission packings and advanced vapor recovery units are being deployed across gas gathering and pipeline applications, particularly in North America, aligning with industry decarbonization targets and methane management goals.

• Increased Deployment in Modular Gas Processing Units: Modular and skid-mounted gas processing units are seeing increased deployment in the Reciprocating Compressor market, particularly for remote and offshore applications. The ability to fabricate, test, and transport complete compressor packages allows operators to reduce site construction times and improve project economics. Countries in Southeast Asia and Africa are adopting modular reciprocating compressors for natural gas processing, enabling flexible capacity expansion while maintaining compliance with safety and operational efficiency requirements.

The Reciprocating Compressor market is segmented based on type, application, and end-user insights, each defining specific operational and investment priorities for stakeholders. By type, the market includes single-acting, double-acting, diaphragm, and other specialized reciprocating compressors used across high-pressure and variable flow applications. In terms of application, the market covers natural gas processing, refinery operations, industrial gas handling, and refrigeration, reflecting diverse energy, industrial, and process demands globally. By end-user, the Reciprocating Compressor market is driven by industries such as oil and gas, chemical and petrochemical, power generation, and manufacturing, where these compressors are essential for high-reliability gas compression and delivery. These segments demonstrate a strategic focus on improving operational reliability, reducing emissions, and enhancing lifecycle efficiency within reciprocating compressor installations worldwide.

Single-acting reciprocating compressors lead the Reciprocating Compressor market due to their widespread use in oil and gas field services, refineries, and small-scale industrial applications where cost-effective, high-pressure gas delivery is needed. They are valued for their lower maintenance requirements and adaptability across various field conditions. Double-acting compressors are the fastest-growing type, driven by their high efficiency and capability to handle larger volumes in continuous operations such as natural gas pipeline transmission and petrochemical processes. Diaphragm compressors find niche applications in handling ultra-pure and toxic gases in the chemical and specialty gas sectors, providing leak-free compression essential for safety-critical environments. Other types, including high-speed reciprocating compressors, contribute by serving offshore platforms and modular installations where weight, footprint, and ease of maintenance are key factors. This diversity across types ensures the Reciprocating Compressor market remains adaptable to varied industrial needs, operational pressures, and site conditions.

Natural gas processing is the leading application segment in the Reciprocating Compressor market, driven by the global demand for gas treatment and transmission across extensive pipeline networks and storage facilities. These compressors are critical for maintaining consistent gas flow and handling high-pressure delivery in processing units and pipeline infrastructure. Refinery operations represent the fastest-growing application segment as global refining capacity expands to meet rising fuel demand while integrating low-emission, high-efficiency compression systems to support hydrocarbon processing and vapor recovery. Industrial gas handling, including air separation and specialty gas production, also holds a notable share, supported by the need for precise and clean compression across industrial and medical gas supply chains. Refrigeration applications, particularly in food processing and chemical industries, continue to utilize reciprocating compressors for their high compression ratios and reliable operation, reflecting the versatility of these compressors in maintaining process stability across a wide range of industrial processes.

The oil and gas sector is the leading end-user segment in the Reciprocating Compressor market, utilizing these compressors extensively for gas gathering, enhanced oil recovery, and pipeline transmission due to their ability to handle high-pressure and variable flow rates reliably. The chemical and petrochemical industry represents the fastest-growing end-user segment, driven by rising investments in petrochemical plants and gas-based chemical production facilities that require robust, leak-free compressors for high-purity gas handling. Power generation facilities are also notable end-users, employing reciprocating compressors for gas turbine fuel supply and in auxiliary processes, reflecting stable demand within this sector. Manufacturing industries, including steel, food and beverage, and electronics, contribute to the market by employing reciprocating compressors for various gas handling and refrigeration processes, demonstrating the widespread reliance on these compressors to support critical industrial operations globally while meeting efficiency and emission reduction targets.

Asia-Pacific accounted for the largest market share at 39.2% in 2024 however, the Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 4.1% between 2025 and 2032.

The Reciprocating Compressor market in Asia-Pacific is driven by rising industrialization and robust infrastructure development in China, India, and Southeast Asia, where these compressors are used extensively in natural gas transmission, chemical manufacturing, and refinery operations. Meanwhile, the Middle East & Africa region is experiencing accelerated investments in oil and gas infrastructure projects, with countries like the UAE and Saudi Arabia focusing on upgrading energy facilities using advanced reciprocating compressors to improve operational reliability while reducing emissions. Europe and North America continue to sustain steady demand due to stringent environmental regulations encouraging the replacement of older units with energy-efficient, low-emission reciprocating compressors, while South America benefits from increasing natural gas exploration and processing projects.

Industrial Expansion and Digital Retrofit Driving Demand Surge

The North America Reciprocating Compressor market captured approximately 26.7% of the global volume in 2024, supported by ongoing investments across oil and gas, chemical, and industrial gas sectors. Demand is driven by shale gas activities in the United States and Canada, where reciprocating compressors support high-pressure gas gathering and pipeline transport. Regulatory changes, including methane emissions reduction programs, are accelerating the replacement of legacy systems with leak-free, low-emission reciprocating compressors. Government incentives for upgrading energy infrastructure and emissions compliance further support this trend. The region is witnessing digital transformation within industrial operations, with operators adopting condition monitoring and predictive analytics on reciprocating compressors to enhance asset reliability, reduce unplanned downtimes, and improve energy efficiency in critical industrial processes.

Clean Energy Goals and Industrial Automation Fuel Market Growth

Holding around 21.3% market share in 2024, the Europe Reciprocating Compressor market benefits from strong demand in Germany, the UK, and France, driven by the chemical, petrochemical, and industrial gas sectors. Regulatory bodies, including the European Environment Agency and local emission control regulations, are enforcing low-emission standards that encourage industries to adopt modern reciprocating compressors with advanced sealing and monitoring systems. Sustainability initiatives across the EU support the transition to hydrogen infrastructure, where high-pressure reciprocating compressors play a critical role in transportation and refueling systems. The adoption of Industry 4.0 solutions is promoting the integration of digital twins and IoT-enabled monitoring, enhancing predictive maintenance and optimizing compressor efficiency across European industrial facilities.

Infrastructure Boom and Industrial Energy Demand Propel Growth

Asia-Pacific remains the highest-volume region in the Reciprocating Compressor market, led by China, India, and Japan as top consumers of high-pressure compressors for refining, petrochemical, and natural gas processing. Rapid infrastructure development, including new LNG terminals and expanded refinery capacities, is driving compressor demand in industrial and energy applications. Countries are modernizing their energy infrastructure with modular gas processing units and automated monitoring to enhance operational efficiencies. Innovation hubs in China and Japan are advancing the development of digital-ready reciprocating compressors, featuring predictive analytics and low-emission technologies tailored for industrial users aiming to align with sustainability and energy efficiency goals across diverse operational settings.

Energy Sector Investments and Industrial Growth Strengthening Demand

The Reciprocating Compressor market in South America, particularly in Brazil and Argentina, is expanding with rising demand in oil and gas processing, accounting for a 7.8% share in 2024. Regional infrastructure improvements, including pipeline expansions and refinery modernization projects, are driving compressor installations across energy and industrial gas sectors. Government incentives for domestic energy production and trade policies supporting oil and gas development are encouraging local industries to upgrade to reliable reciprocating compressor systems for critical operations. The region’s industrial growth, particularly in Brazil’s petrochemical and manufacturing sectors, is creating consistent demand for high-performance compressors designed for varied operational pressures and harsh working environments.

Oil and Gas Infrastructure Development Boosting Market Dynamics

The Middle East & Africa region is experiencing increasing demand for reciprocating compressors, driven by the oil and gas, petrochemical, and construction sectors across the UAE, Saudi Arabia, and South Africa. The region benefits from major upstream and downstream infrastructure projects, where reciprocating compressors are utilized in high-pressure gas gathering, refining, and gas injection applications. Technological modernization is underway, with operators incorporating digital monitoring and AI-based predictive analytics into reciprocating compressors to reduce maintenance costs while ensuring operational reliability. Local regulations supporting energy efficiency and emission reduction are encouraging investment in advanced reciprocating compressor systems that align with sustainability goals while meeting high-capacity operational requirements.

China (24.6%): High production capacity and expanding industrial base driving strong end-user demand in the Reciprocating Compressor Market.

United States (18.2%): Strong end-user demand across shale gas and industrial sectors with consistent upgrades to modern, low-emission reciprocating compressors.

The Reciprocating Compressor market features a competitive landscape with over 45 active global and regional manufacturers focusing on high-performance, energy-efficient compressor systems across industrial and energy applications. Key competitors position themselves by offering advanced reciprocating compressors equipped with low-emission technologies, predictive maintenance capabilities, and modular configurations to serve sectors such as oil and gas, petrochemicals, and industrial gases. Strategic initiatives, including product launches of high-pressure, leak-free compressors and partnerships with digital technology firms for real-time monitoring solutions, are shaping the competitive environment. Mergers and acquisitions among leading players are strengthening technology portfolios and expanding geographic presence, particularly in Asia-Pacific and the Middle East. Innovation trends influencing competition include the adoption of digital twin technology, advanced sealing systems for methane reduction, and the integration of AI-based diagnostics to enhance operational reliability. Additionally, companies are differentiating themselves by providing aftermarket services, including remote monitoring and predictive maintenance packages, to improve equipment lifecycle management, reinforcing their positioning in the Reciprocating Compressor market while meeting evolving customer expectations.

Atlas Copco AB

Siemens Energy AG

Ariel Corporation

Gardner Denver Holdings Inc.

Burckhardt Compression AG

Howden Group

Hitachi Ltd.

MAN Energy Solutions SE

Kobelco Compressors

Ingersoll Rand Inc.

Current and emerging technologies are reshaping the operational landscape of the Reciprocating Compressor market, focusing on efficiency, low emissions, and digital enablement. Advanced sealing technologies are being integrated into reciprocating compressors to reduce fugitive emissions, particularly methane, while maintaining high-pressure operational capabilities in natural gas and petrochemical applications. The adoption of variable frequency drives is improving energy efficiency by dynamically adjusting motor speeds according to system load, supporting operational cost reductions and flexible process handling. Digital twin technology is gaining traction, allowing operators to simulate compressor performance, predict component wear, and plan maintenance without interrupting operations. Sensor-based monitoring systems with vibration and temperature analysis are enhancing predictive maintenance, reducing unplanned downtime, and increasing the reliability of reciprocating compressors across industrial gas and refinery operations. AI-enabled analytics and condition-based monitoring are optimizing gas handling processes, allowing compressors to automatically adjust parameters based on workload and operational conditions. Additionally, modular reciprocating compressor packages designed for offshore and remote installations are being equipped with IoT-enabled monitoring and compact control systems, facilitating faster deployment while ensuring efficient, reliable operation. Collectively, these technological advancements are aligning reciprocating compressors with industrial decarbonization and sustainability goals while improving operational resilience across critical applications.

• In February 2024, Ariel Corporation launched a new high-pressure reciprocating compressor series for hydrogen refueling stations, capable of delivering pressures above 450 bar while incorporating advanced leak detection sensors to support zero-emission hydrogen mobility infrastructure development in Europe and Asia.

• In May 2024, Siemens Energy introduced a modular reciprocating compressor package with integrated digital twin capabilities for real-time performance monitoring and predictive maintenance, targeting refinery and industrial gas facilities seeking to reduce operational downtime while improving energy efficiency.

• In September 2023, Burckhardt Compression expanded its service portfolio with a cloud-based monitoring system for reciprocating compressors, allowing remote condition monitoring, vibration analysis, and predictive diagnostics, supporting industrial customers in enhancing compressor reliability and optimizing maintenance intervals.

• In November 2023, Ingersoll Rand unveiled a new line of oil-free reciprocating compressors specifically designed for the food and beverage industry, featuring stainless steel components and sanitary design to meet strict hygiene standards while maintaining consistent high-pressure performance.

The Reciprocating Compressor Market Report comprehensively analyzes the global market, covering key segments by type, including single-acting, double-acting, diaphragm, and specialized high-speed reciprocating compressors used across industrial, energy, and specialty gas applications. It details application areas such as natural gas processing, petrochemical and chemical manufacturing, refinery operations, and industrial gas handling, reflecting the widespread integration of reciprocating compressors in critical process and energy infrastructure worldwide. The report examines geographic regions, with a focus on high-demand areas such as Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, highlighting regional consumption patterns, industrial expansion, and technology adoption trends. Additionally, it explores the technological landscape, detailing the impact of digital twin systems, IoT-enabled monitoring, advanced sealing technologies, and AI-based predictive maintenance on compressor operations. The report also outlines the competitive environment by profiling major players, strategic partnerships, product innovations, and sustainability initiatives shaping market dynamics. The analysis further includes insights into emerging trends such as hydrogen infrastructure development and modular skid-mounted compressor systems for offshore and remote industrial operations, enabling stakeholders to evaluate investment opportunities, technological positioning, and operational optimization strategies within the Reciprocating Compressor market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 7,114.21 Million |

|

Market Revenue in 2032 |

USD 9,440.71 Million |

|

CAGR (2025 - 2032) |

3.6% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Atlas Copco AB, Siemens Energy AG, Ariel Corporation, Gardner Denver Holdings Inc., Burckhardt Compression AG, Howden Group, Hitachi Ltd., MAN Energy Solutions SE, Kobelco Compressors, Ingersoll Rand Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |