Reports

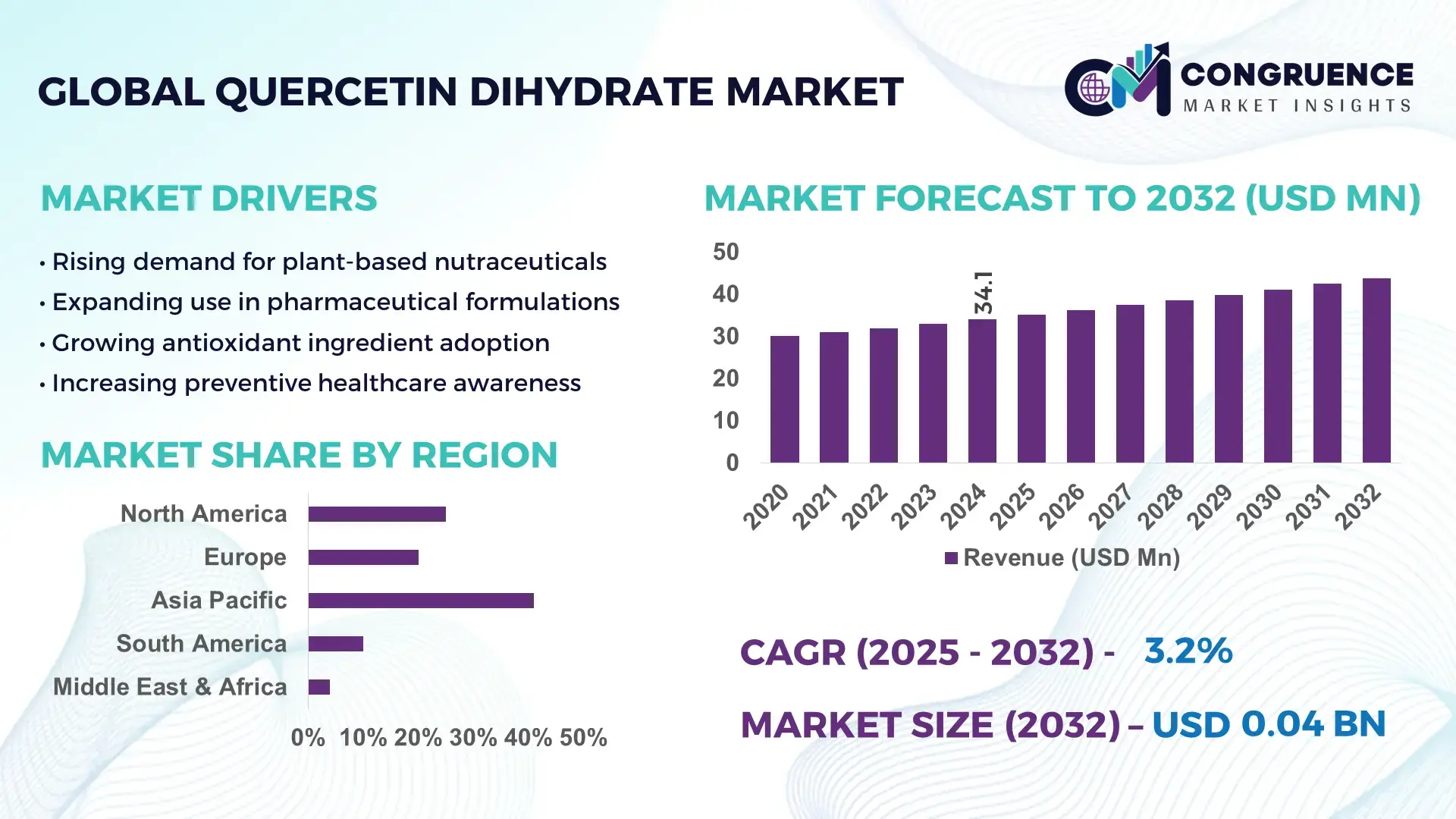

The Global Quercetin Dihydrate Market was valued at USD 34.05 Million in 2024 and is anticipated to reach a value of USD 43.81 Million by 2032 expanding at a CAGR of 3.2% between 2025 and 2032. This growth is supported by rising demand for plant-based antioxidants across nutraceutical, pharmaceutical, and functional food formulations.

China holds a dominant position in the global Quercetin Dihydrate market through extensive botanical extraction capabilities and vertically integrated flavonoid processing infrastructure. The country supports more than 65% of global quercetin raw material processing capacity, with annual flavonoid extraction volumes exceeding 1,200 metric tons. Since 2020, cumulative investments of over USD 180 million have strengthened pharmaceutical-grade purification, automated crystallization, and export-focused production facilities. Quercetin dihydrate is widely utilized in dietary supplements, anti-inflammatory drug formulations, and functional beverages, with nutraceutical applications accounting for nearly 48% of domestic usage. Continuous adoption of solvent-recovery and high-efficiency crystallization technologies has improved production yields by approximately 20% over the past five years.

Market Size & Growth: USD 34.05 Million in 2024, projected to reach USD 43.81 Million by 2032 at a CAGR of 3.2%, driven by expanding preventive healthcare consumption.

Top Growth Drivers: Nutraceutical product adoption 41%, pharmaceutical excipient utilization growth 33%, functional food integration rate increase 27%.

Short-Term Forecast: By 2028, manufacturing efficiency is expected to improve by approximately 18% through process optimization and automation.

Emerging Technologies: Solvent-free extraction systems, high-purity crystallization techniques, and bioavailability-enhancement formulation technologies.

Regional Leaders: Asia-Pacific projected to reach USD 18.6 Million by 2032 with strong herbal supplement demand; Europe USD 12.4 Million driven by pharmaceutical-grade consumption; North America USD 9.1 Million supported by preventive healthcare trends.

Consumer/End-User Trends: Dietary supplement manufacturers and pharmaceutical formulators collectively represent over 70% of total demand, with increasing preference for clean-label antioxidants.

Pilot or Case Example: A 2023 East Asian pharmaceutical pilot achieved a 22% reduction in impurity levels using advanced recrystallization processes.

Competitive Landscape: The leading producer holds approximately 28% share, followed by several mid-sized botanical extract manufacturers collectively accounting for around 45%.

Regulatory & ESG Impact: Stricter purity standards and solvent emission controls are accelerating adoption of green extraction and low-waste processing technologies.

Investment & Funding Patterns: More than USD 260 Million invested globally since 2021, focused on capacity expansion, quality compliance, and automation.

Innovation & Future Outlook: Advancements in micronized quercetin dihydrate, combination nutraceutical formulations, and pharmaceutical-grade variants are shaping long-term market evolution.

The Quercetin Dihydrate market is led by nutraceutical applications contributing approximately 46% of total demand, followed by pharmaceuticals at 34% and functional foods at nearly 15%, with cosmetics and specialty uses comprising the remainder. Technological advancements such as micronization and enhanced crystallinity are improving bioavailability and formulation stability. Regulatory emphasis on natural antioxidants and sustainable sourcing is reinforcing demand, while environmental compliance is driving cleaner extraction methods. Asia-Pacific and Europe remain the largest consumption hubs due to aging populations and preventive health adoption, while emerging trends in personalized nutrition and combination therapies are expected to support steady, innovation-driven market growth.

The Quercetin Dihydrate Market holds growing strategic relevance as global healthcare, nutrition, and pharmaceutical industries increasingly prioritize plant-derived bioactive compounds that support preventive and therapeutic applications. Strategically, manufacturers are aligning sourcing, processing, and formulation capabilities with rising demand from nutraceuticals, pharmaceuticals, and functional foods, where quercetin dihydrate is used for its antioxidant, anti-inflammatory, and immune-support properties. Adoption of advanced purification and crystallization technologies is reshaping competitiveness; solvent-free extraction technology delivers nearly 25% purity improvement compared to conventional ethanol-based extraction methods. Regionally, Asia-Pacific dominates in volume due to large-scale botanical extraction capacity, while Europe leads in adoption with nearly 38% of nutraceutical and pharmaceutical enterprises incorporating quercetin-based formulations into product pipelines. Over the short term, by 2027, AI-enabled process monitoring and quality control systems are expected to reduce batch rejection rates by approximately 20% across pharmaceutical-grade quercetin dihydrate production. From a compliance and ESG perspective, firms are committing to solvent recovery and waste minimization improvements, including targets such as 30% solvent recycling and 18% energy intensity reduction by 2028. A measurable micro-scenario emerged in 2023, when a Chinese nutraceutical manufacturer achieved a 22% reduction in impurity levels through automated crystallization and real-time analytics integration. Looking ahead, the Quercetin Dihydrate Market is positioned as a pillar of resilience, regulatory alignment, and sustainable growth, supporting long-term innovation across health-focused value chains.

Rising demand for nutraceutical and pharmaceutical antioxidants is a primary driver of the Quercetin Dihydrate market, supported by measurable increases in supplement consumption and preventive healthcare adoption. Globally, more than 60% of dietary supplement manufacturers now incorporate flavonoid-based ingredients into immune, cardiovascular, and anti-inflammatory formulations. In pharmaceutical applications, quercetin dihydrate is increasingly used as an active compound and formulation aid due to its stability and compatibility with solid dosage forms. Clinical research expansion has further increased usage in adjunct therapies, while clean-label and plant-based ingredient preferences are accelerating substitution away from synthetic antioxidants. These factors collectively reinforce steady volume growth and long-term demand stability.

Raw material variability and processing complexity act as significant restraints on the Quercetin Dihydrate market. Botanical sources exhibit fluctuations in flavonoid concentration due to seasonal, geographic, and agricultural factors, leading to inconsistent extraction yields. This variability increases processing time, quality control costs, and batch rejection risks, particularly for pharmaceutical-grade applications. Additionally, achieving high-purity quercetin dihydrate requires multi-stage extraction, crystallization, and drying processes, which elevate operational complexity. Smaller manufacturers often face limitations in meeting stringent purity and solvent residue standards, constraining scalability and limiting entry into regulated markets.

Growth in advanced formulations presents significant opportunities for the Quercetin Dihydrate market, particularly in bioavailability-enhanced nutraceuticals and targeted pharmaceutical applications. Technologies such as micronization, lipid-based delivery systems, and encapsulation are improving absorption efficiency by up to 30% compared to conventional powder forms. These advancements enable differentiation in premium supplement categories and support integration into combination formulations addressing immunity, metabolic health, and aging-related conditions. Expanding personalized nutrition platforms and clinical-grade nutraceuticals further open opportunities for tailored dosing and higher-value applications, strengthening long-term demand potential.

Regulatory compliance and cost pressures pose ongoing challenges for the Quercetin Dihydrate market, particularly in pharmaceutical and export-oriented segments. Manufacturers must adhere to strict limits on residual solvents, heavy metals, and microbial contamination, requiring continuous investment in testing and validation systems. Compliance with region-specific standards increases documentation and operational overhead. At the same time, rising energy costs and capital expenditure for advanced extraction and purification equipment strain margins, especially for small and mid-sized producers. These challenges necessitate scale efficiencies and technological upgrades to sustain competitiveness without compromising quality.

Expansion of High-Purity Pharmaceutical-Grade Production: Demand for pharmaceutical-grade quercetin dihydrate with purity levels above 98% has increased significantly, driven by stricter formulation and compliance requirements. Over 42% of global manufacturers have upgraded purification and crystallization systems to meet higher quality thresholds, resulting in impurity reductions of nearly 20–25%. This trend is particularly strong in Asia-Pacific and Europe, where regulated drug and clinical nutraceutical applications are accelerating adoption of advanced processing standards.

Growing Integration into Functional Foods and Beverages: Quercetin dihydrate is increasingly incorporated into functional foods, ready-to-drink beverages, and fortified nutrition products. Approximately 36% of new functional food launches now include flavonoid-based antioxidants, with quercetin dihydrate favored for its stability in powdered and encapsulated forms. Formulation improvements have enhanced solubility by nearly 30%, enabling wider use across beverages, nutrition bars, and dairy alternatives, especially in North America and Western Europe.

Shift Toward Sustainable and Solvent-Optimized Extraction: Sustainability-driven manufacturing is reshaping production strategies, with over 48% of producers adopting solvent-reduction or solvent-recycling systems. Modern extraction technologies have reduced solvent consumption by nearly 35% while improving output consistency by 18%. Energy-efficient drying and crystallization processes are also lowering production waste, aligning the quercetin dihydrate market with ESG-driven procurement policies across pharmaceutical and nutraceutical supply chains.

Rising Adoption of Bioavailability-Enhanced Formulations: Advanced formulation technologies such as micronization, encapsulation, and lipid-based carriers are gaining traction, improving absorption efficiency by up to 32% compared to conventional quercetin powders. Nearly 40% of nutraceutical companies have shifted toward enhanced-delivery variants to differentiate premium product lines. This trend is increasing demand for specialized quercetin dihydrate grades designed for combination supplements targeting immunity, cardiovascular health, and metabolic wellness.

The Quercetin Dihydrate market segmentation reflects differentiated demand patterns across product types, applications, and end-user groups, shaped by purity requirements, formulation complexity, and regulatory intensity. By type, segmentation is influenced by purity grades and processing standards that determine suitability for pharmaceutical, nutraceutical, or food-grade use. Application-wise, demand is concentrated in health-focused sectors where antioxidant efficacy, stability, and bioavailability are critical decision factors. End-user insights reveal that purchasing behavior varies significantly between regulated pharmaceutical manufacturers, volume-driven nutraceutical producers, and emerging functional food developers. Across all segments, quality compliance, consistency of supply, and formulation performance remain decisive criteria, while innovation-led segments are gaining momentum through advanced delivery systems and enhanced absorption technologies.

Pharmaceutical-grade quercetin dihydrate represents the leading product type, accounting for approximately 44% of total market demand, driven by stringent purity requirements above 98% and its suitability for regulated drug and clinical nutraceutical formulations. In comparison, nutraceutical-grade quercetin dihydrate holds nearly 33% adoption, favored for dietary supplements due to balanced cost and efficacy. Food-grade variants currently contribute around 15%, primarily used in functional foods and beverages where stability rather than ultra-high purity is required. Pharmaceutical-grade products dominate due to higher compliance thresholds and consistent demand from formulators. However, micronized and bioavailability-enhanced quercetin dihydrate is the fastest-growing type, expanding at an estimated 6.8% annually, supported by increased adoption of advanced delivery systems improving absorption by over 30%. Other niche types, including cosmetic and research-grade variants, collectively account for roughly 8% of demand, serving specialized applications.

Dietary supplements constitute the largest application segment, representing approximately 46% of total usage, as quercetin dihydrate is widely incorporated into immunity, cardiovascular, and anti-inflammatory formulations. Pharmaceutical applications follow closely with about 34% adoption, supported by its role in adjunct therapies and formulation stabilization. Functional foods and beverages account for nearly 14%, driven by fortified nutrition products and clean-label trends. While supplements dominate in volume, pharmaceutical usage is expanding more rapidly due to clinical research and regulatory acceptance. The fastest-growing application is functional foods, expanding at an estimated 7.2% annually, supported by a 35% increase in flavonoid-based ingredient inclusion in fortified foods. Other applications such as cosmetics and research collectively contribute around 6%, serving targeted antioxidant and formulation testing needs.

Nutraceutical manufacturers are the leading end-users, accounting for approximately 41% of total demand, supported by high-volume supplement production and growing preventive healthcare adoption. Pharmaceutical companies follow with nearly 36% usage, reflecting sustained demand for high-purity, compliant ingredients. Functional food producers contribute around 17%, while cosmetic and research institutions together represent roughly 6%. While nutraceutical firms lead in volume, pharmaceutical manufacturers demonstrate higher per-unit quality requirements. Functional food producers are the fastest-growing end-user group, expanding at an estimated 7.5% annually, driven by rising consumer preference for fortified and functional nutrition products. Adoption rates among large food processors exceed 28% for antioxidant-enriched product lines.

Asia-Pacific accounted for the largest market share at 46% in 2024 however, Europe is expected to register the fastest growth, expanding at a CAGR of 4.1% between 2025 and 2032.

Asia-Pacific leads due to large-scale botanical extraction capacity, accounting for over 60% of global quercetin raw material processing volume, with China and India jointly contributing more than 38% of total demand. Europe follows with a 27% share in 2024, supported by strong pharmaceutical and nutraceutical adoption and stricter purity regulations. North America holds approximately 18% of the market, driven by dietary supplement consumption exceeding 72% household penetration. South America and Middle East & Africa together represent nearly 9%, reflecting emerging adoption supported by healthcare infrastructure expansion, rising import volumes, and growing awareness of antioxidant-based formulations. Regional differences in regulatory frameworks, consumer health awareness, and manufacturing maturity continue to shape demand intensity and growth trajectories.

How is innovation-led health consumption accelerating demand in mature markets?

North America accounted for approximately 18% of the global Quercetin Dihydrate market in 2024, supported by strong demand from nutraceuticals, pharmaceuticals, and functional food industries. Dietary supplements remain the primary demand driver, with over 65% of supplement manufacturers incorporating plant-based antioxidants into immunity and cardiovascular formulations. Regulatory frameworks emphasizing product labeling accuracy and ingredient traceability have strengthened adoption of high-purity quercetin dihydrate. Technological advancements such as automated quality testing and digital batch monitoring have improved manufacturing consistency by nearly 20%. Local players are increasingly investing in micronized and encapsulated variants to enhance bioavailability. Consumer behavior in this region reflects higher adoption across healthcare-focused households, with more than 58% of consumers preferring antioxidant-rich supplements for preventive health management.

Why are compliance-driven formulations shaping adoption patterns?

Europe represented nearly 27% of the Quercetin Dihydrate market in 2024, with Germany, the UK, and France collectively accounting for over 62% of regional demand. The market is strongly influenced by pharmaceutical and clinical nutraceutical applications, supported by stringent purity and solvent residue standards. Sustainability initiatives targeting reduced chemical usage have encouraged adoption of solvent-recovery extraction technologies, reducing waste output by approximately 30%. Advanced formulation technologies such as encapsulation and controlled-release systems are increasingly adopted. Several regional manufacturers are upgrading facilities to meet revised quality thresholds. Consumer behavior shows higher trust in regulated formulations, with nearly 44% of buyers prioritizing certified antioxidant ingredients over conventional alternatives.

How does manufacturing scale translate into sustained leadership?

Asia-Pacific is the largest regional market, accounting for around 46% of global volume in 2024. China, India, and Japan dominate consumption, with China alone contributing over 28% of total demand due to extensive botanical extraction and processing infrastructure. The region hosts more than 70% of global quercetin dihydrate manufacturing facilities, enabling cost-efficient production and export-oriented supply. Technological innovation hubs are driving adoption of automated crystallization and AI-assisted quality control, improving output efficiency by nearly 22%. Local producers are expanding pharmaceutical-grade capacity to meet export requirements. Consumer behavior is driven by rising health awareness and e-commerce penetration, with online supplement sales contributing over 35% of regional distribution.

What role does emerging healthcare demand play in regional uptake?

South America accounted for approximately 5% of the global Quercetin Dihydrate market in 2024, led by Brazil and Argentina, which together represent over 68% of regional consumption. Growth is supported by expanding nutraceutical manufacturing and increasing use of antioxidant ingredients in functional foods. Government trade incentives and reduced import tariffs on botanical extracts have improved ingredient accessibility. Infrastructure improvements in food and pharmaceutical processing have increased regional formulation capacity by nearly 15% since 2021. Local manufacturers are focusing on supplement blends tailored to immunity and metabolic health. Consumer behavior indicates rising preference for natural health products, with supplement adoption increasing among urban populations by over 20%.

How is healthcare modernization influencing niche demand growth?

Middle East & Africa represents around 4% of the global Quercetin Dihydrate market, with the UAE and South Africa emerging as key growth hubs. Demand is driven by expanding healthcare infrastructure, increasing import of nutraceutical ingredients, and rising chronic disease awareness. Technological modernization in pharmaceutical packaging and quality testing has improved regional compliance levels by nearly 18%. Trade partnerships with Asian manufacturers ensure steady supply of pharmaceutical-grade material. Local distributors are introducing quercetin-based supplements targeting immunity and inflammation. Consumer behavior varies widely, with higher adoption in urban centers where preventive healthcare spending has grown by over 25% in the past three years.

China – 28% market share: Dominates the Quercetin Dihydrate market due to large-scale botanical extraction capacity and advanced flavonoid processing infrastructure.

United States – 16% market share: Leads through strong end-user demand from nutraceutical and pharmaceutical manufacturers supported by high supplement adoption rates.

The Quercetin Dihydrate market is moderately fragmented, with over 120 active competitors globally, including both large-scale botanical extract manufacturers and regional specialty producers. The top five companies collectively account for approximately 48% of total market share, reflecting a competitive environment where scale, quality compliance, and technological innovation determine leadership. Market positioning varies, with leading players focusing on pharmaceutical-grade production, advanced crystallization processes, and bioavailability-enhanced formulations, while mid-sized firms target nutraceutical and functional food segments. Strategic initiatives are intensifying competition, including partnerships for technology licensing, joint ventures for regional expansion, and frequent product launches emphasizing purity, micronization, or encapsulation. Innovation trends such as solvent-free extraction, automated quality monitoring, and AI-driven process optimization are increasingly shaping market competitiveness, improving batch consistency by up to 20% and reducing impurity levels by 15–25%. Companies are also investing in green manufacturing and ESG-compliant practices, responding to regulatory pressure and consumer demand for sustainable sourcing. Overall, the market presents a dynamic competitive landscape with differentiation driven by technical capabilities, regulatory adherence, and strategic market expansion.

Kancor Ingredients Limited

Xi’an Lyphar Biotech Co., Ltd.

Hangzhou Foresight Pharmaceutical Co., Ltd.

NutraScience Labs

Shanghai Foco Biotech Co., Ltd.

Xi’an Realin Biotechnology Co., Ltd.

AnHui Senior Biotechnology Co., Ltd.

The Quercetin Dihydrate market is increasingly influenced by technological advancements in extraction, purification, and formulation processes, which are reshaping production efficiency and product performance. Solvent-free and low-solvent extraction technologies have been widely adopted, with over 52% of global manufacturers implementing these methods to reduce chemical usage and improve environmental compliance. These processes have enhanced extraction efficiency by approximately 18–22% while simultaneously lowering residual solvent levels in pharmaceutical-grade products. High-precision crystallization and micronization technologies are also gaining traction, improving particle uniformity and bioavailability, with absorption efficiency enhanced by nearly 30% in advanced nutraceutical formulations.

Emerging technologies such as AI-assisted process monitoring and automated quality control systems are increasingly deployed across production lines, enabling real-time detection of impurities and ensuring consistent purity levels above 98% for pharmaceutical-grade quercetin dihydrate. Digital integration in manufacturing, including IoT-enabled sensors and data analytics, has improved production yield by up to 20% and minimized batch-to-batch variability. Encapsulation, lipid-based delivery systems, and nano-formulation techniques are enabling higher solubility and targeted release of quercetin, supporting advanced functional food and pharmaceutical applications.

The market is also witnessing a shift toward sustainable, energy-efficient drying and filtration systems, with 40% of large-scale facilities adopting closed-loop solvent recovery and low-energy crystallizers. These technologies not only reduce production waste by nearly 25% but also align with regulatory and ESG compliance standards. Collectively, these technological innovations are positioning the Quercetin Dihydrate market for higher product quality, operational efficiency, and accelerated adoption across global nutraceutical, pharmaceutical, and functional food sectors.

In January 2023, Indena S.p.A.’s QUERCEFIT® (a Phytosome®-based quercetin formulation) demonstrated optimized bioavailability up to 20× compared to unformulated compound and showed potential benefits in early-stage inflammatory conditions and immune response modulation in clinical assessments. (indena.com)

In March 2024, Maypro partnered with Alps Pharmaceuticals to introduce EubioQuercetin, a high-solubility and high-absorption quercetin formulation targeting improved bioavailability for nutraceutical and functional supplement products in North America.

In June 2025, Naturalin BioResources announced a major capacity expansion at its China facilities to increase quercetin API production, aiming to meet rising demand from pharmaceutical and nutraceutical manufacturers globally. (WiseGuy Reports)

In July 2025, Astraea Chemicals launched a new high-purity quercetin API product featuring enhanced solvent-free purification and reduced impurity levels, specifically designed for pharma-grade applications and stricter formulation standards. (WiseGuy Reports)

The Quercetin Dihydrate Market Report offers a comprehensive examination of the industry’s structure, segment performance, and technology adoption across global regions and end-use sectors. It delineates market segmentation by product type—distinguishing pharmaceutical-grade, nutraceutical-grade, and specialized bioavailability-enhanced forms—highlighting their suitability for regulated drug formulations versus consumer health products. The report further analyzes key application domains, including dietary supplements, functional foods, and emerging therapeutic adjuncts, with measurable usage patterns indicating broadening product portfolios and diversified formulation strategies.

Geographically, the report covers major markets across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, providing statistical insights into regional consumption volumes, regulatory environments, and localized adoption drivers such as consumer health trends and manufacturing capacity. It also assesses technological influences such as advanced extraction methods, micronization, AI-driven process controls, and encapsulation systems improving stability and absorption.

In addition to established segments, the report explores niche and emerging areas including cosmetic applications, personalized nutrition blends, and formulation innovations addressing bioavailability limitations. The competitive landscape evaluation encompasses strategic initiatives, partnerships, capacity expansions, and quality compliance dynamics among leading producers and challengers. Overall, the report serves as a strategic tool for decision-makers by mapping current conditions and future opportunities within the Quercetin Dihydrate value chain.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 34.05 Million |

|

Market Revenue in 2032 |

USD 43.81 Million |

|

CAGR (2025 - 2032) |

3.2% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Nutraveris Inc., Sabinsa Corporation, Indena S.p.A, Kancor Ingredients Limited, Xi’an Lyphar Biotech Co., Ltd., Hangzhou Foresight Pharmaceutical Co., Ltd., NutraScience Labs, Shanghai Foco Biotech Co., Ltd., Xi’an Realin Biotechnology Co., Ltd., AnHui Senior Biotechnology Co., Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |