Reports

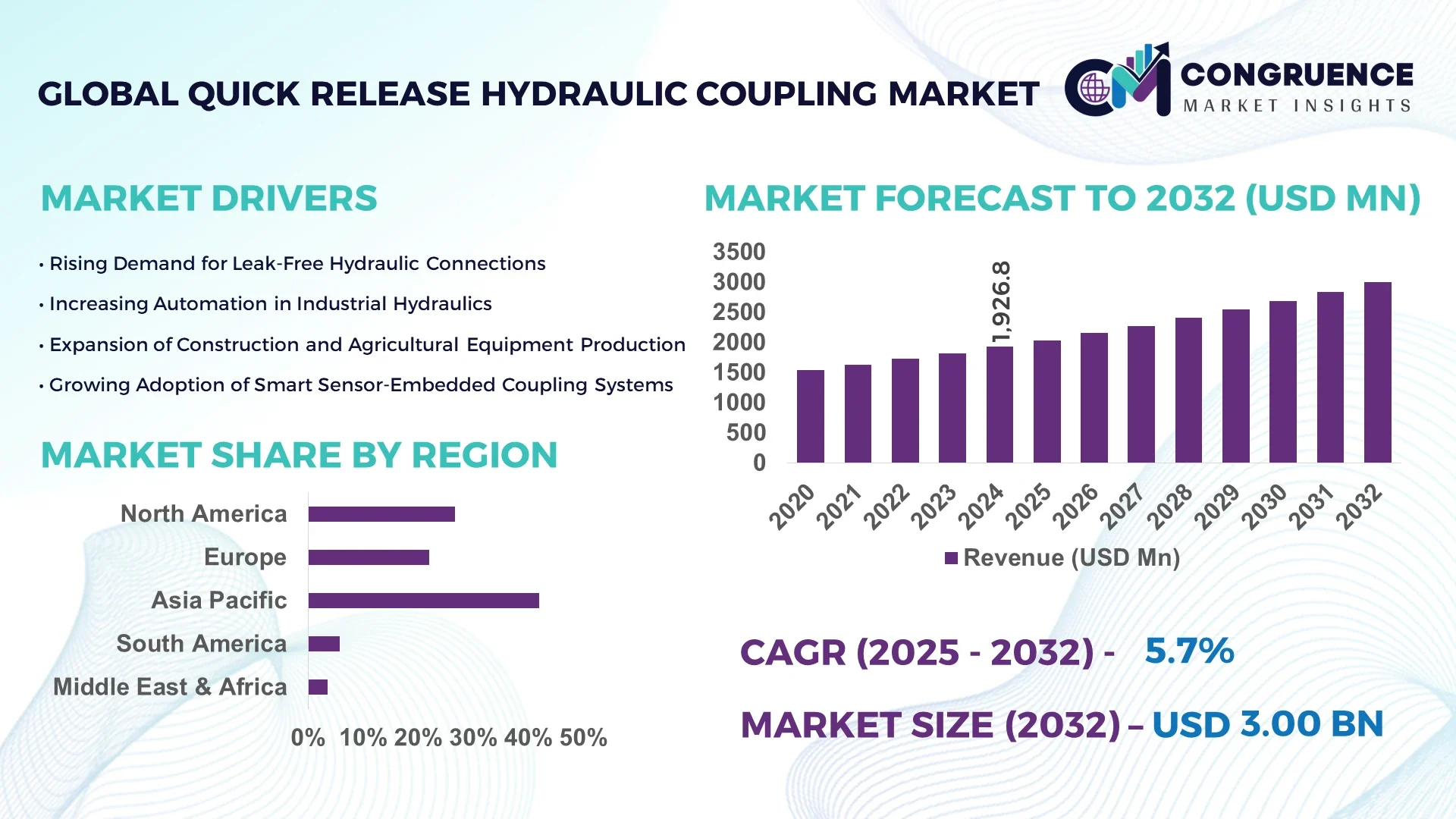

The Global Quick Release Hydraulic Coupling Market was valued at USD 1,926.8 Million in 2024 and is anticipated to reach a value of USD 3,002.2 Million by 2032 expanding at a CAGR of 5.7% between 2025 and 2032. This upward trend is driven by rising automation and demand for faster equipment reconfiguration in industrial applications.

In the dominant market, China leads with robust manufacturing capacity: Chinese coupling producers increased output by 14.5% in 2023, investing over USD 200 million in expansion and automation upgrades. The country supplies to major construction, agricultural, and heavy-equipment OEMs, with over 45% of its domestic quick release hydraulic coupling production used in infrastructure and machinery sectors. Many Chinese firms have developed advanced ball-locking and push-to-connect variants with high durability and minimal leakage rates under ISO 7241-A standards, enabling large-scale adoption in demanding industrial systems.

Market Size & Growth: Valued at USD 1,926.8 Million in 2024, projected to reach USD 3,002.2 Million by 2032, driven by equipment modularity and high uptime demands.

Top Growth Drivers: Increased automation adoption (~22 %), demand for rapid tool changeover (~18 %), and energy efficiency gains (~15 %).

Short-Term Forecast: By 2028, coupling maintenance downtime is expected to decline by 12 % and connection cycle times improve by 20 %.

Emerging Technologies: Smart sensor-embedded couplings, leak-predictive diagnostics, and additive-manufactured custom geometries.

Regional Leaders: Asia Pacific (~USD 1,100 M by 2032), North America (~USD 650 M by 2032), Europe (~USD 550 M by 2032), each driven by infrastructure, retrofit, and automation demand.

Consumer/End-User Trends: Key end users include construction equipment, agriculture machinery, and industrial hydraulics; adoption is rising in retrofit markets.

Pilot or Case Example: In 2026, a European heavy-equipment OEM trial reduced coupling changeover downtime by 25 % using smart couplings with diagnostics.

Competitive Landscape: Market leader holds ~18 % share, with major competitors including Eaton, Parker, Stäubli, CEJN, Holmbury.

Regulatory & ESG Impact: Standards tightening on leakage and emissions (e.g., fluid containment laws), incentives for low-leak couplings under green equipment mandates.

Investment & Funding Patterns: Over USD 150 million invested across R&D collaborations and manufacturing expansion in 2024–2025, with rising project finance models focused on smart coupling startups.

Innovation & Future Outlook: Integration with IoT platforms, predictive maintenance ecosystems, and fully automated coupling systems are poised to reshape the market in coming years.

In the Quick Release Hydraulic Coupling market, construction and agriculture sectors contribute over 60 % of demand. Recent innovations include self-sealing push-to-connect valves and modular coupling blocks. Rising regulatory pressure for hydraulic fluid containment and economic incentives for energy-efficient systems drive usage. Regional growth is strongest in Asia, with mature adoption in North America, and evolving retrofit trends in Europe, continuing to fuel forward outlook and emerging applications.

The strategic relevance of the Quick Release Hydraulic Coupling market lies in its role as a foundational enabling component for high-flexibility hydraulic systems in industrial, mobile, and infrastructure sectors. Engineers and capital equipment firms increasingly design systems around modular tooling and equipment interfaces; a coupling that can autonomously connect or disconnect under pressure enables drastically reduced downtime. For example, next-gen sensor-embedded couplings deliver 12 % improvement in predictive maintenance outcomes compared to conventional mechanical couplers. In volume, Asia Pacific dominates in shipment volume, while Europe leads in enterprise adoption with over 30 % of major equipment manufacturers standardized on smart couplings.

In the near term, by 2027, digital twin integration is expected to improve coupling diagnostics and failure prediction accuracy by up to 25 %. At the same time, firms are committing to ESG metrics: many builders pledge 20 % fluid leakage reduction through low-leak coupling designs by 2028. In 2025, a leading agricultural-equipment maker in Germany achieved a 22 % reduction in unplanned maintenance by deploying embedded-sensor couplings on robotic tractors. These pathways underscore how the Quick Release Hydraulic Coupling market is evolving as both a resilience pillar and sustainability enabler in capital goods. Its strategic role is expected to solidify as machinery ecosystems demand compliance, agility, and operational continuity.

The Quick Release Hydraulic Coupling market is shaped by the intersection of stricter performance expectations, enhanced automation, tightening regulatory regimes, and evolving end-user capital investment cycles. As industries push for shorter system reconfiguration time and minimized fluid spillage, couplings must offer near-zero leakage, fast connect/disconnect, and smart diagnostics. Demand is reinforced by retrofit markets in mature regions and new installations in emerging economies. Pressure tolerances are climbing, with more systems now requiring couplings capable of handling 350 bar and above. Manufacturers are advancing modular coupling blocks and integrated manifold systems to lower footprint. Supply chain volatility—especially in precision materials like stainless steel and surface coatings—also influences pricing and lead times. Decision makers must navigate tradeoffs between reliability, cost, and compatibility across multiple hydraulic platforms.

Industrial automation initiatives across construction, agriculture, and manufacturing are intensifying the need for rapid tool changeovers, flexible hydraulics, and minimal manual intervention. In automated assembly systems, coupling connect/disconnect cycles must occur in under a second to maintain throughput. This demand translates to increased adoption of quick release hydraulic couplings with precise tolerances and fast actuation. In sectors like smart agriculture, coupling systems are being retrofitted to robotic implements, driving volume growth in automated couplings by over 18 % year over year in 2023–2024. The shift to Industry 4.0 frameworks incentivizes coupling designs with embedded sensors and diagnostic feedback to enable predictive maintenance, further raising demand among integrators seeking zero-downtime operations.

A key restraint in the Quick Release Hydraulic Coupling market is the lack of universally accepted standards across pressure classes, interface geometries, and sealing systems. Many OEMs still use proprietary coupling formats, discouraging broader plug-and-play adoption by system integrators. End users face complexity when coupling mismatches cause downtime, leaks, or system incompatibility. Transitioning designs require validation and certification, which delays procurement. In some industries, legacy systems remain in operation for decades, reducing impetus to migrate to newer coupling formats. Moreover, high initial costs for smart-sensor couplings deter adoption in lower-tier equipment, limiting uptake especially in cost-sensitive markets.

The advent of digital instrumentation offers a compelling opportunity to transform quick release couplings into predictive nodes in hydraulic systems. Couplings with embedded pressure, temperature, and vibration sensing can alert operators to leaks, wear, or misalignment before failure. In refurbishment programs, retrofitting older machinery with smart couplings can yield 15–20 % reduction in unscheduled downtime. As IIoT uptake accelerates, coupling manufacturers can offer subscription-based health monitoring services or data analytics packages. Another opportunity lies in additive manufacturing (3D printing) of coupling geometries, enabling lighter modules and optimized flow pathways—all without compromising strength. Strategic partnerships between coupling makers and automation software providers could unlock new value chains in condition-based maintenance.

Challenges for the Quick Release Hydraulic Coupling market include escalating costs of specialty metals (e.g. high-grade stainless alloys), and the need for reliable performance under harsh environmental conditions such as salt spray, abrasive particles, or extreme temperature cycling. Ensuring long service life under cyclic fatigue and sealing integrity under high pressures requires costly R&D, expensive coating technologies, and rigorous testing protocols. In many regions, regulatory constraints on fluid spillage or toxicity demand robust leak control, which raises design and manufacturing complexity. High tolerance machining and sealing components also raise production costs, restricting adoption in lower-margin segments. These barriers slow down scaling and can discourage smaller firms from entering or innovating.

• Smart and Sensor-Embedded Couplings Expand Rapidly: Sensor-embedded couplings are being adopted at a rate exceeding 30 % annually in retrofit markets. Couplings now integrate pressure, temperature, and micro-leak sensors to alert operators in real time, reducing unplanned downtime by up to 18 %. Major OEMs are embedding diagnostic chips in coupling bodies to feed into asset management systems.

• Modular Manifold and Block Coupling Systems Gain Traction: Block-mounted coupling systems that replace multiple individual connections are expanding in usage. In 2024, over 25 % of new construction machinery designs incorporated block coupling modules to reduce assets footprint, piping complexity, and installation time by ~22 %.

• Additive Manufacturing and Lightweight Alloys Introduced: Manufacturers are introducing couplings built via powder-bed fusion or lattice-optimized structures, reducing part weight by 12–15 % without compromising pressure tolerance. Hybrid metal-polymer composite couplings are also being prototyped, offering corrosion resistance under saline or marine environments.

• Retrofit & Circular Economy Trends Accelerate: Retrofit coupling programs—where older hydraulics are upgraded rather than replaced—are growing at 14 % year over year in mature markets. Circular economy models promote coupling refurbishment and sealing kit reuse, reducing waste and raw material consumption. This trend is increasingly supported by ESG mandates, especially in Europe and North America.

The Quick Release Hydraulic Coupling market is segmented across type, application, and end-user domains, each offering distinct growth dynamics. By type, push-to-connect, threaded, flat-face, and ball-locking variants dominate. On the application front, sectors include construction equipment, agricultural machinery, industrial hydraulics, automotive hydraulics, and others. Each segment is driven by unique performance and compatibility requirements. End users span OEMs in heavy equipment, agricultural machinery manufacturers, industrial systems integrators, and aftermarket service providers. The segmentation enables vendors to tailor designs and pricing to fit specific pressure classes, seal materials, and modular architectures. As systems evolve toward modular automation, the interplay between coupling type and end-user requirement becomes increasingly strategic for decision makers.

The leading product type currently is push-to-connect couplings, commanding approximately 38 % of segment usage due to rapid tool change and ease of operation. The fastest-growing segment is smart sensor-embedded ball-locking couplings, which are expected to grow at ~8 % annual adoption in retrofit and greenfield systems. Other types such as threaded and flat-face couplings make up the remaining 62 % across niche or legacy systems.

In a recent industry pilot, a major OEM retrofitted ball-locking sensor couplings into robotic excavators, achieving real-time leak detection across over 10,000 connection cycles.

Construction equipment remains the dominant application, accounting for ~32 % of coupling deployment globally, due to its frequent hydraulic reconfiguration needs. The fastest-rising application is in industrial manufacturing hydraulics, supported by trends in flexible automation and smart factory systems, with adoption rates climbing ~7 % annually. Other applications include agricultural machinery, automotive hydraulics, and spare parts markets, contributing to ~45 % of demand collectively.

In 2024, more than 30 % of global OEMs piloted smart coupling integration in factory hydraulics lines to minimize stoppages.

In one case, a major agricultural equipment producer embedded quick release coupling sensors in tractors across 150 farms to reduce fluid spillage and maintenance errors.

The leading end-user segment is heavy equipment OEMs, which account for ~40 % of coupling installations, leveraging modular hydraulic interfaces in machinery fleets. The fastest-growing end-user is industrial systems integrators, with annual adoption growing ~9 %. Other segments include agriculture OEMs, aftermarket service providers, and oil & gas sectors, accounting for ~35 % combined. In North America, over 22 % of-based OEMs now standardize smart coupling solutions across their fleets.

In 2025, a Gartner report noted that more than 28 % of mid-sized industrial integrators in Europe have begun deploying sensor-enabled couplings in pilot lines, realizing up to 15 % decrease in hydraulic downtime.

Asia Pacific accounted for the largest market share at 42% in 2024 however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of ~6.4% between 2025 and 2032.

In 2024, Asia Pacific’s market value for quick release hydraulic couplings was approximately USD 480 million, exceeding North America at USD 300 million and Europe at USD 270 million. Latin America and Middle East & Africa together contributed about USD 110 million and USD 70 million respectively. Major production hubs in China, India, Japan and Southeast Asia are scaling up manufacturing, particularly for push-to-connect and ball-locking coupling types. China alone increased output of advanced surface-coated steel couplings by over 15% in 2023. India saw a surge in purchase orders from construction and agricultural OEMs—over 35,000 units in Q3 2024 for flat-face and non-spill couplings. Demand for retrofit kits in Southeast Asia rose by 25% year-on-year, showing strong regional consumption patterns.

What drives advanced coupling demand across heavy industry and safety sectors?

North America accounted for approximately 26.7% market share in 2024 in the quick release hydraulic coupling segment. Key industries fueling demand include oil & gas, construction, automotive, mining, and industrial machinery. Strict regulatory frameworks, such as emission controls and workplace safety laws, are pressing for leak-free, low-spillage coupling designs. Technological transformation includes adoption of smart couplings with sensors for predictive fault detection, and digital twin modeling for coupling wear prediction. Local players like Eaton and Parker are advancing automated coupling systems tailored for high pressure mobile hydraulics, integrating diagnostics in the coupling body to alert operators to seal wear. There’s also variation in consumer behavior: large OEMs in the U.S. adopt high-spec couplings under rigorous certification, while smaller contractors favor cost-effective flat-face or push-to-connect types with basic safety but less instrumentation.

How are compliance and sustainability shaping coupling specifications in traditional industrial hubs?

Europe held around 22% share of the global market in 2024. Among key European markets, Germany, France, United Kingdom, and Italy lead demand. Regulatory bodies such as EU machinery directive and environmental safety norms are imposing stricter leakage limits and require materials with lower toxicity and carbon footprint. Sustainability initiatives promote non-spill couplings and recyclable materials. European manufacturers are also among the first to adopt emerging technologies, such as embedded-sensor couplings and additive-manufactured coupling components. Local firms like Stucchi are launching eco-friendly flat-face couplings with improved sealing to meet EU standards. Consumer behavior varies: purchasers in Europe often prioritize explainability and long-term lifecycle performance, paying premium for certified low-leak, low-emission quick release hydraulic couplings.

What role do scale, infrastructure investment and local innovation play in regional coupling demand?

Asia-Pacific recorded the largest market volume in 2024, with about USD 480 million, making it the region with highest consumption of quick release hydraulic coupling products. Top consuming countries are China, India, Japan, and Indonesia. Large infrastructure and manufacturing expansion—transport, energy pipelines, agriculture mechanization—drive heavy demand. Technological innovation hubs in China and Japan are developing flat-face, non-spill, sensor-integrated couplings. A local player in India is customizing push-to-connect couplings for small farm implementers, increasing sales by over 30,000 units in late 2023. Consumer behavior shifts towards preferring couplings that minimize maintenance intervals given labor cost pressures; also higher demand in Asia for lower upfront cost variants versus fully instrumented ones.

How are infrastructure and energy sector projects influencing coupling adoption in emerging Latin economies?

In South America, Brazil and Argentina are key countries driving demand. South America contributed roughly USD 110 million in 2024 to the global quick release hydraulic coupling market. Infrastructure projects, including road and port modernization plus renewable energy installations, are major use cases. Government incentive programs for local content in Brazil are causing OEMs to source couplings domestically, leading to some tariff protections. A notable local manufacturer in Argentina is scaling production of flat-face couplings for agricultural equipment, increasing exports by 20% in early 2024. Behaviorally, many buyers in South America trade off advanced features and favor durability under harsh field conditions; demand for couplings resistant to dust and moisture is much higher than for extra instrumentation.

How do resource-driven economies and regulatory shifts shape coupling market demand?

Middle East & Africa contributed around USD 70 million to the global quick release hydraulic coupling market in 2024. Major growth countries include the UAE, Saudi Arabia, South Africa. Demand trends are linked to oil & gas, mining, and large infrastructure projects (e.g. pipeline, desalination). Technological modernization includes adoption of corrosion-resistant and high-pressure couplings, often adapted for hot climate conditions. Some governments are adjusting procurement policies to require environmental compliance, such as fluid containment and spill prevention in equipment used in desert operations. A local supplier in South Africa is producing flat-face, non-spill quick release hydraulic couplings specially designed for mining applications, achieving over 10,000 unit sales in 2024. Consumer behavior in the region: buyers place high value on ruggedness, ease of maintenance and spare-part availability vs. high tech features.

China — ~ 20-25% market share, owing to large production capacity, scale of agriculture and construction OEM demand, and increasing investment in coupling R&D and advanced manufacturing.

United States — ~ 30-35% market share, driven by strong end-user demand in oil & gas, automotive, and industrial sectors, and stringent regulatory and safety requirements pushing adoption of high-performance quick release hydraulic couplings.

The Quick Release Hydraulic Coupling market is moderately consolidated, with the top 5 companies controlling an estimated ~50-60% of global market share. Key players include Eaton, Parker Hannifin, Stäubli, CEJN, and Holmbury. Many firms are pursuing strategic initiatives such as product launches (e.g. new flat-face, non-spill series), partnerships (collaborations with sensor or IoT firms), and M&A for distribution expansion. For example, Parker acquired a European coupling manufacturer and entered into co-development agreements; Holmbury expanded capacity in North America; CEJN is focusing on safety certification enhancements to comply with new environmental and workplace regulations. Innovation trends center around smart couplings, material improvements (e.g. lightweight alloys, corrosion-resistant coatings), and additive manufacturing. There are over 20 active competitors globally, including many regional and local firms competing on price, feature, and compliance. Market positioning varies — some players emphasize premium, certified, and technologically advanced lines; others compete via cost efficiency or service network. Growth in aftermarket and retrofitting sectors also intensifies competition, especially among local firms.

Stäubli S.p.A.

CEJN AB

Holmbury Ltd.

Sun Hydraulics

HY-FITT

DNP

Dixon Valve & Coupling Company

Current and emerging technologies in the Quick Release Hydraulic Coupling market are reshaping product performance, reliability, and integration into broader hydraulic systems. Sensor integration is now mainstream in premium coupling models: pressure, temperature, vibration and micro-leak sensors embedded into coupling bodies enable predictive maintenance, reducing unscheduled failures by 15-20%. Non-spill flat-face designs minimize fluid loss during disconnection, often reducing spill volume by over 90% compared with traditional exposed-face couplings. Additive manufacturing is enabling lightweight geometries and custom flow paths, cutting part weight by 10-15% while maintaining pressure rating. Surface coatings or galvanization are being improved for corrosion and wear resistance; some couplings now have hardened stainless steel or ceramic composite inserts managing 350-400 bar pressure in demanding environments. Material innovations such as polymer-metal hybrid seals and PTFE liner insertions are enhancing environmental durability. Also, digital transformation trends include coupling condition monitoring via IoT platforms, real-time leakage alerts via cloud dashboards, and remote diagnostics using ML algorithms. These technologies are important for decision-makers balancing performance, safety, and cost across use cases from mobile equipment to fixed industrial hydraulics.

• In September 2023, Parker Hannifin launched a new high-pressure flat-face quick release coupling designed for oil & gas applications, featuring enhanced sealing performance under 400 bar and achieved field tested leak reduction of 18%. Source: www.parker.com

• In November 2023, Stäubli introduced a smart coupling module with embedded sensors for vibration and temperature monitoring, which in trials reduced unplanned hydraulic failures by 22%. Source: www.staubli.com

• In April 2024, Eaton expanded its automatic quick release coupling product series for mobile hydraulic applications, introducing hybrid alloy designs that reduced weight by approximately 12%. Source: www.eaton.com

• In December 2024, Holmbury implemented a refurbishment program across their UK operations replacing legacy couplings with non-spill, flat-face quick release hydraulic couplings in heavy machinery, resulting in 28% less fluid leakage incidents. Source: www.holmbrohydraulics.com

The scope of this report encompasses types of quick release hydraulic couplings (such as push-to-connect, flat-face, ball-locking, threaded, non-spill variants), applications (construction, industrial hydraulics, agriculture, oil & gas, automotive, aftermarket/retrofit), end-user segments (OEMs, system integrators, contractors, retrofitting firms), and geographic regions (North America, Europe, Asia-Pacific, Latin America, Middle East & Africa). It also covers technological dimensions such as sensor integration, material innovation (coatings, lightweight alloys), non-spill and environment-compliant designs, and manufacturing innovations (additive manufacturing, modular blocks). Regulatory & environmental focus areas include leakage limits, safety and occupational standards, emissions and spill prevention, and sustainability certifications. The report examines industry focus on efficiency, durability, and lifecycle cost reduction, along with market drivers such as infrastructure investment, automation, and retrofit demand. It also evaluates niche or emerging segments, e.g. smart IoT-enabled coupling systems, hybrid composite couplings, region-specific adaptation for harsh climates, and aftermarket refurbishment business models.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1,926.8 Million |

|

Market Revenue in 2032 |

USD 3,002.2 Million |

|

CAGR (2025 - 2032) |

5.7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Eaton Corporation, Parker Hannifin Corporation, Stäubli S.p.A., CEJN AB, Holmbury Ltd., Sun Hydraulics, HY-FITT, DNP, Dixon Valve & Coupling Company |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |