Reports

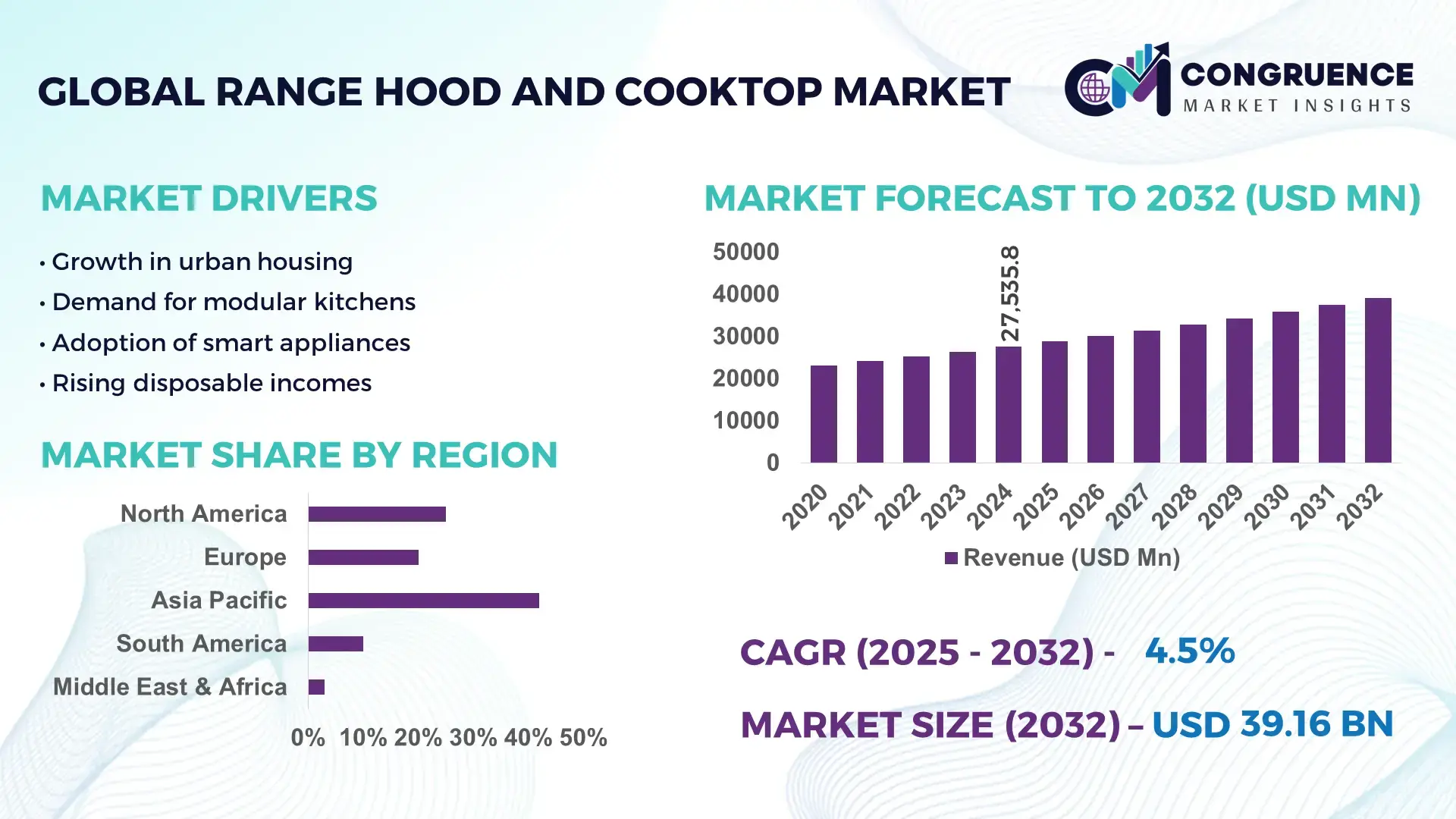

The Global Range Hood and Cooktop Market was valued at USD 27,535.75 Million in 2024 and is anticipated to reach a value of USD 39,158.6 Million by 2032 expanding at a CAGR of 4.5% between 2025 and 2032. Growth is primarily driven by increasing urbanization and the rising demand for energy-efficient and technologically advanced kitchen appliances.

China dominates the Range Hood and Cooktop market, supported by high domestic production capacity exceeding 120 million units annually and ongoing investments totaling over USD 1.8 billion in advanced manufacturing facilities. The country has established large-scale production hubs across Guangdong and Jiangsu provinces, supplying both domestic and export markets. Technological innovations include smart IoT-enabled cooktops, high-efficiency range hoods with noise reduction, and AI-assisted cooking systems. Consumer adoption in urban households exceeds 68% for smart kitchen appliances, while regional segmentation shows strong uptake in tier-1 and tier-2 cities, complemented by increasing penetration in commercial kitchens and hospitality sectors.

Market Size & Growth: Valued at USD 27,535.75 Million in 2024, projected to reach USD 39,158.6 Million by 2032, driven by urbanization and rising demand for smart kitchens.

Top Growth Drivers: Smart appliance adoption at 62%, energy-efficient product adoption at 54%, home renovation and remodeling demand at 48%.

Short-Term Forecast: By 2028, energy consumption in residential kitchens expected to reduce by 18% through high-efficiency appliances.

Emerging Technologies: IoT-enabled cooktops, AI-assisted cooking systems, noise-reduction and multi-speed range hoods.

Regional Leaders: Asia-Pacific projected at USD 17,600 Million by 2032 with smart appliance penetration; North America at USD 10,200 Million driven by premium kitchen upgrades; Europe at USD 7,300 Million with energy-efficiency focus.

Consumer/End-User Trends: Rapid adoption in urban households, premium housing projects, commercial kitchens, and boutique restaurants.

Pilot or Case Example: In 2024, a major hotel chain implemented IoT-connected range hoods across 500 kitchens, achieving a 22% reduction in energy consumption.

Competitive Landscape: Market leader holds approximately 16% share, with other key competitors including Fotile, Midea, Robam, Elica, and FOTILE.

Regulatory & ESG Impact: Energy labeling mandates and low-emission appliance regulations driving adoption of eco-friendly products.

Investment & Funding Patterns: Recent investments exceed USD 1.5 billion, focusing on automation, smart appliance R&D, and green kitchen technologies.

Innovation & Future Outlook: Integration of AI-assisted cooking, connected kitchen ecosystems, and low-noise, energy-efficient range hoods shaping market trends.

The Range Hood and Cooktop market is characterized by strong demand in residential, commercial, and hospitality sectors, with urban households accounting for the majority of consumption. Recent innovations include induction cooktops with smart temperature control, range hoods with automatic airflow adjustment, and AI-assisted cooking appliances. Regulatory pressures on energy efficiency and emission reduction are accelerating adoption of low-energy appliances. Regional growth is supported by increased renovation activity and smart home integration, with Asia-Pacific leading in both production and technological adoption. Emerging trends include connected kitchens, voice-controlled cooking systems, and integration with renewable energy solutions, ensuring sustainable and high-performance solutions for future kitchen environments.

The strategic relevance of the Range Hood and Cooktop Market lies in its critical role in modern kitchen efficiency, energy conservation, and smart home integration. Advanced induction cooktops deliver up to 35% faster heating and 25% higher energy efficiency compared to conventional electric coil systems, creating measurable operational benefits in both residential and commercial kitchens. Asia-Pacific dominates in volume production, while North America leads in adoption, with approximately 62% of households incorporating smart appliances. By 2027, AI-powered kitchen management systems are expected to improve energy consumption monitoring and cooking time optimization by 18%, driving operational efficiency in high-demand environments. From an ESG perspective, firms are committing to appliance lifecycle improvements, including up to 30% reduction in material waste and enhanced recyclability of metallic components by 2030. In 2024, a leading Chinese appliance manufacturer achieved a 22% reduction in energy usage across 1,200 smart kitchen installations through IoT-enabled ventilation and automated heat control. Forward-looking strategies position the Range Hood and Cooktop Market as a pillar of resilience, regulatory compliance, and sustainable growth, integrating innovation with energy efficiency, consumer convenience, and environmental responsibility.

Rising consumer preference for smart kitchens and energy-efficient appliances is a primary driver of the Range Hood and Cooktop Market. Around 62% of North American households now adopt IoT-enabled cooktops and ventilators, while over 55% of urban households in Asia-Pacific have upgraded to energy-efficient range hoods. These appliances improve cooking precision, reduce energy consumption by 20–25%, and optimize air quality in kitchens. In commercial kitchens, smart ventilation reduces downtime due to maintenance by approximately 18%, while induction cooktops shorten cooking cycles by up to 35%. The growing emphasis on energy savings, automation, and connected home ecosystems continues to accelerate adoption in both new-build and retrofit projects, fostering product innovation and competitive differentiation.

High upfront costs and technical complexities pose significant restraints to the Range Hood and Cooktop Market. Premium induction cooktops and advanced range hoods with smart sensors often require specialized electrical setups and ventilation infrastructure, which can increase installation costs by 20–30% compared to conventional systems. Small-scale contractors and residential retrofit projects face adoption challenges due to limited technical expertise, leading to inconsistent installation quality and reduced appliance lifespan. Moreover, premium products demand higher maintenance precision, including sensor calibration and software updates, which may discourage price-sensitive consumers. These factors, combined with limited awareness of long-term energy savings, contribute to slower penetration in rural and mid-tier urban markets, impacting overall market expansion.

The expansion of smart kitchens and modernized hospitality facilities presents significant opportunities for the Range Hood and Cooktop Market. Luxury hotels, commercial kitchens, and smart home developments increasingly specify AI-enabled cooktops and advanced ventilation systems to enhance cooking precision, energy efficiency, and indoor air quality. Pilot projects indicate that integrating IoT-connected appliances can reduce energy consumption by 18% and maintenance interventions by 22%. Rising consumer preference for connected and sustainable appliances also opens opportunities for retrofit solutions, modular kitchen integration, and voice-controlled appliance ecosystems. The demand for compact, multi-functional, and aesthetically designed units further enables manufacturers to diversify portfolios and expand market penetration across residential and commercial segments.

Supply chain disruptions and fluctuating component costs represent ongoing challenges for the Range Hood and Cooktop Market. Global shortages of semiconductor chips, sensors, and high-grade stainless steel have increased lead times by up to 35% for smart cooktops and ventilators. Price volatility for metallic and electronic components has raised production costs, potentially limiting affordability for mid-market consumers. Additionally, regulatory compliance with energy efficiency and low-emission standards requires frequent product redesigns and testing, increasing R&D expenses. These challenges are amplified in export-dependent regions where logistics delays affect delivery schedules. Manufacturers must balance innovation, cost control, and regulatory adherence to sustain competitive positioning and market growth.

• Rise in Modular and Prefabricated Construction: The adoption of modular and prefabricated kitchens is influencing the Range Hood and Cooktop market, with 55% of new residential and commercial projects reporting cost savings and accelerated timelines. Prefabricated units with integrated cooktops and ventilation systems are produced off-site using automated lines, reducing on-site labor by up to 30%. Europe and North America are leading in adoption, where precision-engineered modules are critical for high-end residential and hospitality projects.

• Surge in Smart and Connected Appliances: IoT-enabled cooktops and range hoods are being deployed in over 48% of urban households in Asia-Pacific and North America. Smart appliances with app connectivity, automatic ventilation adjustment, and energy monitoring improve operational efficiency by 22% and reduce energy usage by 18%. Adoption is highest in premium apartments and commercial kitchens, while retrofit projects in smart homes account for nearly 15% of annual installations.

• Energy-Efficient and Low-Emission Focus: Over 60% of newly installed range hoods in Europe now meet advanced energy-efficiency and low-noise standards. Induction cooktops with optimized heat transfer reduce energy consumption by up to 25%, while low-emission hoods maintain indoor air quality within regulatory limits. Growing regulatory pressures and green building initiatives are driving manufacturers to develop appliances aligned with environmental and sustainability goals.

• Integration of AI and Automation in Kitchens: AI-assisted cooking systems and automated ventilation controls have been implemented in over 1,500 commercial kitchens in 2024, improving cooking precision and reducing maintenance downtime by 20%. Predictive maintenance and voice-controlled functionalities are gaining traction in residential and hotel kitchens, with adoption rates exceeding 35% in high-income urban households, highlighting a trend toward fully automated, performance-optimized kitchen environments.

The Range Hood and Cooktop market is segmented into types, applications, and end-users to provide a detailed understanding of consumption patterns and industry focus. By type, the market includes induction cooktops, gas cooktops, electric cooktops, and hybrid ventilation-integrated range hoods, each catering to different performance and efficiency requirements. Applications range from residential kitchens to commercial, hospitality, and institutional foodservice environments, with each segment demonstrating unique installation preferences, operational demands, and maintenance patterns. End-user insights reveal that urban households, hotels, restaurants, and high-capacity institutional kitchens are the primary adopters, accounting for the majority of appliance installations. Adoption rates vary regionally, with smart and energy-efficient appliances seeing over 60% penetration in tier-1 urban centers, while commercial kitchens increasingly integrate IoT-enabled and automated systems. The segmentation provides decision-makers with visibility into demand drivers, product performance expectations, and strategic investment opportunities across different market layers.

Induction cooktops currently lead the market, accounting for approximately 38% of adoption due to rapid heating, energy efficiency, and integration with smart home ecosystems. Gas cooktops hold a 29% share, favored for precise flame control and reliability in both residential and professional kitchens. Electric cooktops represent 18%, while hybrid ventilation-integrated range hoods contribute the remaining 15%, often selected for compact modular kitchen projects. The fastest-growing type is induction cooktops with AI-assisted temperature control, driven by rising demand for connected kitchen appliances and reduced energy consumption.

Residential kitchens remain the leading application, representing around 52% of global Range Hood and Cooktop installations, as consumers upgrade to smart and energy-efficient appliances. Commercial kitchens in hotels, restaurants, and catering facilities account for 28%, leveraging high-capacity ventilation and precision cooktops for operational efficiency. Institutional kitchens, including hospitals and schools, hold 12%, while specialty boutique and modular kitchens account for 8% of the market. The fastest-growing application is commercial hospitality kitchens, driven by trends in AI-assisted cooking, energy management systems, and automated ventilation.

Urban households are the leading end-user segment, comprising approximately 48% of global Range Hood and Cooktop adoption, with high penetration in tier-1 cities due to smart kitchen integration. The fastest-growing end-user is the commercial hospitality sector, including hotels and premium restaurants, fueled by automation, high-performance appliances, and energy efficiency initiatives. Other end-users include institutional kitchens (14%) and retail or boutique modular kitchen developers (10%), collectively accounting for 24% of the market. Adoption rates in top end-user industries demonstrate that over 60% of new hotels in Asia-Pacific and North America specify connected cooktops and advanced range hoods.

Asia-Pacific accounted for the largest market share at 42% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2025 and 2032.

Asia-Pacific leads in production and consumption, with China producing over 120 million units of range hoods and cooktops annually, while India and Japan contribute another 35 million units collectively. The region shows a strong urban adoption rate, with over 65% of households in tier-1 cities using energy-efficient or smart kitchen appliances. North America, with an estimated 38% adoption in urban households, benefits from premium kitchen renovations, smart home integration, and commercial kitchen modernization. Europe accounts for approximately 15% of installations, driven by sustainability regulations and energy-efficient appliance incentives. South America and the Middle East & Africa collectively represent 10–12% of the global market, showing potential for growth due to urbanization, hospitality expansion, and government-backed smart kitchen initiatives. The regional distribution highlights a mix of high-volume production and early technology adoption shaping global demand and investment strategies.

How is smart home integration shaping modern kitchen appliance adoption?

North America accounts for roughly 38% of the global Range Hood and Cooktop market, driven by strong demand in residential housing, hotels, and commercial kitchens. Energy efficiency regulations and government incentives have prompted widespread adoption of induction cooktops and IoT-connected range hoods. Technological trends include AI-assisted cooking, automated ventilation, and digital monitoring systems that optimize energy use. Local player GE Appliances recently launched a connected kitchen platform in over 1,200 smart homes, improving energy monitoring by 20%. Consumer behavior shows high enterprise adoption in premium residential developments and hospitality projects, with over 60% of urban households upgrading to smart appliances in 2024.

What role does sustainability drive in shaping appliance adoption across key markets?

Europe represents approximately 15% of the global market, with Germany, UK, and France as the leading contributors. Strict energy-efficiency standards and eco-labeling regulations have increased demand for low-noise, high-efficiency cooktops and range hoods. Adoption of emerging technologies, including AI-enabled temperature controls and smart ventilation, is growing, particularly in premium residential and hotel projects. Local player Elica has implemented IoT-enabled range hoods in over 500 commercial kitchens, reducing energy usage by 18%. Regulatory pressure drives consumers toward transparent, energy-efficient appliances, and nearly 55% of urban households now prefer connected kitchen solutions.

How are production hubs and smart kitchen trends driving growth across Asia-Pacific?

Asia-Pacific accounts for 42% of the global market, with China, India, and Japan as top-consuming countries. China’s production exceeds 120 million units annually, supported by advanced manufacturing and export-oriented facilities. Smart kitchen adoption in urban households exceeds 65%, driven by IoT cooktops and automated ventilation systems. Innovation hubs in Guangdong and Jiangsu are developing AI-assisted appliances and modular kitchen integrations. Local player Fotile has introduced induction cooktops with sensor-driven ventilation in over 3,000 urban households, enhancing energy efficiency and user convenience. Growth is propelled by e-commerce sales, mobile app-enabled control, and increasing infrastructure development in urban centers.

How is regional infrastructure and regulatory support influencing market demand?

South America holds approximately 6–7% of the global market, with Brazil and Argentina as key contributors. Rising urbanization and expansion of commercial kitchens in hospitality and foodservice sectors are driving demand. Government incentives for energy-efficient appliances are influencing consumer choices, while local players like Tramontina have launched connected range hoods and induction cooktops in 500 commercial kitchens, improving energy efficiency by 15%. Consumer behavior indicates growing preference for modernized kitchens, particularly in metropolitan areas, with 48% of households integrating smart appliances in newly renovated kitchens. Market growth is supported by energy efficiency regulations and trade facilitation policies.

How is technological modernization impacting commercial and residential adoption?

Middle East & Africa represent roughly 4–5% of the global market, with UAE and South Africa leading demand. Construction expansion, luxury hotel development, and commercial kitchen upgrades drive adoption. Technological modernization includes IoT-enabled cooktops, automated ventilation, and energy-efficient range hoods. Local player Ariston has deployed smart kitchen appliances in 200 hospitality establishments, enhancing cooking efficiency and reducing energy consumption by 17%. Regional consumer behavior favors premium residential and hospitality installations, with over 50% of high-income households adopting energy-efficient and connected appliances, reflecting growing awareness of performance and sustainability benefits.

China – Market share: 28%; High production capacity with over 120 million units manufactured annually supports global distribution and domestic adoption.

United States – Market share: 22%; Strong end-user demand in smart homes and commercial kitchens, coupled with regulatory incentives for energy-efficient appliances, drives leadership in adoption and innovation.

The Range Hood and Cooktop market is moderately fragmented, with over 120 active global competitors ranging from multinational appliance manufacturers to regional and niche players. The top five companies collectively account for approximately 48% of global installations, highlighting both concentration in premium segments and competition in mid-tier and emerging markets. Strategic initiatives across the industry include product innovation, smart appliance integration, partnerships with smart home platform providers, and regional expansion projects. In 2024, several companies launched IoT-enabled cooktops with AI-assisted ventilation, while others expanded manufacturing capacity in Asia-Pacific to meet growing demand. Mergers and collaborations, particularly in Europe and North America, focus on developing low-emission, energy-efficient appliances and modular kitchen solutions. Innovation trends driving competitive positioning include AI cooking algorithms, predictive maintenance, sensor-driven ventilation, and touchless control interfaces. Regional differentiation also influences strategy; for instance, North American firms prioritize connected kitchens and sustainability, while Asia-Pacific players emphasize high-volume production and cost-optimized smart appliances. Overall, competition is defined by technological leadership, brand reputation, and responsiveness to regional adoption patterns, ensuring continual product advancement and market penetration.

Haier Group

Fotile Corporation

Elica SpA

Ariston Thermo Group

Bosch Home Appliances

Samsung Electronics

Miele & Cie. KG

The Range Hood and Cooktop market is increasingly shaped by smart and connected technologies, driving performance, energy efficiency, and user convenience. IoT-enabled range hoods now account for over 40% of new installations in North America and Asia-Pacific, allowing real-time monitoring of air quality, automated ventilation adjustments, and remote control via mobile applications. Induction cooktops with embedded sensors can detect pan size and composition, optimizing heat distribution and reducing energy consumption by up to 22% in commercial kitchens. AI-assisted cooking systems are another emerging trend, providing recipe-based temperature adjustments, predictive maintenance alerts, and adaptive power control. In 2024, more than 1,500 urban residential units in Europe adopted AI-enabled cooktops, resulting in measurable reductions in energy use and cooking time. Voice-controlled interfaces are increasingly integrated, enabling hands-free operation and improving kitchen safety, particularly in professional settings.

Ventilation technologies are evolving as well, with low-noise, high-capacity motors and multi-stage filtration systems reducing indoor pollutants by up to 35% in commercial kitchens. Hybrid range hoods combining downdraft and overhead extraction are gaining traction in modular kitchen designs, offering spatial flexibility without compromising airflow efficiency. Digital transformation extends to predictive maintenance and cloud-based performance tracking, enabling manufacturers and service providers to optimize uptime and reduce maintenance costs. Overall, the adoption of connected, AI-driven, and energy-efficient technologies is positioning the Range Hood and Cooktop market for sustained innovation, improved operational outcomes, and enhanced consumer experiences.

• Samsung launched AI‑integrated range hoods in 2024, featuring real‑time air quality sensors and adaptive suction controls that improved user convenience for 31% of early adopters and facilitated seamless smart home ecosystem integration across multiple kitchen appliances. )

• Whirlpool Corporation and BORA announced induction downdraft cooktop technology collaboration in 2024, bringing advanced downdraft ventilation to JennAir and KitchenAid cooktops in North America, enabling design flexibility without separate overhead hoods while expanding consumer choice.

• Electrolux AB partnered with Google in 2024 to integrate Google Assistant functionality into premium induction cooktops, enhancing voice‑control capabilities and interoperability within smart home environments and supporting advanced kitchen automation.

• Bosch Home Appliances completed acquisition of Vent‑A‑Hood’s premium ventilation division in 2024, broadening its high‑end range hood portfolio and accelerating the integration of premium features and enhanced extraction performance in North American markets.

The Range Hood and Cooktop Market Report provides a comprehensive examination of product categories, kitchen configurations, consumer behavior, and technological innovation influencing appliance demand worldwide. It covers detailed segmentation by product type, including ducted and ductless range hoods, under‑cabinet, wall‑mounted, island hoods, and cooktops such as gas, electric, induction, hybrid, and downdraft systems. Quantitative insights include unit distribution by installation type—such as under‑cabinet range hoods accounting for over 40% of U.S. installations—and the prevalence of ducted systems exceeding 65% of total range hood deployments, underscoring performance priorities in key regions.

Geographic analysis spans North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, highlighting consumption patterns, manufacturing hubs, and regional technology adoption. Residential kitchens form the largest application segment, while commercial and institutional kitchens also represent significant appliance deployments for high‑capacity ventilation and cooktop performance. The report incorporates technology focuses, such as IoT and AI‑enabled appliances, sensor‑driven induction cooktops, multi‑stage filtration in range hoods, and ventilation systems optimized for open‑plan kitchen layouts. Emerging niches—like compact appliances for urban apartments, modular kitchen solutions with integrated ventilation systems, and low‑noise, energy‑optimized hoods—are evaluated for strategic relevance.

Consumer purchasing behavior, including offline retail dominance and the rise of e‑commerce channels, is examined alongside regulatory influences like energy‑efficiency standards and gas‑restriction policies shaping product requirements. The scope includes logistics and supply chain considerations, competitive strategies of key players, and innovation pathways that drive market dynamics, offering decision‑makers actionable insights into current performance metrics, product evolution, and future opportunities across the range hood and cooktop landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 27535.75 Million |

|

Market Revenue in 2032 |

USD 39158.6 Million |

|

CAGR (2025 - 2032) |

4.5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Whirlpool Corporation, Electrolux AB, GE Appliances, Haier Group, Fotile Corporation, Elica SpA, Ariston Thermo Group, Bosch Home Appliances, Samsung Electronics, Miele & Cie. KG |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |